Compensation and wages

The Labor Code of the Russian Federation in Article 129 synonymizes the concepts of “remuneration” and “wages” and defines them as a set of three elements:

| 1. remuneration for work | main (mandatory) part |

| 2. compensation | |

| 3. incentive payments | additional part |

However, it is worth considering that not all components are required to be paid to the employee.

Monthly earnings cannot be lower than the minimum wage level established by the Government, and includes allowances for the complexity of the work and special conditions (work on weekends, etc.). But incentives remain at the discretion of the employer and are awarded only if the employee has done his job well, in the opinion of the employer.

As a result, it turns out that the concept of remuneration is broader than the concept of wages, because is a list of all the elements from which the wages of a particular employee are subsequently collected.

Each employer decides independently how to pay wages, taking into account the minimum provisions of the Labor Code.

Art. Art. 23 and 132 of the Labor Code establish the impossibility of discrimination against workers with equal qualifications, output and quality of work. This means that you cannot set different pay for the same work.

Accordingly, the employer must apply uniform parameters when setting wages. A variation of such parameters represents a remuneration system. It must be based on legal norms and not worsen the employee’s position in comparison with them.

The concept of wages and its determining factors

Nominal salary

is the amount of money accrued to an employee for his work.

Real salary

– this is the quantity of goods and services that can be purchased for a nominal salary.

Meeting in the labor market, households and business organizations determine the level of nominal salary, while the price of labor has its own specific characteristics:

1) it is not profitable for an enterprise to establish flexible labor rates; a rigid administrative wage system is much more economical and functional, i.e. one in which labor rates are controlled by the administration and fixed at a certain level. This level is formed taking into account the current labor legislation, the industry average wage level and the strategy of the enterprise.

2) institutional restrictions

– this is labor legislation and the activities of trade unions.

3) restriction of geographic mobility.

4) sociological restrictions, primarily discrimination.

5) the existence of deliberately non-competitive groups in remuneration.

6) equalization of non-monetary differences in work through payment (compensation for the unattractiveness of work with money).

7) the existence of monopsony labor markets.

There is a certain limit after which an employee values his free time more than money for work.

There is a certain limit after which an employee values his free time more than money for work.

Forms of remuneration

Do not confuse the concepts of “payment system” and “form of payment” - they are not identical, although in the literature they replace each other.

A system is a set of rules for remuneration. Form is one of these rules.

Art. 131 of the Labor Code of the Russian Federation establishes two forms in which labor can be paid:

- Cash – made in rubles.

- Non-monetary - in kind - paid in any material or immaterial form not prohibited by law. The size of the natural part is no more than 15% of the person’s entire salary.

Pay systems

The remuneration system is a documented “instruction” on how to calculate an employee’s salary for a specific period worked, containing a complete list of parameters for the accrual and deduction of funds.

The employer, depending on the nature of the business activity, can use wages to increase output and/or reduce costs. To do this, you need to choose rational remuneration systems.

There are 3 main systems, divided into many types. For clarity, they are all presented in the table below.

1. Tariff system

How is the tariff system of remuneration implemented at the enterprise?

At state enterprises, wage scales and salaries of employees are established by higher authorities. Private organizations can independently determine the level of salary and bonus.

Scope of application

The tariff system of remuneration is used everywhere.

It can be found in private and public enterprises: hospitals, educational institutions, factories, shops, etc.

Individual entrepreneurs and various small organizations are not prohibited from using the tariff system.

What is a tariff-free wage system? Read our article. When is personal income tax paid on wages? Find out here.

Is it possible to send a part-time worker on a business trip? Information is here.

Based on what documents is it calculated?

Depending on the chosen form of remuneration, the amount of money is calculated on the basis of several documents:

- time sheet;

- staffing schedule;

- regulations on bonuses for employees;

- work order to implement the plan;

- piece rate.

As a rule, employers make do with the first two documents.

Tariff system of remuneration

Tariff SOT is the most common, used by both government agencies and commercial organizations. It is based on the ranking of employee salaries depending on their qualifications, work experience, acquired skills, output, conditions and nature of work. In government agencies, the Unified Tariff Schedule is used. In commercial ones - documents similar to it, approved taking into account the opinion of the trade union body.

