Registration of backhoe loader rental services occurs in several stages.

The first stage is signing the lease agreement. At this stage, the parties agree on rental conditions, price, and possible nuances.

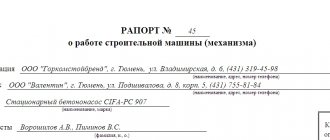

The second stage is recording the working time in the report on the work of the construction machine, form ESM-3, or in the waybill ESM-2. The amount of time worked at the site is recorded and signed by the excavator operator and the foreman, site manager or other responsible person on the customer’s side.

Next, based on the entries in the report or voucher, a report on the work/services performed is drawn up, which records the total number of hours for the period; the report is usually signed by the directors of the customer and the contractor, or other authorized persons.

In addition, the fact of the operation of the construction machine, and the responsibility of the customer’s representative for the commands given to the excavator operator, can be recorded in a special journal ESM-6, this is done to avoid possible misunderstandings that may arise in unforeseen cases. For example, when an underground cable or pipe breaks.

On this page we have posted for you the primary documentation, usually used to record working hours when renting construction equipment, use it to your health!

Report on the operation of a construction machine (shift report), standard interindustry form ESM-3, EXCEL file

Construction vehicle waybill, standard interindustry form ESM-2, EXCEL file

Logbook for the operation of construction machines, standard interindustry form ESM-6, EXCEL file

Help for payments for work (services) performed, standard interindustry form ESM-7, EXCEL file

A report on the operation of a construction vehicle or mechanism (form ESM-3) is a document very similar in many of its columns to the waybill for a construction vehicle, form ESM-2. Its important difference lies in the purpose and type of technology used.

Components of a report

The paper is filled on both sides. The title side lists information about the date the report was compiled, its number, the OKUD and OKPO form. At the top of the title page, in addition to the phrase “Report on the operation of the construction machine (mechanism)” with the paper number, there must be the name of two organizations: the customer and the contractor of the construction work. The name, brand of the car and the person driving it are also indicated.

After, on the right, in the report there is a small plate with columns to indicate:

- code of the type of operation performed;

- period of work, from what date to what date (practice has shown that it is most convenient to draw up a report for a decade);

- section or column (if available);

- inventory and personnel number of the mechanism (machine), its brand or model.

For what types of equipment can it be used?

In total, the Russian nomenclature of construction machines, as well as mechanized construction tools, includes more than a thousand different standard sizes. Moreover, new models appear regularly and further expand this list.

If we divide machines and mechanisms by the type of work performed (and this is a very arbitrary division, since there are many models that combine functionality and can be additionally equipped), you will get the following grouping:

- Earthmoving machines. These are excavators (including multi-bucket ones), hydromechanical devices, scrapers, graders, bulldozers.

- Sealing varieties. Static or vibration compaction rollers, hydraulic vibrators, vibration compaction surface machines, etc.

- Drilling models. These include pneumatic drilling hammers, as well as shock-rope, rotary or pneumatic impact machines.

- Pile driving machines. These are vibratory hammers, vibratory hammers, various pile driving equipment, diesel hammers, etc.

- Lifting and transport. The most common of this type are tower cranes, cranes, and truck cranes of various models.

- Loading and unloading. Gantry cranes of various lifting capacities, lifts of various models, etc.

- Transport. Slab trucks, panel trucks, cement trucks.

- Crushing and screening plants. Mobile crushing and screening plants.

- Mixing. Truck-mounted concrete mixers.

- Concrete placing machines, in particular concrete mixers, concrete mixer trucks.

- Reinforcement. Benders of reinforcement of various designs, equipment for its welding, tensioning.

- Finishing. Plastering units, mortar pumps, mosaic grinding machine, etc.

- Road.

- Power tool.

Naturally, the list is incomplete.

All equipment that can be described in a report on the operation of a construction machine can be found in SNiP 3.01.01-85 on the organization of construction production.

For example, in the form of such a report on the operation of a construction machine, reports on the operation of generators using any type of fuel, stationary and mobile concrete pumps can be received.

In any case, when deciding on the form of the document, you must be guided by the presented list. The mechanism or machine must belong to one of the sections given.

Nuances

It is worth remembering that each work shift has its own line. It is possible to combine strings of the name of the object on which the work is being carried out. But the signature of the driver and the customer must be affixed to each line as the work is completed.

When submitting a report on the operation of a construction machine to the accounting department, it must bear the signature of the foreman and the driver. After payroll calculations have been made, the second side is signed by the person who made them (accountant) and the head of the organization.

