The estimate for entertainment expenses - the sample for its preparation is not approved by law - will be a significant element of document flow in companies that hold official events. What is the purpose of this document and where can I download a sample?

Why do you need an estimate of entertainment expenses?

What is an estimate for entertainment expenses?

Drawing up an estimate: approval of the document and reflection of information about it

Budgeting: number of participants

Budgeting: reflecting expenses

Drawing up an estimate: we certify the document

Estimate as part of the provision for entertainment expenses: nuances

Results

Why do you need an estimate of entertainment expenses?

Representative expenses include expenses of the company that are associated (clause 2 of Article 264 of the Tax Code of the Russian Federation):

- with the organization of official business events;

- with transport and catering services ordered as part of the relevant events;

- with payment for the services of a translator, if his assistance was sought as part of official events.

In an amount that does not exceed 4% of labor costs in the same reporting period (their list is given in Article 255 of the Tax Code of the Russian Federation), entertainment expenses can be used to reduce the tax base of the enterprise.

Like any other expenses, hospitality must be confirmed. At the same time, previously the Ministry of Finance of the Russian Federation (in letter dated November 13, 2007 No. 03-03-06/1/807) advised confirming the relevant expenses by means of:

- issuing an order from the director on holding an official event within the framework of which expenses were incurred;

- drawing up estimates of entertainment expenses;

- drawing up a report on entertainment expenses;

- supplementing the indicated sources with primary documents.

However, there is a newer legal act from the Ministry of Finance - letter dated April 10, 2014 No. 03-03-RZ/16288. In it, among the recommended documents that can be used to confirm hospitality expenses, there is only a report, as well as a primary source supplementing it.

Nevertheless, many companies prefer, when preparing a set of documents to confirm entertainment expenses, to focus on the earlier list recommended by the Ministry of Finance. This is often due not only to the desire to protect oneself from possible claims from controllers, but also to internal corporate financial reporting standards that allow effective control over entertainment expenses in one’s organization.

In many cases, one of the key documents confirming entertainment expenses is the estimate - as a source that allows you to consistently detail costs.

Let's study what this estimate could be.

Tax accounting: standard for profit and VAT

Tax accounting of entertainment expenses consists of three stages.

STEP 1. We calculate the entertainment expenses of the current month (quarter).

STEP 2. We find out what part of entertainment expenses can be taken into account in the current period based on the standard - 4% of accrued labor costs (listed in Article 255 of the Tax Code of the Russian Federation) for the current reporting/tax period. 2 tbsp. 264, paragraph 4 of Art. 272 of the Tax Code of the Russian Federation.

Please note that both the amount of entertainment expenses and the amount of labor costs during standardization must be determined on an accrual basis from the beginning of the year. 7 tbsp. 274, art. 315 Tax Code of the Russian Federation. And if some part of the entertainment expenses is not taken into account in one quarter, with a high degree of probability it can be (at least partially) taken into account in the next quarter of the same calendar year.

We invite you to read the Application to bailiffs for recovery under a writ of execution

STAGE 3. We accept for deduction VAT on entertainment expenses taken into account within the standard as expenses of the current period.

If the sellers presented input VAT for all entertainment expenses, then the formula for calculating the part of the tax that can be presented for deduction is as follows (note that all amounts are taken on an accrual basis from the beginning of the year).

But this happens quite rarely. And if for some costs the sellers presented input VAT, but for others there was no input tax, then it is more profitable to take a different route. Proceed from the fact that when calculating income tax within the limits of the standard, you take into account, first of all, those expenses that are accompanied by input VAT.

If the amount of entertainment expenses within the standard is greater than the amount of expenses for which the seller has submitted input VAT, then the entire input VAT on entertainment expenses can be deducted.

Otherwise, a calculation will be required to determine the amount claimed for deduction. Let's give an example that is suitable in most cases. Again, all amounts in it are considered a cumulative total from the beginning of the year.

