Failure to pay the actual value of the share

According to the Federal Law of 02/08/1998 No. 14-FZ (as amended on 07/29/2017) “On Limited Liability Companies” (hereinafter referred to as the LLC Law), virtually any of the participants (founders) has the right to leave the company (LLC).

I quote paragraph 1 of Art. 26 (Withdrawal of a company participant from the company) :

- A participant in a company has the right to leave the company by alienating a share to the company, regardless of the consent of its other participants or the company, if this is provided for by the charter of the company. The application of a company participant to withdraw from the company must be notarized according to the rules provided for by the legislation on notaries for certifying transactions.

- The right of a company participant to leave the company may be provided for by the company’s charter upon its establishment or when amendments are made to its charter by decision of the general meeting of company participants, adopted unanimously by all company participants, unless otherwise provided by federal law.

At the same time, it is worth considering one important point: the withdrawal of a participant from the company (LLC) cannot be carried out in the following cases:

- if the participant (founder) is only one person;

- if all participants (founders) decided to leave.

If a participant leaves the company on the basis of his submitted application for withdrawal from the company, then from the moment such an application is received by the company, the share of this participant passes to the company, and the company becomes obligated to pay the actual value of the share to this participant within the period prescribed by law for payment of the actual value of the share when a company participant leaves the company.

How is the actual value of a share paid when a participant leaves?

Payment to the participant of the actual value of the share is made in cash and, as a rule, by wire transfer to the account of the withdrawing participant. But in the case when payment of the actual value of a share of property on the basis of the consent received from the withdrawing participant must be made in the form of property of the same value, then such property is transferred under the appropriate transfer deed.

How to calculate the actual value of a share

In order to pay the actual value of the share when a participant leaves the company, the accountant needs to calculate the actual value of the share when the participant leaves.

In order to know how to calculate the actual value of a share, it is necessary to understand that the company can give the withdrawing participant, in place of money, in kind property of the same value, but this may be feasible after obtaining consent from this participant.

According to Art. 14 of the Law on LLC, the authorized capital of a company consists of the nominal value of the shares of its participants, and the shares of participants in this authorized capital are determined as percentages or as fractions.

According to paragraph 2 of Art. 14 of the LLC Law, I quote :

- The size of the share of a company participant must correspond to the ratio of the nominal value of his share and the authorized capital of the company.

- The actual value of the share of a company participant corresponds to a part of the value of the company's net assets, proportional to the size of his share.

✎ Example:

The authorized capital of Romashka LLC consists of 10,000 rubles. Romashka LLC was founded by three participants (founders - individuals) in the following shares:

- Participant 1 – 8% of the authorized capital, which is 800 rubles;

- Participant 2 – 22% of the authorized capital, which is 2200 rubles;

- Participant 3 – 70% of the authorized capital, which is 7,000 rubles.

You can also represent these fractions as a decimal fraction:

- Participant 1 – 0.08 authorized capital;

- Participant 2 – 0.22 authorized capital;

- Participant 3 – 0.70 (or 0.7) of the authorized capital.

You can also represent these shares as an ordinary fraction:

- Participant 1 – 2/25 of the authorized capital;

- Participant 2 – 11/50 of the authorized capital;

- Participant 3 – 7/10 of the authorized capital.

It is worth noting that in the rarest cases, shares are indicated in the form of an ordinary fraction, but this is not a fundamental issue.

Based on this, the accountant should always know that the actual value of the share of a company participant corresponds to a part of the value of the company’s net assets, proportional to the size of his share. And according to Order of the Ministry of Finance of the Russian Federation dated August 28, 2014 No. 84n “On approval of the procedure for determining the value of net assets,” namely clause 4 of the Procedure for determining the value of net assets, I quote:

- The net asset value is determined as the difference between the value of the organization's assets accepted for calculation and the value of the organization's liabilities accepted for calculation. Accounting items recorded by the organization on off-balance sheet accounts are not taken into account when determining the value of net assets.

