How is income tax collected on sick leave?

A certificate of temporary incapacity for work is a document regulating the relationship between an employer and an employee in the absence of the latter at work. It is issued in the event of illness, injury, or pregnancy.

Based on sick leave, benefits are calculated and transferred by the Social Insurance Fund. The document also certifies that the employee was absent for a valid reason.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem , contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FREE !

While the employee is on sick leave, certain payments are accrued. They are produced by the employer and the Social Insurance Fund. Amounts transferred to a person are considered his income. Therefore, income tax is charged on sick leave.

In addition to personal income tax, no other contributions to various funds are withheld. It is important to know how the tax calculation procedure works in 2020.

What taxes must be paid on sick leave payments?

To answer the question of what taxes are imposed on sick leave, you need to know what form of taxation the company is on. As a rule, everyone pays:

- income tax;

- pension contributions;

- payments to the Social Insurance Fund;

- social Security contributions.

The taxation of sick leave is carried out in exactly the same way and in the same manner as the taxation of wages.

Back to contents

Is it taken at all?

Employees often do not know whether income tax is charged on sick leave. In accordance with Russian legislation, compensation payments upon the occurrence of temporary disability are considered the citizen’s income. Therefore, like any other income, taxation is applied to it.

Sick leave certificates are issued on the basis of the social insurance law, which was issued by the Ministry of Health. It reflects the order in which they are provided and the possibility of increasing the duration.

Expert opinion

Polyakov Pyotr Borisovich

Lawyer with 6 years of experience. Specialization: civil law. More than 3 years of experience in drafting contracts.

Clarifying norms are prescribed in the Tax Code of the Russian Federation. According to its articles, taxation is applied to such income. There are no exceptions to sheets issued when a child becomes ill.

The list of income on which tax is not levied includes maternity benefits. Therefore, expectant mothers receive payment in full.

When will personal income tax be withheld and when not?

Example:

Masha and Dasha are friends, they work in the same positions, and they have the same salary. One day Masha went on maternity leave, and Dasha broke her leg and spent two months on sick leave. But the amount of temporary disability benefits paid to Masha turned out to be more. Dasha’s payslip indicates that personal income tax is withheld from the benefit amount, but her friend does not have such a deduction on her payslip. The girls are perplexed: is income tax taken from sick leave or not?

If temporary disability benefits are accrued due to an employee’s illness or injury, then personal income tax will be withheld from him. The same applies to the situation when sick leave is issued to care for a child or other family member. But the amount of maternity benefits is not taxed, so the woman will receive all the money in full.

Main formalities

The income that an employee receives from sick leave is taxed. Legislative acts prescribe the procedure for calculating, paying and reflecting the amount in the document.

References to the law

Confirmation of the occurrence of an employee’s incapacity for work is possible only on the basis of an extract. This norm is reflected in Order of the Ministry of Health No. 1345, issued on December 21, 2012.

Income tax is withheld in accordance with Article 217 of the Tax Code of the Russian Federation. It reflects the procedure for accruing and collecting funds from the income received by the employee, and also highlights cases when taxation is not applied.

Benefits for temporary disability of a person are counted as income. Therefore, it is necessarily taxed. Based on paragraph 1 of Article 217 of the Tax Code of the Russian Federation, collection is made even when issuing sick leave to care for a child during his illness.

The same article states that sick leave related to pregnancy and childbirth is calculated in a different way. Personal income tax does not apply to them.

The order of reflection in the document

The procedure for not only withholding and deducting tax from sick leave, but also for reflecting transactions in the documentation is established by law. The employer reports to employees using a certificate in form 2-NDFL. It is necessary when contacting the tax service to receive a deduction.

Using this document you can also reflect:

- payment of benefits;

- payment of tax;

- impossibility of withholding funds.

The certificate will have signs 1 and 2. In this case, the disability benefit is prescribed in the form of code 2300.

The calculation of tax fees that have been accrued and withheld is reflected in Form 6-NDFL. The document was introduced in January 2020. Information is provided every quarter.

When creating a 6-NFDL certificate, information is indicated not on individual sick leave, but on generalized information.

