Photo: unsplash.com Updated: 03/27/2020

The standard child tax deduction is one of the types of social assistance for families with children. The amount of the deduction does not depend on the amount of wages, but depends on the number of children in the family.

A tax deduction allows you to return part of your salary by reducing the amount subject to personal income tax. The benefit is provided to both parents for each child.

The amount of the benefit depends on:

- Number of children in the family

- Age of children

- Presence of children with disabilities in the family

The law sets a limit on the amount of annual deduction. If this is exceeded, from the next month until the end of the calendar year, this benefit is not provided. Also, the amount of the benefit cannot exceed the amount of wages.

This benefit is of a declarative nature, i.e. is provided only after a written request to the employer. Tax deductions occur every month (through the employer) or upon completion of the calendar year and application to the tax authority.

The deduction can be received simultaneously with other social benefits provided for the treatment and education of children.

Conditions of receipt

Tax deductions are provided for children under the age of 18 (24 years for full-time students). You can take advantage of the deduction from the date of birth (adoption) of the child until he reaches adulthood.

If the child was born in October, then the parents can receive the benefit only for 3 months. Moreover, regardless of the month in which the child turns 18 years old, the benefit will be valid until the end of the calendar year.

Who does this benefit not apply to:

- For the unemployed

- For individual entrepreneurs applying simplified types of taxation

The following categories of citizens have the right to receive a tax deduction (clause 4 of Article 218 of the Tax Code):

- Parents and adoptive parents

- Adoptive parents

- Trustees and guardians

If the parents divorced and remarried, then their new spouse also receives the right to benefits, provided that they take part in the financial support of the children.

A parent can receive double the deduction if the second working parent refuses the benefit in favor of the first parent. Divorce is not a basis for granting double benefits.

Double standard personal income tax benefit

Parents and guardians of children under 18 years of age have the right to claim a tax deduction. Some categories of citizens are entitled to a double standard deduction. This is possible if it is received by:

- single mother or father (sole parent or guardian);

- one of the parents, provided that the other refused the deduction. This right applies only to blood and adoptive parents; it does not apply to guardians.

The current legislation of the Russian Federation determines that only working citizens can apply for a tax benefit of this type, from whose salaries 13% is withheld monthly.

It is important to note that if the child’s only parent, regardless of whether it is the mother or the father, gets married, the right to receive a double deduction disappears.

If such circumstances occur, the natural parent and stepmother/stepfather have the right to claim a standard deduction for personal income tax. It is assumed that both spouses will be involved in raising the child, so each of them can count on financial support.

The tax benefit is not doubled if one of the guardians is deprived of parental rights and does not participate in the life of the child. If one of the parents is not employed, the other parent also does not have the right to claim a double standard deduction.

A certain maximum wage is established for the application of personal income tax benefits.

Employed citizens can count on receiving benefits until their earnings reach the established level. For 2020 this is 350,000 rubles.

Standard tax deductions for personal income tax in 2020 for children

The income limit for the annual personal income tax deduction for children in 2020 is 350,000 rubles.

Thus, the benefit is provided until the month until the parent’s official income (before taxes) exceeds this amount. After which the benefit is not provided until the end of the calendar year. Monthly child tax credit in 2020

| Tax deduction, rubles | Parents | To the guardian |

| For the first child | 1 400 | 1 400 |

| For a second child | 1 400 | 1 400 |

| For the third and subsequent children | 3 000 | 3 000 |

| For a disabled child | 12 000 | 6 000 |

| Annual deduction limit | ||

The standard tax deduction is not a cash payment, but a tax benefit.

The standard tax deduction is summed up for all children raised in the family, but the total amount of the deduction cannot exceed the full amount of income tax (cannot be more than the amount of wages).

At birth (adoption), all children in the family are taken into account, except:

- Adults not studying full-time

- Children over 24 years old

- Deceased

If spouses have a common child, as well as a child from previous marriages, then the common child will be considered the third, and the parents will be able to receive a tax deduction for him in the amount of 3,000 rubles.

