Does the bank check the apartment when applying for a mortgage?

Banks organize only a minimal verification of documents; the buyer will have to take care of the legal purity of the transaction on his own. Before executing a mortgage agreement, the lender is presented with documents that he studies:

- Preliminary purchase and sale agreement (PSA).

- Extract from the Unified State Register of Ownership of the seller.

- Technical passport.

- The document on the basis of which the seller acquired the right of ownership: an old deed of ownership, a certificate of inheritance, an agreement of exchange, rent or gift.

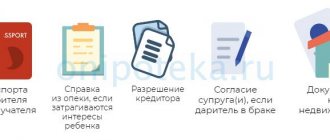

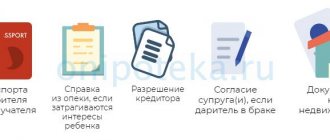

- Other documents depending on the situation: consent of the seller’s spouse for the sale, permission from the guardianship authority.

Important! The submitted documents are checked by the bank's lawyers. If everything is in order with them and the apartment is without encumbrances, the deal will be approved. It makes no difference to the lender whether the seller used capital to purchase the home, whether shares were allocated, or whether there are third parties who can lay claim to it.

Take the survey and a lawyer will tell you for free how to avoid mistakes in an apartment purchase and sale transaction in your case

Do banks check the legal purity of mortgaged real estate?

A financial organization, when issuing financial loans to citizens, must check their solvency. Since the purchased property serves as collateral for the loan, the bank carries out mandatory underwriting (verification) of mortgage housing. The purpose of the procedure is to confirm the current market value and verify information related to the condition of the object. The lender is interested in ensuring that the home, if necessary, can be sold quickly and at a good price. Checking an apartment by Sberbank for a mortgage comes down mainly to assessing the liquidity of the property and identifying problems that could lead to the cancellation of the purchase and sale transaction.

How does Sberbank check an apartment for a secondary mortgage?

Sberbank and most other banks do not check the legal purity of the transaction. Usually only a few things become clear:

- Market value of real estate. An appraisal is performed to determine the size of the mortgage. Usually, no more than 80% of the price of the apartment is given, the rest must be paid by the borrower from the down payment.

- Submitted documents. Authenticity and absence of encumbrances are checked.

- Redevelopment. If they are not legalized, the mortgage will be refused.

- The seller's ownership of the home. This is confirmed by an extract from the Unified State Register.

In fact, the bank checks only superficially the mortgaged property; a detailed check of the owner (seller) is not carried out. He will not be asked for a certificate from a psychoneurological dispensary; they will not find out whether he is involved in the bankruptcy procedure, they will not check the history of the transfer of ownership.

Buying an apartment with a mortgage through Sberbank

Receipt for receipt of a deposit, collateral, advance payment upon purchase or sale of an apartment

How long does the verification procedure take?

Financial institution specialists begin the inspection after preliminary approval of the loan and provision of documentation for the purchased property. The answer to the question of what Sberbank lawyers check depends on the type of housing. If the loan is intended for the purchase of a secondary property, bank employees analyze the technical documentation for the purchased object, verify information from Rosreestr, and study the house register. The purchase of housing in a new building is accompanied by an inspection of the developer company. To ensure that the development is legal, permission is sought from the seller.

When purchasing housing on the secondary market, three parties are involved in the mortgage transaction: the bank, the borrower and the owner of the property being purchased. The main document is the purchase and sale agreement, drawn up taking into account that the purchased property will remain pledged to the lender until the loan is fully repaid. In addition, the seller must provide the financial institution with a package of documents for the purchased property, including:

- proof of ownership;

- the document that served as the basis for obtaining rights to the immovable property;

- extract from the Unified State Register of Real Estate;

- consent to sale from husband or wife;

- refusal of other owners if the property is in shared ownership;

- permission to sell from guardianship authorities, in the presence of minor children or incapacitated owners.

The consent of the spouse and the refusal of the shared owners are formalized by a notary. The buyer needs to assess the market value of the property and provide the bank with the results. The procedure is carried out by an organization accredited by Sberbank.

How long does it take for the bank to verify an apartment's mortgage?

Let's consider how much the bank checks the apartment and the borrower for a mortgage:

- First, the borrower submits an application. The response is received within 5-30 minutes, the mortgage is pre-approved.

- The client brings his own documents to the lender, they are checked immediately. But it also happens that the answer is given only after 2-3 days.

- The property is located, the documents for it are submitted to the bank. The verification takes on average 5-7 days. At this time, the market value is also assessed.

