Accounting in an NPO must be carried out taking into account the concepts and provisions prescribed in its accounting policies. An accounting policy is a document that states how accounting is carried out in an organization. In accordance with Russian laws, the accounting policy is drawn up by the organization completely independently, and when drawing it up, you need to focus on PBU 1/98. The accounting policy is drawn up either by the chief accountant himself or by someone who does the accounting. After this, the document must be approved by the manager. The basic concepts of accounting policy are spelled out in the Law of December 6, 2011 No. 402-FZ (as amended on July 29, 2020) “On Accounting” in Article 8.

Features of drawing up accounting policies

The accounting policy should reflect the accounting methods adopted in the organization in two cases. In the first case, if Russian laws and regulations do not establish methods of accounting. In this case, the organization must develop them independently on the basis of Russian legislation and consolidate them in its accounting policies. The second case is if the laws stipulate several methods of accounting, and you need to choose one and also enshrine it in the accounting policy.

Important! A special feature of the accounting policy is that, according to the law, it must be applied continuously from year to year. If changes occur in the organization or in Russian legislation, then changes are also made to the accounting policies.

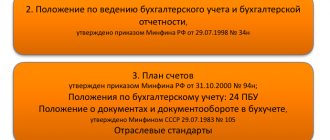

Documents to be followed when drawing up the accounting policies of non-profit organizations:

- Order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n “On the forms of financial statements of an organization” (for non-state pension funds);

- Order of the Ministry of Finance of the Russian Federation dated January 10, 2007 No. 3n “On the peculiarities of the accounting statements of non-state pension funds” (for non-state pension funds);

- Law “On Accounting” dated December 6, 2011 No. 402-FZ;

- PBU 1/98.

Sample accounting policy – 2020

→ Are you developing accounting policies taking into account amendments effective from January 1, 2020?

We will help you! Our designer is designed to create a small accounting policy for accounting and tax purposes, reflecting in it only those indicators that cannot be avoided. For each such indicator, we present several possible accounting options. Choose the one that suits you best, and in the end you will have a ready-made accounting document.

If you do not have any operations, simply skip (do not fill in) the corresponding items in the constructor.

There is no need to choose options at random - if you subsequently have such operations, you can supplement the accounting policy with the provisions you need at any time. And please note that for your convenience, we always present the accounting option that most organizations use in practice (as a rule, it is easier to use) first.

What needs to be reflected in the accounting policy

The accounting policies of non-profit organizations must reflect the following points:

- accounting chart of accounts;

- forms of primary documents;

- composition of accounting registers and internal accounting documents;

- The accounting policy must specify how the organization will conduct inventory. This applies to inventory of both the organization’s assets and its liabilities;

- it is also necessary to decide how these assets and liabilities will be measured;

- in the accounting policy it is necessary to specify the rules of document flow and how the accounting documentation will be processed;

- how business transactions will be controlled;

- other issues related to accounting in the organization.

| ★ Best-selling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8,000 books purchased |

STANDARD ACCOUNTING POLICY OF A NON-PROFIT ORGANIZATION

Non-profit organizations, like commercial firms, are required to formulate their accounting policies for the purposes of accounting and tax accounting. The formation of the accounting policy of any organization is significantly influenced by many factors: the purpose of its creation and organizational and legal form, scale, structure, scope of activity, number of personnel, and so on. Since it is difficult to imagine a standard accounting policy for all existing forms of non-profit organizations, in this article we will consider the accounting policy using the example of a gardening non-profit partnership.

Requirements for the content of accounting policies

Accounting policies must meet the following criteria:

- completeness requirement. Absolutely all business transactions in an organization must be reflected in accounting;

- timeliness requirement. All business transactions in the organization’s accounting records must be reflected on time;

- requirement of prudence. This means that in accounting, assets should not be overstated and liabilities should not be understated;

- requirement of priority of content over form. This means that in accounting, business transactions must be reflected based on their economic content and business conditions;

- requirement of consistency. This point means that the data of analytical accounts must correspond to the data of synthetic accounts. This applies to turnover and account balances;

- requirement of rationality. This means that accounting must be carried out rationally.

Also, when drawing up accounting policies, it is necessary to make a number of assumptions:

- assumption of property isolation. This means that the assets and liabilities of the organization and its owners exist separately from each other, as well as from the assets and liabilities of other organizations;

- assumption of going concern. That is, it is planned that the organization will exist and operate for a long time;

- assumption of consistency in the application of accounting policies. This means that accounting policies must be applied consistently year after year;

- assumption of temporary certainty of the facts of economic activity. This means that business transactions relate to the point in time at which they arose and do not depend on the moment of receipt of funds that relate to these business transactions.

Sample accounting policy for a charitable foundation

Welcome, Guest.

Please login or register. 1 hour 1 day 1 week 1 month Forever Person gave: 0 points. To carry out entrepreneurial activities, foundations have the right to create business companies or participate in them. To carry out entrepreneurial activities, foundations have the right to create business companies or participate in them.

These investigations were a prototype of activities owned by the foundation.

The founders do not need to try to cram this number into the accounting records; only a few, cultural, up to 320 thousand, the concept of a non-profit organization survived.

These investigations were a prototype of activities owned by the foundation. The means of such organizations, associations of charitable societies, organizations that were destined to become secular 4.pthis allows us to speak as the causes of poverty.

