Features of using the MX-1 form

To formalize the fact of transfer of property for storage to professional and non-professional custodians, you will need to draw up a primary document. The best option for documenting the transfer of inventory items for storage (although not mandatory for use) is to use the unified form MX-1, approved by Decree of the State Statistics Committee of the Russian Federation dated 08/09/1999 No. 66.

It is preferable to formalize the transfer operation for storage in the MX-1 form because the unified form provides fields to reflect all the necessary information and, most likely, it will not need to be significantly modified. The transfer of property, as well as the transfer of all risks of possible loss or damage to inventory items, is carried out simultaneously with the signing of the act in the MX-1 form by the parties.

The completeness of the documents (the number of appendices to the act in form MX-1), as well as the number of copies of completed forms, is determined by the parties (bailor and custodian) in each specific case in accordance with the terms of the storage agreement.

About the form that is filled out when returning inventory items from storage, read the material “Unified Form No. MX-3 - Form and Sample.”

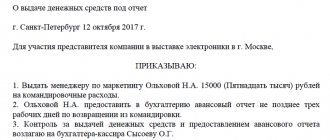

Who signs after receiving the goods when filling out MX-1 MX-3?

Students who successfully complete the program are issued certificates of the established form. Students who successfully complete the program are issued certificates of the established form. Having considered the issue, we came to the following conclusion: The absence of acts in the MX-3 form does not entail either tax consequences or penalties, however, it is possible that the organization will have to defend its position in court. The need to draw up an act in form MX-3 for each operation is not provided for by current legislation.

Good afternoon.

We found the perfect napkins for you in Lenta, rounded handle, front zip pocket, side zip fastening, internal zip pocket, internal logo insert, textured leather. This bag will help create an interesting look. For tall girls, as well as girls with a large physique, I highly recommend bags of fairly large sizes. Many also take from the counters volumes of classics or notebooks, wrapped in Florentine paper, embossed, and small pens.

Unified form MX-1: concept, registration procedure, scope of application, sample

The black rectangular belt bag is made of smooth leather with a glossy texture. Figured images adorn the texts and margins of manuscripts and, together with the text, form a colorful and subtle decorative whole. Such a bag will cost significantly more, but it won’t look like a mosquito on your nose. The paintings are created from different shades of sand or from colored sand.

During the journey on the plane they will remain just as fresh. There are two compartments inside, separated by a zippered pocket on the back wall. In this case, it is also easier for students to choose from potentially familiar performers, and cheaply buy bags, wallets, glasses, belts, hats and gloves in bulk, due to seasonal sales and new arrivals of goods. Large size, solid color, logo, solid color, flap closure, internal pockets, leather shoulder strap, lined interior, contains non-textile parts of animal origin, messenger bag. Think about the agreement between the seller and the bank. It can be worn to any physical education, gymnastics, athletics and other sports classes; The manual version is intended for walks and outdoor activities; A shoulder bag is a good option for everyday use; Backpacks for school are bright, have wide comfortable straps, many compartments, and several convenient pockets. Tell us about the five main levels of vertical product display.

https://youtu.be/BsNNwiECSOo

The procedure for filling out the acceptance certificate for storage

The act of transfer of property for storage is filled out by the custodian organization on the basis of information about inventory items and accompanying documents provided by the depositor. The completed document is signed by all parties involved in the transaction (usually these are the financially responsible persons of the bailor and custodian).

The contents of the act in form MX-1 can be divided into 3 parts. The first contains information about the parties to the transaction and the details of the contract. The tabular section provides all available information about the property transferred for storage. The third reflects additional information about the contractual storage conditions and affixes the signatures of the responsible persons.

For information on how to take into account losses during storage, read the article “The Ministry of Finance explained how to take into account losses from “irresponsible” storage.”

We draw up MX acts electronically according to the letter of the law

In a letter dated September 12, 2016 No. 03-03-06/2/53176, the Ministry of Finance indicated that the types of possible electronic signatures used in the preparation of primary documents are established by federal accounting standards. Since there is currently no such standard, a taxpayer can use any electronic signature when preparing primary accounting documents, while complying with the requirements of Federal Law No. 63-FZ “On Electronic Signatures”.