We provide different types of services, and each type corresponds to a set of official forms in accordance with the Civil Code and orders of regulatory authorities. When completing transactions and further work, the entire proposed package must be signed by both parties.

1. Rental of special equipment

- Option 1. Contract for the provision of construction equipment services. Standard contract in PDF

- Option 2. Rental agreement for construction equipment (with crew) Standard agreement in PDF

- Certificate of delivery/acceptance of performed services. Standard act in Excel

- Form ESM-3. The form (Report on the operation of construction equipment) serves as the primary document for recording the operating time of the construction equipment. Form (Report) ESM-3 in Excel

- Form ESM-7. The form (Certificate) serves as a document for writing off fuel as the cost of services in accounting. Form (Help) ESM-7 in Excel

Shift reports

A report on the operation of a construction machine (mechanism) (form No. ESM-3) is used in specialized organizations to record the work of a construction machine (mechanism) at an hourly rate and is the basis for obtaining initial data when calculating wages for service personnel. The report is written out in one copy by the official responsible for rationing and calculations, the foreman or an authorized person. This is stated in the resolution of the State Statistics Committee of the Russian Federation dated November 28, 1997 No. 78.

Previously, when providing construction equipment by a contractor, the customer had to provide:

– waybill for construction vehicle (form No. ESM-2); – a certificate for payments for work (services) performed (form No. ESM-7).

These forms are unified, approved by Resolution of the State Statistics Committee of the Russian Federation dated November 28, 1997 No. 78. Resolution of the State Statistics Committee of Russia dated November 28, 1997 No. 78 is not registered with the Ministry of Justice of Russia. Since 2013, the forms of primary documents have been approved by the head of the organization upon the recommendation of the person entrusted with accounting (Part 4 of Article 9 of the Law of December 6, 2011

No. 402-FZ). The composition of the mandatory details of primary accounting documents is established by paragraph 2 of Article 9 of the Federal Law “On Accounting”.

Thus, the documentation of transactions depends on the subject of the contract. If the subject of the contract is excavator services, a certificate of services rendered is sufficient. It is not necessary to receive a report in form No. ESM-3 from the contractor.

The rationale for this position is given below in the recommendations of the “GlavAccountant System” vip – version and in the articles of the journal “Accounting in Construction”, which you can find in the “Magazines” tab of the “GlavAccountant System” vip – version

1. Recommendation: How to organize document flow in accounting

The documents that the accounting department works with can be divided into two groups:*

- tax accounting and reporting documents;

- accounting documents.

Tax accounting and reporting documents include tax reporting forms and tax registers.

https://youtu.be/xQUUh1Xq9-I

Accounting documents are divided into three groups:*

- reporting forms;

- accounting registers;

- source documents.

The composition of the accounting reporting forms depends on whether the organization is a small enterprise, as well as a commercial or non-profit organization.

Source documents

Each fact of economic life must be confirmed by a primary document (Part 1 of Article 9 of the Law of December 6, 2011 No. 402-FZ).

The forms of primary documents are approved by the head of the organization upon the recommendation of the person entrusted with accounting (Part 4 of Article 9 of the Law of December 6, 2011 No. 402-FZ).

The primary document must contain the following mandatory details:*

- Title of the document;

- date of document preparation;

- name of the economic entity (organization) that compiled the document;

- content of the fact of economic life;

- the value of the natural and (or) monetary measurement of a fact of economic life, indicating the units of measurement;

- the names of the positions of the persons who completed the transaction, operation, and those responsible for the correctness of its execution, or the names of the positions of the persons responsible for the accuracy of the execution of the accomplished event;

- signatures of these persons with transcripts and other information necessary to identify these persons.

Such a list is established by Part 2 of Article 9 of the Law of December 6, 2011 No. 402-FZ.

The primary document must be drawn up when a fact of economic life is committed, and if this is not possible, immediately after its completion (Part 3 of Article 9 of the Law of December 6, 2011 No. 402-FZ).*

Primary documents are drawn up on paper and (or) in the form of an electronic document signed with an electronic signature (Part 5 of Article 9 of the Law of December 6, 2011 No. 402-FZ).

Standard forms*

Unified forms of documents contained in albums of unified forms approved by resolutions of the State Statistics Committee of Russia are not mandatory for use. At the same time, the forms established by authorized bodies on the basis of federal laws remain mandatory for use.

Such clarifications are contained in the information of the Ministry of Finance of Russia dated December 4, 2012 No. PZ-10/2012.