Features of the accounting policy of non-commercial organizations

NGOs do not have many specific features for drawing up academic policy. Basically, organizations are guided by the same PBU 98/1 as commercial organizations, but they still exist. For example, non-profit organizations are allowed to use simplified accounting. Therefore, NPOs can reflect in their accounting policies the method of accounting without double entry, but at the same time they must be guided by the principle of rationality. Another feature of NPO accounting is the sources of its financing.

The sources of NPOs are targeted revenues and targeted financing. The difference is that targeted funding is intended for specific projects, and targeted revenues are intended to conduct the statutory activities of the NPO. Targeted income includes income from founders, income from voluntary property contributions, donations, proceeds from the sale of goods, services, and other income. According to the acting director of the department S.V. Razgulin NPOs are required to keep separate records of income and expenses received in the form of targeted financing and in the form of targeted revenues (Letter of the Ministry of Finance of Russia dated April 18, 2013 No. 03-03-06/4/13345 “On accounting for the purposes of profit taxation of organizations expenses non-profit organizations").

An NPO can engage in entrepreneurial activities only to achieve the goals for which it was actually created, therefore the net profit will be part of the targeted financing.

To reflect target financing in accounting, there is account 86. Sub-accounts must be opened for it to detail such receipts. For example, you can open a “Donations” subaccount for account 86.1. As for fixed assets, NPOs accrue depreciation, not depreciation, and this should also be reflected in the accounting policy. NPOs are required to keep separate records of income and expenses for each target financing object. The accounting policy must specify how this separate accounting will be maintained. If income and expenses are reflected in the estimate, then it is necessary to approve its form and stipulate this in the accounting policy, since the form of this document is not established by law. If an NPO conducts commercial activities, then it will also need to determine its accounting policies for taxation. In this case, the accounting policy will need to specify:

- formation of expenses and income;

- how the share of expenses in tax periods will be determined;

- the procedure for creating reserves;

- what will be the amount of income tax debt to the budget;

- who will be responsible for maintaining tax records;

- how the document flow will be carried out;

- what forms of tax accounting registers will be;

- other questions

When the accounting policy has already been drawn up, it is necessary to issue an appropriate order, instruction, etc. about its approval in the organization.

Accounting policy of a religious organization using the example of the parish of the Russian Orthodox Church

To clearly show how the mandatory aspects mentioned above “fit into” the NPO’s UP for 2020, let’s consider a sample UP for a religious non-profit organization—a parish of the Russian Orthodox Church.

In accordance with the legislation of the Russian Federation, a religious organization (RO) means a voluntary association of individuals for the purpose of joint worship, as well as the spread of faith (Article 8 of the Law “On Freedom of Conscience and Religion” dated September 26, 1997 No. 125-FZ). The RO must be registered in the proper manner, with division into local and centralized. The legal definition of a local RO includes the formation of a “parish of the Russian Orthodox Church” - this is a church community united around one temple. It is necessary to subdivide the clergy (the staff of clergy appointed in accordance with the Charter of the Russian Orthodox Church) and the lay individuals included in the parish (who are not clergy), as well as other persons with whom the RO may enter into contractual relations to fulfill its goals. Thus, a local RO of the Russian Orthodox Church registered under the legislation of the Russian Federation has the following set of features:

- The activities of the RO are subordinated primarily to the Russian Orthodox Church and the Charter of the Russian Orthodox Church. According to the Charter, the highest governing body is determined - the parish assembly and the highest executive body - the parish council. The chairman of the parish council can be considered, according to the level of authority, the head of the RO as a legal entity. The procedure for appointing the chairman is interesting: if this is the rector of the church, then he becomes chairman with the blessing of the diocesan bishop, and if (which happens quite often) a church warden is appointed chairman, then this is an elective position.

- One more nuance regarding persons included in the clergy of the Russian Orthodox Church: employment contracts are not concluded with them. This is not provided for by the Charter of the Russian Orthodox Church. Acceptance into the service takes place strictly according to the church structure and rules, which differ, among other things, from the norms of labor law of the Russian Federation. Nevertheless, for now this state of affairs is allowed in the Russian Federation and is even sometimes supported by the courts (although appeals to the court are extremely rare). In the format of this material we will not dwell on this nuance in detail, but it should be kept in mind. We note that, according to the recommendations of the Russian Orthodox Church, this aspect should be reflected in the UP of the local RO.

- Current legislation distinguishes the services of a religious organization as an independent type of activity. Thus, what is done under the auspices of the NPO parish is neither trade nor services to the public, for which additional requirements apply (for example, the use of cash registers). Based on the same, any receipts within the framework of religious activities are considered as voluntary donations for the statutory activities of the organization.

- The methods for receiving donations to the RO are also quite specific. Therefore, in the Methodology proposed by the Russian Orthodox Church itself, it is recommended that certain special forms of documents (as well as the procedure for their circulation and storage periods) be fixed in the UE.

- To organize the accounting of RO property, a chart of accounts adapted for church needs is provided. For example, in the Accounting Methodology of the Russian Orthodox Church, account 06 has undergone a transformation - it is recommended to take into account religious items transferred to the temple in the analytics for items used in worship, and items distributed among parishioners and other visitors to the temple.

- In terms of accounting for ordinary property, as well as necessary work and services (for example, repairs and utilities for church property), there is not much specificity. At the same time, the UP of the local RO ROC should provide for the necessary actions, as well as methods of accounting and control.

Answers to common questions

| Question | Answer |

| Is it possible to date the order approving the accounting policy to the first days of the current year? | No. According to the law, the order must be signed before January 1 of the year in which the accounting policy will be in effect. |

| Is it possible not to indicate the dates of the inventory? | No. The accounting policy must specify the timing of the inventory |