Since entertainment expenses must be normalized on an accrual basis from the beginning of the year, it may turn out that you can deduct VAT on such expenses partially in one quarter, and partially in another (when the expenses cease to be excess for profit tax purposes). In particular, due to the fact that during the year the wage fund increases and it becomes possible to take into account the additional amount of standardized costs in “profitable” expenses. Letter of the Ministry of Finance dated November 6, 2009 No. 03-07-11/285.

If, at the end of the year, part of the input VAT on entertainment expenses that do not fit into the “profitable” standard remains unclaimed for deduction, then such an amount of VAT cannot be taken into account in tax accounting as an independent expense. 1 tbsp. 170, art. 270 Tax Code of the Russian Federation.

To standardize entertainment expenses and calculate deductible VAT, it is better to create a tax register-calculation. For example, he might be like this.

LLC "Krasnaya Smorodinka" form approved. By Order No. 25 dated December 20, 2013

Register-calculation of entertainment expenses for 20-14 The form of the proposed register provides for the rationing of entertainment expenses throughout the year. However, it must be filled out at the end of each quarter for those income tax payers whose reporting periods are quarterly, half-year and 9 months. If the reporting periods are a month, 2 months, and so on, the column in the accounting register should be larger (the amount of standardized entertainment expenses should be calculated at the end of each reporting period and at the end of the year) art. 285 Tax Code of the Russian Federation

Person responsible for compiling the register

| Accountant | I.V. Reasonable |

Date of compilation: 09/30/2014

For the amounts reflected in line 9a of the above accounting register, you can register invoices for entertainment expenses in the purchase book of the last quarter.

Entertainment expenses can be taken into account for tax purposes.

Thus, for income tax they are taken within the standard - 4% of labor costs. The standard is considered a cumulative total from the beginning of the year. Therefore, expenses that did not meet the standard in the current quarter can be taken into account in the next quarter.

VAT is deductible only on those entertainment expenses that are taken into account for income tax. If the accounted amount of expenses increases in the next quarter, VAT can be deducted (clause 7 of Article 171 of the Tax Code of the Russian Federation).

What is an estimate for entertainment expenses?

The legislator did not approve or recommend the forms of the corresponding estimate. Therefore, the company must develop this document independently.

It is common to prepare an estimate for entertainment expenses in a structure that involves inclusion in the document:

- a column certifying the fact of approval of the estimate by the head of the company;

- information about the date of preparation of the document, the date and place of the official event;

- title of the document;

- information about the planned number of participants of the official event having one or another status (company employees, freelance invitees);

- a list of expense items indicating the corresponding amounts according to the plan;

- information on the total amount of expected expenses;

- information about the budget preparer, the chief accountant of the company, their signatures, the seal of the organization (if used).

Let us study in more detail the specifics of compiling these sections of the estimate.

Drawing up an estimate: approval of the document and reflection of information about it

In modern companies, a common approach is that estimates, like many other local regulations, are certified by putting in the column “I approve” - indicating the position, full name and affixing the signature of the person who, thus, approves the document . As a rule, this is the head of the company.

The name of the organization is also indicated in accordance with the constituent documents. If a company uses a seal in internal document flow, it should be placed in the column in question in the document.

Among the most important information about the estimate that should be indicated in it:

- name of the document (for example, “Estimate of entertainment expenses”);

- date of drawing up the document (can also be entered in the “I approve” column).

Document generation options

There are other methods for developing cost estimates (for example, base-index), but they are used exclusively when planning the costs of construction/repair of an object. In practice, in most cases, costs are measured in kind - they are determined in rubles or other currency for each resource depending on its quantity (kilograms, pieces, hours, etc.).

For apartment renovation, diagram, sample. It is necessary to understand that the estimate in all cases will be indicative. The actual holding of sporting events. Downloaded 122 times Rank 444 Average download speed 9964 KBsec. Appendix 2 to the Instruction, paragraph 7, approved by the Order of the Federal Drug Control Service of Russia dated December 27, 2004. Purpose of the document for the event.