The document notes:

| All funds accrued to employees of the institution as income | 020 |

| Dividends paid | 025 |

| Tax deductions | 030 |

| Accrued NFDL | 040 |

Direct calculation is carried out in lines from 060 to 090. If tax is regularly withheld and there is no refund, you must enter a zero value.

Information about the retention and transfer periods is written in the second section of the reporting, lines 110 and 120. You can compare the created document with the sample that was developed by the Federal Tax Service.

If filled out incorrectly, the tax agent will have to pay a fine for each inaccuracy in the amount of 500 rubles. The same amount will need to be paid if the data is incorrectly indicated in 2-NDFL. Even after paying the fine, new paperwork will be required.

This is important to know: In what cases is sick leave paid 100 percent?

Payment Features

Expert opinion

Polyakov Pyotr Borisovich

Lawyer with 6 years of experience. Specialization: civil law. More than 3 years of experience in drafting contracts.

Benefits paid to an employee for a period of temporary disability are not included in the list of non-taxable benefits. This is stated in Article 217 of the Tax Code of the Russian Federation.

During sick leave, the employee will receive an amount less than 13% of the original amount.

The employer will need to transfer funds to the state treasury within a certain period:

| During the transfer to the employee's account | On the same date. |

| When issuing cash through a cash register | On the date the funds are debited from the account. |

| In the case of issuing cash that is working capital | No later than the next settlement date. |

What is the procedure for reflecting personal income tax from sick leave in accounting

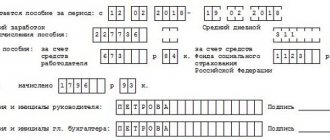

From an income tax perspective, the payment of benefits by the employer is classified as other production-related expenses. An example of income tax reflection in this case is presented in the table.

| Contents of operations | Debit | Credit | Amount, rub. | Primary document |

| Temporary disability benefits accrued at the expense of the organization (364.38 x 3) | 20 | 70 | 1093,14 | Certificate of incapacity for work, Payroll |

| Temporary disability benefits were accrued at the expense of the Federal Social Insurance Fund of the Russian Federation (2186.28 - 1093.14) | 69-1 | 70 | 1093,14 | Certificate of incapacity for work, Payroll |

| Personal income tax withheld (2186.28 x 13%) | 70 | 68 | 284,21 | Tax card |

| Temporary disability benefits paid minus withholding tax (2186,28 – 284,21) | 70 | 50 | 1902,07 | Payroll |

Noteworthy moments during pregnancy and childbirth

Taxation may not apply on some income. Such payments include benefits that are issued when pregnancy and childbirth occur.

After 30 weeks of bearing a child, a woman must submit a certificate of temporary incapacity for work to her place of work. If the package of documents is complete and executed correctly, calculation and payment are made within 10 days from the date of contacting the accounting department. Funds are transferred in full without withholding personal income tax.

Onset of disability

Loss of ability to work is recorded at an appointment with a doctor - if there are signs of the disease.

There are several reasons for issuing sick leave:

- disease;

- pregnancy and childbirth;

- staying in quarantine;

- getting injured;

- the need for follow-up treatment in inpatient or sanatorium conditions;

- caring for a child or other sick family member.

The fact of incapacity for work is reflected in the sick leave certificate. It does not indicate the diagnosis, since it constitutes a medical secret; only the corresponding code is entered.

Additionally, the document indicates the duration of sick leave, on the basis of which compensation is calculated.

Payment Features

Payment for sick leave is carried out on the basis of a sick leave certificate. The first three days of forced leave are compensated by the employer, the remaining days - by the Social Insurance Fund.

The law provides for cases when the entire sick leave is paid from the Social Insurance Fund, for example, pregnancy and childbirth.

To receive payment, a sheet of temporary loss of ability to work and all necessary certificates are submitted to the employer and the Social Insurance Fund along with the application.

The documentation is reviewed within 10 days, after which funds are accrued along with the advance payment or wages. Tax is withheld from them in advance.

Is it subject to personal income tax?

Is income tax collected on sick leave? Yes, in 2020 its rate is 13%. It is charged when calculating compensation to the employee.

