VAT is one of the most significant taxes in the Russian Federation. It replenishes the country's federal budget. VAT is considered an indirect tax. It falls on the shoulders of the end customers. Those. The more intermediaries (more precisely, the intermediary price) there are between the producer and the consumer, the higher the state income. No one thought, maybe this is why the state is so actively eliminating “outbidders”? But that's a completely different topic. We will talk in more detail about VAT 10 percent (the list of goods taxed at this rate). But first, let’s talk about how the tax came about.

The history of the appearance of tax in Russia

In our country, VAT has been in effect since 1992. Before this, there was a sales tax.

But such a measure legally exempted many subjects from payment. Then the government of Yegor Gaidar introduced VAT.

It was then regulated by a separate Federal Law, which was called “On Value Added Tax.”

In 2000, the law was “merged” into the Tax Code. The basis of the collection was taken from the USA. But at the moment, almost all countries apply a similar principle for calculating it. Only the rates differ.

Current VAT rates

To begin with, it is worth saying that the value added tax rate is not one, or even three – as many as five can be recognized as such:

- There are only three main ones - 0, 10 and 20%. They are needed to add to the cost of goods and services. Which goods are subject to 10% VAT will be discussed further.

- There are also additional, calculated ones - 20/120 and 10/110. Useful to find out how much of the price is VAT.

Previously, the basic VAT was 18 percent, and the corresponding calculation coefficient was 18/118. But from January 1, 2020, this value increased to 20%, and the calculated value increased accordingly. There were no changes for the rest.

Was it good before?

For those who like to criticize modern “exorbitant taxes”, as well as “sentimentalists” who claim “how wonderful it used to be,” let’s say that from 1992 to 1993 the tax was 28% (a VAT rate of 10 percent looks fantastic against this background). From 1994 to 2004 the rate was reduced to 20%.

Of course, one can argue that “there were no other taxes.” But at this time, personal income tax was also reduced to 13%. At that time, “everyone was coming out of the shadows.” The state reduced rates because the majority preferred not to pay anything. The impotence of law enforcement and tax services, coupled with high stakes, explained the reason for this behavior. Maybe “admirers of the past” remembered this, without paying absolutely any fees.

What is VAT

VAT is a type of indirect tax on goods or services at the time of sale. It is taxed at all stages of production and ultimately falls on the consumer.

That is, the higher the “appetites” of producers, the more profitable it is for the state. For example, you were sold chicken in a store. Its cost was 50 rubles. And the buyer paid 200 rubles for it. A percentage of 150 rubles (200-50) will have to be paid in the form of value added tax. If the seller had been “generous” and the goods had “been given for what he took”, i.e., had not added anything to the original price, then the state would not have received a penny from such a transaction.

It doesn't matter whether the company is making a profit or operating at a loss. VAT is not cancelled. Hence the conclusion: the more they cheat, the better the federal budget. Let's think about whether the state really needs to limit the arbitrariness of intermediaries. With such a system, on the contrary, their growth is only beneficial to the budget. Now let's move directly to the tax rates that are established by the amended Tax Code (2015 edition).

Procedure for confirming codes for preferential tax rates

The entrepreneur is obliged to fill out and submit quarterly calculations and an annual value added tax return to the Federal Tax Service. When filling out these reports, organizations and individual entrepreneurs themselves calculate VAT, i.e. must correctly determine and indicate the rate at which their goods will be taxed.

The legality of reducing tax rates depends on the accurate selection and confirmation of codes according to the OKP and TN VED classifiers. If you fill out the declaration incorrectly, you face a large fine under the Tax Code of the Russian Federation, additional financial expenses, the need to contact the Federal Tax Service with corrective forms, and file complaints in court.

You need to select codes according to OKP2 and Commodity Nomenclature of Foreign Economic Activity based on the identification characteristics of products or products, its description, intended purpose, composition of materials, degree of processing or readiness, and other indicators. To avoid mistakes, please contact our specialists to correctly determine the OKP2 codes and apply the VAT rate of 10 percent. We will help you confirm your right to a preferential rate in the following ways:

- by providing assistance in the development and registration of technical specifications for a product or children's product (the document will contain all the features that allow the product to be correlated with OKPD2 indicators);

- issuing a voluntary certificate of conformity in the GOST R system;

- having received an official conclusion from the Chamber of Commerce and Industry (CCI), which will officially confirm the code for your product;

- by providing assistance in filling out the declaration using preferential rates.

As a rule, documentation is sufficient to confirm the OKPD2 or HS code. However, in the most difficult situations, an examination may be required, an actual study of the properties and characteristics of manufactured goods or food products in the laboratory. You can also get consulting support from experienced specialists on any issues related to product identification.

How much do we pay to the state?

How to determine how much the government will take from the price increase? The 2020 Tax Code provides for three rates: 18% (standard), 10% (preferential) and 0% (customs). VAT rates of 10 and 18% are “internal”.

