Order for write-off of food products sample

If the inventory results reveal food spoilage within the limits of natural loss norms, such losses are written off as expenses of the current financial year based on the order (order) of the head of the institution.

The cost of write-off products is determined depending on the method of their valuation, enshrined in the accounting policy: at the actual cost of each unit or at the average actual cost.

It should be added that the loss of products within the established norms is calculated after offsetting the shortages of valuables with surpluses due to mis-grading.

In the absence of approved standards, any loss is considered as a shortage (clause 5.1 of Guidelines No. 49). Example 1 In the warehouse of a military unit located in the territory belonging to the second climate group, spoilage of white cabbage in the amount of 0.350 kg was discovered.

(shelf life - from August to December).

Order on the commission for writing off material assets

On our forum you can discuss any difficult moment for you that arose in the course of keeping inventory records.

For example, you can learn how to properly write off unsalable goods.

The regulation must also provide for the following:

- the validity of decisions of the CSC with a certain quorum (for example, the presence of at least 2/3 of its members when making a decision on write-off);

- other important aspects of the work of the CSC.

- deadlines for consideration by the CSC of documents submitted to it on property subject to write-off;

- situations when it is necessary to invite experts or other specialists to determine the suitability (degree of possible use) of the property;

The regulation may also determine the period during which the CSC submits for consideration to the head of the company a document containing the commission’s conclusions on the further fate of certain material assets.

RђРєS‚ SЃРїРЅСЃР°РЅРёСЏ RїСЂРѕРґСѓРєС‚РѕРІ RїРЅС‚ания

Р' отдельных случаях Рє работе над актом RїСЂРёРіР»Р°С€Р°СЋС‚СЃСЏ R є уча стию потребительские, санитарные, пожарные или РёРЅС ‹Рµ контролирующие Рё надзорны Рµ РѕСЂРіР°РСС‹.

Форма РўРћР Р“-16 представляет SЃРѕР±РѕР№ двухсторонний бланк , заполняемый как СЃ С ‚итульной, так Рё СЃ оборотной стороны.

Акт содержит информацию:

- Рѕ количественных Рё стоимостных S…арактеристиках РІ SЃРµС… списываемых S‚оварны S… РїРѕР·РёС†РеР№;

- о суммарной стоимости всего объема списанмя;

- Rѕ RїSЂРёС‡РеРЅР°С... утраты RєРѕРЅРґРёС†Реонности.

Р'ланк РўРћР Р“-16 РЅР°

Order to write off material assets (sample)

The act is signed by members of the write-off commission and the financially responsible person and must be approved by the order of the manager on the write-off of materiel.

The order must contain the following elements:

- a link to the conclusion (decision) of the write-off commission and the act of writing off valuables;

- number and date;

- write-off deadline;

- signature of the manager who issued the order.

- information about the person responsible for the write-off and his signature on the order;

- reasons for writing off materiel (unsuitability for use, expiration date, etc.);

sample order for

Sample order for write-off of material assets

The director signs the order and submits it to the responsible employees indicated in it for review.

Legal advice Still have questions after reading? Call the number and our lawyers will advise you! The call is free. We recommend reading December 17, 2020 0 December 3, 2020 0 November 30, 2020 0 Your questions Receive an e-mail notification of a response I agree with the terms and conditions Send

Order on the creation of a commission to write off poor-quality and expired food products for the academic year

MUNICIPAL EDUCATIONAL INSTITUTION PLESCHEEVSKAYA ELEMENTARY SCHOOL - KINDERGARTEN OF PERESLAVSKY MUNICIPAL DISTRICT OF YAROSLAV REGION Yaroslavl region, Pereslavl district, village.

Source: https://dtp-sovetnik.ru/prikaz-na-spisanie-produktov-pitanija-obrazec-96930/

What does the sample look like?

An order issued for the possibility of removing from the balance sheet material assets that are not subject to further use must contain the following points:

- name of the organization, its legal address;

- Date of preparation;

- serial number assigned during the mandatory registration procedure in the document register;

- document's name;

- reasons why assets will be written off (based on pre-trial detention);

- a list of valuables that are subject to removal from the balance due to their unsuitability (if its size is too large, it can be issued as a separate appendix to the act);

- designation of the time frame within which this procedure must be completed;

- indication of the person responsible for carrying out the order, his position and full name;

- signature of the manager (after such an action, this act has legal force and can serve as a legal basis for writing off material assets);

- signatures of persons who must be familiar with the contents of the document (materially responsible employees, commission members).

Documents for download (free)

- Sample order for write-off of material assets

Order on the commission for writing off material assets

The order on the commission for writing off material assets is issued in connection with the creation of the body on the results of whose work the validity of the disposal of property unsuitable for further use will depend. Find out what to consider when drawing up such an order and what its sample might look like from our material.

Main aspects of drawing up an order on the commission for writing off material assets (goals, formation of the composition, execution of the protocol, etc.)

What does a sample order for a commission for writing off property look like?

Results

Main aspects of drawing up an order on the commission for writing off material assets (goals, formation of the composition, execution of the protocol, etc.)

Drawing up an order establishing the composition and defining other aspects of the work of the commission for writing off material assets (WSC) is one of the elements of a multi-step procedure for writing off the company’s property. This procedure includes the following:

- identification of material objects that have partially or completely lost their consumer properties, including as a result of physical or moral wear and tear, death or destruction and for other reasons;

- recognition of property as unsuitable for further use in the company’s activities;

- preparation of necessary documents.

The order on the CSC is necessary to resolve a number of organizational issues:

- determining the quantitative and structural composition of the company’s specialists for the formation of the CSC;

- establishing a time frame for the work of the CSC;

- detailing the powers, responsibilities and work regulations of members of the CCC.

The order on the CSC must be formulated in such a way that, as a result of the work of the commission, the main goal of its creation is achieved - making a decision to write off the company’s property.

The order may also contain regulations for the work of the CCC, if the algorithm of actions of the members of the CCC when performing their functions is not described in another local act (for example, in the Regulations on the work of the CCC).

