Home — Documents

Organizations registered this year and wishing to use a simplified taxation system from the beginning of their business activities, like all other organizations already applying this special tax regime, in accordance with Art. 2 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting” are required to keep accounting records in full. Before Law No. 402-FZ came into force, simplified organizations were required to keep accounting records only of fixed assets and intangible assets (Clause 3, Article 4 of Federal Law No. 129-FZ of November 21, 1996 “On Accounting”).

The reason for this exception was that, according to Art. 346.12 of the Tax Code of the Russian Federation did not have the right to apply a simplified taxation system for organizations for which, in particular, the residual value of fixed assets and intangible assets, determined in accordance with the legislation of the Russian Federation on accounting, exceeds 100,000,000 rubles. If before January 1 of this year, the “simplified” people were still asking the question about the need to draw up an accounting policy, now all doubts on this matter have disappeared. The set of ways an economic entity maintains accounting records constitutes its accounting policy. An economic entity independently forms its accounting policy, guided by the legislation of the Russian Federation on accounting, federal and industry standards (clauses 1 and 2 of Article 8 of Law No. 402-FZ). The basis for the formation of accounting policies for accounting purposes is contained in the Accounting Regulations “Accounting Policy of the Organization” (PBU 1/2008) (approved by Order of the Ministry of Finance of Russia dated October 6, 2008 N 106n). PBU 1/2008 provides a more expanded definition of the organization's accounting policies. This is understood as the set of accounting methods adopted by the organization - primary observation, cost measurement, current grouping and final generalization of the facts of economic activity (clause 2). The choice of one of the options for accounting methods for specific transactions proposed by regulatory documents, independent development of accounting methods and justification for deviations from the requirements of regulatory documents constitute the accounting policy of the organization.

Since to calculate the tax paid when using the simplified tax system with the object “income reduced by the amount of expenses”, the norms of Chapter. 25 “Organizational Income Tax” of the Tax Code of the Russian Federation, which, in turn, also provide for accounting options, then the simplified tax accounting policy of organizations with the specified object is also necessary.

Most often, the simplified taxation system is used by organizations with a small accounting staff (mostly only the chief accountant), so these organizations have a natural desire to simplify and bring together accounting and tax accounting as much as possible. Unfortunately, this is not always possible. Although for small businesses, including “simplified” ones, there are more opportunities, since they may not apply a number of accounting provisions, and they also have special provisions for the application of certain norms from individual PBUs, which make it possible to bring accounting and tax accounting closer together. (The criteria for classifying an organization as a small business are given in Article 4 of the Federal Law of July 24, 2007 N 209-FZ “On the development of small and medium-sized businesses in the Russian Federation.”)

Therefore, the accounting policy of the “simplified” person should begin with a list of regulations on the basis of which he will conduct his accounting. In addition to the aforementioned Law N 402-FZ, it should include the following regulations:

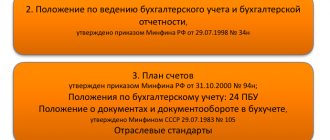

- Regulations on maintaining accounting and financial statements in the Russian Federation (approved by Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n);

- Chart of accounts for financial and economic activities of organizations and Instructions for its application (approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n);

- list of accounting standards that will be used in accounting;

- Information of the Ministry of Finance of Russia N PZ-3/2012 “On a simplified system of accounting and financial reporting for small businesses”;

- methodological instructions and recommendations issued by the Ministry of Finance of Russia and other ministries and departments necessary in the work of the organization (this phrase can simply be transferred to the accounting policy without listing the instructions and recommendations).

Naturally, if both accounting and tax accounting policies are combined in one order, then the main tax document - the Tax Code of the Russian Federation - should also be indicated.

The accounting policy also specifies the persons responsible for organizing and maintaining accounting records. These are:

- manager - for organizing accounting, compliance with the law when performing business transactions and storing accounting documents (Article 7 of Law No. 402-FZ);

- chief accountant - for maintaining accounting records (Article 7 of Law No. 402-FZ) and developing accounting policies (clause 4 of PBU 1/2008).

We remind you that according to clause 3 of Art. 7 of Law N 402-FZ, an agreement on accounting can be concluded with an organization or specialist, and in small and medium-sized enterprises the manager can keep records independently. This should be taken into account when assigning responsibilities.