Tariffing is regulated by law for many industries. For example, for employees in the education sector, an individual tariff SOT has been established in accordance with Government Decree No. 583 dated 05.08.2008.

There are two types of tariff systems: piecework and time-based.

Piece rate form of remuneration

With this form of payment to staff depends on the final result of work, taking into account the quality of services provided or finished products. Such a system gives a person an incentive to increase productivity and ensure good quality of his work.

The amount of earnings is determined at piece rates per unit of production or operation. The transaction is practiced by organizations that can clearly record the quality and volume of goods produced or actions performed.

An organization can make payments for work results individually or collectively, for example, for a team of employees. Depending on the method of calculating wages, the transaction is divided into several types:

- Direct - at fixed prices;

- Premium - bonuses are applied for processing and on other grounds;

- Progressive - prices increase when production exceeds the norm;

- Indirect - earnings directly depend on the result of labor;

- Accord - a deadline and payment are established for the entire volume of work.

Time-based form of remuneration

Time-based SOT is used at those enterprises where there is no need or opportunity to normalize production. Employees' job functions do not include the production of goods or services, so it is optimal to pay wages for time, and not for the amount of work. Almost all administrative and economic personnel “sit” on this COT. Payment will be made based on the employee’s qualifications and actual time worked in the accounting period.

Peculiarities of salary calculation for different types of time-based wages

With a simple time-based wage, the time worked in the period is paid. Periods can be recognized as: hours, days, months and variations of these periods.

With a bonus , a bonus for the quality of work is added to the salary for time, calculated as a percentage of the salary at the rate. The bonus may be one-time or applied on an ongoing basis.

With a salary , the employee has the right to count on a monthly salary in the amount as established in the employment contract. Upon achieving a certain qualification (determined subjectively by the employer), the salary may be increased.

Basic forms of remuneration

According to paragraph 4 of Art. 1 “Methodological recommendations for accounting of labor costs and their payment...” approved by the Ministry of Agriculture in 2008, the form of remuneration is a salary calculation mechanism that takes into account the amount of labor of employees.

Based on this definition, there are two key forms of remuneration: time-based and piece-rate. Time-based payment is made for the time actually worked by the employee, regardless of the results of work demonstrated by the employee. With the piecework form of remuneration, wages are calculated based on the volume of work performed, regardless of the time spent.

Also, these forms of remuneration are often called remuneration systems. But in some sources, the concepts of forms and remuneration systems are distinguished and the forms are understood only as those listed in Art. 131 of the Labor Code. It says here that wages can be in cash or in kind. Cash payments are made strictly in rubles, while wages in kind can only be paid with the consent of the employee and in an amount of no more than 20% of total earnings.

There is also another more detailed classification of current forms of remuneration. According to it, three large forms are distinguished:

- Tariff.

- Tariff-free.

- Mixed (floating salaries, dealer mechanisms, etc.).

Varieties of the tariff system of remuneration are time-based and piece-rate payment. Types of time-based payment can be considered simple time-based, time-based bonus and salary forms. Subtypes of piecework payment are: direct piecework, piecework-progressive, indirect piecework, piecework-bonus, individual and collective.

Tariff systems of remuneration are directly provided for by the Labor Code, but other forms are not. But this does not mean that the employer has the right to implement only one of the tariff forms.

Labor legislation grants him the right to independently choose the form of remuneration that does not contradict the provisions of the Labor Code.

Tariff system

The tariff system of remuneration today is the most common and is used by both budgetary and commercial organizations.

When using this form of payment, employee salaries are differentiated depending on qualifications, skills, length of service, nature of work and conditions. Tariff systems of remuneration are regulated by the provisions of Art. 143 of the Labor Code. This form includes categories such as tariff rates and salaries, tariff schedules and coefficients.

The tariff scale is understood as a set of tariff categories (professions and positions), which are determined depending on the complexity of the functions performed and the requirements for the level of qualifications of employees. In practice, the tariff schedule is usually drawn up in tabular form, where you can clearly see that the higher the rank of the employee, the higher the coefficient applied to him.

The tariff coefficient is determined by dividing the tariff rate of the assigned category by the rate of the first category . When assigning a tariff category, the complexity of the work and the level of qualifications of the employee are taken into account; when assigning a qualification category, professional training is taken into account.

