In this article we will tell you what to do after paying off your mortgage to the bank. The end of the mortgage loan payment is a joyful event for every borrower. But making the final payment (either ahead of schedule or in accordance with the schedule) does not automatically complete the entire real estate purchase transaction. There is a need to settle a number of formalities. Following the correct sequence of actions will help to avoid possible troubles in the future.

Algorithm for interaction with the bank

Payments for all types of loans (including mortgages) are made to the credit institution according to the schedule. The borrower can follow it by paying the required amounts of money on certain dates. But it is also allowed to increase payments and repay the loan ahead of schedule. In the latter case, the interest amount is recalculated in favor of the borrower.

Next, we’ll figure out what to do if the client is ready to make the last mortgage payment.

In a situation where the client wants to pay the bank early, it is necessary to notify the lender of his intention in advance. This can be done:

- during a personal visit to a credit institution, writing a statement in the established form;

- by calling the bank's hotline;

- by making an early payment through your bank’s personal account online.

Notification is required in order for the remaining debt to be recalculated and the payment schedule to be adjusted. It will also be the basis for complete write-off of the deposited amount, because Simply depositing funds into an account is not enough.

Then you need to make a request to receive an account statement. It is recommended to receive this document in person rather than paying the amount of the last payment according to the words of a bank employee.

The human factor cannot be ruled out: a manager may make a mistake or provide incomplete information. When making the final payment, you should take into account the obligatory amount, commissions and the interest component for any late payments.

There are often cases when a borrower simply forgets to make a payment on time (for example, if he splits it into parts over the course of a month) and does not attach due importance to this. In most cases, a mortgage is a long-term loan, so the underpayment of even a small amount can increase quite significantly over time.

The statement contains complete information necessary both to calculate the final payment amount and to resolve disputes with a credit institution.

Next, all that remains is to deposit the amount of money necessary to fully repay the debt. So, the client has paid off the mortgage - what to do next? All that remains is to order a certificate from a credit institution confirming the absence of debt obligations. The document can be either paid or issued free of charge. It contains the following mandatory information:

- date of issue of this certificate of absence of debt;

- Client's full name;

- the date of full payment of the debt, indicating the number and date of conclusion of the agreement;

- no claims from the credit institution against the borrower;

- position and full name of the person who signed the document.

The certificate is certified by the bank's seal and can be presented at the place of request.

Afterwards, you should make sure that the loan account is closed. Most credit institutions close it automatically after making the last payment. But if this does not happen, then you need to write a corresponding statement indicating the fulfillment of obligations. It must be accompanied by either payment documents or the above-mentioned certificate of absence of debt.

After 2-4 weeks, send a request to the credit history bureau (BKI) to be sure that the data on the paid mortgage is correct and the financial obligations are properly fulfilled.

Expert advice

Before paying off your mortgage and removing the encumbrance, you need to know several important nuances. Let's talk about them.

- When you make your final mortgage payment, check where your mortgage currently stands. If the document is in the same bank branch where you took out the mortgage, it will be issued quickly. But if the mortgage is stored in the bank's central vault, the timing of its issuance may be delayed. Banks often sell mortgages to other financial institutions. Therefore, it is necessary to clarify who the current mortgagee is and find out the date the mortgage was issued.

- If you are paying off your mortgage early, ask your bank when the funds will be debited from your account. On the standard monthly payment date or early write-off is possible, upon request. Some banks close the loan early only on the monthly payment date. For example, the borrower makes payments on the 20th of each month. If the borrower deposited funds to fully repay the mortgage on the 5th, the bank will write it off only after 15 days.

- Contact the head of the bank branch with a request to close the mortgage at a time convenient for you. Of course, not every bank will meet you halfway and issue a mortgage, but it’s worth a try.

- If you have been issued an electronic mortgage, you will not have to do anything further. Once the mortgage is paid off, the mortgage is automatically cancelled.

- For any questions, read the legislation. The main laws in this area are laws No. 102-FZ “On mortgage (pledge of real estate)” and No. 122-FZ “On state registration of rights to real estate and transactions with it.”

Encumbrance of a property

The last payment has been paid in full, what to do next after paying off the mortgage? Until the encumbrance on the property is removed, it cannot be fully disposed of at your own discretion. Purchasing an apartment with borrowed funds does not interfere with living or short-term rental. But legally significant actions (sale, exchange, donation, rent, long-term lease, etc.) are impossible, because A mortgage is one of the types of encumbrances. What to do after paying off the mortgage for an apartment? Remove the encumbrance.