Example 1: There are three children living in a family, aged 25, 15 and 10 years. Mom’s salary is 20,000 rubles, and father’s salary is 40,000 rubles. The first child is already 25 years old and is not provided with a deduction, but is provided for the second and third child. Thus, the amount of personal income tax deduction in 2020 will be 1,400 + 3,000 = 4,400 rubles. This amount will be deducted from the parents' salary before income taxes are paid. Let's calculate the amount of the mother's personal income tax with and without a deduction for children: (20,000 - 4,400) x 0.13 = 2,028.00 rubles and 20,000 x 0.13 = 2,600 rubles. The difference is 2,600 - 2,028.00 = 572.00 rubles. Thus, both parents will receive an “addition” to their salary in the amount of: 572.00 + 572.00 = 1,144.00 rubles.

Example 2: Continuing with the previous example, let’s calculate how many months the personal income tax deduction benefit will be valid for both parents. According to the law, the benefit is provided for up to a month until the total annual income reaches 350,000 rubles. Therefore, for the mother the deduction will apply all year: 350,000 / 20,000 = 17.50, but for the father it will not: 350,000 / 40,000 = 8.75. The whole number is the number of months during which the benefit is valid.

Standard deductions

The amount of standard deductions depends on the number of children in the family, their age, disability, and full-time study at an educational institution. All the nuances of obtaining are described in Article 218 of the Tax Code of the Russian Federation.

Features of standard deductions

The maximum tax deduction is determined as follows:

- For the first child – 1,400 ₽.

- For the second – 1,400 ₽.

- For the third and subsequent – 3,000 ₽.

- For a disabled child, up to 12,000 rubles of income of parents (adoptive parents) and up to 6,000 rubles of income of guardians (trustees) are additionally exempt from tax.

Please note that the personal income tax refund for a disabled person is provided simultaneously with the regular deduction amount. For example, if a child with health problems was born third in the family, then 15,000 rubles (12,000 + 3,000) of the income of each parent are eligible for the benefit. This does not directly follow from the Tax Code of the Russian Federation. But there is a review of judicial practice dated October 21, 2015 (paragraph 14), where such a court decision is indicated.

Income tax refund is due:

- each of the parents who are officially married;

- each of the divorced parents, if they participate in the financial support of their children (pay alimony);

- guardians, adoptive parents and trustees;

- stepmother or stepfather.

Let me clarify the last point. Children in a family from previous marriages are added together to receive benefits. For example, if a husband has two children for whom he pays alimony, and another one is born into his new family, then the man will receive a deduction for him in the amount of 3,000 rubles, as for a third child. If this is the wife’s first child, then she can count on an income tax exemption in the amount of 1,400 rubles.

If each spouse has children from previous marriages, then upon the birth of a joint child, both husband and wife have the right to exemption from personal income tax of 3,000 rubles of their income.

Conditions that qualify for a standard deduction for children:

- You must be a tax resident of the Russian Federation, i.e. live in Russia for at least 183 days a year, receive an official salary and pay income tax on it.

- The maximum amount of income from which the standard deduction for children is due is 350,000 rubles. As soon as the taxpayer exceeds it, the benefit will cease to apply and tax will have to be paid on the entire amount of earnings.

- The refund is provided only for minor children under 18 years of age or up to 24 years of age if, after school, they continue to study full-time at an educational institution.

Calculation of the amount to be returned

You need to understand that no one will return the amounts mentioned above to the bank account. These are amounts by which the income tax base is reduced.

Example 1. There are two minor children in a family. The husband earns 40,000 rubles per month (480,000 rubles per year), the wife – 30,000 rubles (360,000 rubles per year). Both will exceed the legal limit, but in different months. Husband - in September, wife - in December. We will calculate the refund from the state.

