Income recognition under the accrual method

The specificity of the accrual method is that income must be included in the tax base for profit in the period in which they arise according to documents justifying their occurrence, regardless of the actual payment (or the transfer of property as it). The conditions for reflecting income using the accrual method are contained in Art. 271 Tax Code of the Russian Federation.

Revenues from sales can be recognized as of the date:

- acceptance and transfer certificate - for immovable objects (paragraph 2, paragraph 3, article 271 of the Tax Code of the Russian Federation);

- a report or notice drawn up by a commission agent (agent) - on intermediary transactions (paragraph 1, clause 3, article 271 of the Tax Code of the Russian Federation);

- fulfillment of the obligation to transfer securities; crediting funds from partial repayment of the par value of securities - for securities (paragraph 3, clause 3, article 271 of the Tax Code of the Russian Federation).

Let us highlight some dates for the recognition of non-operating income:

- The date of the acceptance and transfer certificate is for the gratuitous transfer of property (clause 4.1 of Article 271 of the Tax Code of the Russian Federation).

- The end date of the reporting period is for transactions reflecting the restoration of the reserve (clause 4.5 of Article 271 of the Tax Code of the Russian Federation).

- The date of settlement in accordance with the contract or the end of the reporting period - for agreements concluded within the framework of lease relations (clause 4.3 of Article 271 of the Tax Code of the Russian Federation).

- Date of payment - in relation to dividends received free of charge (clause 4.2 of Article 271 of the Tax Code of the Russian Federation)

A complete list of situations indicating the moment of recognition of non-operating income for them is given in paragraph 4 of Art. 271 Tax Code of the Russian Federation.

Note that many situations regarding income recognition are controversial. ConsultantPlus experts have compiled a selection of explanations from officials and court decisions on the most common issues:

Get trial access to the system for free and see different points of view.

Note that for income of different periods, when the connection between income and expenses has not been identified, it will be necessary to distribute the income received using the principle of uniformity. The same method should be followed when receiving income from production with a long cycle and in the absence of phased delivery of work. However, taking into account the requirements of Art. 316 of the Tax Code of the Russian Federation, the procedure for the distribution of income, according to this principle, must be recorded in the accounting policy.

See also: Long production cycles may require revenue sharing .

What is the cash method when calculating income tax?

The cash method is discussed in Art. 273 Tax Code of the Russian Federation. According to it, income is recognized in the period in which it is received, and expenses are recognized when it is incurred.

The moment of receipt of income is either the day of repayment of debt to the company by its customers and other debtors, or the day of receipt of an advance payment on account of upcoming shipments.

For expenses, the moment of their recognition is defined as the day of repayment of obligations to creditors by paying funds from the cash register or writing them off from the current account or by disposing of other property.

However, you need to know some features. For example, in order to take into account the costs of purchasing materiel in a specific tax period, three conditions must be simultaneously met:

- materials have been paid for;

- written off for production;

- used in production at the end of the month, i.e. there are no WIP balances.

And in order to take into account the costs of purchased goods, you need to not only pay the supplier for them, but also sell them to the buyer.

For this accounting method, in addition to the primary documentation received from the supplier and issued to the buyer, the basis for including a particular operation in the calculation of income tax are primary documents reflecting the flow of funds: cash receipts and consumables, payment orders, bank statements.

Subscribe to our newsletter

Read us on Yandex.Zen Read us on Telegram

Recognition of expenses using the accrual method

Recognition of expenses is also carried out not when their payment was actually made, but taking into account their occurrence in accordance with a specific economic situation (Article 272 of the Tax Code of the Russian Federation).

You can recognize expenses:

- On the day of transfer of raw materials by the seller or on the date of the acceptance certificate - for material costs (clause 2 of Article 272 of the Tax Code of the Russian Federation).

- Monthly on the last day - for depreciation (clause 3 of Article 272 of the Tax Code of the Russian Federation).

- Monthly – for labor costs (clause 4 of Article 272 of the Tax Code of the Russian Federation).

- On the date when the provision of services occurred - for the repair of fixed assets (clause 5 of Article 272 of the Tax Code of the Russian Federation).

- On the date of payment in accordance with the contract or evenly throughout the entire period of its validity - expenses for compulsory medical insurance and voluntary medical insurance (clause 6 of article 272 of the Tax Code of the Russian Federation).

Non-operating and other expenses can be recognized:

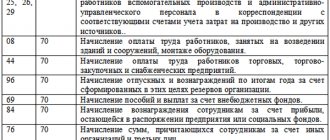

- As of the accrual date - for taxes, insurance premiums, reserves (clause 7.1 of Article 272 of the Tax Code of the Russian Federation).

