Purpose of the unified form INV-3

The INV-3 form is used by Russian economic entities as a tool for documenting the results of an inventory - a procedure during which the actual presence in the established places of their storage of any resources owned or disposed of by a specific entity (inventory, stocks, documents, etc.) is revealed. etc.).

For more information about the inventory inventory procedure, read the article “Inventory of inventories”.

The unified form INV-3 is drawn up in 2 copies. It must be signed by employees who are members of the inventory commission. The data to be entered into the form under consideration is determined based on the results of recalculation, weighing procedures, and measurement of certain resources for each designated storage location. It is also necessary to fill out a separate form for each materially responsible person (MRP) or group of such persons who are responsible for the safety of valuables.

You can find out about the nuances of conducting an inventory when changing the MOL, as well as in other cases provided for by law, in ConsultantPlus. Get trial access to the system for free and go to the Accounting Guide.

The first copy of the INV-3 form must be sent to the accounting department, the second remains at the disposal of the MOL.

You can find INV-3 forms on our website:

A sample of filling out the INV-3 form is also available to you on our website.

What is INV-5

The recipient of the goods, in some cases specified by law, has the right to refuse it. And then, at the time of processing the return, until the supplier takes back his property, it ends up in the custody of the unsuccessful buyer, who is obliged to ensure its safety.

And if at this moment it is time for an inventory, then inventory items in safekeeping should also be taken into account. This is why a special form of accounting document INV-5 has been developed, where the goods falling under this definition must be entered in the appropriate order.

Norms

The need to prepare this document is established:

- Law on Accounting (No. 402).

- Resolution on the approval of working forms for recording cash transactions and inventory results (Goskomstat as amended in 2000).

Content

This form consists of several sheets containing the following content:

- A title page indicating the time and place of the inventory.

- One or two pages of factual information indicating: Who the supplier is.

- What kind of product is it and where is it stored?

- From what date?

- Documentary confirmation.

- Availability in storage location.

- Members of the commission.

Who should use the INV-3 form

Form INV-3 was approved as a unified document (to be used by all legal entities, regardless of their organizational and legal form and the type of economic activity they carry out) by Resolution of the State Statistics Committee of the Russian Federation No. 88, adopted on August 18, 1998.

However, since 01/01/2013, the right to use your own forms for recording inventory results has been legislated (information of the Ministry of Finance of the Russian Federation No. PZ-10/2012). An exception is established for those organizations for which the legislator directly prescribes the use of unified documents. That is, for budgetary structures (clause 1.1 of the order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49).

At the same time, many commercial entities prefer not to abandon the use of the INV-3 form - due to business custom, and also because its structure is convenient and familiar.

Read about the rules governing the use of unified forms of documents in the material “Primary document: requirements for the form and the consequences of its violation .

Sources:

- Resolution of the State Statistics Committee of the Russian Federation dated August 18, 1998 N 88

- Order of the Ministry of Finance of the Russian Federation dated June 13, 1995 N 49

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

How to fill

The form is filled out by one of the members of the commission carrying out the inventory, authorized by the chairman, at the time of conducting an inventory of goods and materials in safekeeping. Two copies of this document must be made:

- The first one is for accounting.

- The second is for those financially responsible for the inventory data.

Instructions

The inventory of goods in safekeeping is carried out as part of the general inventory as follows:

- First, the corresponding order is signed.

- A commission is created.

- A date is set for the property audit.

- The commission is studying the structure of INV-5, the procedure for filling it out and the rules for responsible storage of property.

- The financially responsible employee provides the commission with a receipt confirming the availability of inventory items in storage.

- As the inventory goes through, the commission records the availability of goods in safekeeping and enters it into INV-5.

- The inventory includes all data on the product in accordance with the document form.

- A financially responsible employee of the company must be present when filling out.

- Upon completion of the inventory, the actual data entered into INV-5 is confirmed by the signatures of all commission members by the responsible persons.

- The final completed document forms are handed over to their intended destination.

