Completing section 1

Let us recall that in Sect.

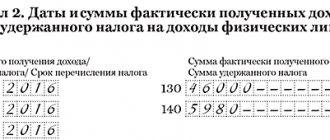

1 of the calculation indicates the amounts of accrued income, calculated and withheld tax, generalized for all individuals, on an accrual basis from the beginning of the tax period at the appropriate tax rate. When filling out this section, tax agents make the following mistakes: 1) filling out section 1 without a cumulative total . This directly contradicts clause 3.1 of the Procedure ;

2) inclusion in line 020 “Amount of accrued income” of income not subject to personal income tax . In accordance with clause 3.3 of the Procedure, this line should reflect the amount of accrued income generalized for all individuals on an accrual basis from the beginning of the tax period. At the same time, income not subject to personal income tax in accordance with Art. 217 of the Tax Code of the Russian Federation , are not reflected in the calculation ( Letter of the Federal Tax Service of the Russian Federation dated 01.08.2016 No. BS-4-11/ [email protected] );