Paragraph 4 of PBU 1/2008 stipulates that, along with the selected accounting methods, the following are approved:

- a working chart of accounts containing synthetic and analytical accounts necessary for maintaining accounting records in accordance with the requirements of timeliness and completeness of accounting and reporting;

- forms of primary accounting documents, accounting registers, as well as documents for internal accounting reporting;

- the procedure for conducting an inventory of the organization’s assets and liabilities;

- methods for assessing assets and liabilities;

- document flow rules and accounting information processing technology;

- the procedure for monitoring business operations;

- other solutions necessary for organizing accounting.

The accounting policy should approve all primary documents used by the organization (clause 4, article 9 of Law N 402-FZ). This applies both to unified forms of primary documents approved by the resolutions of the State Statistics Committee of Russia, and to those independently developed. After all, unified forms of primary documents are no longer mandatory for use.

“Simplified” should also consolidate in the accounting policy the choice of option for accounting reporting forms, because Order of the Ministry of Finance of Russia dated July 2, 2010 N 66n for small businesses provides the right to choose between:

- common reporting forms;

- simplified general forms;

- forms intended only for small businesses.

From our point of view, for “simplified” people who have a small amount of accounting, it is preferable to use forms intended for small businesses.

Another mandatory element of accounting policy is the fixation of the selected object of taxation - “income” or “income reduced by the amount of expenses”.

In the next section “Methodology for maintaining accounting and tax records” of the accounting policy, you should list the accounting elements that the “simplified” will apply.

Accounting registers

Since 2013, the forms of accounting registers have been approved by the head of an economic entity on the recommendation of the official responsible for maintaining accounting records (clause 5 of Article 10 of Law No. 402-FZ).

Registers are selected in accordance with the chosen form of accounting:

- if accounting is kept using a computer program, then the registers provided in this program are used (the most common option);

- With a journal-order accounting system, journals-orders are used;

- with the memorial system, memorial orders are used;

- with a simplified accounting system for small enterprises - a book of business transactions without using (simple form) or using property accounting registers (given in Appendices No. 1 - No. 11 to the Standard Recommendations for organizing accounting for small businesses, approved by Order of the Ministry of Finance of Russia dated December 21, 1998 N 64n).

Article 346.24 of the Tax Code of the Russian Federation provides for only one version of the tax accounting register - this is the Book of Income and Expenses of organizations and individual entrepreneurs using a simplified taxation system (approved by Order of the Ministry of Finance of Russia dated October 22, 2012 N 135n). At the same time, clause 1.4 of the Procedure for filling out the income accounting book provides for the possibility of maintaining it both on paper and in electronic form. It is this choice that should be consolidated in the accounting policy.

https://youtu.be/V2ZtNrl0R1g

What is included in the UE on the simplified tax system “Income minus expenses”

The accounting policy for any special regime differs from the UP of companies on OSNO. The list of items that need to be included in it is significantly reduced. But there are a number of points that cannot be ignored.

Here's what you need to indicate in the UP for accounting purposes:

1. List references to laws, regulations and articles that the company follows when keeping records. 2. Specify the programs that will be used to automate accounting. 3. Prepare and include in the text of the document or attachment the forms of the applicable primary documentation, accounting registers and internal reporting documents. 4. Develop and approve a working chart of accounts with analytical and synthetic accounts that will most fully correspond to the activities of the organization. 5. Include provisions on the procedure for conducting an inventory of liabilities and assets. 6. Approve methods for assessing assets and liabilities. 7. Describe the document flow procedure. 8. Reveal methods of internal control over the correctness and legality of business operations. 9. Establish criteria for determining the level of materiality.

This is what is indicated in the UE for tax accounting purposes:

1. The person or department responsible for maintaining tax records - accounting, chief accountant, etc. 2. The object of taxation is the difference between income and expenses. 3. The tax rate - if it differs from the generally accepted 15% in accordance with regional legislation. 4. The procedure for maintaining KUDiR and programs for accounting automation. 5. The procedure for accounting for depreciable property:

- indicate what property is recognized as a fixed asset;

- data from which accounting accounts are used to determine its value;

- how the initial cost of the operating system and its retrofitting are reflected in KUDiR.

6. The limit on fixed assets is 100,000 rubles for 2020. 7. Methods for evaluating goods. 8. Procedure for writing off OS. 9. Procedure for accounting for raw materials and supplies:

- what is included in inventory costs;

- how the cost of goods for sale is calculated;

- How sold goods are accounted for and written off.

