Conducting a business or any other significant economic activity requires, among other things, close interaction with regulatory authorities and structures. One of them is the state pension fund.

Those organizations and individual entrepreneurs that have employees are required to provide periodic reporting to the Pension Fund of the Russian Federation related to personalized accounting and calculation of insurance premiums. The features of its presentation will be discussed further in the article.

How do you submit reports to the Pension Fund?

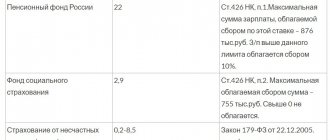

The subjects of compulsory pension insurance are both employees (insured persons) and employers acting as policyholders. Organizations and individual entrepreneurs that have employees are required to make insurance contributions for them to the Pension Fund for the formation of a future pension. The amount of contributions is tied to the salary of a particular employee and amounts to 22% of it.

Important! Insurance premiums are paid both for full-time employees with whom labor relations have been established, and for private individuals carrying out work or providing services on the basis of civil contracts.

Accordingly, every employer has an obligation to submit appropriate reports. It includes information related to the calculation of accrued and paid insurance premiums, as well as other personalized accounting data.

Reporting is submitted by the employer personally, but it is possible to involve specialized accounting organizations on the basis of an agreement. Documents are submitted within strictly regulated deadlines.

It should be noted that the Pension Fund of the Russian Federation is vested with the right to issue acts providing for the prosecution of persons who violate the legislation on legal security . In practice, this means that a legal entity or individual entrepreneur may be fined for late submission of reports.

In general, for 2020, reporting to the state pension fund consists of 5 unified forms that employers must submit. Let's briefly look at each of them

SZV-M

This report is submitted by all organizations. It contains information about insured persons located in the state for a specific reporting period. SZV-M contains information that is necessary for maintaining personalized records.

The form must contain the following information:

- data of the insurer;

- reporting period;

- information about persons insured in the OPS system (full name, SNILS, INN).

For more information about the program, watch the video:

SZV-STAZH

This form is a report that is submitted to the state pension authorities every year. It must necessarily reflect information about all employees with whom the organization has concluded employment contracts, as well as persons with whom there are civil relations.

SZV-STAZH is necessary to provide information about the employee’s existing insurance experience . Let us recall that the insurance period has a direct impact on the possibility of applying for an insurance pension in the future, as well as on the size of the pension itself.

Reference! Individual entrepreneurs with employees are required to submit a report on the form in question only for their employees. If an individual entrepreneur does not have employees, then filing a SZV-STAZH report is not necessary for him.

SZV-TD

This form contains information about the employee’s work activity. This report is new and was put into circulation in connection with the transition to “electronic work books”. In this regard, many policyholders had many questions regarding its filing.

Thus, the following information is entered into the SZV-TD form:

- information about the policyholder (registration number, name, TIN, KPP);

- information about the insured (full name, date of birth, SNILS);

- a note indicating that the insured person has chosen a new form of recording work activity;

- information about periods of work.

It should be noted that a report in the SZV-TD form is submitted only when there are grounds for this, which include:

- hiring;

- dismissal (regardless of the reason);

- transfer to another workplace;

- submitting an application to choose a form of recording work activity.

SZI-TD

SZI-TD is inherently a more detailed form of the SZV-TD report. It contains, among other things, information about the employee, dates of hiring and dismissal, position, type of work and structural unit of the organization where the employee worked.

Important! A document in this form will be issued to the employee upon dismissal for presentation at the place of request.

The SZI-TD form is submitted by policyholders to the Pension Fund of the Russian Federation upon dismissal of an employee. It should be noted that the information in the document in question must directly correspond to the information contained in the SZV-TD form.

EDV-1

At its core, EDV-1 is an inventory of all documents that are transferred to the pension fund by the policyholder. In practice, this means that this form is submitted along with other reporting documents.

It should be noted that the above reporting forms are mandatory. However, in certain circumstances, the employer is required to submit additional forms, including upon direct request from the state pension fund.

A single form for reporting to the Pension Fund

In 2014, starting from the 1st reporting period, the pension fund made the transition to a unified form of reporting documentation.

The innovation is connected, first of all, with the desire of the state. services to reduce the burden on employers caused by the regular preparation of a large number of documents. The new version of RSV-1 includes reporting for both pension and health insurance.

In addition, this form allows you to maintain personalized records for each of the insured persons.

The adoption of these changes was preceded by a sociological survey of employers, which showed that the overwhelming majority (91.2%) of the surveyed insurers have a positive attitude towards the transition to a unified PRF reporting form.

Compliance with the procedure for maintaining personnel records and the rules of labor legislation will protect any organization from adverse financial and legal consequences, and the employee from problems when receiving a pension or getting another job.

Like a regular signature, an electronic signature serves to ensure that it is no longer possible to intentionally enter incorrect or distorted information into the document certified by it. Read about certification of digital signature documentation here.

