In what cases are state fees paid?

A payment, called a state fee, is paid by the applicant when drawing up an application or request for legal action, the issuance of official documents registering or confirming the applicant’s status or authority.

| State duty is paid | When required |

| To magistrates, arbitration, constitutional judges | Submit an appeal, application, complaint, petition or request |

| To judges of general jurisdiction | The defendant requests a review of the judge's decision |

| To tax inspectors and other services | Obtain a certificate of registration of a legal entity, individual entrepreneur |

| Apply for termination of the existence of a legal entity or individual entrepreneur | |

| For copies of documents (charter), duplicate certificates |

State fees are paid to notaries for drawing up official documents, certifying copies, and confirming the personal signature of responsible persons. It can be paid at the place of circulation in cash, through a Sberbank cash desk, or in your personal account using electronic money.

Filling out the form

The application form for a duty refund was approved by Order of the Fiscal Department of the Russian Federation No. ММВ-7-8/ [email protected] dated 02/14/2017. The form consists of 2 sheets, information in which is entered with care. There is a separate cell for each symbol. Corrections and errors are not permitted.

Page 1

The title page of the application must contain the following information:

- Depending on the status of the payer, the TIN and KPP of the business entity are indicated (for individuals - TIN).

- Serial numbering of the application. If during the year the applicant applied for reimbursement of expenses several times, then the application number must correspond to the number of requests. If previously submitted applications turned out to be erroneous, then the request submitted later will have the next serial number.

- Code of the Federal Tax Service branch at the place of registration of the legal entity or individual.

- Name of the legal entity or full name of the citizen;

- An article of fiscal legislation is indicated that allows the return of money to the applicant (Article 333.40 of the Tax Code of the Russian Federation).

- The return code is indicated.

- Payment code. The number 2 should be indicated, since the fee is being refunded.

- Amount to be issued in rubles.

- Date of transfer of the duty to the state treasury.

- OKTMO code (required for individual entrepreneurs and legal entities).

- BCC of state collection (can be determined at the following link https://assistentus.ru/kbk/gosposhlina/).

- Number of sheets in the application along with attachments.

- Next, there must be a note from the management of the business entity stating that the information indicated in the application is reliable. Indicate your full name, telephone number, signature and date of certification of the document.

A sample of the completed form is presented below.

Page 2

On the next page you will need to indicate:

- TIN, KPP of the business entity.

- The name of the banking institution to which the amount to be reimbursed is planned to be transferred.

- Type of bank account (current).

- Correspondent account.

- BIC.

- Details (ownership and account number).

- Name of the business entity or full name of the citizen.

Who pays the state duty?

An ordinary citizen on his own behalf, an individual entrepreneur, or a legal entity of any legal form can pay the state duty. Confirmation of the fact of payment of the state duty will be an official receipt of the established form or a payment order with a bank seal confirming the execution of the payment.

If there is more than one payer, then payment is made by all participants in the transaction in equal shares. State duty is not paid by legal entities or private citizens if they are exempt from encumbrance by law.

Individuals pay state duty when:

- Submitting documents for opening an individual entrepreneur, LLC, JSC;

- Requesting information about the status in the all-Russian unified register;

- Using the term “Russia” in their names;

- Cases of termination of business activities of a businessman.

Legal entities or their official representatives additionally apply to courts of any instance, arbitration or constitutional, while paying a state fee. Also, it is required to pay for the actions of government services to issue permits, licenses, tests or approbations.

| ★ Best-selling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8,000 books purchased |

How to return previously paid state duty from the tax office

To return the state fee, the person who paid it must submit an application for a refund within three years following the payment.

The submitted application must be addressed to the government department that is authorized to provide the services you paid for.

However, before taking the application to the required address, you need to collect additional papers that will confirm your right to carry out the procedure:

- if you want to return the entire amount, then you must attach a copy of the check or receipt received for payment of the duty to your application;

- If you are claiming a refund of only part of the specified amount, then you must also provide a copy of the payment form.

Provided that your request for a refund is satisfied, the refund will be made one month from the date of application and submission of documents.

Read more: What issues do local governments decide?

When does the Federal Tax Service return the paid state duty?