It is important that the employee can receive payment within six months from the end of sick leave, since the validity period of the temporary disability certificate is 6 months.

Fixed deadlines

Until 2020, the deadline for paying personal income tax was set immediately after the date of transfer of benefits. It was difficult for large organizations to comply with the requirements of this standard. After all, their numerous employees could go on sick leave every day. Therefore, tax collections had to be transferred daily.

The Ministry of Finance of the Russian Federation took into account the dissatisfaction of institutions. Therefore, a new rule has been introduced by law regarding the timing of personal income tax transfers. The transfer of amounts to the budget must be made no later than the last day of the month in which the benefit was paid. This does not take into account the nature of the payment made: in cash or to an account.

Tax withholding, in accordance with Article 226 of the Tax Code of the Russian Federation, is made on the same date when the benefit is paid. It coincides with the issuance of wages in the organization.

It is necessary to transfer funds to the budget:

- on the date of receipt of the amount when withdrawing it from the bank account;

- on the day of transfer to the employee, if sent to the account;

- no later than the next day upon payment of funds from the cash register.

This payment procedure is established by paragraph 6 of Article 226 of the Tax Code of the Russian Federation. Income tax on the temporary disability certificate is removed without fail. After all, by law, benefits are considered a citizen’s income. The retention and transfer of funds to the state treasury is carried out by the employer.

What are the current personal income tax rates for tax residents? Find out by clicking on the link.

The personal income tax code for financial assistance can be found here.

- Due to frequent changes in legislation, information sometimes becomes outdated faster than we can update it on the website.

- All cases are very individual and depend on many factors. Basic information does not guarantee a solution to your specific problems.

That's why FREE expert consultants work for you around the clock!

- via the form (below), or via online chat

- Call the hotline:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

Personal income tax on sick leave - is it taxable, payment deadline and procedure

Hello! Today we’ll talk about personal income tax on sick leave and figure out whether the tax is withheld or not. You will learn about cases of accrual of personal income tax on sick leave, the timing of the transfer of personal income tax, the procedure for calculating sick leave and what the Social Insurance Fund pilot project is.

Is personal income tax withheld from sick leave?

A sick leave certificate, or temporary disability certificate , is an official document issued to an employee by medical institutions and indicates the impossibility of the employee’s continued participation in the labor process. By its name and essence, this benefit is nothing more than compensation in connection with the suspension of official duties.

On the other hand, such a payment is in many ways equivalent to wages, since its recipient is forced to pay income tax on it - personal income tax. If the employee is officially registered in the organization, then the function of correctly calculating and paying income tax on sick leave is performed by the employer, being the employee’s tax agent.

As a general rule, income tax is paid on sick leave, and these are the following cases:

- The employee is on sick leave due to illness or injury;

- The employee did not come to work because he was caring for a sick child;

- During the imposed quarantine.

Cases when personal income tax is not paid on sick leave:

- Pregnancy and childbirth;

- Adoption of a child.

Any additional payments by the employer to sick leave for pregnancy and childbirth are subject to personal income tax.

Deadline for payment of personal income tax on sick leave

Until the beginning of 2016, representatives of the tax authorities officially obliged the employer to pay personal income tax on sick leave immediately after the payment of benefits. In large organizations, strict adherence to this rule would lead to the fact that every day some amounts would have to be transferred to the budget, taking into account the number of employees and their sick leave. In reality, they didn’t do this, otherwise they would have had to maintain a whole staff of accountants.

This forced failure to comply with this requirement led to friction between the accounting department and tax authorities. Fortunately, the Ministry of Finance has now changed this old rule due to its unviability.

Now the general rule regarding the deadline for paying personal income tax on sick leave is:

The employer, on behalf of his employee, must transfer the amount of personal income tax to the budget no later than the last day of the month in which the employee received the benefit.

It does not matter how the payment was made to the employee: in cash or by bank transfer.

Procedure for calculating sick leave

How much should an employee be paid for sick leave, and how much should be given to the state?

Calculation procedure:

- View the number of days of official sick leave - this figure is indicated on the sick leave certificate. For this number of days we will accrue benefits to the employee.