When introducing a tariff form of payment, the employer must carry out a tariffication procedure, namely, assigning types of work to tariff categories or certain qualification categories depending on the complexity of labor tasks.

When charging, the assignment of categories is carried out taking into account the unified qualification directory of professions and works, the directory of positions of managers and specialists and approved professional standards.

These directories are approved taking into account Government Decree No. 787 of 2002 “On the procedure for approving ETKS...”.

If an organization has approved a tariff system, then government institutions use the Unified Tariff Schedule, and commercial institutions use similar documents approved within the organization, taking into account the opinion of the trade union organization.

For many industries, tariff rates are fixed by law: for example, for workers in the educational and medical industries.

There are two major types of tariff system : piecework and time-based. The tariff form of remuneration is introduced at the enterprise by the provisions of the collective agreement or other legal acts.

Time-based

The time-based form is used at enterprises where there is no need to standardize output or this is impossible. In this form, employees do not produce goods or provide services, so it is optimal for them to be paid for the time worked, and not for the amount of work performed. Typically, this form of payment applies to administrative and business personnel : accountants, secretaries, lawyers, marketers, etc. This form also often applies to part-time workers.

When calculating wages on a time-based basis, the time actually worked by the employee in the reporting period is taken into account. Such a period can be an hour, a day, a month, or any other option.

If the month is not fully worked, the employee’s salary is accrued only for the time actually worked.

Some organizations use a time-based bonus form, when a premium for quality work in the form of a certain percentage of the salary is added to the basic salary, calculated on a time-based basis. The award may be one-time or regular . The amount of the bonus may be specified in the Regulations on Bonuses, a collective agreement or contained in the Employer’s Order.

With a salary system, an employee has the right to count on receiving a fixed amount each month, which is specified in his employment contract. The salary is transferred to the employee if he works for the full period.

Piecework

The piecework system is usually applied to production units or workers involved in the service sector. The profit of such companies largely depends on the speed of work of the staff, so it is more profitable for them to pay not for the time worked, but for the amount of work performed.

For each volume of work completed or unit of output produced, the employee is paid a certain amount, which is called a piece rate. The more products (provides services) an employee produces, the higher his earnings. Therefore, piecework in practice is a good incentive for workers to increase productivity.

In practice, with piecework payment, quality control is important. This allows you to avoid spending extra money on paying for poorly performed work. For example, if an employee produced 250 parts, of which 50 are rejected by the quality department, then they will only pay him for 200.

In organizations based on piecework payment, it is necessary to carefully keep records of personnel performance indicators. These documents subsequently form the basis for payroll calculation.

With direct piecework, payment is made strictly for the number of units produced by a specific employee. In this case, the fee for each unit is the same.

With a progressive piece-rate form of payment, prices for each unit of production produced above the plan are higher. In the regressive form, if the employee does not achieve target indicators, payment is made in a smaller amount.

When applying a bonus form of payment under the direct system, a bonus for fulfilling the plan, absence of defects, savings on components and raw materials, etc. is added to the salary.

With indirect piecework, the work of support personnel is paid taking into account the performance of the production unit in the form of a certain percentage of the salary of the main employee (for example, the salary of the equipment adjustment service in the production workshop can be calculated in this way).

The lump sum salary is calculated and paid for the comprehensive implementation of the plan (for example, for the completion of work at a certain stage). There is a distinction between the individual piecework wage system and the collective system. In the latter case, the salary of a certain employee depends on the successful achievement of target indicators by the team.

Tariff-free

A tariff-free wage system is usually used in start-up companies. For example, here a general wage fund is established, and each employee is paid a certain percentage from the general fund. As a company becomes more profitable and develops, employees' earnings increase.

The procedure for determining earnings under a tariff-free system must be prescribed in a collective agreement or other local legal act.

For example, the wage fund is 100 thousand rubles. The company employs 5 people, each is entitled to 20% of the fund, i.e. 20 thousand rubles. But it is also possible to rank the amount of earnings depending on the employee’s contribution to the development of the company or the complexity of the functions he performs. A certain labor participation coefficient may be introduced for employees.