Recommended article: How to reduce or increase your mortgage payment

Encumbrance of collateral real estate

Any transaction with a mortgaged apartment is complicated by the fact that the bank places an encumbrance on the property. The essence of this legal procedure is simple: the lender wants to be sure that after concluding the contract, the client will not be able to sell the mortgaged home without the knowledge of the bank. Even if the borrower finds a buyer, Rosreestr will refuse to register the transfer of ownership of the mortgaged apartment, bypassing the credit institution.

If necessary, the encumbrance can be removed until the loan is fully repaid under certain conditions. This happens when a bank client wants to repay the loan ahead of schedule using funds from the sale of a collateral apartment. Transactions with collateral real estate are not uncommon; registration schemes have already been worked out. Therefore, you should not be prejudiced when buying an apartment with a mortgage - the bank controls the legality of the borrowers’ actions.

Procedure for removing the encumbrance

Most often the algorithm looks like this:

- pay off the debt in full, taking into account the balance and possible additional payments;

- obtain a certificate of no obligations from the bank;

- write two applications - one demanding the removal of the encumbrance, the second about the issuance of a mortgage;

- obtain a mortgage with the necessary records;

- cancel it at the registration authority (Rosreestr);

- pay state fees (in some cases);

- receive a current extract from the Unified State Register of Real Estate with no record of the presence of an encumbrance (in this case, a mortgage) on the property.

It should be borne in mind that a mortgage can be issued either with or without a mortgage. Let's consider both options.

What to do after paying off your mortgage to the bank if you have a mortgage

The mortgage regulates the relationship between the borrower and the institution that issued the loan for the purchase of real estate. It outlines all the characteristics of the lending object and the conditions for providing a mortgage loan. The mortgage is designed to protect the interests of the lender. With its help, if the borrower fails to fulfill the obligations, the housing can be sold.

What to do after closing a mortgage? Contact a banking organization with a request to issue a mortgage. This procedure consists of several stages:

- drawing up an application requesting the issuance of this security;

- processing of the request by the credit institution;

- execution of an act of acceptance and transfer of the mortgage;

- issuance of the document to the applicant.

The waiting time for a document varies from several days to a month.

In accordance with the legislation of the Russian Federation, a mortgage must be issued immediately after the borrower fulfills its obligations. But most credit institutions even indicate a period of 14-30 days in the mortgage agreement. This is due to the fact that paper is most often stored at the head office of a banking organization, which, in turn, may be located in another city/region. Therefore, it takes some time to process the request and transfer the document to the applicant.

The borrower receives the original from the credit institution; issuing a copy of the mortgage note is not allowed. The back of the document must contain the following marks:

- date of final payment and exact amount of funds;

- fulfillment of the client's obligations in full;

- absence of claims against the borrower and mortgagor.

After receiving the security (i.e., mortgage), you need to contact the registration authority to complete the procedure for removing the encumbrance.

What to do with the mortgage after paying off the mortgage

What to do after paying off the mortgage if the mortgage was not issued

In this case, a joint application for the removal of the encumbrance is drawn up. It is signed by the borrower and the banking organization. It also indicates the facts of repayment of obligations and the absence of claims from the creditor. A bank employee (usually a lawyer) is sent to the registration authority at the same time as the borrower.

What to do after removing the mortgage encumbrance if maternity capital was used

In practice, there are situations when the removal of the encumbrance is not the final stage of the real estate acquisition procedure. Most often this refers to the operation of purchasing a home using funds/part of maternity capital funds.

If these funds were raised (down payment or repayment), then, in accordance with the legislation of the Russian Federation, there is a need to allocate shares to children and spouse. There also remains the possibility of redistributing shares in the future. For example, another child was born, and the shares between existing owners need to be reduced in order to allocate a new one.

Recommended article: Mortgage guardianship

The law does not directly indicate what exactly the minimum allowable share size should be. But if we take the existing norm of housing area per individual, then it is 12 square meters. meters. If the area of the apartment does not allow the specified footage to be allocated, then the sanitary standard of 6 sq.m. should be taken into account.

After the last payment is paid and the encumbrance on the housing is cancelled, the borrower/s have six months to allocate shares. The following methods are possible:

- execution of the relevant agreement or gift agreement;

- in court (in case of disputes about the size of shares).