Husband:

- for two children: (1,400 + 1,400) * 8 = 22,400 ₽;

- the savings will be: 22,400 * 13% = 2,912 ₽ per year.

Wife:

- for two children: (1,400 + 1,400) * 11 = 30,800 ₽;

- the savings will be: 30,800 * 13% = 4,004 ₽ per year.

Total per family: 6,916 ₽.

Example 2. Let's say a third child is born in the family from the previous example. He is supposed to reduce his income by 3,000 rubles.

Husband:

- for three children: (1,400 + 1,400 + 3,000) * 8 = 46,400 rubles;

- the savings will be: 46,400 * 13% = 6,032 ₽.

Wife:

- for three children: (1,400 + 1,400 + 3,000) * 11 = 63,800 rubles;

- the savings will be: 63,800 * 13% = 8,294 ₽.

Total per family: 14,326 ₽.

Example 3. Parents give birth to a second child who is disabled. The income of both does not exceed 350,000 rubles per year. The savings for everyone will be:

- (12,000 + 1,400 + 1,400) * 12 * 0.13 = 23,088 ₽ per year.

Example 4. There are three children in a family. The oldest is 25, the middle is 16 and the youngest is 11 years old. Each parent has the right to reduce their taxable income for two minor children:

- 1,400 + 3,000 = 4,400 rubles per month.

Note! The reduction in the tax base begins from the month the child is born until the end of the year in which he turns 18 years old. For example, if a child became an adult in February 2020, then until the end of 2020, the parents’ income decreases every month by 1,400 rubles (if there are no more children).

The following are entitled to double amounts:

- Single parent if the other one is dead or missing.

- A single mother, if there is a dash in the column about the father on the birth certificate.

- A parent who is divorced or has not formalized the relationship. But only if the second one wrote a refusal of his benefit in favor of the first one. At the same time, the second one must also be officially employed and pay income tax on his earnings.

Receipt procedure

To receive benefits you do not need to go to the tax office. Everything is done through the employer's accounting department. If there are several places of work, then the deduction is provided for only one of them, at the payer’s choice.

Documents that will need to be prepared for accounting:

- statement;

- a copy of the birth certificate of one or more children;

- document confirming disability;

- a certificate from an educational institution, if the child is over 18 but not yet 24 years old.

For special cases you will need:

- death certificate of one of the parents;

- a document confirming that one of the parents has been declared missing;

- a copy of the passport page that does not contain a note about the mother’s marriage;

- confirmation of rights to adoption, guardianship, trusteeship.

The accounting department must check and accept documents and calculate deductions. The next year it is not necessary to re-submit the application and certificates (only if conditions change, for example, the birth of children, the death of one of the parents, etc.). The benefit will be extended automatically. If for some reason you did not have time to complete the documents by the beginning of the year, you can submit in any other month. A recalculation will be made.

If an error was made in the accounting department, then for the past 3 years you can apply for a refund of the overpaid tax at the tax office. You will need:

- statement;

- documents similar to those described above;

- certificate of income in form 2-NDFL for those years for which there are accounting errors;

- completed declaration 3-NDFL.

Submission methods: in person, by registered mail or on the tax service website in the taxpayer’s personal account.

How to apply for a tax deduction for a child

There are 2 ways to apply for benefits for children:

- Contacting your employer

- Contacting the tax office

Apply for a tax deduction for children at the place of employment

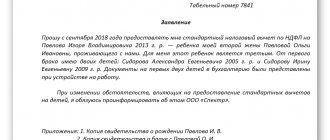

An application is written addressed to the manager, asking for a tax deduction for children. Along with the application, you must submit copies of documents for the children: birth or adoption certificates. In addition to copies of documents, you must show their originals.

If a parent works for several employers, then bring a certificate from other places of work stating that a personal income tax deduction is not provided.

Registration of deductions at the tax office

A parent can personally contact the tax office to receive a tax deduction for children. You need to apply if the parent did not receive benefits from the employer, or received them but in a smaller amount. You can receive the benefit at the end of the calendar year by filing an income tax return with the tax authority at your place of residence.