But in an employment contract it is not allowed to stipulate the salary in the form of a certain percentage . The salary for the month is indicated here - for example, 20 thousand rubles. monthly.

This form of remuneration is designed to increase staff interest in the results of the enterprise and increases the level of individual responsibility for the results achieved.

The use of a non-tariff form of payment is very limited, since it cannot be implemented in large companies due to the difficulty of accounting for the individual contribution of each employee to work results.

Piece wage system

Piece work is used by organizations that provide services, perform work, or produce goods. Their profit directly depends on the speed of their employees’ work, so it is profitable to pay not per unit of time, but per unit of output. The payment formula is as follows: as much as you did, you received as much. The quantity of the product is multiplied by the unit price (piece rate). Such SOT encourages employees to constantly improve their output and quality of work. The second indicator is no less important, because Salaries are calculated based on the results of the period strictly after analyzing the work. Those. if Petrov produces 200 parts, of which 100 are unusable, only 100 will be paid for.

The basis for calculating wages will be documents confirming that employees have fulfilled their personal production plan. In order to facilitate calculations and minimize errors, it is necessary to carefully consider the system for recording employee performance.

How labor is paid for different types of piecework wages

With direct payment, payment is made for the number of units of output at the same price for each.

With progressive - the piece rate increases for each unit above the plan.

With a bonus , a bonus is added to the salary calculated according to the direct piece-rate system for fulfilling the plan, compressing deadlines, absence of defects, economical material consumption, etc.

With indirect payment, the work of support staff is paid, the amount of payment is set as a percentage of the salary of the main employee.

With a lump sum salary, the salary is accrued for the comprehensive implementation of the plan in general; the unit of output in this case does not play a role. There are:

- individual piecework SOT - salary for achieving one’s own indicators;

- collective - the salary of one person depends on the successful achievement of goals by the entire team. This system develops team spirit in the team.

Tariff-free wage system

The tariff-free SOP is similar to the option system in startups. There is a payroll and employees. Let’s assume 100 thousand rubles and 10 people. The employer establishes that:

- The payroll can be increased if the company’s profits rise,

- The share of each employee’s salary is 10%.

The share can rank employees by the amount of participation in work or be the same for everyone.

In the employment contract, of course, they will write down 10 thousand rubles - salary per month. It is impossible to mention % according to the Labor Code, and it is not very profitable for the company.

After the announcement of working conditions, there is no need to establish additional incentives; employees themselves will strive to increase the company’s income. This model is applicable to small, start-up companies that will not go public, but want to interest employees without having money for bonuses.

Mixed remuneration system

A mixed SOT combines tariff and non-tariff SOT - the employee has a certain salary, but in this case it directly depends on the success of his work: on the number of sales, on the quality of developments, on time worked, etc.

The more output, the higher the salary. And vice versa. The difference from the tariff is that the entire salary is reduced down to the minimum wage.

How are salaries calculated for different types of mixed labor protection?

The floating salary system involves recalculating salaries on a monthly basis based on the results of work for the previous period.

In commission calculations, an employee can count on a percentage of the company’s profit in general, or from each unit of output. This COT is very often used in insurance companies.

Payment for labor in a dealer network is very close to payment under a civil contract, but it also occurs in labor law. An employee is obliged to sell a certain amount of company goods, which he purchases at his own expense. The difference between the purchase price and the selling price to third parties is the person’s wages.

The mixed wage system is interesting because it combines both the features of a tariff system and the features of a non-tariff wage system.

A system of this type can be used, for example, in a budget organization that has the right to carry out business activities in accordance with the constituent documents.

Mixed remuneration systems include:

b system of “floating” salaries,

b commission form of remuneration,

b dealer mechanism.