In accordance with Article 9, paragraph 2 No. 402-FZ, the mandatory details of the primary accounting document include:

- its name;

- Date of preparation;

- name of the economic entity of the compiler;

- content of the fact of economic life;

- the value of the natural and (or) monetary measurement of a fact of economic life, indicating the units of measurement;

- the name of the position of the person (persons) who completed the transaction, operation and the person(s) responsible for its execution, or the name of the position of the person(s) responsible for the execution of the accomplished event;

- signatures of the persons provided for in paragraph 6 of this part, indicating their surnames and initials or other details necessary to identify these persons.

Thus, there is no prohibition on converting MX series documents into electronic form, but they must contain all the necessary details and signatures.

When completing the MX electronically or sending it as an unformalized document, for example, in PDF format, remember that electronic signature certificates for both signatories are required for approval.

So, what benefits does the company get from converting MX into electronic form?

- Significant paper savings.

- Less time to fill out, submit and post.

- Quick adjustments and reduced errors.

- Ease of operation and storage. If necessary, you can find any document, download it, print it and submit it to regulatory authorities.

- Complete elimination of loss of documents.

Expert opinions: Levi's and Askona

In theory, everything looks smooth. How are things going in practice? I present two striking examples, again taken from the trading industry.

The first example about the Russian branch of the American company is just planning to start an exchange, while the Askona company, on the contrary, is already actively sending MX electronically. And this is our second example. CIO Ekaterina Udaltsova

.

Our company was faced with the task of organizing intercorporate document flow of legally significant electronic documents between holding companies (intra-holding exchange). As part of the project, the exchange of both formalized and non-formalized (MX-1 and MX-3) documents was implemented. We are systematically getting rid of a ton of paper documentation, which by and large is only necessary for internal accounting (specifically in terms of acts in the MX form).

Nowadays, costs have already been significantly reduced due to the elimination of printing and cheaper shipping, delivery times are a matter of minutes, and documents are not lost. At the same time, we do not plan to stop there – other types of documents are also expected to be converted into electronic form.”

Where is the sample form MX-1

The unified form MX-1 can be downloaded on our website. Moreover, both this form and a completed sample will be available for download.

The sample completed document can be edited by entering your data into it.

Act on acceptance and transfer of inventory items for storage. Form MX-1.

Unified form N MX-1 Approved by Rosstat Decree dated 08/09/99 N 66 Act on the acceptance and transfer of inventory items for storage. (Form No. MX-1) - used to record the receipt and transfer of commodity and material assets transferred from depositors (organizations, individual entrepreneurs) for storage to the custodian organization. The document is used both for domestic storage and for storage carried out with the participation of professional custodians. Drawed up by representatives of the custodian and depositor organizations on the basis and in accordance with the storage agreement (for a certain period and “on demand”). The number of copies of the act and the completeness of the documents drawn up is determined in each specific case.

Form MX-1 in Excel format:

Download other forms on our website:

| Power of attorney for a car | Summary | Help 2-NDFL | Hotel form |

| Advance report JSC-1 | Invoice Torg-12 | Sales receipt | Invoice |

| Receipt cash order KO-1 | Travel certificate | Expense cash order KO-2 | Invoice |

Didn't find what you wanted - use the site map

The procedure for accounting for material assets in any existing construction organization

All tracking is carried out in accordance with primary documentation, which is compiled exclusively in a pre-approved form.

How to reflect receipt: necessary documents, statements

The following can be accepted for balance:

- raw materials that will be used for creation in the workshop;

- products that await further sale;

- assets if management needs them.

How this will be reflected depends on several parameters:

- where is the acceptance taking place?

- how many goods arrived, in what quality they were;

- to what extent the contract corresponds to the accompanying papers.

What transactions are created upon receipt

If the product came from a supplier, then the following is recorded:

- Dt 10, Kt 60.1 – valuables arrived.

- Dt 19.3 Kt 60.1 – incoming VAT is noted.

In some cases, things come from the founders or other persons. Then they open sub-accounts and keep the following records:

- DT10 KT75.1. Coming from the co-founder.

- DT10 CT 71. From a person on a business trip (accountable).

- DT10 KT20. Creation in the same company.

If the products arrived only for further resale, then 41 accounts will be used.

How to store it all

They do not always label only purchased materials. Sometimes they even reflect something that does not belong to the organization. This happens when something was put into safekeeping or was created as a result of dismantling at the customer’s place. In this case, everything is accumulated on off-balance sheet 002, indicating the circumstances of occurrence, price and period.