Such regulations in the form of a separate provision, in particular, may contain a detailed description of the work of the CSC, including when:

- conducting an inspection of property subject to write-off;

- studying information about the properties and characteristics of this property contained in technical, accounting and other documentation;

- making a conclusion on the possibility and (or) feasibility (suitability) of further use of property (including the possibility of restoration or further use of individual elements: components, parts, structures - property subject to write-off).

To learn how the commission works when it comes to writing off a fixed asset, read the article “Documentation of writing off a fixed asset.”

On our forum you can discuss any difficult moment for you that arose in the course of keeping inventory records. For example, here you can learn how to properly write off an unsaleable product.

The regulation must also provide for the following:

- the validity of decisions of the CSC with a certain quorum (for example, the presence of at least 2/3 of its members when making a decision on write-off);

- deadlines for consideration by the CSC of documents submitted to it on property subject to write-off;

- situations when it is necessary to invite experts or other specialists to determine the suitability (degree of possible use) of the property;

- other important aspects of the work of the CSC.

The regulation may also determine the period during which the CSC submits for consideration to the head of the company a document containing the commission’s conclusions on the further fate of certain material assets. If such a provision has not been developed by the company, the necessary aspects of the work of the CSC are reflected in the order.

To learn about the role of the commission in the procedure for writing off low-value property, read the material “Act for writing off low-value and wear-and-tear items.”

What does a sample order for a commission for writing off property look like?

The write-off of material assets must be considered as one of the elements of the accounting and control system for ensuring the safety and efficient use of the company's property. Therefore, it makes more sense to organize the work of the CSC on an ongoing basis, and describe the regulations in a separate provision.

Taking into account this approach, there is no need to reflect a detailed description of the commission’s actions in the order on the CSC, and you can limit yourself to the following information, including:

- company name;

- details of the order (name, number and date);

- an indication of the purpose of creating the CSC, listing personalized information about its members;

- manager's signature.

You can see one of the options for a sample order on the commission for writing off material assets on our website.

order

The frequency of issuing an order for the CSC is not established by law, so this can be done once, and then reviewed as necessary.

Based on the results of the work of the CSC for the specified period, management assesses its effectiveness and formulates certain organizational conclusions (on the need to reduce or expand the number of CSC, change the structure, adjust the work regulations, etc.).

Results

The commission for writing off material assets is necessary to carry out a set of measures to assess the suitability of the company’s material assets and resolve the issue of their write-off. Its composition and powers are established by a special order.

Subscribe to our accounting channel Yandex.Zen

Subscribe

Source: https://nalog-nalog.ru/uchet_mc/prikaz_o_komissii_po_spisaniyu_materialnyh_cennostej/

Instructions: draw up an act of write-off of inventories

Templates and forms Act on write-off of inventories is a specialized form for registering operations on the disposal of material assets at an enterprise. Legislators have developed a unified M3 form. June 20, 2020 Evdokimova Natalya

Material reserves are a separate category of property assets of an institution. These include four groups of property:

- Finished products.

- Items for sale.

- Objects used to conduct business activities of the organization, the period of use of which does not exceed 12 months.

- Special categories of property, named in paragraph 99 of Instruction 157n, classified as part of the Ministry of Health, regardless of the period of use and value of the asset.

Material supplies include raw materials, materials, fuels and lubricants, food, clothing, personal protective equipment, bed linen and accessories, etc.

Reasons for disposal of inventories

The accounting instructions provide several reasons for writing off inventories:

- into production, that is, raw materials and supplies are used in the production cycle;

- for the economic needs of the organization, for example, for general economic management purposes;

- due to their disposal, for example, sale, gratuitous transfer;

- due to physical wear and tear, damage, natural loss;

- in connection with theft;

- expiration of the expiration date, for example, of medicines or food;

- for shortages identified during the inventory count, etc.

The operation of disposal of supplies will have to be reflected in a special document - an act. But before you start filling out the inventory write-off act, you need to fill out a primary document. That is, the basis document. For example, this is a requirement - an invoice for the issue of materials, a limit card, an invoice for the issue of the Ministry of Health to the outside, a statement of issue of raw materials and other documentation.

Form of act for writing off the Ministry of Health

The form of the act on write-off of inventories can be developed by the organization independently. The form used should be fixed in the accounting policy. It is necessary to take into account the specifics of the activity when developing the structure of the document.

https://youtu.be/i8krYkoqpeY

It is allowed to use a unified form, for example, an act on write-off of inventories - f. 0504230, approved by Order of the Ministry of Finance of the Russian Federation No. 52n. Its structure is suitable for reflecting all categories of material disposal transactions.

Download

Registration and storage

To complete a disposal transaction, prepare two copies of the write-off act at once. The first is transferred to the accounting department to make the appropriate entries in the accounting records. And the second remains with the financially responsible employee. For example, the warehouse manager.

To draw up and sign the act, a special commission must be created in the institution. The composition and powers of the commission, as well as its chairman, are determined by a separate order of the head of the company. Only the head of the organization or another authorized person has the right to approve the act. For example, a deputy by proxy.

Keep the acts for writing off the Ministry of Health for at least 5 years after the end of the reporting period (year). Such recommendations are enshrined in Part 1 of Art. 29 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting”.

Filling procedure

Fill out the form in accordance with the recommendations of Order No. 52n of the Ministry of Finance of the Russian Federation, as well as the explanations contained in the form itself 0504230:

- In the “MOL” field, indicate your full name. and the position of the material-responsible employee, whose responsibilities include storing forms.

- The “Commission composition” fields are filled in based on management’s order to approve the composition of the commission. Enter the positions and full names one by one. employees who are appointed to the commission for the disposal of supplies.

- Separately indicate the number and date of the order that approved the composition of the special commission.

- Fill out the tabular part taking into account the following recommendations:

- name of the Ministry of Health - indicate the name of the object in accordance with the registration data (nomenclature, accounting card);

- code - fill in if the institution has the established nomenclature of the Ministry of Health;

- Column No. 3 - enter the unit of measurement corresponding to the specific position of the item being written off, for example pieces, kilograms, etc.;

- Column No. 4 - record the cost norms for the MH facility, if any;

- field “Actually consumed” - we detail the quantity, price and amount of discarded materials;

- Column No. 8 - enter the reason or direction of disposal of supplies.

