Any officially employed citizen has the right to go on vacation paid for by the employer once a year, but this right must be earned. There are various situations in life in which it may be necessary to urgently apply for leave or there is a strong desire to interrupt your work experience for a vacation ahead of schedule. Some categories of employees want to add early leave to their due leave, for example, maternity leave, or to quit immediately after the rest.

- Can an employer meet such wishes of employees, does this not contradict the requirements of the Labor Code, and what does he risk in doing so?

- Does he have the right to refuse outright?

- How to arrange “vacation in advance”?

Let's understand the nuances.

The concept of “vacation in advance” and its legislative framework

There is no official term “vacation in advance” in Russian legislation. Annual paid leave, guaranteed to each employee by the Labor Code (Article 122), is earned for 1 working year. It is counted not from the beginning of January, but from the date of registration of the employment contract, that is, it is individual for each employed person.

An employee can go on this leave after completing six months of work experience (the provisions of Article 122 of the Labor Code of the Russian Federation) or earlier, in agreement with the employer. It is not difficult to calculate that during this time, at best, only half of the officially established vacation duration will be worked. It turns out that the second half, if the vacation is not divided into parts, the employee receives in advance.

If the length of service is less than 6 months, then the advance payment of vacation days provided is even longer.

In the second and subsequent years of work, vacation is given according to the schedule at any time; length of service no longer matters, so vacation is often assigned in advance.

FOR YOUR INFORMATION! International Labor Organization Convention No. 132 on Holidays with Paid, which the Russian Federation ratified in 2010, states that an employee can receive leave from any day of his employment for a duration proportional to the time worked. However, many employers give preference to the norms of the Labor Code of the Russian Federation, which are legally “above” the conventional ones. The Labor Code does not deprive the employer of the right to allow early leave, and, regardless of the time worked, it allows you to receive it in full.

Thus, it is possible to define leave provided in advance as annual paid time for legal absence from the workplace, received before the moment of its actual working out.

If the employer forgave the employee's debt

Income tax. Expenses of the employing organization incurred in connection with the dismissal of an employee who did not work the vacation days provided in advance are not taken into account when forming the taxable base for income tax. They do not meet the requirements of paragraph 1 of Art. 252 of the Tax Code. This was pointed out by specialists from the capital's tax department (Letters from the Federal Tax Service of Russia for Moscow dated 06/30/2008 N 20-12/061148 and dated 04/17/2006 N 21-07/ [email protected] ).

However, recognition of the amount of paid vacation pay as expenses during the period of vacation is justified, and there is no need to recalculate the tax base for income tax for the previous period.

Personal income tax. Since the tax on advance vacation pay has already been fully taken into account, the employee does not have additional income subject to personal income tax when the debt is forgiven.

Insurance premiums. The amount of accrued insurance premiums is also not subject to adjustment.

A few more words about income tax. Insurance premiums accrued from the outstanding amount of debt are taken into account as part of other expenses associated with production and sales on the date of their accrual (clause 49, clause 1, article 264 of the Tax Code of the Russian Federation)

The Russian Ministry of Finance drew attention to this in Letter dated 04/23/2010 N 03-03-05/85

Differences between advance leave and timely leave

The conditions under which such a vacation becomes a reality differ from the usual guarantee of annual vacation in several important nuances:

- the manager has the right to refuse permission for such leave, since providing rest in advance is not his responsibility;

- vacation granted in advance cannot be replaced with monetary compensation, because these funds have not yet been earned;

- like regular leave, such leave can be divided into parts, one of which cannot be less than 2 weeks.

What types of holidays cannot be provided in advance?

Not all types of vacations can be taken off earlier than expected. The concept of “vacation in advance” most often refers specifically to annual vacation paid by the employer. But there are some types of leave that must have a documentary basis, so they cannot be granted in advance if the employee does not have an official document confirming this basis. Such holidays include:

- additional;

- administrative;

- training;

- maternity leave (both for childbirth and for caring for the baby).