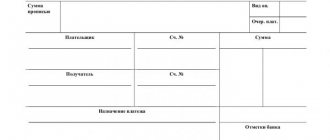

Sample of filling out the inventory list INV-3

In the main tabular part of the INV-3 form, the following fields are filled in (see Table 1).

| Column number | Content |

| 1 | line numbering |

| 2 | account and subaccount number |

| 3 | name of inventory items |

| 4 | nomenclature number |

| 5, 6 | measuring units (according to OKEI, name) |

| 7 | price |

| 8 | inventory number |

| 9 | passport number (for certain types of inventory items) |

| 10-13 | Availability of inventory items based on fact and accounting data (quantity and amount) |

Inventory form and sample download

Document year: 2019

Document group: Forms, Forms

Type of document: inventory, statement

Download formats: DOC, EXCEL, PDF

The inventory list is intended to record material assets in enterprises of various forms of ownership. It is drawn up in 2 copies, where the signature of the responsible persons included in the commission and the employee who bears full responsibility for the preservation of goods and materials is affixed. One copy is sent to the accountant, and the second is kept by the person with financial responsibility.

Before starting the inventory, a receipt is taken from one person or group of persons responsible for inventory assets, the purpose of which is to confirm that all assets are available for recounting. Thanks to the inventory of inventory items, it is possible to obtain information regarding the property operated by the organization.

Download documents

If you have not found the answer to your question or there are still misunderstandings, contact a lawyer for a free consultation in the chat on our website

| Inventory list INV-3 blank form |

| Inventory list INV-3 example of filling |

| Inventory list 0504087 blank form |

| Inventory list 0504087 example of filling |

Related posts:

- VAT recovery postings The nuances of VAT recovery and what postings are used? Restoration of VAT previously accepted for deduction...

- Form 12 Form 12 for an apartment, what is it? This article describes in detail Form 12 for an apartment...

- 2 purchase prices 2020 2 purchase prices form instructions for filling out the 2 purchase prices form looks like a questionnaire and consists of…

- Application for goods Sample document for the purchase of goods: how to write a memo for the purchase? Workwear (PPE) Furniture Stationery Office equipment…

Basic moments

Inventory of inventory items in a store or other enterprise engaged in commercial activities is carried out taking into account certain important points.

A complete list of them is reflected in sufficient detail in special legislation. Moreover, it is important to remember about the documentary support of such an inventory.

Verification of the relevant forms is carried out by regulatory authorities. There are also certain features of the procedure in certain segments of activity.

These include inventory of inventory items in a pharmacy. There is a certain shelf life and storage of such goods.

Failure to follow the rules can lead to quite serious troubles. Inventory allows you to solve a large number of different problems at the same time.

Before you begin the inventory procedure, you will need to consider the following issues:

- what it is?

- what is the role of the document;

- legal regulation.

What it is

First of all, it is necessary to understand the very concept of “inventory”. The easiest way to do this is with a simple example.

There are also several types of inventory procedures to keep in mind. It can be carried out both because of the presence of such a requirement in legislative norms and on other grounds.

Often, an inventory is carried out by the owner of the enterprise himself in order to identify losses and determine the exact quantity of goods.

Another important point concerns the inventory form itself. In accordance with legal regulations, it must be used in the prescribed format.

There are simply no alternatives. This point is fixed at the legislative level. It is required to use only the unified form INV-3.

But this rule applies only to inventory, which will subsequently be used for reporting.

Since INV-3 is precisely a reporting document. Required for preparing financial statements.

If the inventory process is carried out on the owner’s own initiative, the format for displaying information can actually be any other.

What is the role of the document

The role of a document of this type is essential. Using the INV-3 form it is possible to solve a variety of problems.

At the moment, this unified form is used for the following purposes:

| Reflection in documentary order | All material and commodity assets available for storage |

| Indicates location | Specific property |

| The path of movement is indicated | Valuables or goods by organization |

| Preparation of financial statements | And other documents |

| Other | — |

Moreover, this document allows not only to establish the fact of the presence of a certain quantity of goods.

In the future, after drawing up, it can be requested for consideration by regulatory organizations. First of all, this is the Federal Tax Service.

There are also many other institutions that also have the right to request reporting documentation.

Also, INV-3 is almost always drawn up if there is a change in management or other reorganization actions take place at the enterprise.

Thus, the process of transferring property into ownership of another person is carried out. This moment has a large number of different nuances.

It is important to avoid making mistakes when compiling such an inventory sheet. Since this can lead to quite serious problems in the future.