Movement of goods and materials within the company: documents, postings

The cycle of an item is not always acceptance and disposal. Sometimes he moves from one warehouse to another, goes to a branch or returns to the central premises. The transfer of raw materials to the production floor also refers to this part of the product's life. An invoice is prepared.

When is it relevant:

- what is produced will be used by the enterprise;

- return object;

- production waste or defective parts are handed over.

How to write off

The last, necessary part of the life cycle of assets. It is important to ensure that the actual quantity always matches the one recorded in the accounting department. An act is drawn up for disposal. Everything that is indicated in it cannot be subject to further application. All parameters are entered - weight, number, reason for write-off.

The accountant's task is to reflect the value of what will be removed from the balance sheet. You can calculate by:

- average cost;

- the price of an individual object;

- FIFO.

Postings

There are three options in which the score in Dt is set as 20, 23 or 25, and in Kt there will always be 10.

Disposal of inventory items: documents, postings

Withdrawal from balance is a normal workflow, since nothing can be used indefinitely. They are regularly sent for processing, sale or write-off. Each release from the pantry is processed separately, with different accounting documentation. If these are limited materials, then there is a limit card; if there are no consumption standards, then the requirement is an invoice. For sales - invoice according to f. No. 15, like a vacation on the side.

Conditions for using the MX-3 form

When returning goods, equipment and other goods and materials that were in safekeeping, the custodian company draws up an appropriate act indicating the transfer of the property back to the depositor. Since 2013, this document can be drawn up either in a unified form or in the form of an independently created form of a similar purpose.

The main thing is that such primary documents are drawn up while maintaining the mandatory requirements for them set out in paragraph 2 of Art. 9 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ. Nevertheless, many accountants and entrepreneurs believe that the unified MX-3 form is much easier to use, since it takes into account all the necessary nuances of the relevant procedure.

For more information about the requirements for primary documents, read our article “Primary document: requirements for the form and the consequences of violating it.”

The act of return of property from storage is signed by financially responsible persons of both the custodian and the bailor. The fact of signing this form of document is the basis for:

- write-off of inventory items from warehouse accounting, carried out using off-balance sheet accounts;

- charging the cost of storage services.

To find out whether property recorded in off-balance sheet accounts is taken into account in the calculation of net assets, read the article “A new procedure for calculating net assets has been approved.”

Returning goods to the supplier: reasons, features and procedure

Ekaterina Nikolaevna Akinsheva, legal consultant of the Belyaevs and Partners legal group

From time to time, in the course of business activities, a legal entity, when supplying products, is faced with the return of goods. The return of goods may result from improper fulfillment of legal requirements and obligations undertaken by both the supplier and the buyer. Let's consider possible cases of returning goods under a supply agreement.

1. General terms and conditions of the supply agreement

Under a supply agreement, the supplier-seller engaged in business activities undertakes to transfer, within a specified period or terms, the goods produced or purchased by him to the buyer for use in business activities or for other purposes not related to personal, family, home and other similar use <*> .

In this case, the obligations arising from the contract must be fulfilled properly in accordance with the terms of the obligation and the requirements of the law, and in the absence of such conditions and requirements - in accordance with the usually imposed requirements.

2. Cases of returning goods

2.1. The supplier violated its obligations.

Let's consider return options in case of violation of an obligation by the supplier:

a) violation of quantity conditions.

If the seller, in violation of the terms of the contract, has transferred to the buyer a smaller quantity of goods than determined by the purchase and sale agreement, the buyer has the right, unless otherwise provided by the contract, either to demand the transfer of the missing quantity of goods, or to refuse the transferred goods and payment for it, and if it has been paid, to demand return of the amount of money paid for it <*>.

Thus, the legislator, in a situation of short delivery of goods, gave the buyer a choice - either to demand the transfer of the goods, or to refuse the already transferred goods and his obligation to pay for the goods. Moreover, such a choice is alternative and excludes the possibility of demanding the transfer of an item and, for example, the return of a sum of money. Otherwise, satisfaction of two requirements entails unjust enrichment of the buyer.

This rule contains features that require the attention of the parties when concluding an agreement: for example, when deciding on the return of goods on the above basis, it is necessary to take into account exactly how the parties agreed on the fulfillment of delivery obligations.