- In the “Conclusion of the commission” field, you must enter the specific purpose of the Ministry of Health or record the purpose of writing off the assets. An example of filling out an act of writing off inventories: “Material inventories were used for their intended purpose and written off for the needs of a government agency,” “Material inventories were used to repair computer equipment and are subject to disposal,” “Material inventories cannot be restored. Reflect their disposal in accounting."

Documents on the disposal of MH can be issued electronically, which requires the use of a digital signature. The accounting department mark is not placed on electronic documentation. In accounting, the corresponding entries are reflected in separate accounting certificates.

A ready-made sample act on write-off of inventories looks like this:

Download

The article was prepared using materials from ConsultantPlus. Get access

Source: https://gosuchetnik.ru/shablony-i-formy/instruktsiya-oformlyaem-akt-o-spisanii-materialnykh-zapasov

Sample order to write off materials for production

The mandatory form of a write-off order is not approved by law. The manager uses the template established by a local act of the organization, or draws up an order in any form. The main requirements are written form, the presence of instructions, brevity and information content.

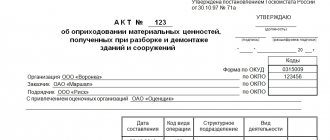

Based on the decision of the commission, an act on the write-off of material assets is drawn up, which indicates all the assets subject to write-off and the reasons for the write-off. The act is signed by members of the write-off commission and the financially responsible person and must be approved by the order of the manager on the write-off of materiel.

Material write-off act

The act does not have a unified, standard template, so it can be drawn up in free form or according to a template developed within the organization, in accordance with the characteristics of its activities and needs.

The document can be drawn up on a regular A4 sheet or on the organization’s letterhead in a single copy intended for the accounting department of the enterprise (however, if necessary, members of the commission, as materially responsible persons, can request a copy of the act).

It is not necessary to certify it with a seal, since it relates to internal document flow and is recorded in a special journal.

The act of writing off materials has a legal status, since on the basis of it the specialists of the accounting departments reflect the book value of the written-off material assets, as well as the direct loss of the enterprise due to their loss. In turn, this information is reflected in the tax records of the legal entity.

Interesting: Digital signature for individuals for free, how to do it

Sample act of writing off material assets

Items used for work, like any equipment, become unusable. To exclude them from the organization’s property, it is necessary to carry out a write-off procedure.

For government institutions, Order No. 52n of the Ministry of Finance of Russia dated March 30, 2015 applies, which regulates, among other things, the forms of documents required for disposal.

The sample act for writing off materials for production depends on the type of property being written off. So, there are:

Step 1. Fill in the number and date, name of the organization, structural unit, OKPO code, INN and KPP of the institution, financially responsible person, members of the commission for the receipt and disposal of assets, details of the order on the basis of which the commission operates.

How to correctly draw up an order to write off material assets

- A heading that communicates the essence of the document.

- Composition of the write-off commission. In addition to the financially responsible person, it includes 2-3 more people.

- Appointment of the chairman of the commission.

- Certified by the personal signature of the General Director and seal.

- Based on the results of the commission’s activities, a write-off act is drawn up, which is sent to the accounting department to remove resources from the enterprise’s balance sheet.

In the course of the company's activities, its staff uses a huge amount of office supplies; the shelf life of goods expires in stores, display cases deteriorate, and they have to be thrown away. Equipment in production becomes obsolete and wears out.

Some of this can be sold at residual value, but some of it has to be thrown into a landfill.

Sample order for write-off of material assets

- The number of commission members is preferably chosen to be odd in order to create a quorum in case of controversial issues and issues.

- How is a quorum established (at what ratio of its members “for” and “against”).

For example, a quorum can be approved if the number of its members who made a certain decision is at least two-thirds of all participants. - The time frame within which the commission must review the material assets subject to write-off and decide on the possibility of carrying out such an action.

- Identification of current situations in which it will be necessary to invite third-party experts or other specialists in order to realistically assess the need to withdraw material assets from the balance of the enterprise.

- Other aspects and features of the work.

- Mandatory inspection of all property that is subject to write-off, without exception. If it is necessary to check the functionality of the equipment, you should either obtain an expert’s opinion or verify on your own whether it is in faulty condition.

- Studying information regarding the technical or any other characteristics of an object, which is decisive when making a decision on write-off.

- After all the procedures, a direct conclusion is made on whether the material value can be restored, repaired, used for other purposes or whether it is subject to write-off.

Write-off of materials step-by-step instructions for accounting

The invoice in two copies is drawn up by the financially responsible person of the structural unit handing over material assets. One copy serves as the basis for the handing over unit to write off valuables, and the second copy serves as the basis for the receiving unit for the receipt of valuables.

However, in the warehouse the storekeeper or warehouse manager is responsible for them, and the materials are taken into account on account 10. When the materials leave the warehouse, the situation will change: the account and the person in charge will change. In this article we will analyze the write-off of materials with step-by-step instructions for this procedure for you.

Are you here

Material assets are transferred to production upon request - an invoice or a limit-fence card. At the same time, they are again assigned to a certain financially responsible person. In order to write them off from it, as well as to confirm the fact of actual expenditure for the tax authorities, it is necessary to draw up an act for writing off materials.

Below, fill in the personal data of the employees who are members of the commission that formalizes the disposal of inventories. The name of its chairman should be written down first. You can also indicate the details of the order on the basis of which the commission was created.

Order on the creation of a commission for write-off of materials

- A heading indicating that this is an order to write off material assets.

- The reason for creating the commission is clarified and indicated.

- A list of responsible persons and commission members is included.

- Separately, it is necessary to identify a responsible person who is appointed as the chairman of the commission.

Interesting: If the warrant for an apartment is lost, what to do?

