Materials inventory book

Document type: Book

In order to save a sample of this document to your computer, follow the download link.

Document file size: 25.0 kb

As an alternative to accounting warehouse cards, in order to simplify accounting operations, a warehouse book has been created for recording material assets - the so-called form M-17. Each nomenclature number of this document must have its own personal account. These accounts are assigned numbers in the same way as in the case of index cards. Each account should be allocated one or more ledger pages. On all accounts, you must fill in all the details that are indicated on the warehouse account cards.

Rules for registering materials inventory books

The legislation does not provide for strict requirements for maintaining a book in the M-17 form. There is also no specific, unified form. Each enterprise has the right to establish its own procedure for drawing up this document. But there are several rules that you need to follow when filling out this book. These rules include:

- A table of contents must be placed on the first or last page of the book. It should indicate the numbering of all personal accounts, the name of the materials with a note about their distinctive features and characteristics. The number of pages in this book is also noted here;

- all sheets of the document are numbered, and the ledger itself is stitched;

- data on the number of pages of form M-17 is certified by the seal and visa of the company’s chief accountant or other authorized person;

- The materials inventory book is registered in the accounting department of the enterprise. The accountant is required to make a note about registration in the document and indicate the register number assigned to this book.

Items in cart: 0. There is currently 1 item in cart.

Cost:

Delivery cost Determine

Total to be paid:

Continue shopping Place an order

Add items worth more than RUB 3,000.00 and get free shipping!

Free delivery within Moscow

> Paper and paper products>Paper products>Books and magazines>Material inventory book (form M-17) A4, 16 sheets, on a clip, block of writing paper

Back

Forward

RUB 267,426

to order 1-2 days

Attention: limited quantity of goods in stock!

Will be available:

- Description

- Characteristics

Form M-17:

The standard interindustry form M-17 can be supplemented with your own fields, if necessary. But you can use it without changes. Download the standard material accounting card form (Form M-17) and fill it out on the computer or manually.

Get the form for free!

Register in the online document printing service MoySklad, where you can: completely free of charge:

- Download the form you are interested in in Excel or Word format

- Fill out and print the document online (this is very convenient)

Leave a comment on the document

Do you think the document is incorrect? Leave a comment and we will correct the shortcomings. Without a comment, the rating will not be taken into account!

Thank you, your rating has been taken into account. The quality of documents will increase from your activity.

| Here you can leave a comment on the document “Sample. Materials warehouse card. Form No. M-12”, as well as ask questions associated with it. If you would like to leave a comment with a rating , then you need to rate the document at the top of the page Reply for |

Rules for filling out the materials warehouse card M-17

The document is needed to capitalize inventory items, monitor their movement and consumption. It is compiled on the basis of receipt documents upon receipt of materials. An accounting card (form M-17) is created for each type of inventory.

The warehouse accounting book (form M-17) also helps to find the necessary inventory items: it indicates where they are located.

- Card number.

- Name of the organization.

- OKPO code.

- Date.

- The structural unit where inventory items are stored.

- Kind of activity.

- Stock.

- A rack or cell where an item is located.

- Brand, grade, profile, size. These are optional columns: the sample for filling out the M-17 form allows you to put a dash in them if the data is unknown.

- Nomenclature number of materials.

- Unit of measurement and price.

- Stock norm. In this column, indicate the amount of material needed for uninterrupted operation: this is the number of inventory items that should always be in stock.

- Best before date. This is necessary, for example, for paints, varnishes or similar materials. If the storage period is not important, put a dash.

- Supplier name.

In the second table of the materials accounting card (form M-17), enter the name of the goods and materials and information about their movement:

- The date of receipt or release from the warehouse.

- Name of the supplier or consumer.

- Unit of measurement.

- Income and expense - they must be recorded separately, that is, each type of operation with materials is indicated.

- Remainder.

Sample of filling out the M-17 card

At the top of the form, fill out the name of the organization in whose warehouse material assets are stored, reflect the name or number of the storage warehouse, and also put the card number and the date of its preparation.