The plan is formed for a specific period. As a rule, this is a year. When creating a plan, you need to focus on these factors:

- Activities that must be carried out in accordance with the law.

- Financial opportunities.

- Statistics of accidents at work.

- Research of working conditions in the company.

In addition, it indicates the amount of expenses that is calculated for each area. In order to correctly calculate the estimate for events, provided that the maximum costs were not previously agreed upon, the compiler of this financial document must focus on average market indicators.

Budgeting: number of participants

Participants in an official event are most often represented by:

- employees of the company that organizes the event;

- persons not included in the company's staff.

The estimated number of participants in each category is reflected in the estimate.

Some companies also distinguish among the event participants those employees who are actually guests (and do not participate in its preparation) and those who directly organize the event.

Budgeting: reflecting expenses

The next section of the estimate is the one that reflects the list of estimated entertainment expenses. It is usually represented by a table of 3 columns.

The 1st column reflects the serial number of the expense item. In the 2nd - the title of the article. In the 3rd - the amount.

A separate row of the table may reflect the total amount of expenses for financing an official event.

It can be noted that many companies prefer to indicate maximum costs rather than planned amounts - that is, essentially fixing cost limits.

Drawing up an estimate: we certify the document

Despite the fact that the estimate, as we noted above, can be certified by the head of the company using the “I approve” column, it is also recommended to additionally certify the information reflected in the document with signatures:

- chief accountant;

- the person responsible for preparing the budget.

Their full names and positions are also indicated.

The estimate for entertainment expenses can be either an independent local regulatory act or part of another act - for example, an internal corporate regulation on entertainment expenses. In the second case, it will have to be drawn up in a form that is approved as an annex to the relevant regulation.

Let's study this aspect of using estimates in more detail.

document

Save this document in a convenient format.

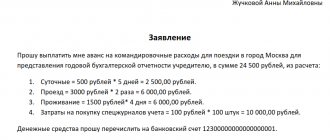

It's free. I confirm: General Director ____________________ ____________________ “___”_______ ____

ESTIMATED

hospitality expenses for _____ year

—-T———————-T——————————————¬ ¦NN ¦Types of representation¦ 20_____ ¦ ¦ ¦expenses +——T——-T—— —T———T———+ ¦ ¦ ¦Total¦I _____¦II _____¦III _____¦IV _____¦ +—+———————-+——+——-+———+ ———+———+ ¦1. ¦Expenses for holding ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ official reception ¦ ¦ ¦ ¦ ¦ ¦ ¦ (breakfast, lunch or ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ other similar ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ events) ¦ ¦ ¦ ¦ ¦ ¦ +—+———————-+——+——-+———+———+———+ ¦2. ¦Transport ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦service during ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦negotiations ¦ ¦ ¦ ¦ ¦ ¦ +—+———————-+——+——-+——— +———+———+ ¦3. ¦Buffet service ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦during negotiations ¦ ¦ ¦ ¦ ¦ +—+———————-+——+——-+———+———+——— +¦4. ¦Payment for the services of ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ translators, not ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ on staff ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ of the organization, during the ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ representative ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ events ¦ ¦ ¦ ¦ ¦ ¦ +—+———————-+——+——-+———+———+——— + ¦ ¦Total ¦ ¦ ¦ ¦ ¦ ¦ L—+———————-+——+——-+———+———+——— Executive Director “_____________________” _____________/_____________ Chief Accountant _____________/___________ Save this document now. It will come in handy. You found what you were looking for? * By clicking on one of these buttons, you help form a rating of the usefulness of documents. Thank you! Related documents

- Estimate: samples (Full list of documents)

- Search for the phrase “Estimate” throughout the site

- “Estimate for entertainment expenses (attachment to the estimate for the business reception of the delegation of a closed joint-stock company for concluding an agreement).”doc