Not in every case the Federal Tax Service returns funds. It is required to draw up an application requesting a refund of the state duty in full or in part. Confirmation of payment of the state fee must be attached to the application. According to the Tax Code of the Russian Federation, Article 333.40 contains cases of refund of overpayment in full or in part:

- After payment, the payer did not perform any actions or requests;

- Payment was made in a larger amount than required (in case of property disputes, technical error);

- The proceedings on the claim/case were terminated or left without consideration;

- The appeal/petition was returned to the payer/respondent;

- The application for the procedure for registering intellectual property (computer database) was withdrawn;

- The applicant was refused a Russian passport or refugee certificate.

If the parties have signed a settlement agreement, the legislative act allows the payer to return 50% of the paid duty. Also, the payer has the opportunity to offset the resulting overpayment against future payments for similar registration actions. The refund is carried out if the payer submitted an application before the three-year period for the return of overpaid payments has expired.

Other formalities

The application must be submitted in the manner prescribed by law. It has a number of features that are important to consider. The applicant needs to study the reasons for sending the document and fill out the appropriate form.

Features of the procedure

People, when contacting various government agencies, are often not aware of the benefits provided for paying state fees. After depositing funds, they find out that the money could not have been paid.

Over the course of three years, it is possible to return the funds paid. Documentary confirmation of status is not required. The Federal Tax Service or the court independently sends a request for a decision to be made.

The return procedure is reflected in the Tax Code of the Russian Federation.

Article 333.40 states that it is possible to return funds if:

- overpayment;

- lack of legal action;

- failure of a person to appear at the tax authority;

- refusal to provide services by the institution;

- refusal to complete the procedure by the user.

In this case, funds will not be returned to pay for the services of the Civil Registration Authority or for filing an application through the State Services portal. Refunds are made upon submission of an application to the tax authorities.

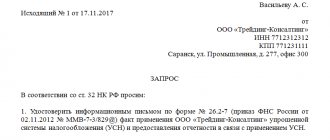

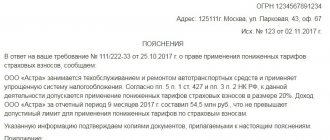

Application form for refund of state duty to the tax office

Comments on the standards

The law identifies six grounds for the return of state duty.

You can get a partial or full refund if:

- excessive payment;

- failure to act by an official at the request of the payer;

- termination of administrative proceedings;

- refusal of persons to take legal action;

- refusal to issue a passport of a citizen of the Russian Federation;

- withdrawal of an application for registration of an intellectual property object.

If the arbitration makes a decision on an amicable agreement between the parties, then half of the paid fee may be refunded. A similar rule applies to the conclusion of a settlement during the execution of a decision.

Refunds will not be available when paying for services by:

- marriage registration;

- dissolution of marital relations;

- name change;

- correction of civil status records.

It is necessary to submit an application to those authorities where it was planned to perform legally significant actions. You can confirm your right to return using payment documents. The decision is made by the body that must conduct the procedure. The refund is carried out by the Federal Treasury.

It will not be possible to return funds if a citizen is refused registration of ownership of real estate. If it is terminated, a refund of half of the funds paid may be possible.

The payer is given the right to offset the overpaid amount for future procedures. The offset is made on the basis of an application to the authorized body.

An application for a refund of state duty must be submitted to the tax office within three years after payment.

You need to attach to it:

- the court's decision;

- court certificate;

- documentary evidence of the circumstances for the return;

- receipts and payment orders.

Reasons for the request

Article 333.40 of the Tax Code of the Russian Federation states the grounds for the return of state duty:

- You can return funds if you collect them in a larger amount than required by tax legislation. The reasons for overpayment are not taken into account, even if a technical failure occurred.

- A refund can be made if the person’s application is refused. In this case, it is allowed to count the funds towards payment when applying again.

- The procedure is carried out when judicial proceedings are terminated or they are not considered by the courts. If a settlement agreement is concluded, half of the deposited amount is returned.

- A person can independently refuse to consider an appeal. In this case, the state duty is refundable.

- Refusals to issue a passport of a citizen of the Russian Federation are accompanied by compensation for the state fee.

- A refund is provided when the claim is sent to another court (incorrect jurisdiction or territorial determination) with advance payment of the state fee. Funds can be credited when contacting the required authority.