In the upper table of the M-17 form, basic information about the materials and storage location is filled in:

- structural unit where materials are stored;

- type of activity of this unit;

- name and number of warehouse;

- specific storage location in the warehouse - rack number, cell; this information will help you find the necessary material assets at the right time in the shortest possible time);

- characteristics of materials (brand, grade, size, warehouse nomenclature number, unit of measurement, price, stock rate (the amount of materials of a given brand that must always remain in the warehouse for uninterrupted operation), expiration date (if established), name of the supplier.

Below is the name of the material, as well as information about the presence of precious metals and stones in its composition (if any).

The table below is intended to reflect incoming and outgoing transactions in relation to this type of material.

For each operation, fill in a separate line in which you need to write:

- recording date;

- Number of the document on the basis of which the entry is reflected in the warehouse accounting card M-17;

- name of the organization or unit from which the material assets were received or allocated;

- accounting unit;

- quantity of materials received or issued;

- balance after completing an incoming or outgoing transaction;

- signature and date of the responsible person.

document

Materials warehouse card form M-17 form - download.

Materials accounting card sample filling M-17 - download.

In what cases is the warehouse accounting book used?

Materials arriving at the warehouse must be registered by the materially responsible person (MOL) in a book or record card for the relevant materials (clause 54 of the order of the Ministry of Finance of the Russian Federation “On approval of the Guidelines for accounting of inventories” dated December 28, 2001 No. 119n). In this case, the use of books or materials accounting cards is equivalent (clause 274 of order No. 119n).

For information about what other functions are included in the responsibilities of a warehouse manager working in a warehouse, read the article “Job description of a warehouse keeper” .

A feature of warehouse accounting books is the need to number their sheets and lace them together. The document must be sealed and certified by the chief accountant or other competent person. The book is also subject to registration in the accounting department.

The form of the materials warehouse accounting book, which had the number M-17 (like the warehouse accounting card introduced by Decree of the State Statistics Committee of Russia dated October 30, 1997 No. 71a), was approved by order of the Ministry of Finance of the Russian Federation dated December 30, 1999 No. 107n, which lost its force as of October 1, 1997. 2005 (order of the Ministry of Finance of the Russian Federation dated September 29, 2004 No. 87n).

However, nothing prevents you from using the canceled form in your work. You just need to approve its use by order of the manager or enshrine it in the accounting policy.

You can download the form of the warehouse accounting book, given in the order of the Ministry of Finance of the Russian Federation dated December 30, 1999 No. 107n, on our website.

And the form of the current M-17 card and the rules for its registration can be found in the article “Material warehouse card - form and sample.”

Comment on the rating

Thank you, your rating has been taken into account. You can also leave a comment on your rating.

Is the sample document useful?

If the document “Sample.

Materials warehouse card. Form No. M-12" was useful for you, we ask you to leave a review about it. Remember just 2 words:

Contract-Lawyer

And add Contract-Yurist.Ru to your bookmarks (Ctrl+D).

You will still need it!

Accounting book according to the canceled form M-17: document structure

The book compiled according to the canceled M-17 form must indicate:

- name of the warehouse owner;

- the name of the structural unit in which the materials are located;

- Full name of the financially responsible person, his personal code according to the personnel service registers;

- coordinates of the warehouse, rack, cell in which the materials are placed;

- name and code of the unit of measurement of the volume of placed material;

- basic information about the material - its price, brand, grade, size, profile, as well as the stock rate;

- name of the material, its code in accordance with the classifier used;

- date, serial number of making an entry in the book;

- date and number of the primary document on the basis of which information is entered into the book;

- information about the entities that are recipients or senders of the material;

- income and expense indicators.

Each entry in the book is certified by the signature of MOL.

The structure of the document also contains a block reflecting the fact of checking the information in the book. It indicates the date of the control, its results, and the position of the inspector. Each entry in this block is certified by the signature of the inspector.

The last page of the book records the number of numbered pages. The document must be certified by the signature of the chief accountant, which is affixed by him along with the start date of maintaining the book - also on its last page.