- On the date of settlements according to the contract or the last day of the month - for commission fees, payment for work (services) under contracts, rent (clause 7.3 of Article 272 of the Tax Code of the Russian Federation).

- On the date of payment - for lifting, compensation for the use of personal transport (clause 7.4 of Article 272 of the Tax Code of the Russian Federation).

Of course, these lists are incomplete, and it is difficult to cite absolutely all the dates and situations provided for by the Tax Code of the Russian Federation in a short article. A complete list of points for recognizing expenses associated with production and sales can be found in paragraphs. 2–6 tbsp. 272 of the Tax Code of the Russian Federation, non-operating expenses - paragraphs. 7–10 tbsp. 272 of the Tax Code of the Russian Federation.

The procedure for accounting for subsidies by organizations using the cash method

The provision of subsidies to legal entities is regulated by Art. 78 BC RF. According to clauses 1 and 2 of this article, subsidies are provided from the federal budget, the budget of a constituent entity of the Russian Federation, the local budget, as well as from extra-budgetary funds on a free and irrevocable basis.

Subsidies are provided for the following purposes:

- compensation of lost income;

- financial support (reimbursement) of costs in connection with the production (sale) of goods, performance of work, provision of services.

In the first case, subsidies are received within the framework of a reimbursable agreement related to the sale of goods, works, services at regulated prices, tariffs (that is, the difference between the base price (tariff) and the actual sales price is compensated). When forming the income tax base, the specified subsidy is subject to reflection as part of income from sales on the date of receipt of funds to the current account on the basis of clause 2 of Art. 273 Tax Code of the Russian Federation.

If the subsidy was not received within the framework of a reimbursable agreement, it is taken into account as part of non-operating income in the manner provided for in clause 2.1 of this article:

- subsidies received to finance expenses not related to the acquisition of assets (depreciable property) and property rights are taken into account for no more than three tax periods, counting the tax period in which these subsidies were received, as expenses actually incurred through these subsidies are recognized funds. At the end of the third tax period, subsidies received that are not included in income are classified as non-operating income as of the last reporting date of this tax period (paragraph 2);

- subsidies received to finance expenses associated with the acquisition of investment assets and property rights are taken into account as expenses actually incurred using these funds are recognized. When selling, liquidating or otherwise disposing of the specified property, property rights, subsidies not included in income are treated as non-operating income as of the last date of the reporting (tax) period in which the sale (liquidation, other disposal) occurred (paragraph 3);

- subsidies received to compensate for previously incurred expenses not related to the acquisition of AI and property rights are taken into account at a time on the date of their enrollment (paragraph 4);

- subsidies received to compensate for previously incurred expenses related to the acquisition of AI and property rights are taken into account as a lump sum on the date of their enrollment in an amount corresponding to the amount of accrued depreciation for previously incurred expenses related to the acquisition. The difference between the amount of subsidies received and the amount included in income on the date of their crediting is reflected in income in a manner similar to that provided for in paragraph. 3 clause 2.1 art. 273 (as expenses are recognized, in particular for fixed assets - as depreciation is calculated) (paragraph 5).

In paragraph 6 of clause 2.1 of Art. 273 stipulates that in case of violation of the conditions for receiving subsidies provided for in this paragraph, they are fully reflected in the income of the tax period in which the violation was committed.

| Budget subsidies, with the exception of subsidies within the framework of a reimbursable agreement (clause 2.1 of Article 273 of the Tax Code of the Russian Federation) | |||

| To finance expenses | To compensate for previously incurred expenses | ||

| Not related to AI (paragraph 2) | Related to AI (paragraph 3) | Not related to AI (paragraph 4) | Related to AI (paragraph 5) |

Example 3

In January 2020, Secret LLC acquired and paid for fixed assets for RUB 1,110,000, which belongs to the third depreciation group. It was put into operation in the same month. The estimated useful life is 37 months.

In July 2020, a subsidy was allocated from the regional budget in the amount of RUB 1,110,000. In the same month, the entire amount was transferred to the company's bank account.

The depreciation rate for fixed assets is 2.7027% (1/37 months). The depreciation amount per month is 30,000 rubles. (RUB 1,110,000 x 2.7027%).

Subsidies for compensation of previously incurred expenses related to the acquisition of depreciable property are taken into account in accordance with paragraph. 5 clause 2.1 art. 273, that is, at a time on the date of their enrollment in an amount corresponding to the amount of accrued depreciation.

The amount of depreciation accrued from February to July inclusive amounted to 180,000 rubles. (RUB 30,000 x 6 months). Non-operating income in July 2020 should include RUB 180,000.