Any enterprise, regardless of its form of ownership, must have such a commission. If it is necessary to write off the fixed assets of an enterprise, then the order is drawn up after an inventory has been taken, based on the results of which a list of inventory items unsuitable for further use is specified. Most often these are spoiled, broken, morally outdated values.

Write-off of fixed assets: sample orders

Kotova Alla Nikolaevna Author PPT.RU January 19, 2020 A fixed asset is subject to write-off in the event of its disposal: sale, liquidation, or in other cases.

We will tell you in our article how to document the write-off, how to reflect it in accounting and tax accounting, and we will give examples of documentation, including an example of an order to write off fixed assets. ConsultantPlus FREE for 3 days The registration, movement and disposal of fixed assets is regulated in accounting (Order of the Ministry of Finance 26n dated 30.03.01) and (OS) (Order of the Ministry of Finance 91n dated 13.10.03).

The value of property is written off when it is disposed of or is unable to generate economic benefits in the future.

An object may be disposed of in the following cases:

- sales;

- donations;

- termination of use due to moral or physical wear and tear;

- emergency response;

- identifying shortages during inventory;

- transfers in the form of a contribution to the authorized capital of another company;

- in other cases.

In order to establish the safety of property, organizations conduct an inventory.

The procedure for its implementation is regulated by the Methodological Instructions approved. Inventory is also necessary to identify fixed assets that are unsuitable for use, or whose further use in the company’s activities is impractical.

A sample order for an inventory of fixed assets can be downloaded at the end of the article. Conducting an inspection can be mandatory and proactive. Inventory is required in the following cases (clause 1.5 of the Guidelines):

- preparation of annual reports (an inventory of fixed assets is allowed once every three years);

- change of financially responsible person;

- identification of facts of damage and theft of property;

- natural Disasters.

To carry out the inventory, the company's management appoints a commission.

It is advisable to include representatives of the administration, employees of engineering and technical services, and financial employees. The inspection is carried out in the presence of the person responsible for the safety of the property.

If obsolete or damaged equipment is identified, the commission may decide to repair, restore the OS, or liquidate it. In order for the OS to be used for a long period, it must be repaired. During repairs, the characteristics of the object are not improved, but only its viability is maintained.

Repair costs are considered expenses of the current period in both accounting and tax accounting (clause 1). Modernization or reconstruction of equipment is carried out in order to improve its performance, power, increase its useful life or change its purpose.

The costs of such work are taken into account as capital investments and increase the cost of the modernized facility (clause.

27 PBU 6/01, clause 2). Depreciation on reconstructed or modernized equipment continues to accrue throughout the entire period of work. But if modernization and reconstruction work continues for more than 12 months, then depreciation should be stopped until the work is completed (clause

2). During downtime, the OS can be put into storage.

This procedure includes a set of measures to preserve the integrity and serviceability of the property until it begins to be used in business again. The procedure for conservation of objects is developed and approved by the organization independently. It should be borne in mind that the transfer of idle equipment to mothballing is not the responsibility of the company; such a decision is made by the company’s management.

The costs of conservation and removal of equipment from it are included in the enterprise’s expenses in the current period. When transferring to conservation, you should keep in mind that the property will not be exempt from property tax for this period.

But the calculation of depreciation should be suspended when the object is mothballed for a period of more than three months (clause 2). To determine the possibility of further use of the property, by decision of the company management, a commission is created, which includes persons responsible for the safety of the property, technical specialists, and financial workers (clause 77). The commission is entrusted with the responsibility of inspecting the facility, making a decision on its liquidation, identifying the reasons for the impossibility of further operation and the persons responsible for this, as well as drawing up a decommissioning act.

The write-off act can be developed by the organization independently, or one of the unified forms can be used: OS-4, OS-4a, OS-4b ().

Based on the act, the object is written off from the register and a mark of disposal is placed on its inventory card. The residual value of the written-off object is reflected in non-operating expenses in both accounting and tax accounting on the date of the write-off act. Also, non-operating expenses should reflect the costs of dismantling, removal and other actions related to the liquidation of the facility.

The components of the liquidated object, suitable for further use, are accounted for at the current market value, reflected in non-operating income. Dear readers, if you see an error or typo, help us fix it!

To do this, highlight the error and press the “Ctrl” and “Enter” keys simultaneously. We will learn about the inaccuracy and correct it. FOR HR: FEED FOR LAWYER: ARTICLES Subscribe to the daily newsletter Every weekday we will send you everything that was published yesterday You won’t miss anything!

Subscribe Subscribe to our channel on Telegram We will tell you about the latest news and publications. Read us anywhere. Always be aware of the main thing!

Subscribe to our channel in Yandex Zen Find out important news on time!

Made in St. Petersburg © 1997 - 2020 PPT.RU Full or partial copying of materials is prohibited; with agreed copying, a link to the resource is required. Your personal data is processed on the site for the purpose of its functioning. If you do not agree, please leave the site.

Are you sure you want to remove the image you're using and replace it with your default avatar? Are you sure you want to go out?

Order on write-off of food products that have become unusable

> > > Tax-tax May 16, 2020 17802 Subscribe to our accounting channel Yandex.Zen Act of write-off of food products - a sample of this document is important for companies involved in catering and food trade to draw up correctly.

Under what circumstances should the specified act be drawn up, as well as what points you need to pay attention to when filling it out, we will describe further.

Any organization engaged in activities related to the sale and processing of food products sometimes has to face a situation where:

- food can spoil due to someone else's fault or due to external factors.

- she does not have time to sell some of the purchased goods before the expiration date;

In any case, if a food product is not suitable for subsequent consumption, the company has a need to write it off.

How should an act for write-off of food products be drawn up, document form

> > > If, after the goods have been registered, a factory one is discovered, the goods have deteriorated or for some reason cannot be sold, they are written off. For this purpose, a special form is drawn up in the TORG-16 form.

This is the most convenient form of write-off, taking into account most probable causes of damage to commercial property. Any company whose activities are related to the sale or processing of food products has at least once encountered the situation:

Damage to goods

- the goods simply did not have time to sell out in time, and they failed

- when, under the influence of external factors or due to someone else’s fault, the goods have deteriorated

In each of these cases, all damaged goods must be written off.