Deadline for payment of actual share value

In order to avoid non-payment of the actual value of the share, it is necessary to know that the law provides for a period for payment of the actual value of the share when a company participant leaves the company by alienating his share based on the company participant’s application to leave the company.

According to clause 6.1. Art. 23 of the Law on LLC, the deadline for payment of the actual value of the share or, with the consent of the withdrawing participant, the deadline for issuing property of the same value to him in kind, or in the event of incomplete payment by him of the share in the authorized capital of the company, the actual value of the paid part of the share is 3 (three) months from the date of occurrence corresponding obligation, unless a different period or procedure for payment of the actual value of a share or part of a share is provided for by the charter of the company.

Such an obligation arises when a share or part of a share is transferred to the company from the date the company receives an application from a company participant to leave the company, if the participant’s right to leave the company is provided for by the company’s charter.

✎ It is worth noting that:

The company does not have the right to pay the actual value of a share or part of a share in the authorized capital of the company or to issue in kind property of the same value, if at the time of these payments or issuance of property in kind it meets the criteria of insolvency (bankruptcy) in accordance with the federal law on insolvency (bankruptcy) or as a result of these payments or the issuance of property in kind, the specified signs will appear in the company.

Calculation of the actual value of a share upon withdrawal of a participant

As such, the calculation of the actual value of the share upon withdrawal of a participant can be represented as the following formula:

Std = RFA x RDUUK

- Std is the actual value of the share;

- RFA is the size of net assets;

- RDUUK is the size of the participant’s share in the authorized capital.

Since the actual value of a share or part of a share in the authorized capital of a company is paid out of the difference between the value of the company’s net assets and the size of its authorized capital, then if such a difference is insufficient, the company is obliged to reduce its authorized capital by the missing amount.

And since a decrease in the authorized capital of a company may lead to its size becoming less than the minimum amount of the authorized capital of the company established by the Law on LLC, on the date of state registration of the company, the actual value of the share or part of the share in the authorized capital of the company is paid out of the difference between the value net assets of the company and the specified minimum amount of the authorized capital of the company.

At the same time, it is worth noting that the deadline for payment of the actual value of the share in this case or part of the share in the authorized capital of the company is established in such a way that it can be paid no earlier than 3 (three) months from the date the basis for such payment arose.

An equally important point is that in such circumstances, the payment of the actual value of a share when not one but several participants leave, the actual value of such shares or parts of shares is paid from the difference between the value of the company’s net assets and the specified minimum amount of its authorized capital in proportion to the size shares or parts of shares owned by company participants.

✎ It is worth noting that:

There are also controversial issues regarding the valuation of property on the company’s balance sheet when determining the actual value of a share in the authorized capital of the company upon the withdrawal of a participant, where in most cases the courts proceed from the legal position set out in the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated April 17, 2012 No. 16191/11 on case No. A40-18600/05-134-138, which states that the actual value of a share in the authorized capital of a company upon the exit of its participant is determined taking into account the market value of real estate reflected on the balance sheet of the company, and due to the legal position set out in the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated September 10, 2013 No. 3744/13 in case No. A28-358/2012, the amount of the actual value of a share in the authorized capital of a company is determined based on the market value of real estate without including the amount of value added tax. However, Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated September 10, 2013 No. 3744/13 in case No. A28-358/2012 has a number of references to Order of the Ministry of Finance of the Russian Federation No. 10n, FCSM of the Russian Federation No. 03-6/pz dated January 29, 2003 “On approval of the Procedure for assessing the value of net assets of joint-stock companies”, which lost its force after the entry into force (November 4, 2014) of the Order of the Ministry of Finance of Russia dated August 28, 2014 No. 84n “On approval of the Procedure for determining the value of net assets,” which is current as of December 2020.