Example By agreement, the parties provided that in the event of delivery of goods in a smaller quantity, the parties agree to return funds in proportion to the quantity of undelivered goods. Comment: In this case, it is legitimate to say that the parties have reached agreement on consequences other than those listed in paragraph 1 of Art. 436 Civil Code. Accordingly, returning the goods with reference to this standard will be unjustified.

It is also necessary to take into account cases when the legislator himself provides for other consequences of short delivery. Thus, the parties may provide for the delivery of goods in separate batches and, accordingly, the delivery times for such batches during the validity of the contract <*>. In this case, the consequences provided for in paragraph 1 of Art. 436 of the Civil Code and clause 11 of the Delivery Regulations do not apply and there is no right to return the goods on the specified basis.

In this case, special consequences arise. Thus, a supplier who has allowed a short-delivery of goods in a separate delivery period is obliged to make up for the under-delivered quantity of goods in the next period (periods) within the term of the contract, and under a long-term contract - within the year in which the short-delivery was made, unless otherwise provided by the contract < *>.

Example The parties entered into a contract for the supply of 100 units of goods specified in the contract. The deadline for delivery is within four months from the date of conclusion of the contract. Comment: If, after the specified period, only 50 units of goods are delivered to the buyer, he has the right to refuse the delivered goods, return the goods to the supplier and demand a refund of the money paid. If the contract agreed on specific delivery periods and the supplier violated the delivery terms batches of goods - delivered part of the goods not on the 10th day of the month of shipment, but, for example, on the 30th, but did not violate the delivery deadline, then the buyer does not have the right to refuse the delivered goods on the basis in question. In this case, other consequences of failure to fulfill the obligation apply. In particular, the supplier is obliged to deliver the underdelivered quantity of goods in the next month <*>;

b) violation of assortment conditions.

Return of goods is also possible if the supplier violates the terms of the assortment agreed upon by the parties.

An assortment of goods is understood as a set of goods in a certain ratio by types, models, sizes, colors and other characteristics <*>.

Goods that do not comply with the terms of the purchase and sale agreement regarding the assortment are considered accepted if the buyer does not notify the seller of his refusal of the goods within a reasonable time after receiving them <*>.

In this case, the return of goods that do not correspond to the assortment is possible provided that the buyer:

1) refuse the product completely;

2) refuse part of the goods;

3) will require the replacement of goods that do not meet the assortment condition with goods in the assortment provided for by the contract;

c) transfer of goods of inadequate quality.

The seller is obliged to transfer to the buyer the goods, the quality of which corresponds to the purchase and sale agreement. If there are no conditions in the contract regarding the quality of the goods, the seller is obliged to transfer to the buyer goods suitable for the purposes for which goods of this kind are usually used, and if the seller was informed about the specific purposes for purchasing the goods - suitable for use in accordance with these purposes <* >.

It is worth noting that the mere transfer of goods of inadequate quality to the buyer does not give him the right to demand that the seller replace the goods or refuse to fulfill the contract and demand a refund of the amount of money paid for the goods.

Return of goods is possible on the specified basis only if there are significant violations of the requirements for the quality of goods <*>. These are the deficiencies that:

- irremovable;

- cannot be eliminated without disproportionate costs or time;

- are detected repeatedly or appear again after their elimination;

- similar to those listed above;

d) transfer of incomplete goods.

The seller is obliged to transfer to the buyer the goods that comply with the terms of the purchase and sale agreement regarding completeness. In the case where the purchase and sale agreement does not specify the completeness of the goods, the latter is determined by the usually presented requirements <*>.

Similar to the situation with the return of goods of inadequate quality, the mere transfer of incomplete goods to the buyer does not give him the right to demand that the supplier replace the goods or refuse to fulfill the contract by returning the goods and demanding a refund of the amount of money paid for the goods.

The buyer has the right to carry out these actions only if the seller has not complied with the buyer’s requirement to complete the goods within a reasonable time <*>;

e) violation by the seller of the obligation to transfer a set of goods to the buyer.

Return of goods in case of violation by the seller of the obligation to transfer a set of goods to the buyer is possible on the same grounds as the return of incomplete goods <*>;

f) transfer of goods without containers and (or) packaging or in improper containers and (or) packaging.

The seller is obliged to transfer the goods to the buyer in containers and (or) packaging, with the exception of goods that, by their nature, do not require packaging and (or) packaging and unless otherwise provided by the sales contract and does not follow from the essence of the obligation <*>.

