What the law says

In accordance with the Civil Code of the Russian Federation, a citizen has the right to independently dispose of his property: sell, exchange, donate. In the latter case, when exercising his rights, the owner is obliged to take into account the provisions of Art. 572 of the Civil Code of the Russian Federation.

Donation implies that some movable or immovable property is transferred free of charge and with the good will of the previous owner to the new owner. If a donation of an apartment, house, townhouse is intended, then an agreement is concluded confirming the transfer of ownership. On its basis, changes in the title of real estate are registered in the Unified State Register of Real Estate.

Everything described earlier is possible in one case - the property belongs to the donor, no encumbrances are imposed on it in favor of third parties, for example, a bank.

If the apartment or cottage was purchased with credit money, the contract has not yet been closed, it is necessary to carefully study the Federal Law “On Mortgage” - Federal Law dated July 16, 1998 N 102-FZ (as amended on December 31, 2017) “On Mortgage (Pledge of Real Estate)” (with amendments and additions, effective from 01/01/2019). In accordance with paragraph 1 of Art. 37 of this regulatory act, any alienation of collateral property is possible only with the consent of the creditor.

Who will be allowed to donate an apartment?

Is it possible to donate a house with a mortgage? What about an apartment? For a bank, changing a borrower is a troublesome process. Donating living space for which the debt has not yet been repaid implies that not only square meters, but also loan obligations are transferred to the new owner. He will have to make monthly payments in the future, pay for insurance, etc.

The likelihood of approval of the transaction increases if the original borrower has paid more than 50% of the total amount under the agreement.

Accordingly, the recipient's candidacy is subject to careful consideration and study. The new borrower must be solvent and within the age limits established by the specific lender. And the “old” debtor will definitely be required to prove the reasonableness and necessity of such a transfer of obligations.

If we are talking about the presence of a serious illness, an extract from the medical record and a certificate from a specialized doctor will be useful. If the financial situation worsens - a dismissal order, a copy of the work record book or a 2-NDFL certificate.

Important! If the lender's security service decides that the risks of non-repayment of funds increase with a change of owner, the transaction will be prohibited.

Below we consider the attitude of credit structures to different categories of persons - apartment recipients.

Recommended article: Mortgage under an equity participation agreement secured by rights

How to re-issue a mortgage to another person: procedure and conditions is detailed in another article.

The apartment is transferred to a minor or relative

Is it possible to give an apartment with a mortgage to your daughter or son? The option is unlikely if he is not yet 18 years old. He is considered incompetent and does not yet have his own income sufficient to pay off the debt. In 99% of cases, the bank will not agree to a change of owner.

Assuring parents that they will take over the loan payments themselves or going to court to recognize the recipient as legally competent will not help. Banks insure against such risks and in most cases stipulate in the agreement a ban on transferring property to a minor.

If, for various reasons, the borrower wants the apartment or house to go to a specific son/daughter/nephew, he can draw up a will and have it certified by a notary. This procedure is not prohibited by law.

Is it possible to gift an apartment with a mortgage to a relative? Yes, provided that he meets the bank's requirements, is solvent, has not reached the upper age limit set by the lender, and does not have his own credit obligations.

Lenders do not approve the procedure of gifting real estate to elderly people, regardless of the degree of relationship. It is believed that the only stable income is a pension, but it will not be enough to pay off the debt. An exception is the provision of additional collateral, guarantors or co-borrowers.

Gift recipient - spouse

In accordance with current legislation, spouses automatically become co-borrowers under the Credit (Mortgage) Agreement and co-owners of the purchased property.

Important! Banks strongly “recommend” registering living space not as shared ownership, but as common joint ownership.

There are only two cases when a spouse is not included in the list of co-borrowers:

- he/she is not a citizen of Russia. Some banks refuse such restrictions and issue loans to residents of the Russian Federation. But most of the creditors are conservative, not wanting to cooperate with those who can leave the country at any time and never return here;

- The spouses entered into a prenuptial agreement providing for separate ownership of real estate. In this case, the husband/wife does not become co-borrowers and cannot claim a share in the purchased apartment.

The process of donating a mortgaged apartment to a spouse is considered inappropriate and is not practiced. Initially, the contract implies a community of ownership, and therefore responsibility. There may be exceptions, but in a very limited number of cases, for example:

- the loan agreement was signed by the husband/wife before marriage;

- The apartment was purchased during marriage, but the union broke up. One of the spouses wants to get rid of unnecessary property and transfer it to the other.