When developing the new form, the changes adopted in the insurance legislation in 2013 were taken into account, introducing the following amendments:

- The individual information provided by policyholders does not indicate the amount of all insurance premiums made.

- The payment of contributions starting from 2014 is displayed in a single payment document. In this case, the insurance and savings parts are not allocated.

The above parts are highlighted, taking into account the age category of the employee, his citizenship and the choice of one of the pension options, by the Pension Fund of the Russian Federation itself.

In addition, a unified reporting format displays arrears of contributions, as well as their additional accruals and payments for the period from 2010 to 2013.

Methods for sending reports

Reporting documents can be sent to the Pension Fund in different ways. At the same time, the pension fund's policy in this regard is aimed at increasing the use of electronic communication methods in this part. For example, restrictions are introduced on the number of employees at which it is allowed to submit information on paper.

By post

This method involves sending paper documents by registered mail to the pension fund. The reporting filing date is the day the letter was sent, which is determined by the postmark.

It is advisable to send a letter with a list of the contents and a notification of delivery. It should be noted that not all policyholders can take advantage of the opportunity to submit documents by mail, but only those with a staff of no more than 24 people inclusive. If the number of employees is larger, then the information is submitted only electronically.

Through the Internet

Submitting documents electronically has a number of advantages, including the following:

- impossibility of data loss;

- the ability to correct entered data;

- receiving a report from the Pension Fund on the acceptance of documents, which allows you to avoid delays in submitting them.

Before submitting documents in electronic format, the organization must contact the pension fund to sign an agreement on this type of interaction.

Electronic documents must be certified by the signature of the responsible employee. We are talking about digital signature. Moreover , if reports are submitted in batches, then an electronic signature must be affixed to each file.

For the convenience of filling out forms, organizations and individual entrepreneurs can use special programs developed by Pension Fund specialists. You can download them on the official website of the foundation, as well as on the websites of territorial branches.

What should an accountant tell employees?

There is a high probability that employees will turn to accountants with a request to help them understand the innovations that are associated with the abolition of indexation of insurance pensions. Let's look at some points that make sense to tell employees about.

Legislators provided that from February 2020, the planned indexation of the insurance pension and the fixed payment to it will apply only to those pensioners who, as of September 30, 2020, were not working (did not work on the basis of civil law contracts). The fact that a pensioner is working as of September 30, 2020 will be determined by Pension Fund specialists on the basis of personalized information contained in the RSV-1 calculation for 9 months of 2015.

In case of termination of work during the period from October 1, 2020 to March 31, 2020, the pensioner himself can notify the Pension Fund of this fact. To do this, you need to submit an application and documents confirming the end of your labor activity (for example, a copy of the work book with a notice of dismissal) to the fund’s division. From the first day of the month following the month in which the pensioner notifies the Pension Fund of the Russian Federation about the termination of work, the fund will begin to pay him an insurance pension, taking into account indexation (clause 3 of Article 7 of the commented Law No. 385-FZ). The form for this application is posted on the Pension Fund website.

Please note that a pensioner can confirm the completion of employment or civil law relations in the period from October 1, 2020 to March 31, 2020 no later than May 31, 2020 (Clause 2 of Article 7 of the commented Law No. 385-FZ). If a pensioner stops working in April 2020 or later, he will no longer have to report this to the Pension Fund, since fund employees will determine all the necessary information based on monthly data provided by policyholders. If it follows from the policyholder’s reporting that the pensioner has retired, then the decision to assign a pension, taking into account indexation, will be made in the month following the month of reporting (Clause 6, Article 26.1 of Law No. 400-FZ), and payment of the pension in the new amount will begin from next month (clause 7, article 26.1 of Law No. 400-FZ). If in the future the pensioner gets a job again, the amount of his insurance pension will not be reduced (Clause 8, Article 26.1 of Law No. 400-FZ).

Due dates

Depending on the timing of submission of reports to the Pension Fund, they can be classified as follows: monthly, quarterly, annual.

- Monthly . Monthly - before the 15th day of the month following the reporting month, it is necessary to submit forms SZV-M and SZV-TD.

- Quarterly . Reporting is submitted quarterly in the form DSV-3. This report is submitted only if additional insurance premiums are paid for the employee. We are not talking about increased coefficients for special working conditions, but about a voluntary decision of the employee aimed at increasing the size of his pension. Additional contributions can be made by the employee independently or through the employer. In the latter case, the organization submits a report in form DSV-3 quarterly no later than the 20th day of the month following the reporting month.

- Annual . Once a year, based on the results of this period, it is necessary to submit documents using the SZV-STAZH form.

It should be noted that some reports are submitted not within the framework of any frequency, but as required. Thus, the SZI-TD form is sent to the Pension Fund on the day the employee is dismissed.

In addition, the state pension fund may request additional reports, the deadlines for submission of which are indicated in the official request of the fund.