Procedure for receiving payment:

- Fill out a tax return in form 3-NDFL ()

- Write an application for a tax refund if there is an amount for a tax refund in the tax return

- Obtain a certificate from the employer in form 2-NDFL ()

- Prepare copies of documents confirming the right to a tax deduction

- Submit documents to the tax office at your place of residence; when submitting copies of documents, you must have their originals with you

The tax refund is made within 1 month after filing the application (clause 6 of Article 78 and clause 2 of Article 88 of the Tax Code), but not earlier than the end of the desk audit.

Tax refund methods and deduction procedure

To assign a benefit, it is advisable to act in 2 ways: through the tax office or the employer.

Through the Federal Tax Service

This method is suitable if you require a one-time payment of the entire annual refund amount. The benefit should be issued after the end of the reporting period, for example, the next year after the purchase of living space. To assign a benefit, they submit documentation to the Federal Tax Service at the place of registration: papers can be sent by mail, via the Internet through the taxpayer’s personal account, or delivered in person. Next, all the data provided is checked for several months. If approved, the refund will be credited to the account provided by the recipient.

Through the employer

When using this option, the refund occurs in parts - personal income tax is not withheld from the employee’s salary every month.

IMPORTANT! To receive the benefit, you do not need to wait until next year; accruals can be made already in the current year.

To assign compensation, you need to send a package of documents to the Federal Tax Service in any convenient way: by mail, via the Internet or in person. Within 30 days, the inspectorate will generate a notification of entitlement to the benefit. It must be handed over to the employer, additionally enclosing an application for personal income tax compensation.

Sample application to employer for deduction

List of documents

The list of papers required to receive the benefit depends on the type of deduction. The general list includes:

- passport (copy);

- statement;

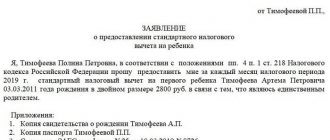

Sample application for deduction to the Federal Tax Service

- Declaration 3-NDFL (not required when issued through an employer);

- income data;

Help 2-NDFL

The list of additional documents includes:

- confirmation of family ties - when returning to children, brothers, sisters, and so on;

- an agreement with a medical enterprise, a copy of its license, receipts for payment for services, a prescription in form 107/u with a note for the tax authorities - when deducting for treatment;

- a copy of the education agreement, the institution’s license, confirmation of payments - for education benefits;

- papers for property, bills or receipts, loan agreement, certificate from the bank about paid interest - in case of property deduction.

Registration of benefits through the Federal Tax Service usually takes about 4 months, the procedure through the employer is faster, and it is possible to receive accruals as early as the next month after the notification from the inspectorate is sent to the enterprise.

Each taxpayer can exercise the right to compensation for their own expenses in the form of a refunded personal income tax. However, one should take into account the terms, features and restrictions on benefits established by law. Before registering it, it is important to be aware of innovations in the regulatory framework regulating the procedure for providing tax deductions.

Claiming the Standard Child Tax Credit

Immediately after the birth or adoption of a child, parents can apply for the standard child tax credit. The application is submitted once and is valid indefinitely. You need to reapply only if your tax deduction rights change, for example:

- An adult child has entered or transferred to full-time study at a university

- Another child has appeared in the family

- One of the children received a disability

- Receiving double payout

- Entering into a new marriage and refusing to receive double benefits

- Transfer to another employer

The tax deduction for children is of an application nature, so to receive it you need to submit an application yourself; the benefit is not granted automatically.

The application for a tax deduction is written in free form; you just need to provide the necessary information:

In the upper right part of the application it is indicated in whose name the application is being written: the name of the company, the position of the manager, and his full name are indicated. All data is written in the dative case. Then the applicant writes information about himself: position and full name. Information is written in the genitive case. Additionally, you can indicate your TIN and registration address in your passport.