Form and order of submission

The application form for a refund of state duty is not provided for at the legislative level. Therefore, the document is drawn up by the applicant at his own discretion.

It is important that he notes in the text:

- name of the judicial authority;

- personal data (last name, first name, patronymic, passport series and number, address and contact information);

- the fact of payment of the state fee (date, amount, legally significant event for which funds were paid, nature of the actions);

- grounds for making a refund (articles of the Tax Code of the Russian Federation);

- a request to the judicial authority to return the overpaid funds and issue a certificate for submission to the Federal Tax Service;

- attachments (documents confirming payment: receipts, copies of a court decision on the return of the application, refusal to accept);

- date of compilation.

At the end of the document, the citizen confirms the above with a signature.

If a person applies to a judicial authority, the application is created in a similar way. It does not matter the type of institution (arbitration, magistrate, district court) to which the filing is made.

The serving order is also identical in both situations. If you refuse to perform a legally significant action and pay the state fee, the document makes a decision on the absence of a petition from the person in the consideration of the case. With a court certificate, you can get a refund of the amount.

The application to the judicial authority can be submitted personally by the applicant when contacting the office. In this case, the form will be marked with the date of receipt, position and details of the person who accepted the application and signature.

The referral is also made by mail. Then a registered letter is prepared with a description of the attachment. The fact of sending is confirmed by a notification of delivery. When applying to the arbitration court, the option of filing through the “My Arbitrator” service is possible. This makes the return process much easier.

Sample of filling out an application for refund of state duty to the tax office

Reasons for refusal to refund the state duty

There are certain conditions when a refund of state duty is not allowed. The return procedure is not possible if you paid for:

- To carry out actions in the registry office (conclusion/divorce, on a child’s birth certificate, change of name, surname);

- During the lawsuit, the defendant voluntarily admitted and satisfied all the plaintiff’s claims;

- State bodies refused to apply to the Rosregister for registration of rights to property;

- In the process of testing, analyzing, and stamping jewelry or precious metals.

A refusal will follow if the application with the corresponding request is received after the three-year period in which they apply for the return of money from the budget has expired. Also, it is necessary to indicate the reason why the payer insists on refunding the state duty.

Application for refund of state duty (sample)

1) payment of state duty in a larger amount than provided for in this chapter;

2) return of an application, complaint or other appeal or refusal to accept them by the courts or refusal to perform notarial acts by authorized bodies and (or) officials. If the state duty is not returned, its amount is counted towards the payment of the state duty when a claim or administrative claim is filed again, unless the three-year period has expired from the date of the previous decision and the original document on payment of the state duty is attached to the repeated claim or administrative claim;

(Clause 2 as amended by Federal Law dated 03/08/2015 N 23-FZ)

(see text in previous)

3) termination of proceedings in the case (administrative case) or leaving the application (administrative claim) without consideration by the Supreme Court of the Russian Federation, courts of general jurisdiction or arbitration courts.

When concluding a settlement agreement before a decision is made by the Supreme Court of the Russian Federation or arbitration courts, 50 percent of the amount of the state duty paid by him shall be returned to the plaintiff. This provision does not apply if the settlement agreement is concluded during the execution of a judicial act.

The paid state fee is not subject to refund if the defendant (administrative defendant) voluntarily satisfies the demands of the plaintiff (administrative plaintiff) after the said plaintiffs appeal to the Supreme Court of the Russian Federation, an arbitration court and a ruling is made on accepting the statement of claim (administrative statement of claim) for proceedings, as well as when approval of a settlement agreement, reconciliation agreement by the Supreme Court of the Russian Federation, a court of general jurisdiction;

(Clause 3 as amended by Federal Law dated 03/08/2015 N 23-FZ)

4) refusal of persons who have paid the state duty to perform a legally significant action before contacting the authorized body (official) performing this legally significant action;

5) refusal to issue a passport of a citizen of the Russian Federation for leaving the Russian Federation and entering the Russian Federation, certifying in cases provided for by law, the identity of a citizen of the Russian Federation outside the territory of the Russian Federation and on the territory of the Russian Federation, a refugee travel document;

6) sending the applicant a notice of acceptance of his application to withdraw the application for state registration of a computer program, database and topology of an integrated circuit before the date of registration (in relation to the state fee provided for in paragraph 1 of Article 330.30 of this Code).