Composition of reporting

The following information must be submitted monthly for each employee:

- individual personal account insurance number (SNILS);

- last name, first name and patronymic (full name);

- taxpayer identification number (TIN) (clause 2.2 of article 11 of Law No. 27-FZ).

Please note that the full name and SNILS of employees are also indicated in subsection 6.1 of section 6 of the RSV-1 calculation (see “New RSV-1 form: features of filling out and submitting the calculation for the first half of 2015”). However, starting from April 2020, this information, as well as the TIN of employees, will need to be reported additionally. The pension fund must develop a form for a new monthly report, as well as a format for submitting reports via the Internet.

We also note that the commented Law No. 385-FZ does not clarify some issues that may arise when drawing up a new report. In particular, is it necessary to submit information for employees who did not receive insurance premiums in the reporting month (for example, if the employee was on long-term leave without pay or on parental leave)? Should “blank” monthly reporting be submitted if the company has only one director (aka the only founder) with whom an employment contract has not been concluded? If remuneration to an employee under a civil contract concluded for a long term is not paid every month, then how often do you need to submit information: only for the month of payment or for each month of the contract? What to do if the employee does not have a TIN? Perhaps answers to these and other questions will appear in the order of filling out the new report and official explanations for it.

Will the pensions of individual entrepreneurs be indexed?

The Pension Fund website reports that if a pensioner belongs to the category of self-employed people, that is, is an individual entrepreneur, notary, lawyer, etc., then such a pensioner will be considered working if he is registered with the Pension Fund as of December 31, 2020.

Elena Kulakova, an expert at “Kontur.Otchet PF” (on the Online Accounting forum she writes under the nickname KEGa) believes that Pension Fund officials could equate individual entrepreneurs who receive a pension with working pensioners based on the norm of Article 26.1 of Law No. 400-FZ. Paragraph 1 of this article states that indexation is not due to pensioners who carry out not only work, but also “other activities during which they were subject to compulsory pension insurance in accordance with Federal Law dated December 15, 2001 No. 167-FZ “On Compulsory Pension Insurance” In Russian federation". And in paragraph 1 of Article 7 of the commented Law No. 385-FZ it is noted that the fact of carrying out other activities is established on the basis of information about registration as an insurer in the Pension Fund of the Russian Federation.

According to Article 6 of the Federal Law of December 15, 2001 No. 167-FZ, policyholders for compulsory pension insurance are, among other things, individual entrepreneurs. Thus, we can conclude that the planned indexation of insurance pensions is “frozen” for all retired entrepreneurs who will be registered with the Pension Fund as policyholders on December 31, 2015. We also note that although in the message on the Pension Fund website entrepreneurs are mentioned only as self-employed people (along with lawyers, notaries, etc.), this does not mean that the ban on indexation of insurance pensions applies only to individual entrepreneurs who do not have employees. Retired entrepreneurs who are employers are also deprived of such indexation. An individual entrepreneur (with or without employees) does not have to submit monthly information to the Pension Fund.

Note that if an individual entrepreneur is registered with the Pension Fund, but does not conduct business activities and does not receive any income from it, then he still will not be able to count on indexation of the insurance pension. The right to indexation will arise only after the entrepreneur is deregistered with the Pension Fund of Russia (remember that the fund deregisters an individual entrepreneur after he loses this status and a record about this appears in the Unified State Register of Individual Entrepreneurs). At the same time, it is most likely not necessary to submit an application for termination of activities using the form posted on the fund’s website. However, this cannot yet be stated unequivocally.

How to report to the Pension Fund for employees?

All employers who pay hired citizens wages or other type of remuneration for the work done are accountable for their employees. This also applies to individual entrepreneurs who have at least one employee. To report to the Pension Fund of the Russian Federation, employers must be registered in the OPS system .

Citizens registered as individual entrepreneurs who work for themselves and do not have hired workers do not provide this information.

There are several types of specially designed document forms by which employers transmit information about their employees to the Russian Pension Fund. This must also be done within a certain time frame.

SZV-TD

The form “Information on the labor activity of employees” is filled out by the employer based on orders and other personnel documents. The report contains information about hired and dismissed employees, as well as about those who experienced any personnel changes (promotions, transfers, etc.).

Data on this form will need to be submitted to the Pension Fund for each month

before the 15th

of the next month. Only information about employees affected by personnel changes is provided.

Starting from 2021, you will need to report for the hiring or dismissal of an employee the next day after signing the order. In addition, all information about changes in the employee’s work activity that were not provided to the Pension Fund earlier should be reflected.

The SZV-TD is certified by the signature of the head (trusted representative) and the seal of the organization. If the employer is not a legal entity, the document is certified by a personal signature.

The method of submitting the report is in paper or digital format. But only employers with fewer than 25 employees can submit a document on paper. For others, an electronic version of the form certified with an electronic signature is required.