Below in the middle of the line is written the name of the document: “Application”.

A request is written on the red line, for example: I ask you to provide me with a tax deduction for children...

In order of birth of children, their full name and date of birth are listed.

After the request is fully written, a list of documents confirming the right to a tax benefit and attached to the application is indicated. The list is indicated in the form of a list, with each document on a separate line. At the end of the line, the number of sheets for each attached document is indicated.

At the bottom of the application, the date of application is written and the applicant’s signature is placed.

If a parent wants to receive a double tax deduction, then this must be indicated in the application and the basis for receiving it must be stated, for example:

- Absence of the second parent (with supporting document)

- Refusal of the second parent's right to benefits (application from the other parent and 2-NDFL certificate from his place of work)

Classification of deductions

There are several types of benefits used in the Russian Federation. Their terms and conditions are specified in the relevant articles of the Tax Code of the Russian Federation.

Table 1. Regulatory framework

| View | Article of the Tax Code of the Russian Federation |

| Property | 220 |

| Standard | 218 |

| Social | 219 |

| Investment | 219.1 |

| Professional | 221 |

Property

Due to transactions carried out by a citizen with property:

- its sale;

- acquisition of living space or a share in it;

- construction of housing or purchase of a plot of land for this purpose;

- acquisition of property from a taxpayer for government needs;

- the cost of repair work if the housing is taken with a rough finish.

The maximum return amount per year is measured by the personal income tax transferred for the year. Then the balance is carried over to the next year and so on until the limit determined by the state is exhausted. In this case, it is allowed to take a deduction at any time, but only funds for the previous 3 years are subject to reimbursement.

IMPORTANT! Non-working people who have recently retired and bought housing can also take advantage of the benefit. They receive a refund for the previous period (3 years previous to the transaction), when they carried out work activities and tax deductions. Employed pensioners can additionally receive benefits further if the maximum deduction amount is not reached during the payment period.

Conditions for assigning a personal income tax refund:

- To qualify for the exemption, the property must be residential. Its location in Russia is a must. If the purchased non-residential premises are converted into residential premises, the deduction will be denied.

- The maximum benefit value is defined as 13% of 2 million rubles (260 thousand). Returns are only possible once in a lifetime. However, if there is a shortfall, it is allowed to use the balance in the future on the next purchase of property. For example, if a citizen purchased living space for 1.7 million rubles, he is entitled to a deduction of 221 thousand rubles. Since the limit has not been spent, he can use the remainder (39 thousand rubles) in the future.

- The limit when registering premises under a loan agreement is 13% of 3 million rubles (390 thousand rubles). Such personal income tax compensation for interest on targeted loans for the purchase of property can be used only once and for one object. If the mortgage interest cap is not used up, the balance is forfeited.

- Maternity capital is not refundable. For example, living space was purchased for 2 million rubles, but part of it was paid for by maternal capital in the amount of 400 thousand rubles. In this case, the deduction is assigned from 1.6 million rubles.

- The benefit is not provided if the property was acquired at the expense of the state, employer, or purchased from relatives, subordinates and other interdependent citizens (Article 105.1 of the Tax Code of the Russian Federation).

The use of a property deduction is advisable not only when purchasing, but also when selling property. The limit for housing is 1 million rubles, for non-residential areas, cars, garages - 250 thousand. If a person sells property that is in his possession for less than a certain period of time, he is obliged to pay 13% of the income.

IMPORTANT! According to innovations in legislation, from May 1, 2018, the period of minimum ownership of residential space has been increased to 5 years. However, for property purchased before 2020, or as a result of a gift, under a maintenance agreement with a dependent, recently privatized, the period remained the same (3 years).

No personal income tax is collected on residential space worth less than 1 million rubles

When transferring 13% of sales, you can take advantage of a fixed deduction, reducing the taxable portion. For example, in 2020, a citizen sold a property purchased in 2020 for 1.5 million. Since the ownership period has not passed (5 years), he must transfer 13% of the income or 195 thousand rubles to the state. If you use the deduction, you can reduce the amount by 1 million, that is, the tax will be: (1.5 million-1 million) * 13% = 50.7 thousand rubles.