Rules for registering a book using the M-17 form

As a rule, the accounting book of inventory items in form N M-17 is drawn up at the beginning of the calendar year (for new goods, a new sheet of the book is created before it arrives at the warehouse) by an employee of the purchasing department. Each sheet of the accounting book is a card for recording inventory items of one item. It records data such as the name of the item, the characteristic features of the product, the number of the item, the unit of measurement, as well as the accounting value of the product.

To fill out form No. M-17, follow this link - sample accounting book M-17.

Each new sheet must be numbered and registered in the accounting department. After this, the accounting book is handed over to the financially responsible person for accounting. The warehouse manager enters information about storage locations for each product. Moreover, records are made on the basis of certain documents:

- Receipt and expense orders;

- Requirements and invoices;

- Other accompanying documentation: TTN, checks, etc.

A record of a completed transaction is made as follows. The person in charge indicates the date of the operation, then enters the details of the documents that are the basis for the operation, and other information about the operation in a brief form.

Transactions must be recorded on the same day they were performed. In this case, information about each new operation must be entered in the next line. At the end of the working day, the materially responsible person checks the transactions performed and displays the results of the remaining goods in the warehouse. At the end of each month, the warehouse manager must enter summary information on receipts and expenses for the month.

Important ! All entries in the M-17 accounting book must be periodically checked by the accounting department. Information about the verification is recorded in the appropriate cells of the table.

At the end of the year, the book displays the balances as of January 1, which are transferred to the new accounting book M-17. The completed book is checked and deposited in the archives of the enterprise.

Materials accounting card according to form M-17

Under the designation M-17 lies a primary accounting document called the “Material Accounting Card”. It is used to control the movement of inventory items stored in the warehouse of enterprises and organizations. The preparation of this document is the responsibility of storekeepers and other warehouse workers, who issue it both upon receipt and upon shipment of goods and materials. It must be filled out directly on the day of the transaction for the movement of inventory and inventory.

What does a materials accounting card look like and what is it for?

To organize the correct accounting of inventory items (TMV) in the warehouse of an economic entity, various forms of accounting documents are provided. One of these forms is the standard intersectoral form M-17, put into effect by Decree of the State Statistics Committee of October 30, 1997 No. 71a.

Since it is not necessary to use unified forms, a business entity can independently develop a warehouse accounting document, taking form No. M-17 as a basis and supplementing it with the necessary details.

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

The card records information about the acceptance of valuables into the warehouse, their issuance and other movements. Based on this document, a consolidated accounting of inventories is provided for each grade, type, size, because it contains data on the amount of capitalized and consumed raw materials (materials), as well as balances for each item.

Basic rules for issuing an M-17 card

Today there is no single, obligatory sample of a material accounting card, so enterprises and organizations have the opportunity, at their discretion, to develop a document template and use it in their activities (sometimes they do this by ordering a printing house to print their own forms or printing them on a regular printer). But most often, warehouse workers, in the old fashioned way, fill out the previously generally accepted form M-17, which reflects all the necessary information about the supplier, consumer and inventory items.

For each type of product or material, its own accounting card is filled out, which is then necessarily numbered in accordance with the numbering of the warehouse card file. All necessary receipts, consumables and invoices are attached to the card.

The document can be written by hand or filled out on a computer. Moreover, regardless of how the data will be entered into it, it must contain the “living” signature of the storekeeper, as a materially responsible person who is responsible for the safety of the property entrusted to him. It is not necessary to put a stamp on the document, since it relates to the internal document flow of the organization.

Inaccuracies and blots in the materials accounting card should not be allowed, but if some mistake does occur, it is better to fill out a new form, or, as a last resort, carefully cross out the incorrect information and write the correct information above, confirming the correction with the signature of the responsible employee. In the same way, it is unacceptable to draw up a document in pencil - this can only be done with a ballpoint pen.