- If everything is fine, the lender approves the transaction and the main contract is signed.

In total, obtaining a mortgage and purchasing real estate takes one month. On average, it takes 7 days to check the apartment itself.

Are you tired of reading? We’ll tell you over the phone and answer your questions.

How long does it take for Sberbank to review an application?

Sberbank enjoys well-deserved popularity among the population for processing mortgage loans. Indeed, low interest rates, fast loan terms, ongoing promotions and discounts attract many borrowers.

A pleasant bonus, in addition to preferential lending conditions, is the minimum processing time for an application. Officially, this period ranges from 2 to 5 working days. In practice it can change significantly.

If the client is not satisfied with the lender regarding the quality of the credit history, adequacy of income or other important factors, then the bank usually makes a negative decision almost immediately. This usually happens at the scoring stage using a special program.

If a potential borrower passes the scoring test, his application is submitted for consideration. The underwriting department is involved in the analysis. They are the ones who carefully check the client’s reliability and the absence of significant risks if the client enters into a loan agreement.

Practice and reviews from existing clients indicate that the average time to make a decision for each borrower is up to two business days. The bank itself is interested in speeding up interaction with the client and processing all paperwork, so there are practically no openly negative reviews about delays in mortgage consideration. The exception is the inspection of the property. It can drag on for a very long time and is not always the fault of the borrower.

If such are found, then usually the reason is hidden in the borrower himself - either the package of documents was not completely collected, or errors were made in the application form, or there were other nuances.

The period for considering a property for a mortgage may already be quite long because... verification of all documents is required. Usually it takes 2-3 days, but it can take longer if a mortgage is issued on a house and land.

What do banks not check when issuing a mortgage?

The bank checks the apartment with a mortgage only for obvious violations, in which case it cannot approve the transaction. For example, if the redevelopment is not legalized or the property is pledged. There are other disadvantages that lenders do not pay attention to:

- Debt for housing and communal services.

- Registered citizens.

- Condition of the house.

Let's look at how to check everything yourself.

Debts for housing and communal services

If the seller has utility debts, they will not be transferred to the new owner. But he may encounter problems: for example, resource-providing organizations do not care that the debt was not caused by the buyer, and his water or electricity supply may be turned off.

It’s easy to check an apartment for the absence of debts; just ask the seller for a certificate from the HOA or management company. The bank does not require it.

Registered citizens

Registration in an apartment gives the right of residence. If the seller does not register relatives before or after the transaction within the established time frame, the buyer will have to come to terms with their presence in the premises, or have the registration canceled through the court.

To check the absence of registered persons, you need to request an extract from the house register from the seller. It is registered in the HOA or management company.

Condition of the house

It is important for the bank that the house is not considered to be in disrepair: by law, mortgages on apartments in dilapidated buildings are prohibited, and besides, this is a risk for the lender. If the apartment is not in a dilapidated building, but the electricity is constantly cut off, pipes are leaking, there is no hot water supply, these are just troubles for the borrower: the bank is not interested in such shortcomings.

You can check the condition of the house yourself. There is no point in asking the seller: his goal is to sell the home, and he will only show the positive aspects. You can ask your neighbors or invite a specialist who understands the technical details and can identify possible shortcomings.

Property check

The speed of verification is influenced by many different factors. The credit committee requests information from the house register, which lists the persons registered in the house. If children are registered in the premises, the housing transaction will require written approval from the guardianship authorities.

The right of ownership to a share of residential premises is retained by persons who are missing or in prison. Persons being treated in a psychiatric hospital cannot be discharged from their apartment. This rule also applies to dependents who are supported by the landlord.

How do banks check a mortgage borrower?

Unlike checking an apartment for a mortgage, potential borrowers are given much more attention.

What does the bank do:

- Checks credit history. If it is not there at all, there is a chance that the mortgage will not be approved, or the minimum amount will be issued. If your credit history is damaged, the likelihood of a positive decision is close to zero. It is optimal when the client already had loans and all of them were repaid on time.

- Examines debt load. If there are outstanding loans, they are taken into account when calculating the total mortgage amount and monthly payments. Banks try to ensure that in total, no more than 50% of their salary is spent on repaying all loans from clients. If there are too many loans, your mortgage may be denied.

- Checks the salary level. It is confirmed by certificates, for individual entrepreneurs – by tax returns. The amount of monthly earnings is important in determining the mortgage amount.

- Client participation in bankruptcy proceedings. If he is already bankrupt or less than five years have passed since he was declared bankrupt, the mortgage will be denied.