- Calculate average daily earnings . To calculate it, monthly earnings for the last two years are summed up and the total amount is divided by 730 - the number of days in twenty-four months.

- Find out insurance record . The size of the payment directly depends on it. If a person has worked in all his official jobs for a total of five years, then this number of years will be taken into account.

- Calculate what average daily earnings will be taken into account when calculating sick leave. The calculation is carried out as follows: it is calculated how many years of experience a person has, and a fixed percentage is taken according to the length of service.

- Calculate the total amount that will be paid to the employee. To do this, you need to multiply the number of sick days by the average earnings and subtract thirteen percent - the amount of personal income tax that will be transferred to the budget.

The organization pays only for three days of sick leave; the rest of the employee’s recovery payment is deducted from the Social Insurance Fund (SIF).

Let's give an example . Let’s assume that an employee was sick for six days and has seven years of insurance coverage. His total salary for the last two years is 800,000 rubles.

According to calculations, the average daily salary will be 1096 rubles (800,000/730). But taking into account the insurance period, we will take only 877 rubles (1096*80%). The amount for six days without tax is 5262 rubles (877*6). Excluding personal income tax – 4578 rubles (5262-13%).

Moreover, the employer will only pay 2,631 rubles – the employee’s sick leave for three days. The remaining amount is paid by the Social Insurance Fund.

The employer accrues and transfers to the budget only the amount of personal income tax that is calculated from his own payments to the employee. That is, only for a three-day allowance. The FSS must deal with personal income tax for the remaining days of sick leave.

FSS pilot project in 2020

Pilot projects in the regions of the Russian Federation are aimed at simplifying the work of accountants, and therefore the organization as a whole. These projects make it possible to transfer benefits to employees directly from the Social Insurance Fund. We are, of course, talking only about that part of the benefit for which the Social Insurance Fund is responsible. The fund also deals with the issue of how to calculate and transfer personal income tax on these benefits independently. The employer only needs to provide the Social Insurance Fund with the necessary information about the employee.

In 2020, the pilot project covered 33 regions. At the end of 2018, it already included 39 constituent entities of the Russian Federation. It is planned that 20 more regions will join it in 2019, and 18 in 2020. Thus, by the end of 2020, 77 regions will be able to become participants in “direct payments”.

Source: https://kakzarabativat.ru/buxgalteriya-i-nalogi/ndfl-s-bolnichnogo-lista/

What taxes are withheld from sick leave?

In the case when sick leave is issued to a worker who was undergoing treatment for an illness, injury or who was caring for a sick family member, personal income tax is withheld from the sick leave (Article 226, clause 1.4 of the Tax Code of the Russian Federation). As for contributions to the Pension Fund and the Social Insurance Fund, sick leave is not subject to insurance contributions . There is legal evidence for this.

- From the information contained in Art. 7 of Law N FZ-212, it follows that contributions to a state institution engaged in life and health insurance of citizens are paid only from the income of an employee bound by an employment contract with the employer for the provision of services or performance of work.

- Also according to part 1 of Art. 9 clause 1 of Law N FZ-212, insurance payments are not deducted from state benefits and other types of compulsory insurance coverage.

- Based on the information presented in Art. 8 clause 2 of Law N FZ-165 of July 16, 1999, payment for temporary disability is one of the types of compulsory insurance coverage.

In what cases is tax not charged?

Is sick leave subject to income tax?

As stated above, sick leave is not subject to contributions from the Social Insurance Fund and the Pension Fund of the Russian Federation in any case.

As for personal income tax, there are some types of income, according to a certificate of incapacity for work, from which it is not deducted.

These types are defined in Art. 217 clause 1 of the Tax Code of the Russian Federation. Sick leave contributions are not paid from:

- Benefit provided to unemployed citizens.

- Cash compensation paid to pregnant women.

- Payments for childbirth.

Is there any logic

In fact, in accordance with the Tax Code of the Russian Federation, almost all state benefits and compensation paid to citizens are not subject to taxation.