After the end of the reporting period (usually one month), the completed materials accounting card is first transferred to the enterprise’s accounting department, and then, like other primary documents, to the enterprise’s archive, where it must be stored for at least five years.

Instructions for filling out a materials accounting card in form M-17

The first section of the document contains:

- card number in accordance with the numbering of the warehouse card file,

- full name of the enterprise (indicating its organizational and legal status),

- OKPO code (All-Russian Classifier of Enterprises and Organizations - the code is contained in the company’s constituent papers),

- date of document preparation.

Then the structural unit in which the product is contained is indicated.

Below is a table where the first column once again includes information (but more precisely) about the structural unit that is the recipient and custodian of these inventory items:

- his name,

- type of activity (storage),

- number (if there are several warehouses),

- specific storage location (rack, cell).

The following are product details:

- brand,

- variety,

- size,

- profile,

- nomenclature number (if such numbering is available, if it is not used, you can put a dash).

Then everything related to units of measurement is entered:

- code according to the Unified Classification of Units of Measurement (EKEI),

- specific name (kilograms, pieces, liters, meters, etc.).

Next, the cost of the material, the rate of its stock in the warehouse, the expiration date (if one is established) and the full name of the supplier are indicated.

Sample inventory book and filling details

Books for warehouse accounting of forms M-17 and M-40 are documents that are used in warehouses to keep records of available materials. A person with financial responsibility is responsible for maintaining these books . Often they are employees working as warehouse managers or storekeepers.

The accounting department makes notes in these books with a certain frequency when reconciling the volumes of balances with the warehouse accounting program.

When to use

According to the current Order of the Ministry of Finance of the Russian Federation No. 119n, all material objects received for storage in a warehouse are required to undergo a registration procedure by the materially responsible employee of the enterprise, who enters all the necessary information into a special warehouse accounting book or into a special card.

At the same time, it is worth noting the fact that today the use of books or special registration cards is an absolutely equivalent action, which is confirmed by clause 274 of Order No. 119n.

One of the main specific features of books on warehouse accounting is the mandatory need to number all of their pages, as well as their lacing.

This accounting document is sealed and certified by the signature of the chief accountant of the enterprise or another official who can assume such responsibility. In addition, the book must be registered with the accounting department of a commercial organization.

Today, the format of the warehouse accounting book M-17, which was introduced in 1997 by the Decree of the leadership of the State Statistics Committee of the Russian Federation, has lost its force since October 1, 2005 after the adoption of Order No. 87n of the Ministry of Finance of the Russian Federation.

At the same time, there are no legislative prohibitions regarding the use of this outdated form in the work of the warehouse department of the enterprise. The only thing you need to take care of is to approve its use by a special separate order of the organization’s management or to consolidate this form in the internal accounting policy of the company.

Structural device

When using the outdated M-17 form in warehouse accounting, it will be useful to know about its structure, which will help you quickly learn the principle of filling it out and maintaining it. So, in the M-17 format accounting book there are separate paragraphs in which it is necessary to indicate the following information:

- The name of the organization that is the actual owner of the warehouse.

- The exact name of the department of the enterprise where material assets are stored.

- The full name of the employee bearing financial responsibility, as well as his registration code used in the personnel department of the enterprise.

- The exact coordinates of the warehouse, cell and rack where specific objects of material assets are stored.

- Name and coding of units of measurement of valuables stored in the warehouse.

- Basic information regarding the item stored in the warehouse.

- Name and code of material value, according to the classifiers used by the enterprise.

- The date, as well as the number of entries made in this accounting document.

- Date and number of the document on the basis of which changes are made to the registration card.

- Information about entities acting as senders or recipients of material objects.

- Indicators on the volume of available expenses and revenues.

The structure of this accounting document has a separate block, which reflects the facts of verification of the entered information . This block contains information about the date of the reconciliation, the results obtained, as well as the position and name of the employee who carried out the reconciliation. All entries entered into this block are certified by the personal signature of the inspector.

On the last page of this accounting document you must indicate the exact number of numbered pages . This document is certified by the signature of the chief accountant, and the start date of its maintenance is also indicated. All these marks are also left on the last page.