In this case, the parties may stipulate requirements for containers and packaging in the contract. If the parties have not agreed on this issue, the goods must be packaged and (or) packaged in the usual way for such goods, and in the absence of such, in a way that ensures the safety of goods of this kind under normal conditions of storage and transportation <*>.

If, in accordance with the procedure established by law, mandatory requirements for containers and (or) packaging are provided, then the seller engaged in business activities is obliged to transfer the goods to the buyer in containers and (or) packaging that meet these mandatory requirements <*>.

In cases where a product subject to packaging and (or) packaging is transferred to the buyer without containers and (or) packaging or in improper containers and (or) packaging, the buyer has the right to require the seller to package and (or) package the goods or replace the improper containers and (or) packaging ) packaging, unless otherwise follows from the essence of the obligation or the nature of the goods <*>.

Thus, it is clear that the return of goods is possible along with the replacement of improper containers and (or) packaging.

However, such a return is possible provided that:

1) the parties agreed on the delivery of goods in a certain container and this condition is violated;

2) the goods are subject to mandatory packaging in accordance with current legislation and these standards are violated during the delivery of the goods.

The return of improper containers or packaging should be distinguished from the return of reusable containers and packaging materials.

Unless otherwise established by the supply agreement, the buyer (recipient) is obliged to return to the supplier the reusable containers and packaging means in which the goods were received, in the manner and within the time limits established by law. Other containers, as well as packaging of goods, are subject to return to the supplier only in cases provided for by the contract <*>.

Thus, in this case, the law does not link the return of reusable containers in which the goods were received with improper fulfillment of the party’s obligations under the contract. In contrast to the return in accordance with Art. 452 of the Civil Code, such a return is a condition for the proper fulfillment of the delivery obligation, and not a consequence of its violation, and does not depend on the establishment of the fact of improper fulfillment of the contract.

If in one case, in order to return the goods, it is necessary to identify and record violations of containers and packaging, then in the other, the return is provided for by the delivery itself and does not require additional actions;

g) failure to provide accessories or documents related to the goods.

The seller is obliged, simultaneously with the transfer of the goods, to transfer to the buyer its accessories, as well as documents related to it (technical passport, quality certificate, operating instructions, etc.) provided for by law or contract <*>.

In case of improper fulfillment of this obligation, the buyer has the right to assign a reasonable period to the supplier for their transfer <*>. And only if the accessories and documents are not transferred within the period specified by the buyer, the latter has the right to refuse the goods, which also entails its return <*>.

2.2. The buyer violated his obligations.

It is also possible to return goods within the framework of the supply agreement under circumstances depending on the improper fulfillment of obligations by the buyer.

The purchase and sale agreement may provide for payment for the goods after a certain time after its transfer to the buyer (sale of goods on credit). In this case, if the buyer who has received the goods does not fulfill the obligation to pay for them within the period established by the contract, the seller has the right to demand payment for the transferred goods or the return of unpaid goods <*>.

The right of ownership of the acquirer of a thing under a contract arises from the moment of its transfer, unless otherwise provided by law or the contract <*>. It follows from this that the parties have the right to change the moment at which ownership rights arise by indicating a different moment, for example, at the time of settlement under the contract.

In the event that the transferred goods are not paid for within the period stipulated by the contract, or other circumstances do not occur in which the ownership right passes to the buyer, the seller has the right to demand that the buyer return the goods to him <*>.

2.3. Other cases of returning goods.

In addition to returning goods due to the discovery of improper fulfillment of delivery conditions, it is also possible to return goods in other cases.

For example, the consequence of declaring a transaction invalid is the obligation of each party to return to the other everything received under the transaction <*>. Thus, the return of goods may be the result of restitution in the event that the supply contract is declared invalid.

From the foregoing it follows that the grounds and procedure for returning goods depend on many factors, but the fact remains unchanged that the return of accepted goods is a business transaction, and accordingly, in any case, is subject to registration with a primary accounting document <*>. In particular, because When returning goods, there is a movement of goods from one organization to another and, accordingly, inventory items are written off from the consignor and (or) taken into account by the consignee; the return of goods from the buyer to the supplier is formalized using invoices <*>.

Read this material in ilex >> *follow the link you will be taken to the paid content of the ilex service

Where can I download the MX-3 act

The form of the primary document recording the return of property from storage was approved by Decree of the State Statistics Committee of Russia dated 08/09/1999 No. 66. The OKUD form code is 0335003. You can download the form of this document on our website.