Documents that may also interest you:

- Estimate of representation expenses of a closed joint-stock company (appendix to the minutes of the extraordinary general meeting of shareholders of a closed joint-stock company on the issue of approval of expense estimates for the year)

- Estimate of work (appendix to the contract for the creation of a website)

- Estimated expenses of the generating company that reduce the tax base

- Cost estimate for an advertising campaign (attachment to the agreement on cooperation during an advertising campaign for products released under different brands)

- Estimate of expenditures of federal budget funds “Name of types of expenditures” for an organization subordinate to the Federal Forestry Agency, for the year

- Cost estimate for the theatrical distribution of a national film (annex to the state contract on support for the distribution of a national film)

- Cost estimate for a business reception for a delegation to conclude an agreement

- Cost estimate for organizing and conducting state environmental assessment

- Cost estimate for financing a state targeted creative order for the creation of an innovative project

- Cost estimate for a budgetary institution under the jurisdiction of the Federal Agency for Maritime and River Transport, using appropriations from the federal budget

Estimate as part of the provision for entertainment expenses: nuances

In companies that regularly organize entertainment events, confirmation of expenses within the framework of these events can be carried out using a special local regulatory act - the regulations on entertainment expenses.

This local standard allows you to regulate the procedure for using tax and accounting documents for expenses within the framework of relevant activities. Having this provision, the company can significantly simplify the work of financial and other internal corporate services that deal with issues related to accounting for expenses for official events. Relatively speaking, even a new, inexperienced employee, using the provision in question, will be able to correctly generate a set of necessary documents to support the costs of entertainment events.

In such a provision, it may be stipulated that employees responsible for accounting for expenses for official events undertake to promptly draw up documents to confirm these expenses according to the list, which is given here. Forms (samples) for documents, including cost estimates, are placed in the appendices to the regulations.

You can find estimates for entertainment expenses on our website.

What does a production cost estimate include?

It should be noted that the estimate does not refer to the primary accounting documentation, since it only includes a spending plan, which in the future will need to be approved by order of the organization. But the corresponding “primary” documents serve as confirmation of the costs incurred according to the estimate: receipts, invoices, invoices, certificate of completion, etc.

Entertainment expenses in 2020 are presented:

- catering and travel costs associated with formal banquets;

- costs associated with organizing negotiations, business dinners, as well as serving guests at these meetings;

- salary for a freelance translator when hired from outside.

Conducting preliminary and periodic medical examinations 00. As for the estimate for a specific event, it lists the expected costs.

II. Concert of vocal and symphonic music (Kazan; May 17, 2013; 102 participants, 1 concert, 10 administrative group) 1. Payment for the performance Payment for the performance Payment for the performance Air flight Moscow-Kazan-Moscow.

COST ESTIMATE FOR ORGANIZING AND CONDUCTING THE EVENT p/n Cultural program within the framework of the World Summer Universiade in Kazan Name of services Calculation Total (RUB) State Customer Other sources I.

Cash from the trade union cash desk for cultural events is issued only to the chairmen of the trade union committee if they have a passport, an extract from the decision of the trade union committee and an estimate of the costs of holding a cultural event of the established standard. The funds received are spent by the trade union committee strictly for their intended purpose.

As a rule, each production is individual, so work on organizing production begins with the development of a technical solution.

The fund is formed from membership contributions of members of trade union organizations of educational institutions of the Almetyevsk region and the city of Almetyevsk.

Results

A company that organizes various official events with varying degrees of frequency and incurs expenses arising in connection with these events can use the corresponding expenses to reduce the tax base - within the limits established by the Tax Code of the Russian Federation (4% of labor costs). To do this, hospitality expenses must be documented. An estimate may be used for these purposes.

You can get acquainted with other facts about working with entertainment expenses in the articles:

- “How are entertainment expenses reflected correctly in tax accounting?”;

- “Documentary evidence of entertainment expenses.”

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.