Payment of shares in the authorized capital

After the founders agree on the distribution of shares in the authorized capital of the company, it is necessary to pay for them. According to current legislation, company participants have the right to use several options for paying for a share in the authorized capital (Article 15 of the Federal Law “On LLC”):

- cash;

- securities;

- property.

Important!

The share of an LLC participant contributed by property must have a mandatory assessment by an independent appraiser. The minimum amount of authorized capital is 10,000 rubles. You can only pay in cash.

If during the year a participant does not pay for his share in the authorized capital, or does not pay it in full, this part of the share/share is considered to belong to the company (Articles 15 and 16 of the Federal Law “On LLC”). In this case, the company’s share during the year must be distributed among the company’s participants. Please keep in mind that the share owned by the company is not taken into account when voting at the General Assembly, distributing the company’s profits, and the company’s property during its liquidation (Article 24 of the Federal Law “On LLC”).

https://youtu.be/gNa5MbXyjhM

The procedure for paying a share to an LLC participant upon exit

After the company receives a participant’s request to pay him the actual value of his share in connection with withdrawal, it is obliged to pay it no later than 3 months. This period is fixed in paragraph. 3 p. 2 art. 23 of Law 14-FZ, but by the organization’s charter it can be changed up or down.

The inclusion in the charter of a provision establishing a period other than that specified by law can be carried out not only when establishing an organization, but also subsequently. However, the law requires that all participants vote for such a change, otherwise it cannot be considered adopted.

Upon receipt of the relevant notification from the participant, it is necessary to conduct an assessment of the net assets of the enterprise, which will determine the total amount due to the participant.

Form of payment of actual value according to paragraph. 3 p. 2 art. 23 of Law 14-FZ can be not only monetary, but also in kind, that is, in the form of things of equal value. In this case, the natural form can only take place with the consent of the participant himself.

The transfer of funds or property at the appropriate value must be recorded. Confirmation of such payment can include both documents confirming the fact of non-cash payment and written receipts from the withdrawing participant. Such a receipt is in free form, but by virtue of clause 2 of Art. 23 of Law 14-FZ must contain an indication of what this or that asset is being transferred for and what its value is.

Vacancy of the post of founder

A purposeful decision to vacate the post of founder of an organization can be made at any period of its functioning. No one should or has the right to interfere if the participant makes such a decision. But according to the law, the exit procedure must follow two simple but important conditions:

- The presence in the organization's charter of the right to exit. This means not only the very possibility of voluntarily vacating a post, but also recording the consequences associated with it.

- Society cannot consist of one person, there must be at least two.

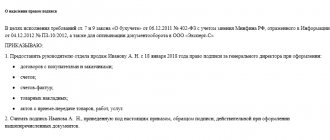

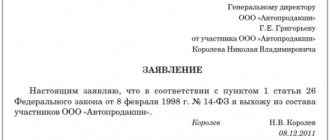

If these conditions are met, the organizer will need to write a statement to exit. There are no special requirements for the text (if necessary, you can always), so it is written in any form and handed to the director or other authorized person. The moment of delivery is considered the moment of leaving the organization.

When a founder decides to leave the LLC, he only needs to write a statement and hand it to the director or authorized person of the organization.

In addition, the organizer can leave his post as a member on the following grounds: due to his exclusion by other participants, due to death (here it is important that his heirs must demand payment).

The expulsion of an organizer, as a rule, occurs when serious conflicts arise between participants that undermine the activities of the society, make it impossible or problematic. The rule on exclusion may not be prescribed in the charter - it is applied if necessary, regardless of this.

Example: participant Petrov deliberately avoids attending general meetings, which is why it is impossible to make important decisions for the organization at them. The work of society is disrupted, deals are disrupted. Therefore, a decision is made to exclude Petrov from the list of participants.

It should be noted that, regardless of the grounds for vacating the post of founder, the value of the share is paid to him in any case, with the exception of situations when the company is in a state of bankruptcy.