Note! After submitting an application for a mortgage, the client undergoes a scoring check, which takes 5-10 minutes. The system analyzes his credit history and determines his reliability based on the completed questionnaire. After this, the potential borrower receives pre-approval. The final decision is announced only after a check by the security service, which examines not only the credit history, but also the submitted documents.

Legal advice: Some banks offer mortgages without proof of income. You shouldn’t count on this: the creditor will still make a request to the Pension Fund to find out whether the person pays insurance premiums. If not, this indicates that he is not officially employed. This system has been used instead of income verification for several years. But for a large amount they will still require income certificates and a certified copy of the work record book.

Elena Plokhuta

Lawyer, website author (Civil law, 7 years of experience)

First stage - visual assessment

When a person comes to the bank for a loan, they begin to evaluate him right from the door. The manager who accepts the application includes his opinion about the potential borrower. And if it is negative, the chances of getting a loan tend to zero.

What does the manager pay attention to:

- the applicant's appearance. It must correspond to the data entered in the application form. If a client says that he is a big manager with a good income, but is dressed in rags, this may confuse the manager;

- his behavior. If he is inadequate, rude, behaves strangely. This will also be a reason for a negative mark on the application form;

- documentation. If there is any damage, suspicion of forgery, or that someone else’s documents were provided, this is also a negative factor.

In this case, the manager visually accepts the application; just a few minutes after it is sent for consideration, a negative response may immediately be received. The specialist informs the client about this, and creditors have the right not to indicate the reasons for the refusal.

The system of any bank has refusal codes that can be entered by the specialist accepting the application. They are always placed when there is suspicion of fraud, when the client is under the influence of alcohol or drugs, or inappropriate behavior.

So, the bank checks the borrower even at the moment when he receives preliminary consultation or fills out a questionnaire. Please take this into account and prepare for your visit in advance. The better the applicant looks and behaves, the more praise he will receive from the manager. And this can radically change the course of things.

What happens if a mortgage real estate transaction is challenged?

Everything is simple here: the bank will lose the collateral, the borrower will lose the apartment. But this will not free you from debt obligations; the mortgage will have to be paid in any case.

During legal proceedings, the borrower can appeal Art. 302 of the Civil Code of the Russian Federation, according to which he is considered to be in good faith if he did not know and could not know about the circumstances under which the transaction could be challenged:

- The sudden appearance of heirs who did not have time to enter into inheritance.

- The property was sold under a power of attorney, which the principal canceled before the day of the transaction.

Important! Recently, courts have not canceled transactions, but obligated sellers to compensate the share of persons who challenge the contract. Buyers are left not only with housing, but also with frayed nerves due to lengthy legal proceedings.

How to check an apartment when applying for a mortgage yourself?

The buyer can check the property himself before purchasing with a mortgage, or contact a lawyer. If the transaction is accompanied by a specialist, the risks are minimized, so the second option is preferable.

There are a few things you can and should check before purchasing:

- Is the seller the owner of the property?

- Are there any encumbrances?

- Is the power of attorney valid?

- Does the seller's spouse have consent to the sale?

- Have you received permission from the guardianship authority to sell the child’s home?

- Are there third parties who can lay claim to the property?

- Are shares in the ownership allocated if the apartment was purchased with capital?

Let's look at the nuances in more detail.

Owner verification

You can check the owner by ordering an extended extract from the Unified State Register yourself. When ordering on the Rosreestr website, it will cost 350 rubles, and will be sent by email within three days after submitting the application.

The statement will include information about the property and owner. It is important that the information about the owner matches the passport details of the seller.

Checking for encumbrances

You can find out about the presence or absence of restrictions in the form of bail or arrest in the extract, or check the information yourself on the Rosreestr website. Just enter the address of the apartment, and the information will appear on the screen in a few seconds.

Legal advice: it is better to order an extended extract. Online information may not be current because... The database on the site is updated extremely rarely, approximately once a month. During this time, the seller could take out a loan secured by real estate, or receive a decree banning registration actions from the FSSP.

Elena Plokhuta

Lawyer, website author (Civil law, 7 years of experience)

Verification of power of attorney

For real estate transactions, a notarized power of attorney is required (Article 185.1 of the Civil Code of the Russian Federation). The principal could give it to the attorney, and then cancel it before the transaction. You can check whether the power of attorney is valid on the FNP website. It is enough to enter the date of certification, registration number and information about the notary.