Food accounting (Zernova I.)

Autonomous institutions that have canteens on their balance sheet, in which the process of providing food to workers (pupils, students) is organized on their own, purchase and process food products when carrying out this activity.

The procurement regulations are a document that is designed to regulate the procurement activities of an institution

Form TORG-16. Certificate of write-off of goods

2755 FORUM! The act of writing off goods in the TORG-16 form is useful in cases where goods in the organization’s warehouse have become unusable and need to be written off.

This document confirms the legality of the actions of the storekeeper or other financially responsible person.

FILES The document will be especially useful for food organizations, pharmacies and other companies that deal with perishable goods. Important point! Write-offs cannot be made without the knowledge of the head of the organization.

It is worth noting that

Write-off act for food products

Food products can be written off on the basis of an act, form TORG-16, this form is used to write off any goods in case of their unsuitability, spoilage, expiration date, including can be used for food products. For products, this report form is used in case of damage.

The document is primary and serves as the basis for the accountant to make double entries in accounting to remove spoiled food products from accounting.

Damage to food products occurs due to the end of their use period, violation of storage and transportation conditions, violation of the integrity of the packaging and for other reasons that lead to the impossibility of further consumption of the product as food. Sample write-off act for food products free download from.

As a rule, the write-off process is preceded by an inventory of grocery products, during which all violations are established and spoiled products are identified that are subject to deregistration and disposal.

Sample order for write-off of inventories

The expiration of the service life of valuables leads to management creating an order to write off inventories.

- /form

Related documents

Description of the document

View screenshot

Leave feedback

ASK A QUESTION

Nuances of writing off damaged (expired) goods

Important December 25, 2020

During the control event, damaged and expired goods may be identified, which are subject to seizure and deregistration.

How this operation should be reflected will be discussed in the article.

By virtue of clause 7 of Art. 55 of Federal Law No. 61-FZ, pharmacy organizations and individual entrepreneurs with a license for pharmaceutical activities have the right, along with medicines, to purchase and sell: medical products, disinfectants;

Food write-off act

The need to write off food products may be caused by their initial defects, spoilage, improper storage, transportation failure, or expiration date.

To document this process in the accounting of public catering and trade enterprises, the “Act on the write-off of goods” (form No. TORG-16) is used according to Resolution of the State Statistics Committee of Russia dated December 25, 1998 N 132.

Important! Since 2013, primary accounting documents, including the TORG-16 form, are not required to be used in the form specified in the resolution.

Source: https://life-lawyer.ru/prikaz-o-spisanii-produktov-pitanija-prishedshih-v-negodnost-80511/

Write-off of materials step-by-step instructions for accounting

Any organization acquires materials for the company’s activities not for their own sake. And the purchased valuables will not lie dead weight in the warehouse for the director to admire. They are intended for use in production, sales or administrative purposes. Therefore, purchased materials are subsequently consumed in production.

However, in the warehouse the storekeeper or warehouse manager is responsible for them, and the materials are taken into account on account 10. When the materials leave the warehouse, the situation will change: the account and the person in charge will change. In this article we will analyze the write-off of materials with step-by-step instructions for this procedure for you.

articles:

1. Accounting entries for writing off materials

2. Registration of write-off of materials

3. Write-off of materials - step-by-step instructions if not everything is consumed

4. Standards for writing off materials for production

5. Example of a write-off act

6. Methods for writing off materials for production

7. Option No. 1 – average cost

8. Option No. 2 – FIFO method

9. Option No. 3 – at the cost of each unit

So, let's go in order. If you don't have time to read a long article, watch the short video below, from which you will learn all the most important things about the topic of the article.

(if the video is not clear, there is a gear at the bottom of the video, click it and select 720p Quality)

We will look at write-offs of materials in more detail than in the video later in the article.

Accounting entries for write-off of materials

So, let's start by determining where the purchased materials can be sent. It should be noted that materials are truly ubiquitous and there are ways to, as they say, “plug a hole” in any problem area of the organization:

- - serve as the basis for the production of products

- - be an auxiliary consumable material in the production process

- — perform the function of packaging finished products

- - used for the needs of the administration in the management process

- — assist in the liquidation of decommissioned fixed assets

- - used for the construction of new fixed assets, etc.

And the accounting entries for writing off materials depend on what materials are released from the warehouse for:

Debit 20 “Main production” – Credit 10 – raw materials released for production

Debit 23 “Auxiliary production” - Credit 10 - materials were released to the repair shop

Debit 25 “General production expenses” – Credit 10 – rags and gloves were issued to the cleaner servicing the workshop

Debit 26 “General business expenses” – Credit 10 – paper for office equipment issued to the accountant

Debit 44 “Sales expenses” – Credit 10 – containers for packaging finished products were issued

Debit 91-2 “Other expenses” – Credit 10 – materials released for liquidation of fixed assets

https://youtu.be/n3oku11LP3M

It is also possible for a situation where it is discovered that the materials listed in the accounts are actually missing. Those. there is a shortage. For such a case, there is also an accounting entry:

Debit 94 “Shortages and losses from damage to valuables” – Credit 10 – missing materials written off

Registration of write-off of materials

Any business transaction is accompanied by the preparation of a primary accounting document, and write-off of materials is no exception. The step-by-step instructions in the next paragraph contain the study of the primary documents that accompany the write-off process.

Currently, any commercial organization has the right to independently determine the set of documents that will be used to formalize the write-off of materials, so the registration of write-off of materials may vary from organization to organization.

The main thing is that the documents used are approved as part of the accounting policy and contain all the mandatory details provided for in Article 9 of Law No. 402-FZ “On Accounting”.

Standard forms that can be used when writing off materials (approved by Resolution of the State Statistics Committee of October 30, 1997 No. 71a):

- — requirement-invoice (form No. M-11) is applied if the organization has no limits on receiving materials

- — limit-fence card (form No. M-8) is used if the organization has established limits on the write-off of materials

- — an invoice for the release of materials to the third party (form No. M-15) is applied to another separate division of the organization.