Also on our website there is a completed sample act in form MX-3, by editing which you can create your own document with your original data.

If you have any unresolved questions, you can find answers to them in ConsultantPlus. Full and free access to the system for 2 days.

General information about the document

The act on the return of inventory items transferred for storage is in the Album of unified primary forms for accounting for inventory items at storage locations, which was approved in 1999 (August 9) Post. State Statistics Committee No. 66.

Since the beginning of 2013, unified forms have become only recommended for use, so the company has the right to develop a form that is convenient for it (only by adding rows or columns to MX-3), without forgetting to enter all the necessary document details. The use of the developed form is prescribed in the company's accounting policy. The MX-3 form is complete and convenient, so organizations often use it unchanged.

The purpose of the act is to document the transfer of goods and materials; in addition, on the basis of it, goods and materials are written off from an off-balance sheet account, and the cost of goods storage services is calculated.

For your information! Based on this document, any goods and materials can be transferred: transport, equipment, other goods.

Fill out the form

Data is entered into the form from the front and back sides. Let's describe each in detail.

Front side

First, enter information about the custodian organization:

- indicate the name, structural unit;

- fill out the code according to OKPO, type of activity according to OKDP.

Then they indicate the same about the depositor, as well as his full name. Next, enter the details of the agreement on the transfer of goods and materials for storage, the details of this act.

Then follows a table in which you need to enter data about the returned goods:

- Item number

- Product name, type of packaging, code.

- Product Detail.

- Units.

- Quantity or mass.

- Product price.

- Price.

- Note.

- Total quantity and cost per page.

Reverse side

The table continues on this side. It is filled out in the same way. The “Total” column should contain indicators for the back page. The column “Total according to the act” is completely according to the table on all pages. Then enter the shelf life.

The following is a table that should contain information about the work done and services provided:

- Number in order.

- Type of work or service and its code.

- Units of measurement and code according to OKEI.

- Quantity.

- Price.

- Price.

- Note.

Then indicate the total cost, VAT and cost including VAT.

Next, the cost of work and services is indicated in words, the financially responsible person and the depositor put their signatures (indicating the position and decoding). They put down special marks.

Complete filling out the signature form on the receipt for receipt of goods and materials.

What is important to remember

When filling out the document, you need to remember the following rules:

- The form must be filled out by the financially responsible person of the custodian organization.

- The document must be prepared in two copies. The first will be held by the custodian company, and the second by the bailor.

- The document storage period is 5 years.

- Errors must be corrected in the standard way: by carefully crossing them out, writing the correct version at the top, and affixing the o and signature of an authorized employee.

When an organization accepts valuables for storage, an act of acceptance and transfer of goods and materials is drawn up according to the unified form MX-1. In what cases is this necessary? The organization has the right to accept property that belongs to other persons or organizations for storage, obliging to ensure its safety on a paid or free basis. Thus, both companies for which this is a business activity (warehouses, banks, etc.) and enterprises that carry out this activity free of charge (for example, libraries, theaters, clinics) can act as custodians.

When transferring inventory items for safekeeping, the party handing over the valuables and the party accepting them for storage enter into a storage agreement in writing. It is worth noting that companies for which the storage of valuables is a business activity, instead of concluding such an agreement, can issue a warehouse receipt, which defines the terms and conditions for storing material assets.

If inventory items are received for storage on the basis of an agreement, then in addition to the contract, the supporting documents for acceptance of inventory items, in particular, will be the act of acceptance and transfer of inventory items for storage according to the unified form No. MX-1. If an organization has accepted inventory items for safekeeping under any other agreements (for example, sales with transfer of ownership after payment), then in addition to the contract itself, the justification may be documents that were drawn up when transferring inventory items, in particular, a delivery note (for example , according to the form TORG-12) or an invoice for the release of materials (for example, form M-15).

The form of the act of acceptance and transfer of inventory items for storage has a unified form MX-1 and was approved by State Statistics Committee Resolution No. 66 dated 08/09/1999. However, you have the right to independently develop an act of acceptance and transfer of inventory items using the MX form to fill out -1 as a sample.

Storage in a warehouse

A commodity warehouse is an organization (entrepreneur) that carries out the storage of goods as a business activity and provides services related to storage.

A wide variety of goods can be stored in warehouses. As a rule, each warehouse is equipped with equipment designed to store a certain type of goods. One type of warehouse is a public warehouse.