In addition to using special warehouse accounting books, the enterprise can use special accounting cards or monthly material reports for small turnover in warehouses.

Basic rules that are used in registration

The accounting book is opened for a period of one year by employees of the supply department. The following data is entered into this document: the name of material assets, their main characteristics (article, brand, grade and size), item number, units of measurement used, accounting value and other information relating to objects stored in the warehouse.

As a rule, a separate card .

The accounting department registers such cards in a separate register . All documents must be numbered and certified by an accountant, and then transferred to the financially responsible person, the manager of the warehouse. The warehouse manager independently enters into the accounting book all the information about the location of storage of material assets.

All sheets of the accounting book are numbered and certified by the chief accountant . In addition, they can be checked, and a corresponding entry is made in a special cell.

All entries in the accounting book are made only if there are correctly compiled and completed:

- product receipt orders;

- material requirements;

- invoices for products;

- waybills and other accompanying documents.

The warehouse manager must indicate the following information :

- date of transactions;

- details of the documentation that gives the right to carry out certain operations;

- brief information about the operation performed.

It must be taken into account that each transaction must be recorded separately in the ledger . If several operations of the same type were carried out in one working day, then you only need to indicate the name of the operation and its quantity.

All entries in the book are made directly on the same day when certain operations were carried out. the warehouse manager sums up the available balances of material assets.

At the end of the month, it is necessary to note the final data on the receipt and expenditure of valuables, as well as on their quantitative balances.

At the end of the year, all balances are indicated as of January 1 of the new year . The accounting book for the previous year is handed over for storage to the archive department of a commercial organization. The main task of management in this matter is to select the financially responsible person responsible for maintaining these accounting documents.

The implementation of warehouse accounting for beginners is presented below.

Materials accounting card (form M-17)

Accounting for material assets in the warehouse is carried out in accordance with the requirements specified in Section. 6 Order of the Ministry of Finance of the Russian Federation dated December 28, 2001 No. 119n. Reception, storage, issuance and accounting of materials in the warehouse is carried out by an official who is responsible for their safety, as well as for the correct and timely execution of operations for their movement (clause 256 of Order of the Ministry of Finance of the Russian Federation dated December 28, 2001 No. 119n).

To reflect information about the location of material assets in the warehouse and their movement for each type, a materials accounting card is intended. The materials warehouse card is maintained by the materially responsible person (for example, a storekeeper) separately for each item number of the material on the basis of primary receipt and expenditure documents on the day of the transaction (Section 3 of the Resolution of the State Statistics Committee of Russia dated October 30, 1997 N 71a).

Sample. Materials warehouse card. Form No. m-12

November 11, 2011 — Administrator

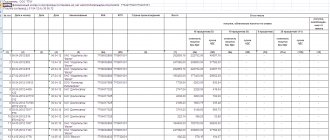

| Form No. M-12 Approved by Decree of the USSR State Statistics Committee dated December 28, 1989 No. 241 __________________________ +———-+ (enterprise, organization) OKUD code ¦ ¦ +———-+ +————+ CARD No. ¦ ¦ WAREHOUSE ACCOUNTING OF MATERIALS +————+ +———————————————————————+ ¦Warehouse¦ Place ¦Brand¦Grade¦Pro-¦Size- ¦Nomen- ¦ Unit ¦Price¦Norm ¦ ¦ ¦ storage ¦ ¦ ¦fil¦measure ¦clature-¦measurement¦ ¦stock¦ ¦ +————¦ ¦ ¦ ¦ ¦ny +———¦ ¦ ¦ ¦ ¦steel -¦cell-¦ ¦ ¦ ¦ ¦number ¦code¦nai- ¦ ¦ ¦ ¦ ¦lazh ¦ka ¦ ¦ ¦ ¦ ¦ ¦ ¦meno-¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ + ——+——+——+——+—-+—-+—-+——-+—+——+—-+——¦ 1 ¦ 2 ¦ 3 ¦ 4 ¦ 5 ¦ 6 ¦ 7 ¦ 8 ¦ 9 ¦ 10 ¦ 11 ¦ 12 ¦ +——¦ ¦ ¦ ¦ ¦ ¦ +——-+—¦ +—-¦ ¦ +————————————————— ——————+ +————————————————+ Name ¦ Precious metal ¦Line number¦ material _________ +————————————¦ in form ¦ ___________________ ¦ name ¦type¦weight, ¦ number ¦ No. |