10. Cost accounting procedure. 11. The procedure for accounting for losses and calculating the minimum tax. Here describe your right to recognize past losses in the current year.

To create a good accounting policy, take into account all changes in legislation. Use international standards, laws, and regulations as a guide. You can familiarize yourself with samples of accounting policies that are available on the Internet and are suitable for your taxation system and type of activity. For example, in the Kontur.Accounting service there are examples of UE suitable for different enterprises at a simplified tax rate of 15%.

Methods of accounting for income and expenses

Most organizations take into account income and expenses in their accounting on an accrual basis (Section IV of the Accounting Regulations “Income of the organization” (PBU 9/99) and “Expenses of the organization” (PBU 10/99), approved by Orders of the Ministry of Finance of Russia dated 05/06/1999 N 32n and N 33n respectively).

But there is an exception to this rule. Paragraph 9 clause 12 PBU 9/99, para. 2 clause 18 PBU 10/99 and sec. The 4 mentioned Model Recommendations allow small businesses to keep records of income and expenses using the cash method. Features of accounting under the cash method of accounting are explained in the Standard Recommendations.

For the purposes of calculating tax according to the simplified tax system ch. 26.2 of the Tax Code of the Russian Federation (Article 346.17) stipulates that “simplers” keep records of income and expenses only on a cash basis.

As you can see, regulatory legal documents allow the “simplified” to use the cash method in both accounting. However, such a choice will not reduce the accountant's work. The fact is that in some cases there are more differences between accounting using the same method than when using different methods of accounting for income and expenses.

So, for example, in accounting using the cash method, material expenses are recognized subject to their payment and write-off as expenses, and in tax accounting using the cash method, only the fact of payment is sufficient for their recognition.

The procedure for approving and changing accounting policies

The accounting policy is drawn up by the chief accountant and approved by the manager. If we are talking about an organization that is already operating, then it is necessary to adopt the UE for the next year before December 31 of the current year.

There is no need to re-approve the UE every year if no changes have occurred. But you can do this too, by specifying such a requirement in the current UP.

If the organization has just been created, it is obliged to publish and approve the UP before the first reporting, but no later than 90 calendar days from the date of state registration.

Changes to an already approved UE are made in several cases. But whenever changes occur, they will come into force only from the new reporting year, unless the changes that occur require otherwise (clause 12 of PBU 1/2008) and are not related to the fact that:

- the legislation of the Russian Federation has changed;

- the organization intends to use new methods of accounting;

- The core activities of the organization have changed.

Organizations with a common accounting system make all changes related to changes in the management program retrospectively. But for organizations that use simplified accounting and accounting, there is a nuance. They can reflect in the accounting system the consequences of changes in the UE prospectively, unless otherwise required by law (clause 15 of PBU 1/2008).

Subscribe to our newsletter

Read us on Yandex.Zen Read us on Telegram

Accounting for low-cost assets that meet the criteria for fixed assets

It is necessary to determine how low-cost assets will be accounted for - as part of inventories or fixed assets, as well as this “boundary” cost (clause 5 of the Accounting Regulations “Accounting for Fixed Assets” (PBU 6/01), approved by Order of the Ministry of Finance of Russia dated March 30, 2001 N 26n).

It is better to choose as the “boundary” value the minimum cost of fixed assets specified in clause 1 of Art. 256 of the Tax Code of the Russian Federation, - 40,000 rubles. (it is also now proposed in clause 5 of PBU 6/01). In this case, accounting for inventories will be the same for both accounting and simplified taxation.

New accounting policy for 2020

The accounting policy is created once (within 90 days after registration of the company) and continues to be applied continuously - from year to year. There is no need to change the new accounting policy annually, but at the same time it may be necessary to make amendments and additions to it.

Amendments to the document are allowed only before the start of the next reporting period (year) and require certain grounds. These include:

- changing the methodology for any section in order to optimize accounting;

- changing the scope of the company’s activities, reorganization and similar procedures;

- changes in legislation in the field of tax and accounting (from the moment they come into force).

By the way, this was precisely the reason for the current amendments: in 2017, changes were adopted to PBU 1/2008 “Accounting Policies of the Organization.”

At the same time, the addition of the UE is not limited. When new types of activities appear and new items requiring accounting are added, there is no need to wait until the beginning of the next year: they can be entered and applied at any time.

Although the accounting policy does not need to be submitted to the tax authorities for approval, it may well be requested by the inspector during the audit.