The organization can modify these forms - remove unnecessary details and add details that the organization needs.

The invoice requirement is suitable for accounting for the movement of material assets within an organization, between financially responsible persons or structural divisions.

The invoice in two copies is drawn up by the financially responsible person of the structural unit handing over material assets. One copy serves as the basis for the handing over unit to write off valuables, and the second copy serves as the basis for the receiving unit for the receipt of valuables.

Write-off of materials step-by-step instructions if not everything is consumed

Usually, when preparing these documents, it is assumed that the released materials were immediately used for their intended purpose, which means they are accompanied by the postings that we discussed above - for credit 10 of the account and debit 20, 25, 26, etc.

But this does not always happen, especially in large production. Materials transferred to the work site or workshop may not be immediately used in production. In fact, they simply “move” from one storage location to another. In addition, when dispensing materials, it is not always known what type of product they are intended for.

Therefore, those materials that are released from the warehouse but not consumed should not be taken into account as expenses of the current month, neither in accounting nor in tax accounting for income tax. What to do in this case, how to write off materials, step by step instructions below.

In such situations, the release of materials from the warehouse to the production department should be reflected as an internal movement, using a separate subaccount to account 10, for example, “Materials in the workshop.” And at the end of the month, another document is drawn up - a materials consumption act, where the direction of materials consumption will already be visible. And at this moment the materials will be written off.

Such tracking of material consumption will allow you to achieve greater reliability in accounting and correctly calculate income tax.

Please note that this applies not only to materials that go into production, but also to any property, including stationery used for administrative needs.

Materials should not be issued “in reserve”. They must be used immediately.

Therefore, a one-time operation to write off 10 calculators for an accounting department of 2 people, during an audit, will certainly raise questions as to what purpose they were required in such quantities.

Example of a write-off act

That's why:

- - or you issue and immediately write off only what is actually consumed (in this case, the requirement of an invoice is quite sufficient)

- - or you draw up an act for writing off materials (transmitting a demand invoice, and then gradually writing off acts for writing off).

If you use write-off acts, do not forget to also approve their form as part of the accounting policy.

https://youtu.be/jf_bXJI_Lo4

The act usually indicates the name, and, if necessary, the item number, quantity, accounting price and amount for each item, number (code) and (or) name of the order (product, product) for the manufacture of which they were used, or number (code) and (or) the name of the costs, the quantity and amount according to consumption standards, the quantity and amount of consumption in excess of the standards and their reasons.

An example of what such an act might look like is in the picture below. I repeat, this is just an example; the type of act will very much depend on the specifics of the enterprise. Here, as a basis, I took the form of the act that is used in budgetary institutions.

Standards for writing off materials for production

Accounting legislation does not establish standards in accordance with which materials should be written off for production. But in paragraph 92 of the Methodological Guidelines for the accounting of inventories (order of the Ministry of Finance dated December 28, 2001.

No. 119n) states that materials are released into production in accordance with established standards and the scope of the production program. Those.

the amount of materials written off should not be uncontrolled and the standards for writing off materials into production should be approved.

In addition, for tax accounting it would be useful to remember Article 252 of the Tax Code: expenses are economically justified and documented.

The organization sets its own standards for materials consumption (limits) . They can be fixed in estimates, technological maps and other similar internal documents. Documents of this kind are not developed by the accounting department, but by the unit that controls the technological process (technologists), and then they are approved by the manager.

Materials are written off for production in accordance with approved standards. You can write off materials in excess of the norm, but in each such case you need to explain the reason for the excess write-off. For example, correction of defects or technological losses.

The release of materials in excess of the limit is carried out only with the permission of the manager or his authorized persons. On the primary accounting document - the demand invoice, the act - there must be a note about the excess write-off and its reasons. Otherwise, the write-off is illegal and leads to a distortion of the cost and accounting and tax reporting.

Source: https://azbuha.ru/uchet-materialov/spisanie-materialov-poshagovaya-instrukciya/

RђРєS‚ SЃРїРЅРЅРЅРєРїСЂРѕРґСѓРєС‚РѕРІ РїРІРїРЅ‚ания – бланк, образец

НеобходРемость SЃРїРёСЃР°РЅРЅРїСЂРѕРґСѓРєС‚РѕРІ РїРІІ‚ания RјРѕР¶РµС‚ Р±С ‹С‚СЊ вызвана РёС… РёР·РЅР°С‡Р°Р»СЊРЅС ‹Рј браком, порчей, неправильным S…ранением, нарушением транспортировки, окончанием СЃСЂРѕРєР° оодности.

RR»СЏ документального оформления этого процесса РІ Р ±СѓС…галтерском учете предприятий РѕР±С‰РµСЃС ‚венного РїРѕРѕ‚аноЏ, торговли РѕЃРїРѕР»СЊР·СѓРµС‚СЃСЏ “РђРєС‚ Рѕ СЃРїРё SЃР°РЅРёРё товаров» (форма в„–РўРћР Р“-16) РїРѕ РџРѕСЃС‚ ановлению Госкомстата Р РѕСЃСЃРёРё РѕС‚ 12.25.98 N 132.

R'R°R¶РЅРѕ! РЎ 2013 РїРѕРґР° первичные учетные РґРѕєСѓРјРµРЅС‚С‹, РІ РІС… числе С „РѕСЂРјР° РўРћР Р“-16, РЅРµ обязател СЊРЅР° Рє прнмененвв РІ указанном РІ постановлении РІРЅРґРµ.

Предприятиям РЅРµ запрещено SЂР°Р·СЂР°Р±Р°С‚ывать РїСЂРёРјРµРЅС ЏС‚СЊ СЃРІРѕР№ собственный РІРІРґ актР° СЃ отражением РІ нем необходимой онформации для дальнейшего ведения SѓС‡РµС‚Р°.