Video - Property deduction in 2020

https://youtu.be/eS87mswv81w

Standard

The benefit allows you to reduce the amount of tax on a monthly basis. It is mainly appointed through the employer, but personal application to the Federal Tax Service is also acceptable.

Table 2. Standard tax deductions

| Reason for granting the benefit | Amount, rub. | Peculiarities |

| Event participants | ||

| “Chernobyl survivors”, liquidators of man-made accidents, disabled people of war and WWII | 3000 | If there are conditions for assigning 2 payments, choose the most beneficial option for the citizen |

| Heroes of the Russian Federation, USSR, participants in wars, WWII, disabled people of groups 1 and 2, childhood (Article 218 clause 2 of the Tax Code) | 500 | |

| For a child under 18 years old | ||

| On the 1st and 2nd | 1400 | Paid monthly until the amount reaches 350 thousand rubles. The amount of the benefit is doubled for a parent who is raising a child alone or if the other has refused it |

| On the 3rd and onwards | 3000 | |

| For a child with a disability up to 18 years old, for a student, graduate student, intern, and so on up to 24 years old with a disability of 1st and 2nd groups | 12,000 for parents, 6,000 for guardians | |

For example, a citizen is raising a 10-year-old daughter alone. A woman’s salary is 50 thousand rubles. She is due a double deduction for 1 child. She filed an application for her intention to take the benefit in January. The deduction will reach the maximum amount (350 thousand) in 7 months, that is, from January to July, the benefit is deducted from her income and only after that the tax is calculated. The savings during this time on personal income tax payments for a woman will be: (1400*7 months*0.13)*2=2548 rubles.

Video - Standard deduction for children

https://youtu.be/fut9_wCpKfc

Social

The benefit is primarily aimed at partial reimbursement of costs for education and medical treatment, as well as for the formation of a future pension and charity. The maximum amount of all social deductions is 120 thousand rubles. Due to personal income tax reimbursement, compensation for medical care is provided:

- Own treatment of the child or parents, including in a clinic, inpatient settings, paid institutions.

- Stay at health resorts. The benefit is provided only for expenses of one’s own funds, and not of state or trade union ones.

- Dental services: treatment and prosthetics (non-cosmetic).

- Spending on drugs.

- Costs of voluntary health insurance (if the policy is paid for by the employee and not by the employer).

IMPORTANT! To issue a refund, the medical institution must be located in the Russian Federation and have a state license. It is necessary to keep the contract for the provision of services and confirmation of payment. Medicines are indicated on form 107/у.

Form 107-1/у

The peculiarity of the deduction for medical treatment is the possibility of receiving benefits without a limit on its value. This applies to some expensive drugs and treatments. Their list is presented in Decree of the Government of the Russian Federation No. 201 of March 19, 2001.

Section 1. Anesthetics and muscle relaxants (RF Government Decree No. 201)

For example, a citizen underwent surgery for 1 million rubles. If the operation is indicated in the list defined by law, this amount is deducted from the person’s income, and personal income tax is payable on the balance. But if a negative result is obtained, when cash receipts are lower than the costs of treatment, the citizen is required to return all tax withheld for the period.

Social deductions also include tuition reimbursement:

- Own - any education is taken into account, including distance education, correspondence or abroad. But the establishment must provide a license for its activities.

- Your own or a sponsored child under 24 years of age. Only full-time education is allowed.

- Brother or sister under 24 years of age. Also, only full-time studies are taken into account.

The benefit does not include the education of spouses, uncles, aunts and other relatives. The maximum amount of return for your studies, a brother or sister is 120 thousand, for your own or a child under your care - 50 thousand rubles.