They apply to goods and services only within the country. If they are exported outside the country, no tax is charged. If you pay VAT when purchasing a product and reselling it abroad, the tax paid is refundable.

What VAT rates apply

To calculate VAT, there are several basic rates - 20%, 10% and 0%, and several calculated rates - 20/120, 10/110 and 16.67%, which are used depending on the type of transaction:

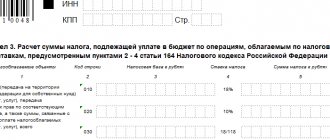

- 20% is the general rate that applies to most transactions (clause 3 of Article 164 of the Tax Code of the Russian Federation). At this rate, tax transactions that are not specified in the Tax Code of the Russian Federation as grounds for applying other rates;

- 10% is the rate at which tax is calculated on the import and sale of certain goods, as well as on the sale of certain services. In paragraph 2 of Art. 164 of the Tax Code of the Russian Federation indicates goods and services, and in the lists approved by the Government of the Russian Federation - product codes. For example, this rate is applied when selling food or medical goods (clause 2 of article 164 of the Tax Code of the Russian Federation);

- 0% - applies to exports, international transport and other operations listed in clause 1 of Art. 164 Tax Code of the Russian Federation;

- 20/120 or 10/110 are estimated rates that are used in cases where the tax base includes VAT. The main cases are listed in paragraph 4 of Art. 164 Tax Code of the Russian Federation. For example, receiving advances, withholding VAT by a tax agent. A settlement rate of 20/120 or 10/110 is applied depending on the rate at which the main transaction is taxed;

- 16.67% is a special settlement rate, which is applied only in two cases: when selling an enterprise as a whole as a property complex and when foreign companies provide services to individuals in electronic form (clause 4 of article 158, clause 5 of article 174.2 of the Tax Code RF).

Is it possible to choose the rates at which to tax VAT transactions?

https://www.youtube.com/watch?v=ytdevru

You cannot choose the VAT rate arbitrarily. Applying the appropriate rate is your responsibility, not your right.

Thus, as a general rule, VAT cannot be calculated at the basic rate (20%) if the transaction is taxed at reduced rates (0% or 10%). The exception is certain transactions, which are taxed at a rate of 0%. In relation to them, you can refuse the zero VAT rate (clause 7 of Article 164 of the Tax Code of the Russian Federation).

VAT rate 10 percent: list of goods and services

18 percent is the regular VAT rate. However, there is a list of goods that reduces it to 10. Many entrepreneurs ask the question: “In what cases is 10% VAT applied?” Let's try to answer it.

The VAT rate is 10 percent, the list of goods and services assumes the following:

- Foodstuffs.

- Domestic air transportation.

- Childen's goods.

- Some medications.

- Periodical printed materials.

The list of all goods was approved by Government Decree No. 908 of December 31, 2004. It is in this document that the entire list is indicated, which is subject to VAT of 10 percent. The list (brief) is given below:

- Milk and dairy products.

- Meat in live weight.

- Eggs.

- Cooking fats, vegetable oil.

- Salt.

- Flour and pasta products.

- Vegetables.

- Children's and diabetic nutrition, etc.

Estimated VAT rates

Estimated VAT rates are applied in cases where the tax amount is included in the tax base and needs to be extracted from there. The list of the most common cases is given in paragraph 4 of Art. 164 Tax Code of the Russian Federation. For example, settlement rates should be used in the following situations:

- upon receipt of an advance for the supply of goods, performance of work, provision of services;

- receipt of funds related to payment for goods (work, services) provided for in Art. 162 Tax Code of the Russian Federation;

- sales of cars purchased from individuals (clause 5.1 of Article 154 of the Tax Code of the Russian Federation);

- withholding VAT by a tax agent (clauses 1 - 3 of Article 161 of the Tax Code of the Russian Federation);

- assignment (termination) of a monetary claim (clauses 2, 4, Article 155 of the Tax Code of the Russian Federation);

- transfer of property rights to housing, garages, parking spaces (clause 3 of Article 155 of the Tax Code of the Russian Federation).

To calculate VAT, three settlement rates are provided: 10/110, 20/120 and 16.67% (clause 4 of article 158, clause 4 of article 164, clause 5 of article 174.2 of the Tax Code of the Russian Federation).

In what cases is the estimated VAT rate of 20/120 applied?

The VAT rate of 20/120 is applied in all cases where the main transaction is taxed at a rate of 20% (clause 4 of Article 164 of the Tax Code of the Russian Federation).