(pp.

6 introduced by Federal Law of December 27, 2009 N 374-FZ)

2. The state fee paid for the state registration of marriage, divorce, name change, corrections and (or) changes in the civil status record is not refundable, if the state registration of the corresponding civil status act was not subsequently carried out or corrections and changes were made to civil registration records.

(as amended by Federal Law dated December 27, 2009 N 374-FZ)

3. An application for the return of an overpaid (collected) amount of state duty is submitted by the payer of the state duty to the body (official) authorized to perform legally significant actions for which the state duty was paid (collected).

The application for the return of an overpaid (collected) amount of state duty shall be accompanied by original payment documents if the state duty is subject to full refund, and if it is subject to partial refund, copies of the specified payment documents.

The decision to return to the payer the overpaid (collected) amount of state duty is made by the body (official) carrying out the actions for which the state duty was paid (collected).

The refund of the overpaid (collected) amount of state duty is carried out by the Federal Treasury.

An application for the return of an overpaid (collected) amount of state duty in cases heard in courts, as well as by magistrates, is submitted by the payer of the state duty to the tax authority at the location of the court in which the case was heard.

Decisions, rulings or certificates from courts about the circumstances that are the basis for a full or partial refund of the overpaid (collected) amount of state duty, as well as original payment documents if the state duty is subject to refund in full, and if it is subject to partial refund - copies specified payment documents.

(edited)

Federal laws dated June 28, 2014 N 198-FZ, dated November 30, 2016 N 401-FZ)

An application for the return of an overpaid (collected) amount of state duty may be submitted within three years from the date of payment of the specified amount.

Refund of the overpaid (collected) amount of state duty is made within one month from the date of filing the specified application for refund.

(as amended by Federal Law dated July 27, 2006 N 137-FZ)

(Clause 3 as amended by Federal Law dated December 31, 2005 N 201-FZ)

4. The state fee paid for state registration of rights, restrictions (encumbrances) of rights to real estate, transactions with it is not refundable in the event of refusal of state registration.

Upon termination of the state registration of a right, restriction (encumbrance) of a right to real estate, a transaction with it, on the basis of relevant statements of the parties to the agreement, half of the paid state duty is returned.

5. Lost force on January 1, 2007. — Federal Law of July 27, 2006 N 137-FZ.

6. The payer of the state duty has the right to offset the overpaid (collected) amount of the state duty against the amount of the state duty payable for performing a similar action.

This offset is made upon the payer’s application submitted to the authorized body (official) to which he applied to perform a legally significant action. An application for offset of the amount of overpaid (collected) state duty may be filed within three years from the date of the relevant court decision on the return of the state duty from the budget or from the date of payment of this amount to the budget.

The application for offset of the amount of overpaid (collected) state duty shall be accompanied by: decisions, rulings and certificates of courts, bodies and (or) officials carrying out actions for which the state duty is paid, on the circumstances that are the basis for a full refund of the state duty, and also payment orders or receipts with a genuine bank mark confirming payment of the state duty.

7. Refund or offset of overpaid (collected) amounts of state duty is carried out in the manner established by Chapter 12 of this Code.

8. The state duty paid for the testing, analysis and branding of jewelry and other products made of precious metals is not refundable if such products are returned in an unbranded form on the grounds provided for by the legislation of the Russian Federation.

(Clause 8 introduced by Federal Law dated 02.05.2015 N 112-FZ)

To the Kirovsky District Court of Yekaterinburg Applicant: Seleznev Viktor Gennadievich, address: 620075, Yekaterinburg, st. Kommunarov, 155

Cases when the state duty can be returned are established by the Tax Code:

- The plaintiff refused to file a statement of claim in court, but he had already paid the state duty. For example, when a civil dispute is resolved by the parties independently or in pre-trial proceedings;

- the court made a decision to return the statement of claim or refuse to accept the claim for proceedings (Articles 134, 135 of the Code of Civil Procedure);

- a ruling was made to terminate the case in accordance with Art. 220 Code of Civil Procedure of the Russian Federation;

- the plaintiff paid a larger amount of state duty than required (due to an incorrect calculation of the cost of the claim or a reduction in the size of the claim). This basis will also apply when the plaintiff has already filed a claim in court, but then changes his mind. Such a refusal must be accepted by the court and formalized in the form of an appropriate ruling.