Legal regulation

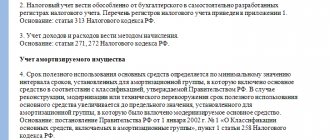

The format of the inventory sheet itself is reflected in the special Resolution of the State Statistics Committee No. 88 dated 08/18/98. At the moment, the edition dated 05/03/2000 is valid.

This document includes the following main provisions:

- the resolution itself;

- unified format of accounting documentation - basic provisions, indicated by complete

- list of forms of accounting documentation of various types;

- basic guidelines for the use and completion of certain formats are established;

- incoming and outgoing orders are used;

- what is an expenditure order;

- unified forms of primary documentation:

| INV-1 | A point is established regarding the inventory of fixed assets |

| INV-2 | Indicates the format of the inventory label, how this document is compiled |

| INV-3 | What is an inventory of goods and material assets? |

| INV-4 | How to draw up an inventory report of already shipped material and commodity assets |

| INV-5 | Reflects a question regarding the inventory list of goods that were previously transferred for safekeeping |

| INV-6 | An act drawn up for material as well as commodity assets that are in transit at a specific point in time |

| INV-10 | An act required to reflect fixed assets, the repair of which for some reason was not completed |

| INV-11 | Future Expense Inventory Process |

| INV-15 | Cash inventory process |

| INV-16 | Inventory list of shares, as well as other securities falling under the designated definition |

| INV-22 | What is an order to carry out an inventory procedure? |

- how an inventory of fixed assets is carried out - INV-1 second page, INV-1 third page;

- inventory list of goods, as well as material assets - the second and third pages of INV-3, the fourth page of INV-3.

This resolution reflects all the most significant nuances associated with both the preparation of INV-3 and the formation of other similar documents.

Whether an additional payment to the pension of civil servants for length of service is due, see the article: pensions for civil servants for length of service. Read the rules for filling out a work book when applying for a job here.

There are a large number of different nuances directly related to the preparation of an inventory list. The person compiling such an inventory should study them.

Errors and typos in such statements are unacceptable. This can lead to serious fines from the Federal Tax Service, as well as other institutions.

Inventory list of inventory items: sample

An inventory list of inventory items is a unified form of documentation drawn up when carrying out procedures for accounting for valuable property at a specific enterprise or organization. The procedure for filling out the accounting inventory, the obligation to use it, the necessary details of the form are the main points that you must know in order to correctly record the inventory results.

Inventory list of goods and materials

The inventory list of goods and materials, form INV-3, was approved by Decree of the State Statistics Committee of August 18, 1998 No. 88. Registration of INV-3 is necessary for the purpose of recording the actual availability of inventory in a particular organization. In this case, goods and materials mean:

- goods;

- finished products;

- production or other inventories of the company, etc.

Valuables may be stored in specially designated places (warehouses, boxes, hangars, etc.) or be at any stage of movement in connection with the activities of a legal entity. Thus, the information entered into the INV-3 form is determined during the ongoing procedures of recalculation, weighing, and measurement exclusively at the location of the inventory items.

Mandatory details of INV-3

When using a unified inventory form during an inventory, employees of the inspection commission need to know what mandatory details must be filled out. The INV-3 inventory list must contain:

Page 1 of the inventory – receipt

Filling out the inventory begins with entering the required details into the receipt:

- In the fields “Organization” and “Structural unit” the full or abbreviated corporate name of the organization is entered in accordance with its constituent documents.

If the staffing table does not provide for division into structural departments of the company, the corresponding field remains blank. - As the basis for conducting an inventory, an internal administrative document of the executive body of the company (resolution, order, instruction), the date of its preparation and registration number are indicated. Unnecessary document names must be crossed out.

The frequency of inventory is determined by the management of a particular legal entity. The inspection can be scheduled or carried out urgently. Inventory records of inventory items during a planned inventory are no different in form and content from those compiled during an unplanned inspection.

- In the fields “Inventory start date” and “Inventory end date”, calendar designations corresponding to the time of inventory actions are entered.

- The document number and date of its preparation are filled in in accordance with the organization’s current policy for maintaining and recording internal document flow.

- In the column “Type of inventory assets” the name of the goods or other industrial products subject to accounting is indicated.

- The next ordinal field must contain information about the type of ownership on the basis of which the legal entity. a person uses or disposes of goods and materials - ownership, rent, storage, processing, etc.