The difference is 930,000 rubles. between the amount of the subsidy received (RUB 1,110,000) and the amount included in income on the date of its enrollment (RUB 180,000) will be reflected in income in a manner similar to that provided for in paragraph. 3 clause 2.1 art. 273, that is, as depreciation is calculated on the fixed asset. Thus, every month, starting from August 2020, 30,000 rubles must be included in non-operating income.

Features of the cash method

The cash method is characterized by the fact that income is reflected at the moment when funds are credited to current accounts (received at the cash desk) or property acting as payment has been received (Article 273 of the Tax Code of the Russian Federation).

Are advances received considered income when using the cash method? The answer to this question is in the ConsultantPlus system. Get free trial access to the system and proceed to the explanations.

Expenses must be recorded when they are actually paid.

It should be noted that not every taxpayer can exercise the right to use this method of accounting for income and expenses. So, you cannot use the cash method:

- Companies whose average revenue for the previous 4 quarters excluding VAT is more than 1 million rubles. for every quarter.

- Banks.

- Credit consumer cooperatives.

- Microfinance organizations.

- Controlling persons of controlled foreign companies.

- Organizations extracting hydrocarbons from a new offshore field, if they have the appropriate license, as well as operators of these fields.

See also the material “What is the procedure (conditions) for recognizing income and expenses using the cash method?” .

In 2006, the right to use the cash method was lost

If average revenue exceeds the established limit, the organization must recalculate the tax base based on the accrual method from the beginning of the year in which the excess was made. This is the requirement of paragraph 4 of Article 273 of the Tax Code of the Russian Federation.

note

: those companies that in 2006 entered into property trust management agreements or simple partnership agreements are also required to switch to the accrual method. Such taxpayers must also recalculate the tax base from the beginning of the tax period.

However, the procedure for recalculating the tax base will be different depending on which method the organization used in 2005: accrual or cash method.

In 2005, the organization used the accrual method

In this case, when recalculating the tax base from January 1, 2006 (based on the accrual method), no special problems will arise. The results of the recalculation are reflected in the updated declarations, which must be submitted to the tax office.

Article 313 of the Tax Code does not oblige taxpayers who have lost the right to use the cash method to make changes to their accounting policies. However, we can recommend that organizations make appropriate changes to their accounting policies and inform the tax office about them. This will help avoid controversial situations.

The amount of tax on amended returns may exceed the amount of tax paid under the cash method. Then the organization must pay the missing amounts of taxes and penalties to the budget.

EXAMPLE 7

Let's use the data from example 6, changing them. Let's say Rubin LLC used the accrual method in 2005. The organization pays only quarterly advance payments of income tax. Based on the results of the first quarter of 2006, Rubin LLC calculated and paid the following tax amounts:

— to the federal budget — 13,000 rubles;

— to the regional budget — 35,000 rubles.

Based on the results of the second quarter of 2006, the tax amounts were:

— to the federal budget — 6,500 rubles;

— to the regional budget — 17,500 rubles.

Since, based on the results of the third quarter of 2006, Rubin LLC lost the right to use the cash method, the accountant recalculated tax liabilities using the accrual method. The amount of the advance payment payable for the first quarter of 2006 was:

— to the federal budget — 15,500 rubles;

— to the regional budget — 41,730 rubles.

The amount of the advance payment payable for the second quarter of 2006 is equal to:

— to the federal budget — 13,000 rubles;

— to the regional budget — 35,000 rubles.

Consequently, Rubin LLC must pay an additional advance payment of income tax for the first quarter of 2006:

- to the federal budget - 2500 rubles. (RUB 15,500 – RUB 13,000);

— to the regional budget — 6,730 rubles. (RUB 41,730 – RUB 35,000).

For the second quarter of 2006 you must pay additionally:

— to the federal budget — 6,500 rubles. (RUB 13,000 – RUB 6,500);

— to the regional budget — 17,500 rubles. (RUB 35,000 – RUB 17,500).

Let's say Rubin LLC repaid the specified debt on October 10, 2006.

The deadline for paying the advance payment of income tax for the first quarter of 2006 is April 28, for the second quarter of 2006 - July 28. Penalties will be charged for transferring missing amounts at a later date. The calculation of penalties is given in the table.

Difficulties in recognizing income and expenses

When using one method or another, the taxpayer often has a question: when should a certain income or expense be recognized? For example, there is a controversial situation regarding the issue of the emergence of non-operating income that arises in the event of the expiration of the statute of limitations on accounts payable (clause 18 of Article 250 of the Tax Code of the Russian Federation).

Tax officials explain that income arises on the last day of the reporting (tax) period in which the statute of limitations expired (letter of the Federal Tax Service of Russia dated December 8, 2014 No. GD-4-3/ [email protected] , letter of the Ministry of Finance of the Russian Federation dated September 12, 2014 No. 03 -03-РЗ/45767). But some arbitrators believe that this income must be taken into account in the period when the manager signed an order to write off such debt (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated July 15, 2008 No. 3596/08).

