Accounting in its modern version is presented as an orderly system for collecting, registering and summarizing information. Data are expressed in monetary terms. They characterize the property and obligations of the organization, as well as their movements through continuous continuous documentary accounting of ongoing business transactions.

Explanation

The definition given above is considered the most comprehensive. In this regard, it is enshrined at the legislative level and is present in the Federal Law “On Accounting”. This concept most fully characterizes the functions of the system. First of all, the orderliness of accounting is emphasized. The definition in a concise form also reflects the main stages of the process: collecting, recording and summarizing information. The features of the system are also clearly defined, distinguishing it from other accounting forms - statistical, operational and others. These features include maintaining strict documentation and continuity of the process. The main measure of information – money – is also indicated in the definition. And finally, reporting objects are highlighted.

Contents of accounting

Accounting is mandatory for all business entities (with the exception of individual entrepreneurs and branches of foreign companies under certain conditions), and is an integral part of the overall management system for the financial and production processes of the enterprise.

The content of accounting consists of accounting objects, which include:

- financial obligations;

- property assets of the enterprise;

- income and expenses;

- business transactions carried out by an enterprise in its activities.

Goals and objectives of accounting: general information

The main function of the system is to provide information to its own and third-party stakeholders in accordance with the law or in accordance with the information needs. The data that is provided to its own users must be reliable, timely and sufficient for making decisions to ensure the most effective management of the enterprise, assessing its activities, planning, carrying out control measures, and functioning in non-standard conditions. Information contributes to the correct choice of organizational policy, investment forecasting, and so on.

Feedback function

The business management system is built on the feedback principle. The constant exchange of accounting data between various production services allows for the smooth functioning of the entire system.

When using feedback, various deviations from the norm are most effectively identified, hidden reserves are revealed and unreasonable costs are reduced. Continuous accounting provides users with data on the state of current assets, relationships with partners, credit institutions, and regulatory authorities.

Main tasks of accounting

They are formulated in the above regulations. The main tasks of accounting are as follows:

- Formation of reliable and complete information about the activities of the enterprise and property status necessary for internal users of reporting. The latter, in particular, include managers, participants, owners, and founders. Data is also made available to external stakeholders. These include creditors, investors and other entities.

- The tasks of accounting include providing information to internal and external users to monitor compliance with legislation in the process of carrying out business activities by the enterprise. Based on the data obtained, the feasibility of the measures, the availability and movement of property and liabilities are assessed. The data makes it possible to analyze the rational use of labor, money and material resources, and the compliance of their use with established estimates and standards.

- The tasks of accounting (financial) accounting also include preventing negative results from the economic activity of an enterprise. Reporting allows you to identify on-farm reserves to ensure the sustainability of the organization.

The essence of accounting, the subject and scope of its application

For proper organization of accounting, it is important to understand the essence of accounting and the scope of its application, as well as the subject of accounting.

The essence of accounting is revealed by its definition, according to which accounting in an enterprise of any form of business is an orderly system of collecting, recording, analyzing and summarizing information about:

- property assets (in monetary equivalent),

- financial obligations of the enterprise,

- on the movement of financial flows of a business entity.

All transactions are reflected in accounting through continuous and continuous document flow.

Considering the essence and objectives of accounting, one should correctly understand its integral part - the subject of accounting.

The subject of accounting is the entire cycle of financial and economic activities of the company, including:

- formation of financial and material sources necessary for the implementation of the enterprise’s activities;

- distribution and placement of generated and raised funds.

The scope of accounting is extensive and is determined by its type or subtype.

The main area of application of accounting is the formation of complete and reliable information about the current financial situation and results necessary for the preparation of financial statements on the activities of the enterprise. It is necessary both for internal users - management, founders, accounting and warehouse employees who carry out current accounting of finances and assets, and for external users - services to which a business entity provides financial statements.

Another area of application is management accounting. This type of accounting provides for the generation of financial information exclusively for internal use by the company’s personnel - managers, economists, top managers who make decisions when determining the company’s production policy.

Tax accounting should also be noted. It is carried out in accordance with tax legislation and is necessary for the collection and analysis of information used in calculating taxable profit. Tax accounting may partially coincide with accounting.