For example, you must apply a calculated rate of 20/120 if you received (clauses 1 - 3 of Article 161, clauses 3 of clause 1 of Article 162, clauses 3, 4 of Article 164 of the Tax Code of the Russian Federation):

- advance payment for the supply of goods, performance of work, provision of services, which are taxed at a rate of 20%;

- interest (discount) on bonds and bills of exchange, which are transferred as payment for goods, works, services, taxed at a rate of 20%;

- interest on a trade loan as part of the sale of goods taxed at a rate of 20%;

- property for rent from state and municipal authorities.

In addition, this rate applies if you purchased from a foreign person who is not registered with the Russian Federation for tax purposes, goods (work, services) taxed at a rate of 20%.

In what cases is the estimated VAT rate of 10/110 applied?

The estimated VAT rate 10/110 is applied in cases where the goods sold or services provided are subject to VAT at a rate of 10% (clause 4 of Article 164 of the Tax Code of the Russian Federation).

For example, you would apply a settlement rate of 10/110 if you received an advance for the supply of goods that are taxed at 10%.

In what cases is the estimated VAT rate of 16.67% applied?

Estimated VAT rate of 16.67% applies:

- when selling the enterprise as a whole as a property complex (clause 4 of article 158 of the Tax Code of the Russian Federation);

- provision of electronic services (including via the Internet) to the population by foreign organizations (clause 5 of Article 174.2 of the Tax Code of the Russian Federation).

Everyone is dissatisfied

This law did not satisfy anyone. The government due to the fact that it began to receive less money due to the budget deficit. Air carriers say this will not solve the industry's problem.

The head of Aeroflot, Vitaly Savelyev, expressed dissatisfaction with this matter. He believes that in the current situation it is necessary to completely remove VAT from air carriers on domestic flights. The situation turns out to be that it is almost cheaper to get from Vladivostok to Moscow on a “round-the-world trip”.

Is Crimea ours?

An interesting situation concerns Crimea and Sevastopol. Referendum, annexation - we all know this very well. But as far as legislation is concerned, not everything is so simple. So internal regulations make us think – is Crimea ours? Russian?

This concerns the law on amendments to the Tax Code in 2020, according to which domestic air transportation is subject to a preferential tax of 10%. The same regulatory legal act contains the wording, “except for trips to Crimea and Sevastopol.”

Apparently, Russian companies are afraid of possible economic sanctions “from recognizing” Crimea as Russian territory. For this purpose, similar regulations on tariffs, taxes, etc. are adopted. Companies do not violate domestic law and are not subject to international sanctions.

10+10=28?

In the section “VAT rate of 10 percent: list of goods and services,” we said that there is a category of socially significant goods that have a VAT exemption. The full list of codes and names is prescribed in Decree of the Government of the Russian Federation of December 31, 2004 No. 908.

But what to do when the product is “at the junction” of two items. In addition, situations seem paradoxical when the products sold consist entirely of “preferential” goods, but are subject to 18%.

For example, pizza. It may consist entirely of those products that are eligible for the benefit. Flour, eggs, meat, cheese, etc. But the “combination” of these “social” products into a “delicacy” pizza is taxed “to the fullest.”

This provision is clarified by letters of the Ministry of Finance dated September 10, 2010 No. 03-07-14/63 and the Federal Tax Service for Moscow dated March 16, 2005 No. 19-11/16469. According to them, VAT of 10 percent is charged on the sale of goods that are included in Government list. The rest fall under 18%.

This list includes the category “pies, pies, donuts,” as well as meat, various cereals, and vegetables. But there is no such thing as “empanadas” or “pizza.” Here officials apply the principle “what is not permitted is prohibited.” They believe they should pay the full 18 percent for spring rolls.

VAT rate on food sales

When selling food products, VAT is calculated at a rate of 10% or 20%.

The VAT rate of 10% applies only to certain types of products in accordance with paragraphs. 1 item 2 art. 164 Tax Code of the Russian Federation.

The code of a food product according to OKPD2 or according to the Commodity Code of Foreign Economic Activity of the EAEU, which is indicated in the documentation for the product, must be included in one of the Lists of product codes for food products. This follows from paragraph 2 of Art. 164 of the Tax Code of the Russian Federation, clause 20 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated May 30, 2014 N 33, Letter of the Ministry of Finance of Russia dated January 16, 2018 N 03-07-07/1527.

A rate of 20% applies if the code according to OKPD2 or the EAEU HS, which is indicated in the documentation for the food product, is not in the relevant Lists (clause 3 of Article 164 of the Tax Code of the Russian Federation).

https://www.youtube.com/watch?v=https:accounts.google.comServiceLogin

At what rates is VAT taxed on sugar sales?

Sales of sugar are subject to VAT at a rate of 10% if the code according to OKPD2 or the EAEU HS, which is indicated in its documentation, is contained in one of the relevant Lists.

For example, if the documentation for sugar indicates code 10.81.12 according to OKPD2, then VAT on its sale is calculated at a rate of 10% (clause 1, clause 2, article 164 of the Tax Code of the Russian Federation, List of codes for types of food products that are subject to VAT at a rate of 10 % upon their implementation (approved by Decree of the Government of the Russian Federation of December 31, 2004 N 908)).