For example, tax is not withheld from unemployment benefits and child care benefits, from pensions and health compensation payments. And withholding personal income tax from sick leave is, in essence, an exception to the general rule. This is probably why people often believe that the accountant made a mistake and withheld the tax incorrectly. However, there is no point in looking for logic in the law; you just have to implement it. comments powered by HyperComments

What contributions are charged by the employer?

To answer this question, we should start by explaining who pays this benefit. According to Art. 12 p. 2 p. 6 of Law N FZ-165, the employer is obliged to pay benefits for sick leave in cases established by the legislation of the Russian Federation. Using our own funds for this, among other things.

At the same time, Art. Part 3, clause 2, clause 1 of the law establishes the following form of benefit payments. The first 3 days of an employee’s sick leave are paid by the employer ; starting from the fourth, funds come from the budget of the Social Insurance Fund of the Russian Federation.

You may also be interested in the following articles on sick leave:

According to the legislative norms described in the first and third sections of this article, personal income tax is withheld from sick leave. Contributions to the Pension Fund and other insurance deductions are prohibited by law.

Is income tax due on the first three days of incapacity?

The legislation states that the first three days of sick leave, which are paid to the employee by the owner of the company, are not subject to contributions from the Pension Fund of the Russian Federation and the Social Insurance Fund.

Since the amount of benefits under a certificate of incapacity for work consists of payments for all compulsory types of insurance.

This is important to know: Is it possible to take sick leave after dismissal?

This is written in part 1 of Art. 9 clause 1 of law N FZ-212.

Based on the information provided above, we can say that the only deduction from this amount is personal income tax.

But it is also charged only for those categories of temporary disability that are described in Art. 217 Tax Code of the Russian Federation.

Personal income tax accounting

Having figured out whether sick leave is subject to tax, let’s move on to accounting for personal income tax. In order to carry out accounting, you must first calculate the amount of tax. If there are no additional nuances, this is done as follows.

- The first thing to do is add up the amount of income for the 2 previous years and divide the result by 730. Income for the current year is not included in the calculations. There is also no tax deduction from this amount.

- Thanks to the calculations carried out, we obtain the average daily income.

- Now you need to multiply this value by the number of days spent on sick leave.

- The resulting amount is income from the certificate of incapacity for work . However, it will be possible to receive the full amount only if the insurance period is equal to or exceeds 8 years. From 5 to 8 years, the employee will be paid 80 percent of the amount. In cases where the length of service is equal to or less than five years, the payment will be only 60 percent.

The scheme will be different for those employees who have not worked in the previous 2 years or were unable to provide an income certificate . In this case, the calculation will be made as follows.

- You need to take the amount specified in the government decree as the minimum wage (minimum wage) and multiply it by the number of days during which the employee was absent.

- The resulting total must be divided by the number of days of the month in which the employee was treated.

- The resulting amount is considered the average daily income.

- The following calculation stages are identical to those above, starting from point 3.

- The amount is paid in full.

After the employee has provided sick leave, he must be granted benefits within 10 days. The employer is obliged to pay it along with the salary that will be paid next after the sick leave. This fact is enshrined in law in Art. 15 Part 1 and Art. 8 h. 13 edition of the decree of July 24, 2009 N 213-FZ.

How to reflect income on the 2-NDFL certificate?

In order to correctly issue a personal income tax certificate for sick leave, in which it is necessary to reflect the tax deduction from income for disability, you should refer to the recommendations of the Federal Tax Service of the Russian Federation.

They are described in letter number ED-4-3/74.

According to Art. 223 of the Tax Code of the Russian Federation, personal income tax certificate 2 for sick leave reflects all income received by the employee for the specified period.

The third section of the certificate is completed as follows. In the “month” field the serial number of the calendar period for which funds are accrued and actually received is entered.

The amount of wages is indicated for the current month, and the income on the certificate of incapacity for work for the previous month, when the employee took sick leave . Each of these amounts will be indicated under different codes. The salary is coded 2000, and the amount for sick leave is coded 2300.

After reading the article, it becomes clear whether personal income tax is charged on sick leave, which is enshrined in law regarding payments based on certificates of incapacity for work. What amount can an employee expect and how to calculate it. How to correctly reflect income on sick leave in certificate 2 - personal income tax or find it in this document.