Recommended article: Termination of a purchase and sale agreement with a mortgage

Regardless of the reason for the transfer of square meters, the bank will assess the recipient’s solvency, taking into account all the requirements and rules in force in the credit institution.

Donating an apartment to a co-borrower

Co-borrowers are special people in the relationship between mortgagees and title borrowers. They are fully liable for debts to the creditor, but do not always claim square meters. Is it possible to gift an apartment with a mortgage to a co-borrower (not husband or wife)? The issue requires separate consideration.

The relationship between the main debtor and each co-borrower is governed by additional agreements. For example, he is allocated a share in an apartment in the amount of 25-30-40-50%, provided that he deposits the required amount into the lender’s account. If the main debtor, for various reasons, stops paying under the agreement, the bank automatically switches its attention to the co-borrower. He won't even have to go to court for this.

Transferring the debt to a co-borrower is possible (the situation when a husband/wife becomes a co-borrower was discussed earlier). For example, the main debtor wants to transfer both obligations and property to a second person specified in the contract due to health reasons, due to the inability to make payments in the future.

Important! Regardless of who the borrower wants to give his property to, the lender will calculate his risks. If, based on the results of the analysis, it is decided that the likelihood of non-return of money increases, the transaction will be prohibited.

In order for the lender to treat the procedure favorably, the recipient must have an income higher than that of the current payer. He should not have debts in banking structures or negative entries in his credit history.

Is it possible for a co-borrower to take out a mortgage and how to increase the chance of approval - is described in detail in another article on our website.

Gift and mortgage

A property subject to a mortgage has restrictions on carrying out legally significant actions. From the point of view of legal norms, there is an encumbrance in the form of a pledge of property until the loan debt is fully repaid.

Article 37 of Law No. 102-FZ of July 16, 1998 regulates the alienation of mortgaged property, according to which the donation of a mortgaged apartment is permitted with the consent of the mortgagee, unless otherwise provided in the loan agreement. A credit institution is involved in participating in a transaction that determines the possibility of its conclusion.

Whether it is possible to donate a mortgaged apartment depends on the will of three parties:

- The wishes of the donor. The owner, despite the presence of an encumbrance, has the right to present a gift to any persons, with the exception of prohibited categories for receiving a gift worth over 3,000 rubles (Article 575 of the Civil Code of the Russian Federation). The donor cannot donate the property:

- employees of educational, medical and social services, subject to treatment and training;

- state, municipal and bank employees in connection with the performance of functional duties.

- Consent of the donee. A gift agreement is a two-sided transaction that requires the parties to sign upon conclusion, otherwise it becomes void. The donee has the right to refuse the deed of gift at any time before the actual delivery, which makes the contract terminated. In relation to an apartment, the refusal must occur before registration in the Unified State Register of Real Estate. Donating an apartment with a mortgage is the most common reason for refusal by the donee, since along with the rights to the property, obligations to repay the loan are transferred.

- Written permission of the mortgagee. In the absence of a ban on alienation in the loan agreement, the bank evaluates the factor of increasing financial risks when there is a change of owner. The credit institution analyzes:

- age and solvency of the donor and donee;

- amount of outstanding debt;

- the period of scheduled payments until the debt is completely eliminated.

Whether it is possible to write a deed of gift for a mortgaged apartment is decided by the bank, based on minimizing financial risks. The credit institution is not a party to the gift agreement, but without the consent of the bank, an apartment with an encumbrance cannot go through the registration procedure in the Unified State Register of Real Estate, which automatically cancels the proposed transaction.

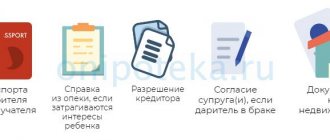

What documents will be needed to register a donation?

To donate an apartment with a mortgage, if the lender has given his permission, the following documents will be required:

- civil passports of the donor and recipient;

- documents confirming ownership of real estate (extract from the Unified State Register of Real Estate, purchase and sale agreement);

- technical passport for the facility;

- consent of the spouse if the property was purchased during marriage;

- an extract from the house register or a certificate from the passport office with information about those registered;

- certificate from guardianship if the rights of minors are affected;

- documented permission of the lender.