Vacation before or after another vacation

Motherhood is such a special event in a woman’s life that the state tries in every possible way to protect this category of workers. Women planning maternity leave have the right to go on another vacation, even without having worked for the organization for the required 6 months. Mothers can receive the same leave immediately after leaving maternity leave.

In addition to pregnant women and young mothers, the right to go on leave regardless of length of service is granted to:

- their spouses;

- relatives if they took maternity leave instead of their mother;

- employees who have two young children under the age of 14;

- fathers and mothers of disabled children under 18 years of age.

The law provides the same right, but for reasons not related to parenthood:

- part-time employees who are granted leave from their main job (it must coincide with the rest from their combined position);

- wives or husbands of military personnel who have received their leave (for military spouses, the vacation time must also coincide);

- other categories of employees for whom this right is provided for by the organization’s labor or collective agreement.

Calculation of the amount of deductions

The deduction of overpaid vacation pay upon dismissal occurs in accordance with the law and mandatory calculations carried out by accounting employees. Here, the calculations use the salary received for the period worked, as well as additional values.

The formula is as follows:

(actual days taken off by a person - the number of allotted days) * average earnings calculated at the time of payment of vacation pay.

https://youtu.be/vbMHOR5urSk

Each value is subject to more careful consideration, which allows you to calculate the withholding upon dismissal yourself.

Algorithm for calculating the amount of debt

Since the calculation of the number of allotted days has already been presented, it remains to give as an example an algorithm for calculating average earnings per day. This indicator is regulated by Article 139 of the Labor Code of the Russian Federation, which states that the obtained value is used to calculate vacation pay or, accordingly, withholding.

Average daily earnings are calculated as follows:

Salary*12/number of days worked per year.

Withholding of vacation pay upon dismissal occurs using the average value that was calculated at the time of leaving for vacation.

It follows that the complete algorithm for how vacation pay is withheld upon dismissal is presented as follows using an example:

- Citizen Galina R. is leaving the company due to staff reduction and receiving all amounts of compensation. When calculating, accounting staff discovered an extra 9 days paid for vacation.

- At the time of her leave, the woman had worked for only 10 months, and her monthly salary was about 29,000 rubles, according to the information received from personal income tax certificate 2. It turns out that the average earnings per day, at the time of providing days for rest, is calculated as: 29000 * 12/257 = 1354 rubles.

- It follows that vacation pay was calculated for 28 days as 1354 * 28 = 37912 rubles.

- If Galina R. received an extra 9 days of vacation, then 1354 * 9 = 12186 rubles will be withheld from her.

It follows that, despite the calculated amount of deduction for unworked leave upon dismissal, the employer cannot take more than 20% of the total monetary value received.

Recalculation of tax withholdings

Withheld funds reduce the tax base for contributions to the Social Insurance Fund, as a result of which employers predominantly “take away” previously issued amounts from employees. But management can forgive the employee for the presented values of the funds paid, so there is no need to display any changes in the accounting entries. This point is simply not indicated in the documents, so there is no need to rewrite the reports.

As for taxes, accounting staff simply calculate wages for the last month before dismissal, taking into account deductions. Thus, an employee leaving the company receives payments that are less than the required amount. This happens according to documents, but accrued wages are paid to him in full. When drawing up an order, the moment of retention is mandatory.

Vacation before dismissal

Before finally leaving the workplace, the employee has the right to “take off” his allotted vacation days. But what if he plans to quit without earning enough experience for a vacation, but nevertheless wants to go on it?