A deduction for financing a future pension is assigned to citizens making contributions:

- in NPF;

- to insurance institutions (life insurance for a period of over 5 years, pension).

At the same time, it is possible to form your own pension contributions for your spouse, parents, or disabled child.

Citizens who make donations to charitable institutions and non-profit organizations have the right to take a deduction for charity.

IMPORTANT! The benefit is not assigned above 25% of a person’s income for the year.

For example, a citizen transferred 200 thousand rubles to charity. For the year, a person’s income was 400 thousand. The benefit cannot be more than 400 thousand * 25% = 100 thousand rubles. Refund amount = 100 thousand * 13% = 13 thousand rubles. The deduction is not assigned if:

- contributions not to charitable institutions, but to funds organized by them;

- assistance with goods and services, rather than cash (provision of premises, advertising, etc.);

- transfers to individuals.

Professional

This type of deduction is considered separate because it is primarily provided to entrepreneurs. Acting as an individual and making deductions from cash receipts, he has the right to use the benefit. The following may qualify for a professional return:

- Individual entrepreneurs staying under the general taxation regime (OSNO);

- practicing notaries, lawyers, etc.;

- taxpayers registered under civil law contracts;

- citizens receiving rewards in the field of art, culture, science;

- self-employed citizens (since 2020, a pilot project has been operating in 4 regions of our country).

Refunds are made for the full amount of costs confirmed by relevant documentation (payments, contracts).

IMPORTANT! Sometimes, if it is impossible to demonstrate expenses for individual entrepreneurs, the deduction rate is set at 20% of income. Self-employed citizens have their own deduction: they do not pay tax until the amount of the calculated fee is 10 thousand rubles.

For some types of remuneration, the legislation defines cost standards.

Costs for various types of activities (clause 3 of Article 221 of the Tax Code of the Russian Federation)

Investment

This type of return is assigned:

- For proceeds from the sale of securities, if a citizen has owned them for more than 3 years. The benefit does not apply to transactions made on an IIS (individual investment account).

- From income contributed over 3 years to IIS. The limit is 400 thousand rubles, that is, 13% of this amount (52 thousand rubles) is allowed to be reimbursed per year. The benefit is intended for people who are employed and have a “white” salary.

- From proceeds from trading in securities carried out on an individual investment account for 3 years. The peculiarity of the benefit is that it can be used by self-employed, unemployed people without reference to salary.

Documents for tax deduction for children

It is easier to apply for a tax deduction from an employer, who will act as an intermediary between you and the tax service.

Documents that must be provided to confirm your right to a tax benefit:

- Child's birth certificate (adoption or guardianship documents)

- Certificate of disability (for disabled children)

- Certificate from the university indicating full-time study (for children over 18 years old)

- Conclusion and divorce of parents

- Certificate 2-NDFL from the place of work of the other parent (provided monthly), for one of the parents to receive a double deduction

- Documents confirming that there is one parent (depending on the reason): Death certificate of mother or father

- Extract from the court decision declaring a parent missing

- Birth certificate of a child that does not contain information about the father

- A document confirming that the parent is not officially married (passport)

Deprivation of parental rights of one parent does not imply the absence of the other parent. If a parent is deprived of rights, but financially supports the children (there is documentary evidence), then the parent has the right to a tax deduction.

Termination of the “children’s” deduction

Stop giving deductions when one of the following conditions occurs:

| Condition | Month from which no deduction is allowed |

| The employee's income exceeded RUB 350,000. | Month in which the employee's income exceeded the limit |

| The child has turned 18 years old | January next year |

| A full-time student, graduate student, resident, intern, student is 24 years old. The child did not stop studying until the end of the year | January next year |

| A full-time student, graduate student, resident, intern, student is 24 years old. The child stopped studying by the end of the year | Next month after graduation |

| Full-time student, graduate student, resident, intern, student who stopped studying before reaching 24 years of age | Next month after graduation |

If you find an error, please select a piece of text and press Ctrl+Enter.