Mixed remuneration systems [p.221]

Mixed remuneration systems. In addition to tariff and non-tariff systems, mixed systems can be distinguished as new forms, and among them are, first of all, the commission form of remuneration and the so-called dealer mechanism. These systems are called mixed because they have characteristics of both tariff and non-tariff forms of remuneration. [p.285]

For each of the proposed situations, determine what the remuneration system for sales workers should be based on (fixed, piece-rate, mixed). [p.776]

The question of the composition of payment, in particular its division into fixed and variable parts, is even more complex. Salespeople strive to receive a fixed salary and at the same time expect that the high efficiency of their work will certainly be rewarded, and the salary itself will increase as they gain experience. On the other hand, the company tends to use a payment system that stimulates the behavior of the seller that is beneficial to it, and uses its own scheme that reflects the balance between various goals. There are three main remuneration systems for sales representatives: a fixed salary, commissions and a mixed payment system. Let's take a closer look at them. [p.376]

Remuneration for workers of mixed teams, in particular those involved in the operation of flexible automated production (GAP), depending on production conditions, can be made according to time-bonus (with the issuance of standardized tasks) or piece-rate and bonus systems of remuneration. [p.81]

There are three main types of remuneration for sales agents: a commission system, a salary system and a mixed payment system (salary and commissions). [p.123]

In the practical activities of organizations that use a non-tariff wage system, questions often arise, especially when applying the guarantee articles of the Labor Code of the Russian Federation (payment for labor in the manufacture of products that turned out to be defective through no fault of the employee, payment for downtime), since the amount of guarantee payments is linked to the rate ( salary). Because of this, mixed systems are used, combining elements of tariff and non-tariff remuneration systems. [p.221]

Such a systematic approach is required, for example, when covering the circulation of economic goods (question 2), features of the structure of production at the turn of the 20th - 21st centuries (question 6), the modern market system (question 22), forms of remuneration (question 35), types of banks ( question 42), a system of macroeconomic indicators (question 48), a mixed type of regulation of the national economy (question 61). [p.16]

When mechanizing labor and wage accounting, accounting codes or a system of accounting codes are developed in the form of symbols, for example, code for construction sites or points, code for categories of workers and their personnel numbers, code for types of wages, code for types of deductions, code for production costs, etc. . The codes used in mechanized accounting differ in the number of digits they contain and the method of numbering. Based on the number of digital symbols, codes are divided into single-digit and multi-digit. Based on numbering methods, there are four code systems: ordinal, serial, decimal and combined (or mixed). [p.80]

The tariff-free system is a distribution option for remuneration. In this case, the employee’s individual salary represents his share in the wage fund earned by the entire team. As a rule, this share is determined on the basis of a constant coefficient assigned to the employee, which determines the level of his labor participation. In the practical activities of organizations that apply a non-tariff wage system, questions often arise, especially when applying the guarantee clauses of the Labor Code (payment for labor in the manufacture of products that turned out to be defective through no fault of the employee, payment for downtime), since the amount of guarantee payments is linked to the rate (salary) ..Because of this, mixed systems are used, combining elements of tariff and non-tariff remuneration systems. [p.130]

The failures of the mixed economy were also based on technical reasons. Attempts to harmonize the consultation process by introducing objective criteria, such as average productivity gains, have not always been successful. The fact is that the latter was difficult to “calculate”. Here the psychological effect came into play, resulting from the presence of a higher than average level of wages in fast-growing sectors of the economy, characterized by rapid technological progress and high productivity, which played the role of the vanguard31. Be that as it may, since the late 70s, governments of various countries, in order to reduce inflation, have sought to slow down wage growth in those sectors where labor productivity grew too slowly. The same reason has prompted governments to cut public spending since the mid-70s. Most were convinced that the social safety net had grown too quickly in previous decades. Economic stagnation should be expressed in a reduction in government spending, which could not be compensated by increasing direct taxes. A heavier tax burden would have a negative impact on savings and investment when they should have been encouraged to lift the economy out of its lethargy. [p.215]

Floating salary system

The use of a “floating” salary system is based on the monthly determination of the employee’s salary depending on the results of work in the serviced area (increase or decrease in labor productivity, increase or decrease in the quality of products (works, services), compliance or non-compliance with labor standards, etc.).

Such a system can be used to pay administrative and managerial personnel and specialists.

Accordingly, the size of the salary depends on the quality of the employee’s performance of his job duties.

Commission form of remuneration

The use of a commission form of remuneration is now quite common.

This system pays for the work of many sales department specialists.

An employee’s salary for performing his job duties is determined in this case as a fixed percentage of income from the sale of goods, products, works and services.

At the same time, the choice of a specific mechanism for calculating wages, when using a commission form of remuneration, is regulated exclusively by the company’s internal regulations and depends on the specifics of the organization’s activities.