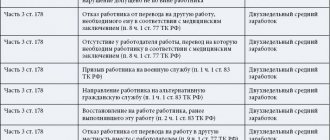

The key point is the employer's consent. If the management does not mind providing the employee with such an opportunity, nothing prevents him from continuing to be listed as an employee of the company during his vacation, having completed the resignation documents on his last working day. However, it should be remembered that before going on vacation, the issue of monetary compensation for vacation not earned by the resigning person must be resolved: it will have to be paid into the cash register voluntarily, or it will be deducted from the salary during the calculation. The employer will not be able to demand this if the employee quits for one of the following reasons:

- consent of the parties (all issues, including payment, are resolved mutually before the order is issued);

- expiration of the employment contract;

- transfer to another place, to another employer;

- changes in working conditions and refusal to cooperate associated with changes;

- sick leave for more than 4 months (except for maternity leave);

- the employee is sent by the company for training;

- the employee was “laid off”;

- the court reinstated the employee who had previously occupied the position of the dismissed person;

- An employee who has rested in advance retires.

NOTE! If an employee leaves voluntarily or quits due to culpable behavior, compensation for unworked but “committed” vacation can be deducted from his salary without asking consent.

Hassle-free option

Let's simulate the situation. Let’s say an employee was granted leave for an unworked period of time, that is, in advance. He was accrued vacation pay in the amount of 60,000 rubles. After some time in the same tax (calculation) period, he resigns. The amount of accruals to an employee upon dismissal is 70,000 rubles. Payment for unworked vacation days - 10,000 rubles. To simplify the example, we will assume that the employee did not have any other income and no personal income tax deductions are provided to him.

First, we will determine whether it is possible to withhold the entire amount for unworked vacation days from the payments due to the employee upon dismissal.

The amount due to the employee upon dismissal minus personal income tax is 60,900 rubles. (RUB 70,000 – RUB 70,000 x 13%). The maximum possible amount of deduction from this amount is RUB 12,180. (RUB 60,900 x 20%). In our case, you need to withhold 8,700 rubles. (RUB 10,000 – RUB 10,000 x 13%). Thus, the amount of payments to the employee is enough to withhold the entire amount. As a result, the employee will receive 52,200 rubles.

Personal income tax

The calculation of personal income tax amounts from income received by an employee is carried out by the company on an accrual basis from the beginning of the calendar year, with the offset of the amount of tax withheld in previous months (clause 3 of Article 226 of the Tax Code of the Russian Federation). When paying vacation pay (including for unworked vacation days), the employee received income in the amount of 60,000 rubles, and the company, on the basis of clause 4 of Art. 226 of the Tax Code of the Russian Federation lawfully withheld personal income tax from him in the amount of 7,800 rubles. (RUB 60,000 x 13%).

Upon dismissal, part of this income attributable to unworked vacation days is withheld from the payment due to him (that is, in fact, a portion of the vacation pay is returned). In letter dated October 30, 2015 No. 03-04-07/62635, the Russian Ministry of Finance explained that if an employee returns previously paid vacation pay to the employer, such amounts will not be recognized as the employee’s income. Accordingly, it is necessary to adjust the tax base for personal income tax for the tax period for this employee. In this case, the tax agent will overpay personal income tax. These clarifications from the financiers were brought to the attention of lower tax authorities by letter of the Federal Tax Service of Russia dated November 11, 2015 No. BS-4-11/ [email protected]

Please note: the tax agent does not have the right to offset the above overpayment against future personal income tax payments, but can only return it (letter of the Federal Tax Service of Russia dated 02/06/2017 No. GD-4-8/ [email protected] ). The fact is that payment of personal income tax at the expense of tax agents is not allowed (clause 9 of article 226 of the Tax Code of the Russian Federation). Consequently, transferring to the budget an amount exceeding the amount of tax actually withheld from the income of individuals does not constitute payment of personal income tax. In this case, the tax agent has the right to contact the tax authority with an application for the return to the current account of an amount that is not personal income tax and was mistakenly transferred to the budget.

Upon dismissal, the employee is accrued income in the amount of 70,000 rubles, personal income tax on which is 9,100 rubles. (RUB 70,000 x 13%). The company must transfer this tax to the budget no later than the day following the day of payment (clause 6 of Article 226 of the Tax Code of the Russian Federation).