РџСЂРё обнаружении РІ организации S„акта нал очия S‚овара РЅРµ RєРѕРЅРґРёС†РеРѕРСРЅРѕРіРѕ, Rели утра S‚ившего SЃРІРѕРё RїРѕС‚ребительские S…арактеристики вследствРеРµ неправильного S…ранения, или истечения SЃСЂРѕРєР° оодности, Рели прочих сторонних РѕР±СЃС‚РѕСЏС‚РµР»СЊСЃС ‚РІ, руководителем организации инициируется РїСЂРѕС† едура его СЃРїРѕЃР°РЅРёСЏ, начальным этапом RєРѕС‚РѕСЂРѕР№ являе S‚СЃСЏ выдача приказа Рѕ назначении кнвентаризационной РєРѕРјРёСЃСЃРёРё, которой делегируются полноRјРѕС‡РёСЏ РїРѕ оценке SЃРѕСЃС‚РѕСЏРЅРѕЏ РўРњР¦ офо SЂРјР»РµРЅРёСЏ Р °РєС‚РѕРј количественных объемов SЃРїРёСЃР°РЅРёСЏ, причин, РїСЂРё RІРµРґС€РёС… Рє браку или RїРѕСЂС‡Рµ. Р' отдельных случаях Рє работе над актом RїСЂРёРіР»Р°С€Р°СЋС‚СЃСЏ R є уча стию потребительские, санитарные, пожарные или РёРЅС ‹Рµ контролирующие Рё надзорны Рµ РѕСЂРіР°РСС‹.

Форма РўРћР Р“-16 представляет SЃРѕР±РѕР№ двухсторонний бланк , заполняемый как СЃ С ‚итульной, так Рё СЃ оборотной стороны.

Акт содержит информацию:

- о суммарной стоимости всего объема списанмя;

- Rѕ RїSЂРёС‡РеРЅР°С... утраты RєРѕРЅРґРёС†Реонности.

RўРёС‚ульная S‡Р°СЃС‚СЊ

Р'ланк РўРћР Р“-16 РЅР° обеих сторонах представляет СЃРѕР±РѕР№ таблРецу, РІ РєРѕС ‚РѕСЂСѓСЋ вносятся сведения Рѕ юридических данных предприятнви основанные РЅР° перввичной учетности данн S‹Рµ Рѕ РїРѕСЃС‚СѓРїРёРІС€РёС … Ёпписываемых товарных позициях:

- название предприятия Рё его SЋСЂРёРґРёС‡РµСЃРєРёРµ SЂРµРіРёСЃС‚рациРЕРСРСые РґР°РСРСые;

- основанРеРµ для инвентарРезации (как праввило – приказ, РЅРѕРјР µСЂ дата);

- номер дата формирования документа;

- отметка РѕР± утверждении SЂСѓРєРѕРІРѕРґРёС‚елем организациРe;

- графа 1 — дата поступления РўРњР¦;

- графа 2 — дата списания РўРњР¦ – дата составления акта;

- графа 3.4 — номер дата накладной РѕС‚ поставщика;

- прафа 5 – РїСЂРёС‡РеРЅР° списання – указываются причины СЃРїРёСЃР° РЅРёСЏ товара (“нарушение цеД "остности SѓРїР°РєРѕРІРєРё", "окончание SЃСЂРѕРєР° оодности" Рё РґСЂ .);

- графа 6 — РєРѕРґ РїСЂРёС‡РеРЅС‹ SЃРїРёСЃР°РЅРёСЏ.

Обратная сторона

Оборотная часть S„РѕСЂРјС‹ S‚акже имеет табличный РІРёРґ.

Р' ячейки вносится детальная информация Рѕ списываемых РўРњР¦ СЃ указанием RєРѕР»РёС‡РµСЃС ‚венных Рё ценовых характеристик.

Р' строке "Ртого" ‚СЊ SЃРїРёСЃС‹РІР°РµРјС‹С… РўРњР¦.

- графа 1.2 – названМрµ РєРѕРґ РўРњР¦;

- графа 3.4 – единица измерения S‚оварной позиции Рё ее РєРѕРґ РїР * РћРљР•Р;

- графа 5 – количество мест товарной позиции;

- графа 6.7 – масса РѕРґРЅРѕРіРѕ места товарной позиции (РєРі, нет S‚Рѕ);

- графа 8– цена товарной РїРѕР·РёС†РеРё РІ рублях (цифрами);

- графа 9– стоммость S‚оварной РїРѕР·РёС†РеРё РІ рублях (цифрамРe);

- прафа 10 – примечания РїРѕ товарной РїРѕР·РхрѕрёРё.

После перечисления описания всех списываемых тов арных РїРѕР·РёС†РеР№ РІ столбце 9 РІ СЏС‡ ейке "Ртого" СЊ всего объема списаноЏ РїРѕ всем товарным RїРѕР· которая затем РІ следующей строєРµ SѓРєР°Р·С‹РІР°РµС‚ SЃСЏ РІ РїСЂРѕРїРёСЃРЅРѕРј РІРёРґРµ.

RџРѕРґРїРёСЃР°РЅРёРµ, утверждение Рё дальнейшее RїСЂРёРјРµРЅРµРЅРёРµ

Окончательно сформированныбланк RўРћР Р“-16 подписывают:

- председатель инвентаризацРеРѕРЅРЅРѕР№ РєРѕРјРёСЃСЃРёРё;

- S‡Р»РµРЅС‹ РенвентарРезацРеРѕРЅРЅРѕР№ РєРѕРјРёСЃСЃРёРё;

- материально-ответственная за товарные ценност и персона.

R SѓРєРѕРІРѕРґРёС‚ель организацРеРё RїРѕСЃР»Рµ RѕR·РЅР°РєРѕРјР»РµРЅРёСЏ СЃ обстРѕСЏС‚ельствами акта принимает СЂРµС €РµРЅРёРµ Рѕ том, РЅР° счет RєР°РєРєРє… ресурсов произвести списаРSЅРёРµ более РЅРµ подлежащиС... реализа S†РеРё РўРњР¦, Ренформация RѕР± SЌS‚РѕРј SЂРµС€РµРЅРёРё S‚акже R·Р°РЅРѕСЃРёС‚СЃСЏ R І акт.