Having examined the concepts and roles of the main components of accounting, you can see how the purpose, essence and main tasks of accounting are interconnected, and what is its role in the activities of the enterprise.

Management reporting system

The tasks of accounting intended for internal users of an enterprise include:

- Focus on achieving certain performance results.

- Providing alternative methods for resolving issues raised.

- Selection of the optimal control option and calculation of standard parameters for its implementation.

- Interpretation of detected deviations from established performance standards and their analysis.

It should be noted that over time, the tasks of accounting in management have expanded significantly. Additional features include:

- Registration of costs and provision of reporting to interested parties. In this case, we are talking, among other things, about classifying, summarizing, disclosing and explaining cost data to users.

- Determination and assessment of the amount of costs in relation to certain products, services (works) or responsibility centers, places where costs arise.

- Cost analysis and cost management. In this case, we mean providing information in such a form that it is suitable for control and planning.

About the subject and methods of accounting

What are the subject and method of accounting? Regarding the first phenomenon, there can be many options. And before revealing them, let’s first define what an accounting object is. Most often, it is understood as one or more structural economic units inside or outside the company (but directly related to the activities of the company), generating data useful to accounting to one degree or another.

Most often, of course, these are numbers - for profits, losses, wages, loans, etc. Actually, the subject of accounting is the specific actions of the object or the results of their implementation, events and other types of important, from the point of view of the current goals and objectives facing before the accountant, facts. The subject and method of accounting are interdependent. The properties of the first are determined by the essence of the second. Accordingly, the characteristics of the accounting method applied in a particular case depend entirely on the subject under study.

Now, actually, about what accounting methods are. Let us immediately remember the differences in the interpretation of the term that we outlined above. Here it is used in the plural. That is, we mean accounting methods. What are they?

In the interpretation generally accepted by Russian economists, they are considered to be a set of methods by which generalization (or, conversely, detailing) of information related to accounting activities is carried out. In practice, accounting methods are used, as a rule, in solving problems related to enterprise management. And in some cases - for reporting and analytical purposes (for example, when the task is to show the success of a business model to investors or the correctness of spending budget funds to departments).

Methodology

The generation of information about current income and expenses, amounts of accounts payable and receivable, the state of sources of funds is achieved through the implementation of various actions, the implementation of techniques and methods for assessing, documenting, and identifying objects. Solving accounting problems is also important. There are a variety of teaching aids containing examples and explanations that contribute to a more complete understanding of the discipline. In particular, to implement certain procedures in practice, you can use a manual that contains some cross-cutting accounting task, presented in two parts. The first provides general organizational and economic conditions for the functioning of an enterprise under a certain tax regime, for example, with the deduction of UTII. This part solves problems related to accounting processes and business transactions. The second part summarizes and systematizes certain provisions of legislative and regulatory acts on the issues of reporting under a different tax regime, for example, the simplified tax system. At the end of both parts, accounting and tax reporting is generated.

Analytical accounting function

In the conditions of modern market relations and constant improvement of capital management, the importance of the analytical function cannot be underestimated. All analytics of the company’s economic activities are based on documented accounting information. The analytical function is inextricably linked with the informational one, but, nevertheless, these concepts carry different semantic loads.

Using the analytical function allows you to determine:

- efficiency of all enterprise structures;

- company profitability;

- justification of costs;

- required sales volumes;

- number of service personnel;

- economic policy taking into account inflation.

Accounting policy is a set of accounting methods adopted in an organization - primary observation, cost measurement, current grouping and final generalization of the facts of economic activity.