Due to the recalculation of vacation pay, the amount of income received by the employee during the period of their payment decreased. Provisions of paragraph 6 of Art. 81 of the Tax Code of the Russian Federation obliges the tax agent to submit an updated calculation of 6-NDFL if distortions are identified in the previously submitted calculation, as well as errors leading to an underestimation or overestimation of the tax amount. In our case, the amount of tax to be transferred to the budget for the period of accrual of vacation pay turned out to be overestimated. Consequently, the company must submit an updated 6-NDFL calculation for this period.

Insurance premiums

The basis for insurance premiums is formed by payments and rewards accrued in favor of an individual from the beginning of the calendar year (clause 1 of Article 421 of the Tax Code of the Russian Federation). In our example, during the vacation pay accrual period, this base was 60,000 rubles. When an employee was dismissed due to deduction for unworked vacation days, the amount of previously accrued vacation pay was reduced and amounted to 50,000 rubles. (60,000 rub. – 10,000 rub.). In addition, he was awarded payments in the amount of 70,000 rubles. Thus, during the dismissal period, the base for calculating insurance premiums is 120,000 rubles. (50,000 rub. + 70,000 rub.). Based on this value, in the month of dismissal the company calculates the insurance premiums payable, minus the amounts of insurance premiums for the previous months of the year (clause 1 of Article 431 of the Tax Code of the Russian Federation).

Please note that in the situation under consideration, there is no need to adjust the base during the vacation pay accrual period. After all, when calculating them, the company acted in accordance with the requirements of the law and did not make any errors or distortions. Accordingly, she should not submit an updated calculation of insurance premiums for this period. This is confirmed by the explanations given in the letter of the Ministry of Health and Social Development of Russia dated May 28, 2010 No. 1376-19. And although they were given at a time when the procedure for calculating insurance premiums was regulated by the provisions of Federal Law No. 212-FZ dated July 24, 2009, in our opinion, they are still applicable now. The fact is that the procedure for calculating insurance premiums, provided for by Chapter 34 of the Tax Code of the Russian Federation, is similar to that established by the above law.

Let us note that there are letters from the Federal Tax Service of Russia dated October 11, 2017 No. GD-4-11/20479, dated August 24, 2017 No. BS-4-11/ [email protected] in which tax authorities talk about the need to submit an updated calculation of insurance premiums when withholding for unworked vacation days. But they are talking about a situation where, due to retention, negative values appear in the calculation. We will talk about when this happens below.

Income tax

Vacation pay is taken into account as part of labor costs (clause 7 of Article 255 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated July 22, 2016 No. 03-03-06/1/43097). Since they were accrued in accordance with the requirements of the law, their entire amount (including that paid in advance for unworked vacation days) was legally included in the expenses of the reporting period in which the employee was on vacation. This means that the company did not make any errors or distortions of the tax base during this period. Therefore, adjustments in connection with the subsequent withholding of overpaid vacation pay are not necessary.

A retention transaction refers to the period during which an employee is dismissed. Its result is the receipt of employee funds into the ownership of the company. That is, she receives income. Since it is not related to sales, it must be taken into account as part of non-operating income on the basis of Art. 250 Tax Code of the Russian Federation.

Financiers and tax specialists also think (letters from the Ministry of Finance of Russia dated December 3, 2009 No. 03-03-05/224, Federal Tax Service of Russia for Moscow dated January 11, 2007 No. 21-08 / [email protected] ). At the same time, they indicate that income must include the amount that was previously included in expenses. Thus, on the date of withholding, the company takes into account excess accrued vacation pay in the amount of RUB 10,000. as part of non-operating income.

Pitfalls of “advance leave” for the employer

It is not surprising that some employers choose not to deviate from their right to provide holiday only on time. There are certain risks in the fact that an employee goes on vacation without earning this opportunity.