If a settlement agreement is concluded between the parties during the consideration of the case, the court makes a decision to refuse to satisfy the plaintiff’s claims or any of its parts, the state fee is not refunded. The same is the case when the claim was accepted for proceedings, and then the defendant satisfied the plaintiff’s demands.

Having established the presence of one of the above grounds for a refund of state duty, prepare a corresponding application in writing. It is filed in the same court that accepted the claim for proceedings, or where the plaintiff was going to apply according to the rules of jurisdiction and jurisdiction.

Such an application can be submitted before the expiration of 3 years from the date on which grounds for a refund of the state duty arose. The application sets out the circumstances of the legality of the requirements for the return of state duty (grounds), which are supported by documents: a procedural act (court ruling) is attached to the application.

Since the refund of the state duty will be made by the tax authority, in the text of the application it is necessary to ask the court to provide a certificate for such an authority.

The court will consider the applicant's claim on its own, without summons. The decision is made, as a rule, within 5 days and is formalized by an appropriate determination. It will come into force in 15 days, after which you can receive a determination and a certificate for the tax office. The refund of the state duty will be made within 30 days.

How to correctly file an application for a duty refund

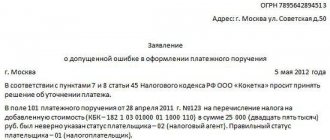

If the taxpayer applied to the fiscal service, then the Federal Tax Service considers the application. Care must be taken when drafting a written request. It is important to correctly indicate the reason why the payer requires the return of funds. In the case where there was a technical error, i.e. a typo in the recipient's details (KBK, name of the payer, recipient or incorrect indication of bank details) this should be indicated in the basis of the application.

Among the mandatory details in the return application, you must indicate:

- Name of the Federal Tax Service department;

- Service location address;

- Name of the organization, full name of the applicant or individual entrepreneur on whose behalf the application was written;

- Grounds for refund of state duty;

- BCC and date of payment of the fee;

- OKTMO and the amount paid by the applicant;

- The amount that is required to be returned to the payer;

- Bank account details where you want to transfer the fee.

Date and personal signature of the applicant. If the payer is an individual, you will need to indicate the payer's TIN. When indicating the reason for which the fee is being returned, you should refer to the provided confirmation of payment (receipts, payment orders) and supporting documents. In various situations, this may be a written confirmation that the applicant did not apply (after paying a fee) for the service or action.

Results

The state duty paid to the budget on the grounds prescribed in Art. 333.40 of the Tax Code of the Russian Federation, the taxpayer has the right to return from the budget. To do this, he needs to send to the Federal Tax Service an application drawn up in the prescribed form for the return of the state duty within 3 years from the date of payment of the duty.

You can find other useful information about state duties in the following materials:

Provided that you have paid a state fee for the provision of any service to you, but for some reason you need to return this fee, you need to contact the Federal Tax Service for help. However, you need to understand that this procedure is accompanied by many difficult nuances. In particular, it is necessary to fill out an application for the return of state duty to the tax office. We will consider a sample filling below.

Application for refund of state duty to the tax office: sample

Who may not pay the state fee

In particular, the state fee is not charged to the plaintiff when filing applications or claims in labor disputes. State-owned organizations receive exemption from paying fees for using the term “Russia” and other combinations of words formed on this form. Federal and regional government structures are also exempt from paying all types of state duties.

The following actions are exempt from payment if the following actions are taken to court:

- Filing complaints against the actions of bailiffs;

- Appeal to court actions;

- Application for deferment or modification of a court decision.

Also, no state duty is charged for the issuance of documents in criminal cases or collection under writs of execution.

Some transactions with real estate are not subject to payment of state duty upon state registration:

- The right to manage property owned by municipal authorities;

- For the indefinite use of land plots owned by the municipality;

- Entry into the unified register of transactions for the right to own real estate due to changes in legislation;

- If the information in the state register is clarified by submitting an application for state registration of property rights.

If an error was made by employees of the institutions when performing state registration operations, the correction is made without additional payment of the state fee from the applicant.

Procedure for individuals and legal entities

The application is written to the Federal Tax Service at the location of the applicant. In the header of the document, you must indicate not only your data, but also in whose name it was drawn up (full name of the head of the inspection). The application is not handed to the management itself, but is submitted to the office.