Recommended article: Which bank to take out a mortgage on a land plot (documents, requirements)

The donation agreement specifies:

- information about the donor, recipient and mortgagee;

- reference to title documents - basis of ownership;

- object parameters (number of floors, area, number of rooms, etc.) based on technical and cadastral passports;

- the rights and obligations of each party under the agreement and a reference to the fact that the property is transferred free of charge.

A separate clause in the contract states that the recipient knows that an encumbrance has been placed on the apartment or house. The recipient agrees that he accepts not only the property, but also all obligations associated with it, including debts on interest, penalties and fines. The agreement is signed by the donor, recipient and representative of the creditor bank.

Is it possible to donate a share of an apartment in a mortgage? Will the application procedure be different? If the borrower wants to transfer not all of the living space, but part of it, to a relative or a complete stranger, the bank’s permission and the drawing up of a tripartite agreement will also be required.

In what cases can you obtain the bank’s consent to donate a mortgaged apartment?

When considering a borrower’s application to donate housing to another person, the bank pays attention to the following points:

- terms of the mortgage agreement . If the agreement contains a clause on the possible procedure for donating housing under mortgage, then the bank will consider the application. Otherwise, banks often refuse borrowers;

- percentage of remaining debt . If the borrower has repaid most of the mortgage, then he can actually obtain the bank’s consent to donate mortgaged housing. If the borrower has not repaid even 50% of the amount that the bank gave him, then the chances of approval of the application are reduced;

- solvency of the new owner . When considering an application for donating a mortgaged apartment, banks are sure to ask where the person to whom the current borrower plans to donate an apartment works, how much he earns, how long he has been working, etc. If the financial condition of such a person is favorable, and the current borrower loses his previous financial stability, then the bank can approve the procedure for donating a mortgaged apartment.

Donation procedure

To donate an apartment with a mortgage, you will have to go through the following steps:

- obtaining the lender's consent;

- collection of documents;

- drawing up a deed of gift indicating all the important points;

- submitting documents to Rosreestr to make changes to registration records.

Important! The list above is not complete or exhaustive. The pledgee has the right to request additional information, for example, to verify the identity and solvency of the recipient.

Is it possible to donate part of an apartment with a mortgage or the entire living space, bypassing the bank? What happens if you draw up an agreement yourself and submit documents for registration?

The best case scenario for the borrower is nothing. The registrar will check the status of the property and reject the application due to encumbrances. At worst, the information will be passed on to the mortgagee. The latter has the right:

- protest the transaction in court;

- terminate the contract unilaterally and demand early payment of the entire amount;

- sell the apartment - the proceeds are used to pay off the debt.

Anatoly Nikiforov, legal consultant of Legal Services Center LLC, answers:

In the situation under consideration, a regime of common joint ownership of the spouses will arise in relation to the apartment. It does not matter to whom the apartment will be registered directly: to you or to your spouse. The mode of common joint ownership of an apartment assumes that it is in your common ownership without defining specific shares.

According to the norms of current legislation, owners of common joint property can alienate such an apartment only in its entirety. Your shares are not defined, and therefore you will not be able to dispose of your specific part. Therefore, in order to complete a transaction to alienate a share, it is necessary to first determine the shares of each of you, and for this it is necessary to change the property regime from joint to common shared.

Spouses have the right, at their discretion, to change the regime of common joint ownership of property acquired during marriage (or part thereof), both on the basis of a marriage contract and on the basis of any other agreement (agreement) that does not contradict the norms of family and civil legislation. In practice, this may be an agreement on determining the shares of spouses or an agreement on the division of property. Based on any given agreement, the Rosreestr authorities will change the property regime and make corresponding entries in the real estate register.

After this, each of you will have the right to independently dispose of your share in any way not prohibited by law, in particular, to donate it. In this case, the donation agreement for real estate registered as shared ownership must be certified by a notary. It is worth noting that the parties to the agreement in this case are exempt from paying tax.

The donation of a share in an apartment is also subject to state registration. As soon as the gift transaction is registered in Rosreestr by making a corresponding entry in the Unified State Register of Real Estate, you will be the full owner of the apartment, and even in the event of a divorce, this property will not be divided between the spouses, but will remain exclusively yours.

Of course, the latter does not apply to the situation if the gift agreement itself is subsequently challenged by the spouse in court as invalid.