[p.316] In the Accounting Regulations Accounting Policy of an Organization (PBU 1/8) (Order of the Ministry of Finance of the Russian Federation dated December 9, 1998 No. 60n), the accounting policy of an organization is understood as a set of accounting methods - primary observation, cost measurement, current grouping and final generalization of facts of economic activity. This definition coincides with the definition of the accounting method, since when deciphering the listed methods, it results in documentation and inventory, assessment and calculation, accounts and double entry, balance sheet and reporting. Therefore, in practice, the question of accounting policy often arises - is it an accounting method or something else? This once again speaks to the difficulty of accurately and completely defining not only the content, but also the very concept of accounting policy. [p.209] Accounting methods include methods of grouping and assessing facts of economic activity, repaying the value of assets, methods of organizing document flow, inventory, methods of using accounting accounts, processing information and other relevant methods and techniques. [p.32]

In cases where an assessment in monetary terms of the consequences of a change in accounting policy in relation to periods preceding the reporting period cannot be made with sufficient reliability, the changed method of accounting is applied to the corresponding facts of economic activity that occurred only after the introduction of such a method. [p.36]

These are methods of organizing document flow, inventory and methods of using accounting. This is the use of a system of accounting registers and the procedure for filling them out. This is a set of accounting methods - primary observation, cost measurement, current grouping and final generalization of the facts of economic activity. [p.50]

The explanatory note should explain the reasons for changes in the balance sheet at the beginning of the year, disclose different accounting methods from the previous year, changes in accounting policies that significantly affect the assessment and decision-making of users of the statements, the reasons for these changes and an assessment of their consequences in monetary terms. [p.87]

The most important element of any methodology for analyzing the financial position of an organization is familiarization with its accounting policies. As mentioned above, in accordance with Art. According to the Federal Law on Accounting, an organization is obliged to annually adopt an accounting policy, which is approved by order or instruction of the person responsible for the organization and state of accounting. The accounting policy of an organization is understood as the set of accounting methods adopted by it - primary observation, cost measurement, current grouping and final generalization of the facts of economic activity (Article 1 of PBU 1/98). As a rule, the main provisions of the order on accounting policies are given in a separate section in the annual report. Depending on the chosen accounting policy or as a result of changes to it, financial performance indicators and financial results may change significantly. Therefore, the analyst (user) must know about the principles of accounting policies adopted at the analyzed enterprise. PBU 1/98 provides only general requirements for the formation and disclosure of accounting policies; as for specific situations, the content of the relevant document can vary significantly. [p.249]

When forming the accounting policy of an organization in a specific area of maintaining and organizing accounting, one method is selected from several allowed by legislation and regulations on accounting. If the regulatory documents do not establish accounting methods for a specific issue, then when forming an accounting policy, the organization develops an appropriate method based on this and other accounting provisions. [p.443]

The accounting methods chosen by the organization when forming its accounting policies are applied from the first January of the year following the year of approval of the relevant organizational and administrative document. At the same time, they

Accounting methods are considered essential, without knowledge of the application of which by interested users of financial statements it is impossible to reliably assess the financial position, cash flow or financial results of the organization. [p.444]

Accounting methods adopted in the formation of the organization’s accounting policies and subject to disclosure in the financial statements include methods of depreciation of fixed assets, intangible and other assets, valuation of inventories, goods, work in progress and finished products, recognition of profits from the sale of products, goods, works, services and other methods that meet the requirements given in clause 11 of these Regulations. [p.444]

Significant methods of accounting are subject to disclosure in the explanatory note included in the financial statements of the organization for the reporting year. [p.445]

It is not considered a change in accounting policy to approve the method of accounting for facts of economic activity that are essentially different from the facts that occurred previously, or that arose for the first time in the organization’s activities. [p.445]

The consequences of changes in accounting policies that have had or are likely to have a significant impact on the financial position, cash flow or financial performance of the organization are assessed in monetary terms. The assessment in monetary terms of the consequences of changes in accounting policies is made on the basis of data verified by the organization as of the date from which the changed method of accounting is applied. [p.446]

If the specified requirement for reflecting the consequences of changes in accounting policies is met, one should proceed from the assumption that the changed method of accounting was applied from the first moment the facts of economic activity of this type arose. Reflection of the consequences of changes in accounting policies consists of adjusting the relevant data included in the financial statements for the reporting period for the periods preceding the reporting period. [p.446]

The organization must select and apply accounting policies in such a way that the financial statements comply with all the basic requirements of the regulatory legal acts of the Russian Federation on accounting. When forming the accounting policy of an organization in a specific area of maintaining and organizing accounting, one method is selected from several allowed by legislation and regulations on accounting. If the regulatory documents do not establish accounting methods for a specific issue, then when forming an accounting policy, the organization develops an appropriate method based on this and other accounting provisions. [p.206]