The agreement/contract is drawn up by a notary. He, in accordance with the latest changes in legislation, will send documents for registration electronically. At the end of the procedure, each owner is given an extract from the Unified State Register, which indicates the size of his share.

You should know that not all family members can become homeowners when raising money from maternity capital. For example, children born in a previous marriage, but not adopted in a new one, will not be allocated shares. The same applies to the spouse if the relationship is registered after the birth of children and receipt of a Pension Fund certificate. Each case is individual, so it is recommended to get advice from a notary office.

List of documents

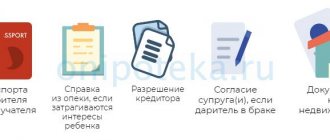

In most cases, the applicant must provide:

- passport of the borrower/co-borrower;

- a certificate or letter from a banking organization confirming full fulfillment of obligations;

- statement of the loan account;

- mortgage (if it was issued);

- power of attorney from a banking organization for actions to remove the encumbrance (if a bank employee does not accompany the borrower);

- title documents for housing (sale and purchase agreement, certificate of ownership);

- credit (mortgage) agreement;

- application for removal of encumbrance (if there are several borrowers, then a document from each is required);

- a receipt confirming the fact of payment of the state fee (in some cases, see below).

All documents are presented in originals and copies (one at a time). The list may be supplemented depending on the individual situation.

For example, there was an assignment of rights of claim, a broker was involved in the procedure for removing the encumbrance, real estate was purchased under a DDU or a military mortgage. The procedure for removing the encumbrance is free. The encumbrance record is canceled within:

- 3 working days – in accordance with the general procedure and in the absence of comments on the package of documents;

- 5 working days – if housing was purchased under the DDU;

- 5-10 working days – if you contact the MFC (multifunctional service center).

At the end of the procedure, the applicant (borrower) receives an extract from the Unified State Register of Real Estate, which does not contain the fact of the existence of an encumbrance.

Removing mortgage encumbrances - instructions

Mortgage repayment

Loan payments can be made strictly according to schedule, or you can close the debt ahead of schedule. In the second option, the borrower must notify the credit institution of his decision by writing an application. Beforehand, it is better to check with the credit institution the exact amount that needs to be repaid. This can be done either by phone or at a bank branch by requesting a statement.

After making the last payment, you must obtain a certificate from the bank confirming that there is no debt. This official paper is not a mandatory document, but may come in handy in the future. Depending on the bank, the certificate is issued for a fee or free of charge. It should contain the following data:

- Full name of the borrower;

- details of the contract and the date of repayment of the debt;

- own details (number, date of provision);

- position of the bank representative who signed the document;

- a phrase stating that the bank has no claims against the borrower.

You also need to make sure that the mortgage account is closed. Some lenders do this automatically, others only upon application.

Where to go to remove the encumbrance

In some cases, borrowers are not faced with the question: after paying off the mortgage, what should they do next? For example, Sberbank performs the procedure for removing encumbrances automatically for its clients. All formalities associated with paperwork are kept to a minimum.

A number of credit institutions also do everything on their own, without involving the borrower in the procedure, so you should clarify the possibility of providing this service. If you decide to remove the encumbrance on your own, you can contact:

- Rosreestr by sending a valuable letter by mail or submitting an application through the form on the official website;

- having visited the MFC, for this you need to clarify the cadastral number of the housing in advance (this information is on the Rosreestr website);

- use the State Services portal to receive services remotely. An electronic signature is required for each applicant.

The choice of method of application depends on the individual situation of the applicant/applicants. Is an extract from the Unified State Register needed in principle, in printed or electronic form, is a person willing to incur additional costs if documents are sent by mail, is there an electronic signature, etc.

Recommended article: Is it profitable to take out a long-term mortgage and why?

Possible problems and nuances

To avoid getting into a difficult situation, it is necessary to take into account all the nuances regarding the closure of a mortgage agreement:

- It is imperative to make the final payment after finding out the exact amount of the debt, from the bank’s point of view. Otherwise, a penny debt may result in a large fine.

- Close the current account to which monthly contributions were transferred so as not to pay for its maintenance.

- If the client does not agree with the statement of the amount of debt, it is better to pay it. And only then figure it out and, in case of overpayment, write an application for the return of the overpayment.