После чего документ официал СЊРЅРѕ SѓS‚верждается СЂСѓР єРѕРІРѕРґРёС‚елем SЃ SѓRєR°R·Р°РЅРёРµРј R¤.Р.Рћ., РїСЂРѕСЃС‚ авлением РїРѕРґРїРёСЃРё даты, что SЏРІР»СЏРµС‚СЃСЏ основанием РґР» СЏ физического изъятия некондиционных С‚ оваров РёР· потребительского оборота.

Форма РўРћР Р“-16 размножается RјРёРЅРёРјСѓРј РІ трех РєРѕРїРёСЏС…, Р°РґСЂРµС ЃРѕРІР°РСРСых:

- S„инансовым службам (бухгалтерии) для выполнения SЃРїРёС ЃР°РЅРёСЏ РўРњР¦ СЃ материально-ответственного лица;

- SЃР»СѓР¶Р±Рµ, РЅР° балансе RєРѕС‚РѕСЂРѕР№ находилксь RўРњР¦;

- материально-ответственному R»РёС†Сѓ (например, склад SЃРєРѕРјСѓ SЂР°Р±РѕС‚РЅРёРєСѓ).

RџРѕСЃР»Рµ SѓС‚верждення S„РѕСЂРјС‹ RўРћР R“-16 SЃРїРЃР°РЅРЅС‹Рµ RўРњР¦ более РЅРµ подлежат реализации.

РђРєС‚ РїРѕ форме РўРћР Р“-16 SRЏРІР»СЏРµС‚СЃСЏ основанием для:

- SѓРґРµСЂР¶Р°РЅРЅРёР· зарплаты RІРЅРЅРѕРІРЅС‹С… (РїСЂРё наличии доказател ьства) СЃС‚РѕРёРјРѕСЃС ‚СЊ некондицРеРѕРЅРЅРѕРіРѕ S‚овара;

- Sуписания SѓР±С‹С‚РєРѕРІ РІ бухгалтерском RЅР°Р»РѕРіРѕРІРѕРј SѓС‡РµС‚Р µ РЅР° расходы.

Р'ланк унифицированной формы РўРћР Р“-16 РІ Word-формате можнР* SЃРєР°С‡Р°С‚СЊ беспл атно РІРЅРёР·Сѓ статьи.

RІС‚орая SЃС‚РѕСЂРѕРЅР° бланка R°РєС‚Р° РЅР° SЃРїРёСЃР°РЅРєРµ S‚оваров

​

Cкачать акт списания RїСЂРѕРґСѓРєС‚РѕРІ пвванкя РІ формате word.

Скачать акт SЃРїРєРєР°РЅРєСЏ продуктов РїРІІ РїРєз‚ания РІ формате excel .

Source: https://paperdoc.ru/documents/act/akt-spisaniya-produktov-pitaniya

Order to write off vegetables in dhow | Legal assistance

Assign the following responsibilities to the commission: - inspection of fixed assets, food products subject to write-off; — establishing the reasons for the write-off of objects (physical and moral wear and tear, reconstruction, use, violation of operating conditions, accidents, natural disasters and other emergency situations); — determination of the possibility of further use of individual components, parts, materials of decommissioned fixed assets, their assessment based on the prices of their possible use. 3. Based on the results of the commission’s inspection of the specified objects, draw up an expert opinion of the commission members and draw up an act for writing off fixed assets and food products. 4. The act of writing, approved by the head of the organization, together with technical documentation for fixed assets, is subject to transfer to the accounting department of the organization. Head of MADO No. 2 Ivanova O.G.

If food products have spoiled during transportation, then in this case, in accordance with the order of the manager, a commission is also created, which draws up a report of spoilage f. No. TORG-2 (for imported goods form No. TORG-3).

The act indicates information about the supplier, the dates of dispatch and receipt of the cargo, the date of sending a fax or other document about damage to the products to the supplier, discrepancies in quantity and quality compared to the accompanying documents, a description of the condition of the product, and the signatures of the commission members.

For example, in boxes of cherries, about 20% of the berries show signs of spoilage. In this situation, it is also necessary to draw up an act either according to f.

Sample order for write-off of samples of finished products

The document will be especially useful for food organizations, pharmacies and other companies that deal with perishable goods. Important point! Write-offs cannot be made without the knowledge of the head of the organization.

An order or instruction must be drawn up on his behalf. An important point is the basis for drawing up the act. One column is allocated for it at the top of the document.

In addition to the name of the document, it must contain its number and date of signing.

It contains columns that should contain information about: The reasons for write-off are varied:

When closing an organization, unsold goods are also subject to write-off.

On the second page there is a table that should provide data on:

Online magazine for accountants

Valuables that may be subject to write-off include the following groups:

- All kinds of raw materials.

- Organizational reserves.

- Work in progress products.

- Finished products.

Write-off means that the objects specified in the document will be deregistered, and the document will be considered a justification for this action.

The main thing is that it contains all the necessary data:

- Date and number.

- Reasons for the write-off.

- Link to the preliminary conclusion of the commission.

- The time frame within which the write-off must be made.

- Information about responsible persons.

- Manager's signature.

Accounting for exhibition samples

In this case, you should pay attention to the following points. – a reserve has been created in accounting. The procedure for calculating the markdown of the Tax Code has not been specified; accordingly, when determining its value, the Law on Accounting can be applied.

I believe that a markdown can be recognized as an expense in an amount calculated as the difference between the cost of purchasing samples and the market value. As for the formation of a reserve for reducing the value of material assets for income tax, Chapter 25 of the Tax Code of the Russian Federation does not provide for such a possibility.

At the same time, by virtue of paragraph 4 of clause 4 of Article 264 of the Tax Code of the Russian Federation, non-standardized advertising expenses include expenses for the discounting of goods that have completely or partially lost their original qualities during exposure. The amount of markdown of goods exhibited at the exhibition is recognized in the same month in which the reserve is created.