The concept and types of mixed forms of remuneration

With a mixed form of remuneration, it is possible to combine non-tariff and tariff systems, which makes it possible to interest the employee in increasing the productivity of his work for the benefit of the entire enterprise. In particular, a whole system of additional payments is established in the form of a percentage of revenue, an efficiency coefficient depending on the growth of labor productivity or the quality of products, etc.

There are 3 types of mixed remuneration :

- With floating salaries.

- Commission.

- According to the dealer system.

Floating salaries

When using such a system, the employer, by adjusting the tariff rate, monthly sets a new salary for each employee, taking into account his work results. Results are assessed based on indicators of labor productivity, quality of products (increase or decrease), etc., subject to the fulfillment of the planned target.

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

The use of a system with a floating salary with mixed remuneration is justified for evaluating in monetary terms the work of highly specialized specialists and administrative and managerial personnel (for example, heads of structural divisions) based on the results of the work of the areas entrusted to them.

Commission system

By establishing a commission system of remuneration, the employer encourages the employee to work more actively (produce/sell more goods, etc.), since his income in this case is directly related to the amount of products produced/sold. With this form of payment, employees’ employment contracts indicate a fixed percentage of production/sales volume, which they receive in monetary terms based on the results of their work for the month.

In some cases, it is possible to use the scheme “a small fixed salary plus interest (commissions) on the results of the enterprise’s work.” It is also possible to set a differentiated commission amount, depending on what goods were sold (with a larger or smaller markup, which brought a certain economic effect for the company). The choice of a specific calculation mechanism is determined by the relevant local regulations adopted by the enterprise.

Dealer systems

When choosing a dealer mechanism of mixed remuneration, the employee himself regulates his earnings, ensuring the volume of sales. By investing his own money in a product purchased from an enterprise, he is directly interested in selling it as quickly as possible for a higher price. After all, his earnings in this case are the margin between the purchase and sale prices.

Dealer mechanism

Finally, let's talk about the dealer mechanism.

This remuneration system is based on the fact that a company employee purchases company goods at his own expense in order to sell them independently.

Accordingly, the employee’s earnings in this case are the difference between the price at which the employee purchased the goods and the price at which he sold them to customers.

Articles on the topic

Companies often have to change their remuneration system in accordance with their goals and objectives. Find out what types of remuneration exist, which ones are most profitable and effective to use, and how to implement them.

The remuneration system (WRS) is a method of calculating remuneration to an employee, which is paid for his work. Such a system is installed depending on the type of business activity, as well as the position held by the employee.

In Russia, according to the Labor Code, there are three main remuneration systems, broken down into subtypes (see diagram below).

Let us examine in detail the features of each system.

Tariff system of remuneration

Tariff SOT is the most popular. It is used by both budgetary organizations and commercial ones. This system is based on ranking employee salaries depending on:

- qualifications;

- length of service;

- skills;

- workings;

- conditions and nature of work.

Tariff SOT has two types:

Piece wage system

With piecework wages, earnings depend on the number of units produced, taking into account their quality, complexity and manufacturing conditions. Such SOT is more often used in production for blue-collar occupations, if the primary goal is output volume indicators.

If you need to solve a quality problem, then premium COT is already used. Then the form of remuneration will be piecework-bonus. The conditions for paying the bonus will be the quality of the products and production standards. Under these conditions, it is also necessary to introduce production standardization indicators, according to which payment is made at piece rates.

Since under the piecework system, earnings depend on the quantity of products actually manufactured and time costs, when deciding whether to introduce them into the company, it is necessary to assess whether it is possible to:

- establish quantitative indicators of output (work performed) and their accounting;

- ensure proper regulation of work;

- increase product output without changing the technological process;

- control product quality.

Depending on the method of organizing work, the piecework system can be individual or collective.

Individual piecework payment is possible in jobs where the work of each employee is subject to accurate accounting. The remuneration depends on the quantity of suitable products produced by the employee and the piece rate per unit of product. If a worker performs several different types of work (operations), each type of work is paid according to the rates established for them.