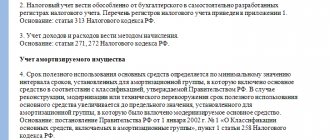

Depreciation of fixed assets and intangible assets

Clause 18 of PBU 6/01 provides for the following methods of calculating depreciation on fixed assets:

- linear method;

- reducing balance method;

- method of writing off value by the sum of the numbers of years of useful life;

- method of writing off cost in proportion to the volume of products (works).

To calculate depreciation of intangible assets, clause 28 of the Accounting Regulations “Accounting for Intangible Assets” (PBU 14/2007) (approved by Order of the Ministry of Finance of Russia dated December 27, 2007 N 153n), the following methods are provided: linear method, reducing balance method, write-off method proportional to the volume of products (works).

For the purposes of calculating tax according to the simplified tax system ch. 26.2 of the Tax Code of the Russian Federation does not provide alternatives in accounting for expenses for the acquisition (construction, production) of fixed assets, for their completion, additional equipment, reconstruction, modernization and technical re-equipment, for the acquisition (creation by the taxpayer himself) of intangible assets. Such expenses are recognized in accordance with clause 3 of Art. 346.16 Tax Code of the Russian Federation.

A decision should be made to revaluate fixed assets and intangible assets or to abandon it in accounting (clause 15 of PBU 6/01, clause 16 of PBU 14/2007).

Method of writing off raw materials and supplies

Clause 16 of the Accounting Regulations “Accounting for Inventories” PBU 5/01 (approved by Order of the Ministry of Finance of Russia dated 06/09/2001 N 44n) provides for the following valuation options when releasing inventories into production and otherwise disposing of them:

- at the cost of each unit;

- average cost;

- the cost of the first acquisition of inventories (FIFO method).

For the purposes of calculating tax according to the simplified tax system, material expenses are taken to reduce income received in the manner prescribed for calculating corporate income tax, Art. 254 of the Tax Code of the Russian Federation (clause 2 of Article 346.16 of the Tax Code of the Russian Federation). Paragraph 8 of this article provides for the following assessment methods when writing off raw materials and supplies used in the production (manufacturing) of goods (performance of work, provision of services):

- by cost per unit of inventory;

- average cost;

- cost of first acquisitions (FIFO);

- cost of recent acquisitions (LIFO).

Costs for delivery of goods

Clauses 6 and 13 of PBU 5/01 provide for options for accounting for costs for the procurement and delivery of goods to the organization’s warehouse:

- their inclusion in the cost of goods (account 41 “Goods”);

- accounting for them as part of sales expenses (account 44 “Sales expenses”) and writing them off in proportion to the sale of goods.

For the purposes of calculating tax under the simplified tax system , expenses directly related to the sale of goods, including costs of storage, maintenance and transportation, are taken into account as expenses after their actual payment (clause 2, clause 2, article 346.17 of the Tax Code of the Russian Federation). Accounting for these expenses does not depend on accounting for goods.

But even if the “simplifier” chooses the same option in both accounts (not including these expenses in the cost of the goods), it will not be possible to minimize the accountant’s work. Indeed, in accounting, the costs of procuring and delivering goods should be distributed between goods sold and those remaining in the warehouse.

Accounting for interest on debt obligations

The accounting regulations “Accounting for expenses on loans and credits” (PBU 15/2008) (approved by Order of the Ministry of Finance of Russia dated October 6, 2008 N 107n) provide a choice only to small businesses. According to clause 7 of PBU 15/2008, small enterprises have the right to choose to recognize all borrowing costs as other expenses or other expenses, with the exception of that part of them that is subject to inclusion in the cost of the investment asset.

For the purposes of calculating tax according to the simplified tax system ch. 26.2 of the Tax Code of the Russian Federation provides for the possibility of accounting for interest paid for the provision of funds (credits, borrowings) for use (clause 9, clause 1, Article 346.16 of the Tax Code of the Russian Federation). Such interest in accordance with clause 2 of Art. 346.16 of the Tax Code of the Russian Federation are taken into account in the manner prescribed for calculating corporate income tax, Art. 269 of the Tax Code of the Russian Federation. By virtue of this norm, interest expenses are accepted for accounting within the calculated limit. There are two ways to calculate it:

- within 20% of the average level of interest paid on debt obligations issued in the same quarter on comparable terms. Debt obligations issued on comparable terms mean debt obligations issued in the same currency for the same terms in comparable amounts, against similar collateral;

- within the limits of the refinancing rate of the Bank of Russia, increased by 1.8 times - when issuing a debt obligation in rubles and a coefficient of 0.8 - for debt obligations in foreign currency.