- It is necessary to go through the procedure for removing the encumbrance. Otherwise, when the need arises to carry out some actions with real estate, it will be impossible to do so.

- In case of loss of the mortgage note, the mortgagee shall draw up a duplicate of it in full compliance with the original. And if, after repayment of the debt, a lost one is found, it will not have legal force.

- If the loan was repaid ahead of schedule, you can demand the return of part of the insurance.

An important point - check that the bank employee involved in the document certification procedure has a power of attorney for the operation.

Possible expenses

If the bank does not provide this service automatically, then you can perform this procedure yourself. There are a number of factors to consider that influence additional costs:

- If you contact an intermediary (for example, a mortgage broker or real estate agent), you will need to issue a notarized power of attorney and pay for his services. Approximate costs can be up to 10,000 rubles.

- When sending documentation by mail (valued letter or express delivery), you must have each document certified by a notary and pay for delivery. This creates a risk of loss or damage to the shipment. Costs can range from 1,000 to 5,000 rubles.

- Upon receipt of a current extract (or certificate) from the Unified State Register of Real Estate, it becomes necessary to pay a state fee.

Let us repeat that the service of removing the burden itself is free. But a fee will be charged if you need to order:

- extract from the Unified State Register of Real Estate in electronic format – 250 rubles;

- paper extract from the Unified State Register of Real Estate – 400 rubles.

It should be noted that as of July 2021, Rosreestr no longer issues a certificate of ownership. In 2021, the owner can receive an extract from the USRN, which will replace both the certificate and the extract from the USRN. The extract is indefinite, but requires updating before each legally significant action. The document is ordered again for the current date.

What documents are needed

Before contacting Rosreestr, the apartment owner must prepare a package of documents. It includes:

- original mortgage note;

- a letter from the bank confirming debt repayment, it must be on company letterhead;

- passports of all owners;

- power of attorney from the bank representative who signed the mortgage;

- contract of sale;

- certificate of state registration;

- application for lifting restrictions;

- receipt of payment of state duty. It is paid if an extract from the Unified State Register is required, without marks of encumbrance;

- loan agreement – not required in cases where a bank specialist accompanies the client.

Sometimes the mortgage is not processed. In such situations, a joint application to lift restrictions is submitted to Rosreestr, and the presence of a bank employee is also required.

Information about the termination of a mortgage should be freely available on the Rosreestr website.

Insurance return

Real estate insurance when applying for a loan/mortgage is a significant cost item for a mortgage loan. Is it possible to return part of the funds if the borrower repays the debt ahead of schedule and the policy is paid before the end of the loan agreement?

The answer depends on the situation. Insurance under a personal contract (with the drawing up of a policy) differs from the same procedure under a collective agreement. The borrower often does not see the last document, receiving only general insurance rules. In this case, you should familiarize yourself with the full terms and conditions of the insurance.

The policy can be issued for the entire period of the mortgage loan, for example, for 20 years, or you can pay for insurance for a certain period of time (a year or several months). If the mortgage was repaid not in 20, but in 10 years, and the policy was paid for the entire period of the loan, then you can return the money for the unused period, i.e. exactly half. If there was no early payment, then nothing can be returned. In this case, the absence of insurance cases does not matter.

Applying for a mortgage is a significant step, and you should carefully consider your financial capabilities and risks. If there is a possibility of quick or early repayment, then it is advisable to issue a policy annually or quarterly. A complete refusal of insurance can lead to either an increase in the rate or to litigation even after the loan is issued.

To return part of the insurance in the event of paying off a loan/mortgage ahead of schedule, you need to write a corresponding application to the company providing insurance services. In the application you should indicate the details where to transfer the money if you agree to a refund. All the same documents must be attached to it as for removing the encumbrance (see above) along with the contract and insurance policy. In case of unlawful refusal, it is recommended to go to court.

Removal of encumbrance: independently or through intermediaries?

The whole procedure can take a lot of time. Collecting documents, waiting for the papers to be ready, visiting the bank and the registration authority - these stages of registration will require strength and patience. Those who do not want to waste time on paperwork can turn to lawyers or realtors who provide such services.

In order to close a loan agreement through intermediaries, you will need to issue a power of attorney from a notary.

Based on this document, the specialist will be able to represent the interests of the property owner in the bank and in the registration authority. He will prepare all the documents and carry out the necessary procedures to remove the encumbrance from the apartment.