Materials accounting card form M-17

Materials accounting card form M-17 (sample)

The standard intersectoral form M-17 was approved by Resolution of the State Statistics Committee of Russia dated October 30, 1997 N 71a.

However, starting from January 1, 2013, form M-17 (materials accounting card) can be developed by the organization independently, indicating in it all the mandatory details provided for in paragraph 2 of Art. 9 of the Law of December 6, 2011 No. 402-FZ. You need to consolidate this form in your accounting policy (Information of the Ministry of Finance of Russia N PZ-10/2012).

If the company decides to use the unified form M-17, the materials warehouse card must be modified taking into account the requirements for the mandatory details specified in paragraph 2 of Art. 9 of the Law of December 6, 2011 No. 402-FZ. The modified material accounting card M-17 must also be fixed in the accounting policy of the organization for accounting purposes (Information of the Ministry of Finance of Russia N PZ-10/2012).

Unified material warehouse card (form): you can download it from the link.

The need for a materials accounting card

Form M-17 was approved by the State Statistics Committee in resolution No. 71a dated October 30, 1997. Let us say right away that the form is not required to be used in the required form. You can make adjustments to its template. But if an enterprise decides to develop its own sample, then it is necessary to focus on the list of mandatory details for such forms. It is fixed by the Accounting Law No. 402-FZ in terms of regulating the content of primary documents (Article 9).

Mentions of how to keep a materials record card of form M-17 are in order No. 119n dated December 28, 2001, authored by the Ministry of Finance.

In essence, M-17 is a materials warehouse card. It reflects accounting data on inventories formed at the company’s storage facilities. The calculation includes all assets that the enterprise has and taking into account the resources of its structural divisions.

The division of values in accounting is carried out with reference to the distinctive features of assets:

- Name;

- quality mark;

- product model;

- varietal characteristics;

- dimensions;

- articles, etc.

The cards record not only the actual availability of inventory items, but also their release into production.

The transfer of material resources from warehouse premises, provided that the M-17 form has been drawn up, occurs on the basis of a limit-fence card. It is issued in a single copy and left in the custody of the recipient of the relevant valuables. He signs on the M-17 form, and the official issuing the goods and materials signs on the limit-fence card form.

Materials inventory book: form M-17

In addition to the M-17 card, to keep track of the movement of material assets, you can use the materials warehouse book (clause 54, clause 274 of the Order of the Ministry of Finance of the Russian Federation dated December 28, 2001 No. 119n).

In the warehouse accounting books, a separate personal account is opened for each item number, which contains the same details and is numbered in the same order as the material accounting cards. The sheets of the warehouse accounting book must be numbered, laced and certified by the signature of the chief accountant (or a person authorized by him) and a seal, if available (clause 274 of the Order of the Ministry of Finance of the Russian Federation dated December 28, 2001 No. 119n).

The unified form of the material inventory book M-17 was approved by Order of the Ministry of Finance of the Russian Federation dated December 30, 1999 No. 107n, which lost its force as of October 1, 2005 (Order of the Ministry of Finance of the Russian Federation dated September 29, 2004 No. 87n).

However, the company has the right to use this form of the materials accounting book, having modified it in accordance with the requirements for the mandatory details specified in clause 2 of Art. 9 of the Law of December 6, 2011 No. 402-FZ, and enshrining it in its accounting policies (Information of the Ministry of Finance of Russia N PZ-10/2012).

Materials warehouse card form

Wealth accounting cards are special forms of accounting documentation designed to reflect information about the movement of inventory in an organization. You can develop the form yourself or work using standardized forms. Let's figure out how to properly draw up accounting documentation.