Thus, the organization is obliged to use standard forms of documents approved by the Government of the Russian Federation, the Bank of Russia (for example, payment orders, cash outgoing and incoming cash orders) and other authorized bodies in pursuance of federal laws.

Unified forms of documents contained in albums of unified forms, approved by resolutions of the State Statistics Committee of Russia, are not required to be used. That is, if for any fact of economic life a unified form of the primary document is established by a resolution of the State Statistics Committee of Russia, then the organization has the right, at its own choice:

- or develop the document form yourself;

- or use a unified form.

According to the general rule, the forms of primary documents are approved by the head of the organization upon the recommendation of the person entrusted with accounting (Part 4 of Article 9 of the Law of December 6, 2011 No. 402-FZ). That is, the manager must approve either the form independently developed by the organization, or the fact that the organization uses unified forms.

In any case, the primary document must contain all the mandatory details listed in Part 2 of Article 9 of the Law of December 6, 2011 No. 402-FZ.

The information included in this list is identical in composition and content to the details of documents compiled according to the forms contained in the albums of unified forms.

That is, the current unified forms comply with the requirements of Part 2 of Article 9 of the Law of December 6, 2011 No. 402-FZ.

If necessary, you can add details to unified forms (additional rows, columns, etc.) or exclude them. Approve the corrected unified form by order (instruction) of the manager as a primary document*.

Such conclusions follow from the provisions of Article 9 of the Law of December 6, 2011 No. 402-FZ and are confirmed by information from the Ministry of Finance of Russia dated December 4, 2012 No. PZ-10/2012.

Sergey Razgulin , Deputy Director of the Department of Tax and Customs Tariff Policy of the Russian Ministry of Finance

2. Article: Loading and unloading operations. Accounting Features

N.S. Kulaeva, tax consultant at BKR-Intercom-Audit CJSC

Construction work involves many complex machines, mechanisms, lifting and other equipment. What nuances need to be taken into account when accounting for loading and unloading operations and transportation? Can these costs be included in tax expenses? The answers are in our article.

Organization of work

Vehicles and equipment used for loading and unloading operations must be suitable for the nature of the cargo being moved.

The sites for these works are planned in such a way that they have a slope of no more than 5 degrees, and their dimensions and coverage correspond to the work project.

The movement of vehicles on construction sites and access roads to them should be regulated by generally accepted road signs and indicators.

When performing loading and unloading operations, the legal requirements on the maximum standards for carrying heavy loads and the admission of workers to perform these works must be met.

It should be taken into account that carrying materials on a stretcher along a horizontal path is possible only in exceptional cases and at a distance of no more than 50 meters, and carrying materials on a stretcher along stairs and stepladders is strictly prohibited.

Workers are allowed to load (unload) dangerous and especially dangerous goods only based on the results of a medical examination. In addition, these workers must undergo special training in occupational safety and subsequent certification. And also know and be able to apply first aid techniques.

The procedure for accounting for work, as well as reflecting transportation costs and costs for loading and unloading operations depends on what type of machinery and equipment the construction organization uses – its own or rented ones.

Rental of transport and equipment

Relations arising in connection with the lease agreement are regulated by Chapter 34 of the Civil Code of the Russian Federation.

Under a lease agreement for a vehicle with a crew, the lessor provides the lessee with a vehicle for a fee for temporary possession and use and provides its own services for its management and technical operation. The lessor's obligation to maintain the vehicle is established by Article 634 of the Civil Code of the Russian Federation.

Operations for the sale of services on the territory of Russia, on the basis of Article 146 of the Tax Code of the Russian Federation, are recognized as subject to VAT. Thus, the lessor organization is obliged to issue an invoice to the tenant construction organization for rental services.

The amount of VAT presented by the lessor is accounted for as the debit of account 19 “Value added tax on acquired assets” and the credit of account 76 “Settlements with various debtors and creditors.” Based on the invoice issued by the lessor and after rental services are reflected on the balance sheet, the amount of VAT is accepted for deduction.

In accounting, an entry is made to the debit of account 68 “Calculations for taxes and fees” and the credit of account 19 “Value added tax on acquired assets.”

The set of documents for leasing machines and mechanisms includes: – a written rental agreement; - the act of providing services;

– invoice.

Machinery and mechanisms leased by the organization are accounted for in off-balance sheet account 001 “Leased fixed assets” in the amount specified in the lease agreement.

How to ensure work safety?

Source: https://www.glavbukh.ru/hl/5594—smennye-raporta