The main problem for employers is the possibility of losses due to amounts overpaid for unworked vacation. The manager may face difficulties withholding funds in the event of dismissal of an “over-rested” employee. An employee does not always agree to compensation for vacation pay of his own free will, while it is very difficult to claim this money in court. The law mainly protects the interests of workers, and the regulations provide for a large number of circumstances to which the claim for compensation does not apply, for example:

- the amounts due before dismissal are not enough to cover the debt;

- if the deduction is not made directly upon dismissal, you will have to act through the court or accept the loss of money, the employer has no other legal ways to force the employee;

- the reason for dismissal excludes the possibility of claiming the debt.

Deduction for vacation upon dismissal tax accounting

Many accountants are concerned about the question of how to withhold personal income tax and calculate insurance premiums when withholding vacation pay for unworked vacation days? The answer to this depends on whether the amount of the employee’s last salary is sufficient to deduct for unworked vacation days or not.

In the situation under consideration, for example, the following options are possible:

- the employee’s last salary is more than the amount of deductions;

- The employee's last salary is less than the amount of deductions. In this case, the employee voluntarily returns the amount of vacation pay for unworked vacation days;

- The employee's last salary is less than the amount of deductions. At the same time, the employee refuses to voluntarily return the amount of vacation pay for unworked vacation days.

If the amount of payments to an employee upon dismissal is sufficient to withhold the amount of vacation pay for unworked vacation days, then proceed as follows.

In accounting, reflect the accrual of the employee’s last salary (without reducing it by the amount of overpaid vacation pay). Withhold personal income tax from the salary amount, charge contributions for compulsory pension (social, medical) insurance and insurance against industrial accidents and occupational diseases.

Reverse the amount of excessively accrued vacation pay in accounting. This conclusion follows from the letter of the Ministry of Finance of Russia dated October 20, 2004 No. 07-05-13/10. Accordingly, make reversing entries for withholding personal income tax and calculating insurance premiums from the amount of overpaid vacation pay.

The basis for correctional entries is an accounting certificate reflecting the amount of vacation pay for unworked vacation days.

Give the employee his final salary minus the withheld vacation pay amounts.

When paying vacation pay, personal income tax was withheld and paid to the budget. Therefore, calculate the personal income tax for the employee’s last month of work by crediting the tax withheld from vacation pay for unworked vacation days. The provisions of paragraphs 2 and 3 of Article 226 of the Tax Code of the Russian Federation allow you to do this.

When filling out Form 2-NDFL for the current year, reflect the amount of vacation pay minus overpaid vacation pay for unworked vacation days. Do this in the month in which the vacation pay was paid.

Upon dismissal, the date of receipt of income is considered to be the last day of work (Clause 2 of Article 223 of the Tax Code of the Russian Federation). Therefore, reflect the employee’s last salary in form 2-NDFL in the month of dismissal (in the actual accrued amount, without reducing by the amount of withheld vacation pay).

Insurance premiums from the employee's last salary are subject to payment minus previously transferred contributions accrued from vacation pay for unworked vacation days (i.e., reversed contributions).

- Download forms on the topic:

- Vacation schedule (form T-7)

- Vacation schedule (form T-7)

- Vacation schedule (filling example)

- Certificate of employment (for obtaining a visa)

- Notifying the employee about the start date of his vacation

Stay up to date! There is too much accounting news and too little time to search for it. We recommend subscribing to the Glavbukh magazine newsletter to keep track of all changes in the work of accountants.

“Paper” registration of early leave

It is no different from the traditional one, the sequence of actions remains usual:

- An employee writing a statement.

- Positive endorsement of the application by management.

- Issuing an order to grant leave.

- Accrual of “vacation” funds (the only difference is that they have not yet been earned).

ATTENTION! If the employee has been working for more than a year, then the first point will be preceded by scheduling vacations.