Thus, accounting methods are considered essential, without knowledge of the application of which a reliable assessment of the financial position, cash flow or financial results of the organization by interested users of the financial statements is impossible. For example, the method used for calculating depreciation of fixed assets should not be considered significant when disclosing information in financial statements. [p.544]

Accounting policy is the organization’s choice of methods for maintaining accounting records, grouping and evaluating factors of economic activity, repaying the value of assets, organizing document flow, methods of using accounting accounts, systems of accounting registers, processing information and other relevant methods and techniques of accounting. [p.30]

Accounting methods that must be disclosed in the financial statements include the method of depreciation of fixed assets and intangible assets, valuation of inventories, goods, work in progress and finished products, recognition of profit from the sale of products, goods, works, services and other required indicators. [p.31]

The main methods of accounting are subject to disclosure in the explanatory note included in the financial statements of the organization for the reporting year. Interim financial statements may not contain information about the accounting policies of the organization if there have been no changes in the latter since the preparation of the annual financial statements for the previous year, which disclosed the accounting policies. [p.32]

An organization can change its accounting policies when legislation or regulations on accounting change when the organization develops new methods of accounting when there is a significant change in business conditions. [p.32]

As necessary, it reflects funds that have not been put into operation. The method of accounting is not reflected in the accounting policy, but is regulated by regulatory documents. This account is present in the chart of accounts used by the organization, without decoding. [p.153]

The method of accounting is not reflected in the accounting policy, but is regulated by regulatory documents. This account is present in the chart of accounts used by the organization, without decoding. [p.153]

The method of accounting is not reflected in the accounting policy, but is regulated by regulatory documents. This [p.155]

According to PBU 1/94, the accounting policy of an enterprise is understood as the set of accounting methods chosen by it - primary observation, cost measurement, current grouping and final generalization of the facts of economic (statutory and other) activities. Accounting methods include methods of grouping and assessing the facts of economic activity, repaying the value of assets, methods of organizing document flow, inventory, methods of using accounting accounts, accounting register systems, information processing and other relevant methods, methods and techniques. [p.497]

conclusions

From the above we can conclude that the considered accounting methods are in organic connection with each other and are widely used. Thanks to these methods, it becomes possible to ensure continuous, complete and documented reflection in the accounting of business objects in different measures: monetary, labor and natural.

We have briefly looked at the method of accounting, its essence and basic elements, as well as its significance.

Leave your comments or additions to the material.

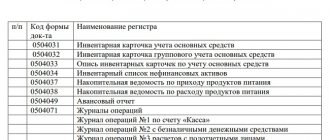

Double entry and ledger accounts

The information contained in the primary documents is systematized and reflected in the accounting accounts. Each object taken into account becomes the owner of an account containing all the information about its movement. Accounting accounts are designed to reflect (record, record) all business transactions that affect the financial condition of the organization.

And each operation necessarily involves at least two accounting accounts (debit and credit). This rule in accounting is usually called double entry. It allows you not only to reflect the availability and movement of funds, but also to monitor the accuracy of account entries.

Balance sheet as an accounting method and other forms of reporting

The formation of a balance sheet completes the work of accounting for business transactions for the period. The balance sheet is a generalized system of indicators characterizing the state of the enterprise at the reporting date.

Indicators in the balance sheet are divided into items, each of which consists of balances in groups of accounts that account for homogeneous types of assets or liabilities (inventories, debt, cash, etc.).

Articles are grouped into sections, which in turn constitute assets and liabilities. The balance sheet asset contains information about all the resources that the enterprise has, and the liability contains information about the sources of these resources. If all accounting transactions during the period were carried out correctly, then the totals of assets and liabilities of the balance sheet should be equal.

In addition to the balance sheet, the final information is reflected in other reporting forms, the main ones of which are the income statement (Form No. 2) and the cash flow statement (Form No. 4). If the balance sheet shows the state of the enterprise as of a specific date, then forms No. 2 and No. 4 reflect the financial results of activities and cash flows for the reporting period. Thus, these three forms complement each other, giving the reporting user a “three-dimensional” picture.