Value added tax (VAT)

The transfer of property within the limits of the initial contribution to a participant in a business company upon his withdrawal from the company is not recognized as a sale and, accordingly, is not recognized as an object of taxation for VAT (clause 5, clause 3, article 39, subclause 1, clause 2, article 146 of the Tax Code of the Russian Federation link).

At the same time, in the tax period in which the fixed assets object is transferred to a company participant, the organization is obliged to restore the “input” VAT in an amount determined in proportion to the residual value of the fixed assets object at the time of transfer (clause 4, clause 2, paragraphs 1, 2, 4 pp. 2 clause 3 article 170 of the Tax Code of the Russian Federation).

Consequences of late payment

Payment to a company participant of the value of his share in the event of withdrawal is the obligation of this company by virtue of paragraph. 3 p. 2 art. 23 of Law 14-FZ. Failure to pay the cost of the share within the time period provided for by law or the charter of the enterprise entails certain negative consequences for the enterprise associated with additional financial costs.

Thus, from the first day following the payment deadline, the withdrawing participant has the right to file claims in court for such payment, as well as the accrual of interest for the use of someone else’s money on the basis of Art. 395 of the Civil Code of the Russian Federation.

In addition, in accordance with paragraph. 5 paragraph 8 art. 23 of Law 14-FZ, upon a written application from a company participant, it must accept him back on the basis of the impossibility of paying him the value of his share and providing him with property.

Recovery of moral damages, including from the point of view of the courts (for example, the resolution of the Federal Arbitration Court of the Volga District dated March 13, 2008 in case No. A55-5543/07), is not possible in such a situation. This is caused by the contradiction of this requirement, as the courts believe, with the very norm of Art. 151 of the Civil Code of the Russian Federation on compensation for moral damage.

Accounting

The company's acquisition of part of its equity capital is reflected in financial documents. The preparation of entries when a participant leaves an LLC is regulated by Instruction of the Ministry of Finance of the Russian Federation No. 94n dated October 31, 2000.

| the name of the operation | Debit | Credit |

| Transfer of a share from a participant to the company | ||

| Payment of actual value | 75 | () |

You will also have to take care of compliance with tax laws. Personal income tax is not paid for assets owned by an individual for 5 years or more. This opinion is shared by the Russian Ministry of Finance in letter No. 03-04-06/80846 dated 11/09/18. The officials' conclusion is based on the provisions of clause 17.2 of Art. 217 Tax Code of the Russian Federation.

In other cases, the tax is calculated at a rate of 13% (residents) or 30% (non-residents). The funds are retained by the company at the time the amount is transferred. The company acquires the status of a tax agent. Citizens of Russia can take advantage of the deduction under Art. 220 Tax Code of the Russian Federation. The norm allows you to reduce the calculation base by direct costs associated with the acquisition of a share in the capital of an LLC.

For the founder-organization, the tax consequences will be somewhat different. The taxation regime will become key in this situation. Payers of OSN are required to include in the calculation of profit the difference between the actual value of the asset and the real contribution made to the capital earlier (Articles 251, 277 of the Tax Code of the Russian Federation). A similar procedure is applied by organizations under the simplified regime. The payment is included in income. The rate is determined by the selected object - 6 and 15% (Article 346.15, 346.20 of the Tax Code of the Russian Federation).

The Romashka Society made a contribution of 100 thousand rubles to Buket LLC. After 3 years, the founding organization withdrew with a payment of 400 thousand rubles. The tax calculation will look like this:

| OSN | simplified tax system | |

| 6% | 15% | |

| (400,000 – 100,000)× 20% = 60,000 rubles | 400,000 × 6% = 24,000 rubles | (400,000 – 100,000) × 15% = 45,000 rubles |

The basis for settlements with the budget are documents on the withdrawal of participants from the LLC. There is no need to draw up contracts. However, the parties can determine the amount of payment by separate agreement. This is not prohibited by law.