On this issue, see the material “In what period are overdue accounts payable included in income?” .

When applying the cash method, the amount of accounts payable (including VAT) is also included in non-operating income, while the period of income recognition falls on the date the debt is written off (letter of the Ministry of Finance of Russia dated August 7, 2013 No. 03-11-06/2/31883). This letter refers to a situation in which the taxpayer applies the simplified tax system, but since clause 1 of Art. 346.17 of the Tax Code of the Russian Federation stipulates that “simplers” keep records of income and expenses using the cash method, it can be assumed that this approach is used by all taxpayers who use this method. It should be noted that previously such accounts payable were not recognized as non-operating income when applying the cash method (letter of the Ministry of Finance of Russia dated August 26, 2002 No. 04-02-06/3/61).

Thus, in order to avoid controversial situations, it is better to establish the procedure for recognizing a particular income or expense in the accounting policy.

See also the material “What to change in tax accounting policies” .

Calculation examples

Let's look at how to calculate income tax; we'll look at an example calculation for a financial year. Let's say the company is on the general taxation system. Income for the reporting period amounted to 6,000,000 rubles. Costs for the same period are 2,000,000 rubles. Thus, the net profit will be: 6,000,000.00 – 2,000,000.00 = 4,000,000.00.

How is income tax calculated in this case?

Contributions to the regional budget will be: 4,000,000.00 × 17% = 680,000.00 rubles.

Interest paid to the federal budget: 4,000,000.00 × 3% = 120,000 rubles.

How is income tax calculated if this organization belongs to a separate category of taxpayers paying contributions to the regional treasury at a simplified tax rate of 13.5?

Local budget: 4,000,000.00 × 13.5% = 540,000.00 rubles.

In any case, the required 3% must be paid to the federal treasury: 4,000,000.00 × 3% = 120,000.00 rubles.

Next, we will provide a calculation of corporate income tax - a sample formula with tables.

In accordance with the profit and loss statement in Form No. 2, Company LLC received income in the amount of 600,000.00 rubles. Let's analyze the cost structure in accordance with the formula:

- 5000 rub. — permanent tax liability;

- 6500 rub. - Deferred tax assets;

- 35,000 rub. — accrued depreciation (linear method);

- RUB 50,000.00 - non-linear depreciation - for tax purposes.

Results

Chapter 25 of the Tax Code of the Russian Federation talks about 2 methods of recognizing income and expenses that can be used when calculating income tax:

- accrual method;

- cash method.

However, if any taxpayer has the right to choose the first of them, then the second is only those that meet the conditions established by the Tax Code of the Russian Federation.

Having given preference to one method or another, its choice should be reflected in the accounting policy.

Sources:

- Tax Code of the Russian Federation

- Letter from the Federal Tax Service of Russia dated December 8, 2014 N GD-4-3/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

Calculation formula

Next, we will analyze the income tax: how to calculate it, an example and a formula for calculation. Let's imagine how it is calculated (for dummies). To calculate the amount of income, you can use the following formulas:

TNP = D – PNO + SHE – IT;

TNU = R – PNO + SHE – IT,

- D - enterprise income;

- R - expenses of the enterprise;

- PNO - permanent tax obligations;

- ONA - deferred tax assets;

- ONO - deferred tax liabilities;

- TNP - current income tax;

- TNU - current tax loss.

Advance payments

If the organization’s profitability amounted to no more than 15 million rubles (quarter) for the previous tax period, then it has the opportunity to pay an advance on income tax quarterly. The amount is calculated from the actual amount of income.

If the company has a profitability exceeding 15 million rubles, then it must make an advance payment monthly.

How to calculate income tax in this case? The specialist can calculate the fee based on the estimated level of income predicted based on the reporting data of the previous quarter.

Long term vs. medium-term decision making and planning

There are many examples of how accrual-based financial information supports long-term planning and decision-making, and it is not surprising that this is one of the main differences from using the cash method, which is a more short-term approach. Better asset and liability management, as discussed above, allows for lower borrowing costs while providing greater flexibility to respond to emerging issues, thereby absorbing fiscal shocks. The accrual method is useful in predicting long-term sustainability, allowing longer-term forecasts to be made.

What expenses are deducted from income?

In order to find out the amount of net profit, you need to subtract income from expenses. In this case, all expenses must be confirmed and economically justified. To do this, the accountant must correctly prepare and maintain primary and tax documentation. When calculating profit, the following costs are taken into account:

- production;

- general economic;

- representative;

- transport;

- advertising, but not more than 1% of sales revenue;

- expenses for training and advanced training of personnel;

- interest on loans and credits.