- The positions and personal data of employees who are entrusted with the responsibility for maintaining records and taking inventory of valuables are indicated as financially responsible persons. Such an obligation may be provided for in an employment contract, order, regulation, agreement on the assignment of duties to ensure the safety of inventory items, job description, etc.

- At the end of the receipt, the actual date of removal of the remaining goods is indicated.

INV-3: sample of filling out 2-4 pages of inventory

The inventory list of inventory items (pages 2, 3, 4) is presented in the form of a table, which includes the following information:

- numbers of accounts and subaccounts;

- name and information characterizing the inventory items;

- number of values, unit of measurement, item number;

- unit cost;

- information on the actually identified quantity of inventory items and on the reflected volumes according to accounting data.

The inventory list of inventory items in the final line is filled in, according to all information, figures and amounts, exclusively in words.

https://youtu.be/_swELBlZ16s

All members of the commission specially created for the inventory sign the inventory form. In addition, the inventory is certified by the signature or signatures of the employees financially responsible for the safety of valuables, and is also endorsed by the chief accountant, confirming the comparison operation.

Obligation to use the document

The use of a unified inventory form, starting from the beginning of 2013, is not the responsibility of business entities.

In order to comply with the norms of the law on accounting, organizations can use an independently developed form for inventory of inventory items. A sample of a self-developed form must contain the mandatory details listed above.

The exception is budgetary organizations, the obligation of which to use a unified inventory form is enshrined at the legislative level.

Before starting an inventory of goods and materials, the initiator of the inspection creates a special commission of employees of the organization. The inventory list of inventory items itself is compiled on paper in 2 copies: 1 is submitted to the accounting department for drawing up a matching sheet, 2 remains at the disposal of persons who are financially responsible.

If the commission identifies goods that are not taken into account by the accounting department, all data on such goods and materials are subject to mandatory reflection in the inventory list of inventories.

For materials related to material assets, but which have lost their properties for further use (spoiled or unsuitable for production), appropriate acts are drawn up.

INV-18 (comparative statement of the results of inventory of fixed assets): form and sample

To account for and record shortages and surpluses of fixed assets, a special form is used - INV-18. When all the actual data is received, they are compared with accounting data. The form contains information about surpluses and shortages of fixed assets (PE) and intangible assets (IMA).

This document consists of 2 pages. The main page is filled out exactly as in the case of the INV-19 statement. The matching statement of the results of the inventory of fixed assets differs from the form for inventory items in the second page, made in tabular form.

Procedure for filling out INV-18

In total, table INV-18 has 11 columns. They contain information about those fixed assets or intangible assets for which the actual data did not coincide with the accounting data. Each object type must be entered on a separate line. To avoid confusion, you can use the INV-18 sample. The document contains the following information:

- object type number in order;

- name of the object and the most important information about it;

- lease terms and name of the lessor (this column is filled in if the property is not the property of the organization, but was leased by it; if the property is owned, then a dash is entered);

- passport, inventory and serial numbers of the object (a sample of filling out the INV-18 matching sheet shows that if there is no passport number, a dash is entered in the corresponding cell);

- information about existing surpluses and resulting shortages (their quantitative volume and total cost).

At the end of the document there is a summary line where generalized data is entered (the number and total amount of surpluses and shortages generated). You can use the INV-18 form and see how to enter this information.

The position and full name of the person responsible for filling out the statement must be indicated. Usually this is an accounting employee. To create a matching statement, he uses the inventory list INV-1. Only after a thorough check of the document does the responsible person sign the collation sheet for the inventory of fixed assets (FA).

The accountant is not the only person signing the statement. All employees representing the MOL on the positions specified in the document put their signature. By signing the paper, they agree with the results obtained and take responsibility for shortcomings, if necessary. There may be several such workers. All of them sign the OS matching sheet.

After filling out all the statements, the INV-26 form is used, which displays the final results of the audit.

Form INV 18

form of a comparison sheet of the results of inventory of fixed assets.

Sample of filling out the INV 18 form

sample comparison statement of the results of inventory of fixed assets.

Similar articles

- How to take an inventory and document it

- Statement of discrepancies based on inventory results (filling sample)

- INV-26 statement of accounting of results identified by inventory

- Inventory list of intangible assets (sample)