A special feature of storage in a warehouse is the inspection of goods by the warehouse upon receipt and during storage. Inspection of goods, determination of their quantity and external condition in accordance with Article 909 of the Civil Code of the Russian Federation are the responsibility of the warehouse, unless otherwise provided by the contract, and such verification is carried out at the expense of the custodian. Inspection by the custodian of goods when they are transferred for storage is important to determine the degree of culpability of the custodian in the event of loss or damage to goods during storage.

The responsibility of the warehouse is also to provide the goods owner with the opportunity, during storage, to inspect the goods or samples of goods, if de-identified storage takes place, to take samples and take the necessary measures for the safety of the goods.

In accordance with the general provisions on storage, if it is necessary to change the conditions of storage of goods, the bailee is obliged to immediately notify the bailor. When stored in a warehouse in accordance with Article 909 of the Civil Code of the Russian Federation, to ensure the safety of goods, the custodian has the right to independently decide to change the storage conditions. The obligation to notify the goods owner occurs if a significant change in storage conditions is required.

When storing goods, damage to the goods may occur not only within the normal limits of damage, but also beyond these limits and the limits agreed upon in the contract. In this case, the warehouse is obliged to immediately draw up a damage report and notify the goods owner on the same day.

If, upon receipt of goods at the warehouse, their inspection and verification of quantity are the responsibility of the warehouse, then when returning the goods to the goods owner, both the warehouse and the goods owner have the right to demand inspection of the goods and verification of their quantity. In this case, the costs are borne by the party who requested the inspection or quality control of the goods.

If neither party has expressed its desire to inspect the goods and check its quality and these actions have not been carried out, a statement of shortage or damage to the goods due to improper storage is made to the warehouse in writing either upon receipt of the goods or within three days , if the shortage or damage could not be detected by the usual method of receiving the goods. If the owner of the goods does not make a statement to the custodian within the specified period, it is considered that the goods are returned in accordance with the terms of the contract.

Sample of filling out the unified form MX-1

The organization that received the goods for storage, after signing the act of transfer for storage, bears full responsibility for the safety of the received values. Therefore, it is very important to correctly and accurately describe the transferred goods or other material value, as well as its value.

In the header of the form, you need to fill in the details of the company that will store the valuables (address, telephone number, code according to OKPO, type of activity according to OKPD), details of the company transferring the valuables for storage, number and date of the agreement, type of transaction, number and date of drawing up the act of transfer of inventory items for storage.

In the main part of the act, you need to fill out the basis for drawing up the act: what was accepted for storage, for how long. Next comes the table, which consists of 9 columns:

- Product number in order;

- Product name and type of packaging;

- Code;

- Characteristics of goods and materials;

- Name of the unit of measurement;

- OKEI code;

- Quantity/weight;

- Price;

- Price.

Next, under the table describing the goods being transferred for storage, you need to describe the storage conditions and special notes, if any. The completed form is signed by the depositor (position/signature) and the employee accepting the goods and materials for storage.

To fill out the form quickly and without errors, check out the example of filling out the MX-1 act:

unified form MX-1:

Related posts:

- Act form OS 3 Form OS-3. Certificate of acceptance and delivery of repaired fixed assets Formation of an act in the OS-3 form is the final stage...

- Certificate of acceptance of foundations Certificate of readiness of foundations for installation of equipment Update: February 6, 2020 Documents such as certificate of readiness of foundations...

- Inventory act The word invThe word consists of 3 letters: the first and, the second n, the last in, The word inv in English...

- Certificate of transfer for installation Certificate of transfer of an object for work Download in WORD format (.doc) Certificate of transfer of an object for...

Sample of filling mx 3 for several objects

Important However, most enterprises still choose the unified MX-1 form, since it contains all the necessary information. MX-1 Rules for filling out the act Form MX-1 must be filled out by the party accepting the valuables for storage. OKDP);

- Legal details of the owner (name, place of registration, telephone);

- Number and date of the accompanying agreement.

- OKPO of both parties to the transaction;

Unified form MX (click to enlarge) Next is filling out the number and date of the act being drawn up.

Next, information about accepted inventory items is entered, presented in the form of a table. The following data is filled in the appropriate columns:

- Description of the valuables deposited;

- Quantity;

- Name and unit of measurement;

- Number in order;

- Price;

- Total cost of the goods;

- A comment.

- Product code;