In collective work, the remuneration of each worker depends on the results of the work of the entire team (team, section). At the same time, the distribution of collective earnings between individual workers should not be equal; it is necessary to take into account the personal contribution of each person to the overall results of the team’s work. This is most often done using the labor participation rate.

Piecework payment has several varieties, which differ from each other in the way they calculate earnings. In addition to direct piecework payment, there are:

- indirect - applied to auxiliary workers, the amount of wages depends on the results of the work of the main workers they serve;

- piecework-progressive - wages for production within the established norm are charged at standard rates for products produced within the norm, and for production in excess of the initial norm - at progressively increasing rates;

- chord - for an individual performer or group, the amount of remuneration is established not for one production operation, but for a set of works).

Time-based wage system

With a time-based wage system, its size depends on the amount of time spent (actually worked), taking into account the qualifications of the employee and working conditions.

Time pay depends on the time worked, that is, the amount is determined by the amount of working time the employee has during the stated period.

The same SOT includes time-based bonus and salary systems. These are the simplest forms. For managers, engineering and technical workers and employees and some categories of workers, time-based wages are established in the form of official salaries.

It should be noted that some manufacturing enterprises transfer working categories of personnel to salaried SOT in the event that the task - product quality - becomes a higher priority than output volume.

What is this form - features

A mixed form is a special type of payroll calculation, which implies some important nuances and rules. Here it is permissible to combine tariff and non-tariff systems. This makes it possible to stimulate the employee to work intensively, which will benefit the enterprise.

In this case, you can install a whole system of pleasant rewards. These may be interest rates, rewards for product quality, additional payments for exceeding established work standards, and so on.

Read about existing forms of remuneration here.

Mixed remuneration system

Mixed COT combines tariff and non-tariff systems. To put it briefly and clearly, this is a remuneration system in which an employee has a certain salary, which depends on the success of his work. For example, on the number of sales, hours worked, etc.

Mixed COT has three types:

SOT of “floating” salaries. It involves recalculating the salary on a monthly basis and depends on the results of work for the previous period.

Commission. In this case, the employee can count on a percentage of the company’s profits as a whole or from each unit of output. This COT is often used by insurance companies.

Dealer network. With this SOT, the employee must sell a certain amount of goods or services, which he purchases from the company at his own expense. Accordingly, the difference between the purchase and sale prices will be the wage.

How to choose and implement a remuneration system

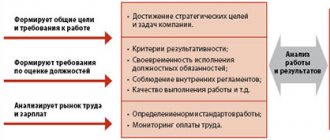

There are situations when the company's existing COT system stops working. For example, the employee’s income level has not changed for a long time and has become lower than what is offered on the market. This provoked a decrease in efficiency, loyalty and the emergence of reasons to quit. To understand what is wrong with the existing system, it must be analyzed. The algorithm is as follows:

1. We analyze the staffing table, comparing it with the data of independent experts on the specialist’s income level. We find out whether salaries correspond to market trends (higher, lower, market average - we take data from analytical reviews of recruiting agencies, look in the personnel journal, in advertisements on employment sites), and how wages are set for an employee (for example, for more qualified workers are provided with an allowance or bonus).

2. We find out the attitude of the staff towards the existing HSE. You can ask indirect questions about how much an employee needs to earn so that he has enough to live on, what scheme will be fair. You can interview those leaving about the reasons for leaving. We discuss with managers what best motivates employees.

3. We compare the information received with the data from the analysis of the staffing table. We draw a conclusion about the disadvantages and advantages of SOT.

4. We are developing a concept for changes to the COT. That is, we record the problems that have been identified, show how the problem affects the performance of personnel (how much the planned indicators have decreased) and how it affects the performance of the company. We propose a solution - a new SOT (for example, increase the salary, introduce bonuses based on performance). We will clarify how this will affect the wage fund and what changes to make to the Regulations on remuneration.

5. We prepare analytical data in the form of documents (concept and position). We create slides for the presentation containing the provisions of the projects. We prepare arguments to convince the company’s owners and the general director of the need to change the COT, and determine how much time it will take (usually three to six months).

Let us note that the SOT must be reviewed when new technologies are introduced and the labor function of workers changes; employees do not understand how wages are calculated; there is an outflow of personnel due to low salaries; it is necessary to reduce personnel costs.