Attention! Do not forget to indicate the correct account details for a refund in your application.

Application form to the tax office for tax refund under 3-NDFL 2018

Do I need to pay tax when donating an apartment?

How to make an application for a refund from the tax office, read the link: https://potreb-prava.com/dokumenty/pretenzionnyj-poryadok/zayavleniya/obrazec-zayavleniya-na-vozvrat-denezhnyx-sredstv-iz-nalogovoj-2018. html

If you plan to return the state fee paid in connection with the trial, then an application for a refund must be submitted to the Federal Tax Service, to which the court where the case is being heard is located.

When submitting an application for a refund of mandatory payments on behalf of individuals, there are a number of features:

- the application is drawn up in your own hand, indicating passport data, reasons for return, account details, contact phone number;

- The application is accompanied by the original receipt, if a full refund is planned, a photocopy, if a partial one, a photocopy of the passport or birth certificate (if the fee is paid by minors).

How to take into account state duty in accounting

To easily write off the state duty paid as an expense when accounting for income tax, the reason for its occurrence should be taken into account. It could be:

- When considering a case in court;

- At the time of acquisition of property or rights to it;

- Actions related to the main activity.

The costs of paying fees that were paid for operations with the main activity (product certification, licensing of activities) are taken into account as the main costs collected in accounts: 08, 10, 20, 26, 41 by debit and credited with account 68. In other situations, all such costs are recorded as non-operating costs. These include notarial operations for certification or preparation of documentation, powers of attorney, agreements.

Most taxpayers have a question. Is it possible to take into account the fees paid at the time of registration of a legal entity? In this case, the legislation establishes that expenses may include expenses that were incurred after the date of entry into the unified register of organizations or entrepreneurs.

What is state duty

State duty is a monetary payment provided by a citizen of the Russian Federation to the country's budget. The required payment is collected from the citizen only if he applies:

- to one of the government departments;

- to officials who have the authority to carry out various legally significant procedures.

The payer of the payment we are interested in in favor of the state can be various entities. Let's look at them in more detail in the table below.

Table 1. Who can become a state duty payer

| Payer's name | Description |

| Individual | An individual is an individual person, a citizen of our or another country, who acts as a subject of civil law. |

| Entity | A legal entity is any organization that owns property of a separate type and is responsible for any obligations assumed with this property. A legal entity has the following rights:

|

| Individual entrepreneur | An individual entrepreneur, simply put, is at the same time:

|

All entities listed in the table above have the right to a refund of previously paid state duty if all the necessary conditions for this are met and the circumstances also correspond to this.

Paying stamp duty, which you will potentially want to pay back in the future if something goes wrong, comes in many cases. The mentioned cases can be divided into two categories.

Table 2. Categories of actual cases of payment of state duty

| Happening | Description |

| Payment for any legally significant services | This category includes administrative type procedures, such as:

|

| Legal costs | Provided that you were one of the parties to the court hearing, you are required to pay court costs, provided that the decision was not made in your favor. |

On what grounds are state fees refunded?

Similar grounds are voiced in the country's Tax Code. These include the following situations:

- If you deposit more money than was necessary, the excess is transferred back to the payer, even if such a situation arose due to technical problems during the payment.

- When they refuse to consider a person’s appeal, even if it is due to the fault of the citizen who applied, the funds can be counted if the person applies again for a similar service.

- If the legal proceedings are terminated or have not even begun, the money will be returned, and when a settlement agreement is signed, only half of the amount will be returned.

- If the applicant independently refuses the proposed service, the state fee is also paid.

- The funds will also be returned if a passport is refused to a foreign citizen who has applied for a Russian-style identity card.

- If the plaintiff initially incorrectly determined the jurisdiction or chose the wrong territorial division of the court, and he wants to send the claim to another branch, he must first return the fee or count it against a new application.

There are other nuances of filing an application that should be kept in mind when preparing it. Qualified lawyers will tell you about them. They will also help with the development of the application.

Free initial consultation with a lawyer Let's look at your legal situation or question. We'll tell you what to do next. Call - it's free:

- For residents of Moscow and Moscow Region:

- Other regions of Russia:

Also write to us via online chat or form on the website.

As an advertisement