ConsultantPlus FREE for 3 days

Get access

Law No. 402-FZ “On Accounting” provides for the right of economic entities to choose the forms of primary and accounting documentation. It is not necessary to use standardized forms.

It is permissible to develop your own formats or modify approved documents.

For example, supplement unified tables with sections and columns necessary to detail specific information about activities.

Each company makes its own decisions. What forms to work on must be specified in the accounting policy. Otherwise, controllers may have questions about documenting accounting.

To systematize information about inventory items, it is permissible to use the unified form M-17 “Material Warehouse Card”. The format of the M-17 form was approved by Resolution of the State Statistics Committee of Russia dated October 30, 1997 No. 71a.

Filling principles

The compilation of accounting cards should be carried out by an employee who is charged with such a duty. Responsibilities should be specified in job descriptions. The job description should not be a formal document hidden deep in the archives: the employee must read the document and sign confirming that he agrees with the wording.

Fill out accounting documentation based on the following requirements:

- Forms can be filled out by hand or on a computer. It is acceptable to use specialized programs for accounting.

- The organization's stamp on the card is not required - it refers to internal documentation.

- If errors are found in the form, corrections are made according to the general rules. An incorrect entry is crossed out with a thin line. The correct information is written next to it. The record is certified by the signature of the responsible person.

- The card is issued for one year. At the end of the period, a new form is filled out.

Documents from previous years must be submitted to the archives for safekeeping. The shelf life of accounting cards is at least 5 years.

Step-by-step instructions for filling out

Let's figure out how to fill out a materials accounting card. Step-by-step instructions for the M-17 form consist of 5 steps.

Step 1. Write down the number and date of the document.

Step 2. We indicate the name of the organization and enter the structural unit.

Step 3. Fill out the tabular part:

- column No. 1 - structural unit;

- column No. 2 - type of economic activity of the unit;

- column No. 3 - warehouse number;

- Column No. 4 and No. 5 - specifies the storage location of the material.

Then we indicate the characteristics of the accounting object. We register the brand, grade, profile, size and other information about the goods and materials. We enter the item number, unit of measurement, cost, price, inventory standard, expiration date and full name of the supplier. If there is no information, put a dash.

Step 4. The following table M-17 is information about the presence of precious metals or stones in the accounting asset. Fill in the appropriate positions in the table if the relevant information is available. Enter the data according to the passport of the tangible asset.

Step 5. The third table reflects information about the movement of inventory items within the organization. Fill in the information in the columns:

- “Record date” - enter the date of actual movement of the inventory asset;

- “Document number” - indicate the number of the primary document on the basis of which the movement is carried out - register the serial number of the operation;

- “From whom it was received or to whom it was issued” - enter the name of the organization or structural unit of the enterprise;

- Next, enter the unit of production of goods and materials;

- in the columns “Receipt”, “Expense” and “Balance” we write down the amount of goods and materials that were received, transferred or remain in storage. Records are recorded after each operation.

The last column is for the signature of the responsible employee. Be sure to indicate the date of the operation.

The completed warehouse accounting cards (sample M-17) are signed by the financially responsible person. Enter his position, full name, date of signing.

Exceptions for state employees

Public sector institutions operate according to different rules and regulations. State and municipal organizations are required to use primary accounting documents approved by Order No. 52n.

Warehouse accounting cards (form for public sector employees) have OKUD code 0504043. They are used to reflect information about goods and material assets stored in the institution’s warehouses. The form provides for the disclosure of information about the type of inventory items, their location (structural unit), their accounting value, supplier and other details.

The primary document must be completed by the responsible employee. For example, an accountant responsible for accounting for inventory items in an institution. The form is convenient to use for small volumes of valuables in storage, since for each asset you will have to create a separate sheet of the inventory card (material assets accounting card).

Form for a budget organization

Source: https://ppt.ru/forms/mat-otvetstvennost/kartochka-ucheta