If the documentation for sugar indicates a code according to OKPD2 or the EAEU HS, which is not in the Lists approved by Decree of the Government of the Russian Federation of December 31, 2004 N 908, then calculate VAT on its sale at a rate of 20% (clause 3 of Article 164 of the Tax Code of the Russian Federation ).

At what rates is VAT taxed on the sale of fish and other seafood products?

A VAT rate of 10% applies to fish and other seafood if the code according to OKPD2 or the EAEU HS, which is indicated in their documentation, is contained in one of the relevant Lists. If there is no such code in the Lists, use a rate of 20% (clauses 2, 3, Article 164 of the Tax Code of the Russian Federation).

For example, if the documentation for fish indicates code 03.22.10.160 according to OKPD2, then VAT on its sale is calculated at a rate of 10% (clause 1, clause 2, article 164 of the Tax Code of the Russian Federation, List of codes for types of food products that are subject to VAT at a rate of 10 % upon their implementation (approved by Decree of the Government of the Russian Federation of December 31, 2004 N 908)).

Please note that the sale of valuable species of fish and delicious seafood and fish products is always taxed at a rate of 20% (clauses 2, 3 of Article 164 of the Tax Code of the Russian Federation).

At what rates is VAT taxed on the sale of bakery products?

Sales of bakery products are subject to VAT at a rate of 10% if the code according to OKPD2 or according to the EAEU HS, which is indicated in their documentation, is contained in one of the relevant Lists. If there is no such code in the Lists, use a rate of 20% (clauses 2, 3, Article 164 of the Tax Code of the Russian Federation).

For example, if the documentation for a bakery product indicates code 10.71.11 according to OKPD2, then VAT on its sale is calculated at a rate of 10% (clause 1, clause 2, article 164 of the Tax Code of the Russian Federation, List of codes for types of food products that are subject to VAT at the rate 10% upon their sale (approved by Decree of the Government of the Russian Federation of December 31, 2004 N 908)).

https://www.youtube.com/watch?v=ytaboutru

At what rates is VAT taxed on the sale of juices?

The VAT rate for the sale of juice is 20%, since this food product is not named in the list of food products, the sale of which is subject to VAT at a rate of 10% (clause 1, clause 2, clause 3, article 164 of the Tax Code of the Russian Federation).

The exception is juices for baby food. Their sales are subject to VAT at a rate of 10% (clause 1, clause 2, article 164 of the Tax Code of the Russian Federation).

For example, to apply a VAT rate of 10%, the documentation for juice must indicate one of the following codes according to OKPD2 (List of codes for types of food products that are subject to VAT at a rate of 10% upon their sale, approved by Decree of the Government of the Russian Federation of December 31, 2004 N 908) :

- 86.10.243 - fruit and fruit and vegetable juices for baby food;

- 86.10.245 - juice-containing fruit and fruit-vegetable drinks for baby food;

- 86.10.246 - fruit and fruit and vegetable nectars for baby food;

- 86.10.247 - fruit drinks for baby food.

At what rates are catering products subject to VAT?

VAT rates of 10% and 20% apply to catering products.

A 10% rate applies if the following conditions are met:

- the product is a food product, which is named in paragraphs. 1 item 2 art. 164 Tax Code of the Russian Federation;

- the product code according to OKPD2 or the EAEU HS, which is indicated in the documentation for it, is contained in one of the relevant Lists.

As for finished products, a VAT rate of 10% can also be applied if its code according to OKPD2 is contained in the List of codes for types of food products that are subject to VAT at a rate of 10% upon their sale (approved by Decree of the Government of the Russian Federation of December 31, 2004 N 908) .

For example, the VAT rate of 10% is levied on the sale of butter pies and buns. Such products have code 10.71.11.130 according to OKPD2, which, in turn, is included in group 10.71.11 specified in the List of codes for types of food products that are subject to VAT at a rate of 10% upon their sale (approved by Decree of the Government of the Russian Federation of December 31. 2004 N 908).

A rate of 20% is applied if these conditions are not met (clause 3 of Article 164 of the Tax Code of the Russian Federation).

The arbitration court is on the side of entrepreneurs

In addition, entrepreneurs use code classifiers that mean “bakery products” for pizza, as well as “meat and meat products” for stuffed meat pancakes. Both of these codes "allow" 10 percent to apply.

Such a “trick” can lead to arbitration. Tax authorities dispute the rate of 10 percent, insisting on 18. But arbitration practice is often on the side of entrepreneurs, because according to GOST “Public catering services. Terms and definitions”, approved by order of the State Standard of Russia dated November 30, 2010, flour culinary products include pies, belyashi, and pizza. And these products contain various fillings.