What is impossible to do without when drawing up an accounting policy?

When registering NUP for individual entrepreneurs on the simplified tax system (income), the main section will be devoted to the algorithm for forming the taxable base for the simplified tax system and the features associated with the procedure for recognizing income.

At the same time, it is not at all necessary to copy verbatim from the Tax Code of the Russian Federation into this paragraph of the NUP the list of income to be taken into account when calculating tax. It is important to distinguish between sales income and non-operating income, as well as indicate non-accounted income based on the actual activities of the individual entrepreneur.

In the NUP, you can detail the nuances of income accounting in the context of the following analytics:

- by type of activity used;

- by methods of receiving income (receiving money at the cash desk, to a current account, income in kind, when paying with bills, etc.).

The NUP may also reflect:

- formulas for calculating advance payments and the amount of the final payment for the simplified tax system;

- reporting procedure;

- tax payment deadlines;

- other nuances (features of tax calculation and registration of KUDiR when receiving money as a refund of erroneously transferred amounts, etc.).

Other accounting policies

These include:

- the procedure for accepting inventories for accounting in accounting. The chart of accounts provides two options: according to the actual cost of their acquisition (procurement) on account 10 “Materials” or at accounting prices (the possibility of using additional accounts 15 “Procurement and acquisition of material assets” and 16 “Deviation in the cost of material assets”). In tax accounting - only at actual cost;

- the procedure for creating a reserve for doubtful debts in accounting (clause 70 of the Regulations on accounting and financial reporting);

- procedure for correcting significant errors in accounting. It is necessary to determine which errors will be considered significant. Small businesses have the right to choose a method for correcting them: in the general procedure provided for by the Accounting Regulations “Correction of Errors in Accounting and Reporting” (PBU 22/2010) (approved by Order of the Ministry of Finance of Russia dated June 28, 2010 N 63n), or in the order established for minor errors, that is, in correspondence with account 91 “Other income and expenses” and without retrospective recalculation (i.e. prospectively) (clause 9 of PBU 22/2010).

Organizations using the simplified tax system and UTII also need to develop a procedure for separate accounting of income and expenses under these special tax regimes. If it is impossible to divide, distribute in proportion to the shares of income in the total amount of income received when applying the specified special tax regimes (clause 8 of Article 346.18 of the Tax Code of the Russian Federation).

The given list of accounting policy elements is not exhaustive. Each organization must take into account the nuances of its activities and provide for the procedure for taking them into account in its accounting policies.

Accounting policies of organizations using a simplified taxation system

The question of whether business entities that have switched to a simplified tax system should formulate and disclose (approved by order of the manager) accounting policies for accounting and tax purposes is debatable.

Vasiliev V.N. Material from the journal “Accountant Consultant” Clause 3 of Article 4 of the Accounting Law establishes that organizations that have switched to a simplified taxation system are exempt from the obligation to maintain accounting records, with the exception of accounting for fixed assets and intangible assets. In addition, paragraph 4 of Article 346.11 of the Tax Code of the Russian Federation establishes that for organizations applying the simplified taxation system, the current procedure for conducting cash transactions is maintained. Fulfillment of this requirement also presupposes the organization of accounting according to universal accounting rules. Chapter 26.2 of the Tax Code of the Russian Federation directly establishes the obligation of organizations that have switched to a simplified taxation system to organize and maintain tax records - in accordance with Article 346.24 of the Tax Code of the Russian Federation, taxpayers that have switched to the simplified tax system are required to keep records of income and expenses for the purpose of calculating the tax base for taxes in the accounting book income and expenses of organizations and individual entrepreneurs using a simplified taxation system, the form and procedure for filling out which are approved by the Ministry of Finance of the Russian Federation. There is no requirement to formulate an accounting policy for tax purposes in Chapter 26.2 of the Tax Code of the Russian Federation. However, as a general rule, one of the main goals that is achieved by developing an accounting policy is to consolidate the choice of one of two or more options for accounting for assets, liabilities or elements that form the tax base. In other words, in the case where it is possible to choose the method of forming the tax base or accounting for individual transactions, the development of an accounting policy seems, at a minimum, appropriate.