Verification of inherited real estate

The riskiest transactions are with real estate received by inheritance. If a person did not have time to enter into an inheritance for good reasons, then he will be able to restore the deadlines and challenge the policy. There is no way to check whether third parties can claim the apartment, even through a notary.

Legal advice: the deadline for accepting an inheritance can be restored within three years from the moment it became known about the death of the testator. It is optimal if the apartment has been owned by the seller for 7-10 years: this way the risks for the buyer are significantly lower.

Elena Plokhuta

Lawyer, website author (Civil law, 7 years of experience)

Verifying Spouse's Consent

If the apartment was purchased during marriage, the seller must obtain the notarized consent of the spouse before the transaction (Article 35 of the RF IC). Otherwise, he will be able to challenge the sale within a year from the moment he became aware of it.

It’s easy to check whether the seller is married: just look at his passport and check the date of marriage with the date of registration of ownership of the home. If it is purchased during marriage, he must present the notarized consent of the spouse to the buyer.

If the apartment of a minor or incapacitated person is sold

The real estate of a child or incompetent citizen can be sold only with the permission of the guardianship authority. You can find out information about the owner in the extract from the Unified State Register of Real Estate. If he is under 18 years old, he must request guardianship permission from the seller.

Maternity capital was used to purchase an apartment

The most common and dangerous transactions for buyers are with real estate, for which maternity capital was used to purchase or pay off the mortgage. According to Art. 10 Federal Law dated December 29, 2006 No. 256-FZ “On additional measures to support families with children”, all family members must be allocated shares if maternity capital is spent for this.

Some sellers ignore these rules and buy housing and then sell it without allocating shares to all family members.

Important! The buyer's risk when purchasing real estate for which the seller has used capital is the possible challenge of the transaction. This can be done by the Pension Fund of the Russian Federation, the prosecutor's office, the spouse, or the children themselves upon reaching adulthood.

To check the use of maternity capital by the seller, just ask him for a passport and see if he has children born in 2007. If there is any, maternity capital definitely stood out. It is necessary to request from the seller a certificate about the balance of funds under the certificate: if it has not been spent, it means that the capital was not used to purchase housing.

For your information: the amount of maternity capital for the first child in 2020 is 466,617 rubles. Another 150,000 rubles are allocated for the second one if both were born after 01/01/2020. Previously, the certificate was given only for the second child.

Does the bank check the place of work?

The question of how banks verify a place of work interests many borrowers. And sometimes these are people who somehow want to hide some fact. For example, they do not actually work in the declared place, have less experience or a different position.

If the loan is issued with a certificate, all the necessary information will be reflected in 2-NDFL. Many lenders accept an electronic account statement from the Pension Fund of Russia on the State Services portal; all the information necessary for the lender is also reflected there. This is how banks check official employment, and at the same time they may ask you to provide a copy of your employment record.

If the loan is issued without certificates, additional checks may be carried out. The reality of the specified organization is checked, all the data provided about it is compared: telephone numbers, addresses. As a last resort, a call is made to the work number or to the manager’s number specified by the client.

In this case, banks check the borrower’s place of work, but still take his word for it, since such checks do not provide a guaranteed honest result, as is the case with a certificate and a copy of the work book. Bankers understand perfectly well that clients can arrange everything as it should, so they simply increase rates on programs without certificates - they introduce risks into them.

Which banks do not check the place of work, they immediately take the applicant’s word for it - it’s impossible to find out, because each credit institution keeps the exact algorithms of its verification secret.

Lawyer's answers to private questions

Can I get a mortgage if I don’t have a residence permit? Will the bank check it?

Yes, permanent registration is required to obtain a mortgage. The bank will check it, like other information from the passport. If there is no registration, the mortgage will not be issued.

Does the bank check the allocation of shares to children if a mortgage with capital is used to purchase an apartment?

No, this is beyond the competence of banks. All checks on the expenditure of maternal capital are carried out by the Pension Fund.

What to do if, after checking the apartment, the bank refused a mortgage?

If a preliminary contract has been signed and a deposit has been transferred, and the bank’s refusal is considered a force majeure circumstance, the seller must return the money to the buyer. You will have to look for another property that the lender will approve.

Is it possible to speed up the inspection time for an apartment when applying for a mortgage?

No. Some deadlines are established by law, some by the bank’s internal rules. The borrower cannot influence this in any way.

How to protect yourself from challenging the purchase and sale agreement for an apartment purchased with a mortgage?

There are no guaranteed methods. Even after a full legal review, third parties may appear who have rights to real estate. But you can get title insurance against loss of title. If the deal is contested, the insurance company will pay the money.