Citizens of the Russian Federation are often faced with the need to submit a tax return in Form 3-NDFL to the tax authority to confirm their income and important expenses, in order to pay income tax or property collection, or, on the contrary, to issue a tax deduction due in accordance with the state subsidy program. In all cases, the data provided is subject to a desk audit by the tax authorities, on the basis of which questions may arise that require clarification.

In what cases can the tax office request explanations?

Inspectors of the Federal Tax Service are ordinary people who act in accordance with the regulations entrusted to them when conducting desk processing of incoming data from taxpayers. They may have questions in the following cases:

- Due to the fact that the declaration is only a confirmation of the events that occurred in the life of the taxpayer during the reporting period in terms of his receipt of one or another type of one-time or periodic income, most often the tax authorities have their own information regarding the individual, obtained from various competent sources.

Over the course of 90 days of a desk audit, this information is verified with the information presented in the report, which does not always coincide with each other. If such inconsistencies are discovered, inspectors will immediately send a letter demanding explanations regarding the discrepancies that have arisen.

- Explanation is also required when the clarifying document is presented with a tax amount reduced in relation to the original 3-NDFL declaration.

- Inspectors pay special attention to those indicators that, based on the results of submitting a declaration and calculating the tax, show not the person’s profits, but the losses incurred by him, which, if the data is correct, completely exempts him from paying tax. Therefore, the applicant must understand how to explain the reduced amount of tax payable.

- An explanation to the tax office about a zero declaration under the simplified taxation system (simplified taxation system) is required in maximum completeness with the balance sheets, since the lack of a taxable base always raises many questions among regulatory authorities. A sample explanatory note to a tax return under the simplified tax system can be viewed on the website www.nalog.ru.

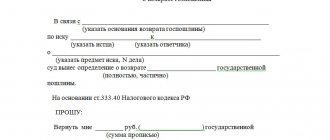

Important! How to write a letter to the tax office for clarification, sample. The letter is drawn up in the classic form on a blank A4 sheet, in printed (preferably) or handwritten form in compliance with the regulations for conducting official correspondence and can be drawn up by both an individual and a legal entity.

Sample explanatory note to the Federal Tax Service

Despite the fact that administrative measures for missing deadlines are not provided in this case, all explanations should be provided as soon as possible in order to avoid postponing the overall period for consideration of the declaration.

Suspicious losses

Income tax raises many questions for the Federal Tax Service, especially if the declaration shows a loss instead of profit. If the loss is one-time in nature, it usually does not attract the attention of regulatory authorities. But in case of permanent losses, the organization should expect quarterly requests from the Federal Tax Service. Such results of commercial activity seem suspicious to tax authorities, especially if the company does not intend to begin bankruptcy proceedings.

Factors influencing the unprofitability of an enterprise can be very different. In most cases, this is due to a high share of non-operating expenses not related to making a profit. For example, an organization has a large amount of overdue accounts receivable and is required by law to create a reserve, the amounts of which are included in non-operating expenses.

The explanatory note to the tax office on the claim for losses must contain explanations about the reasons for the excess of expenses over income. If the results were influenced by macroeconomic factors, it should be written that the company is unable to change the economic situation in the region, the exchange rate, inflation rate, etc. At the same time, it is advisable to promise to optimize costs in the near future.

We must remember that the company is suspected of illegal actions and has the right to summon management to a commission if the answer is not sufficiently substantiated. Explanations are written in free form.

Source

Actions of the taxpayer upon receipt of requests for clarification from the Federal Tax Service

In all cases, the taxpayer must accept the request for consideration, determine for himself the nature of the issues raised, draw up his action plan and provide an adjusted version of the package of documents, which may contain:

- Corrected declaration 3-NDFL under the number of the corresponding adjustment at the top of the title page of the document.

- Supplemented supporting documentation in the form of a certificate of income in form 2-NDFL, contracts for the sale of registered movable or immovable property with profit and the tax base formed as a result of these actions. This also includes missing papers confirming the person’s expenses for treatment, education or residential real estate, which are proven by checks, cash orders or documents confirming payments on a mortgage or other targeted loan. Legal entities in this case should pay special attention to income tax and VAT with the formation of an evidence base.

Persons reporting under the simplified system must provide documentation of advance income tax for each quarter, otherwise, the simplified person risks being transferred to a full-fledged taxation system

The response to the request for clarification on property tax must be completed with certificates of ownership and cadastral documents for the property submitted for reporting. If a person belongs to the category of those applying for benefits, this must also be indicated in the explanations.

- Covering letter with explanations according to the form established at the level of tax legislation.

These documents are drawn up in a single set and submitted together with an explanatory note for re-inspection to the tax authority.

Explanation for checking sample

In what cases are documents required? When receiving a request to submit documents, you need to know that tax authorities have the right to request materials only during an on-site or desk audit. Requirements of this kind include:

- counter checks;

- identified discrepancies in reporting;

- application of tax benefits by the company;

- carrying out tax control activities.

In other cases, the organization is not required to provide documents and may directly indicate this circumstance in its response. An explanatory note to the tax office on the request to provide documents is drawn up depending on the nature of the information. But, in any case, copies of the requested materials must be attached to such a note. How are applications designed? The preparation of evidence must be strictly within the law. The tax office may require an explanation of the reason for the discrepancy in the amounts of accrued, withheld and paid personal income tax by an employee, either if errors were identified when submitting a deduction, or when the amount of personal income tax paid in the current year is less than the personal income tax of the previous year. filling out an explanatory note on personal income tax Explanatory note on the simplified tax system declaration The requirement to provide explanations on the simplified tax system declaration is mainly due to discrepancies in the data on the amount of income in the report with the receipts in the organization's current account. Tax authorities currently have access to the current account of an organization or entrepreneur. And in cases where the results in the inspection and the results in the declaration diverge, this requires explanation. An example of an explanatory note to the tax office upon request in this case could be a reasoned reference to different principles of reporting and accounting. Suspicious losses Income tax raises many questions for the Federal Tax Service, especially if instead of profit in the declaration there is a loss. If the loss is one-time in nature, it usually does not attract the attention of regulatory authorities. But in case of permanent losses, the organization should expect quarterly requests from the Federal Tax Service. Such results of commercial activity seem suspicious to tax authorities, especially if the company does not intend to begin bankruptcy proceedings. Factors influencing the unprofitability of an enterprise can be very different. In most cases, this is due to a high share of non-operating expenses not related to making a profit.

How to write an explanation in response to a notification to the tax office - sample

The letter must necessarily contain the following information:

- In the header of the document, in the upper right corner, you must write an appeal in the form: “To the Head of the Federal Tax Service No. (code of the inspectorate to which the taxpayer is assigned) for the city (city and region of location of the tax service department) from (hereinafter - or passport details of the individual indicating place of permanent registration or name and all details of a legal entity or individual entrepreneur).

- After filling out your personal information in the header, you need to write the heading “Explanations” in the middle of the sheet, after which you should expand the subject of the letter.

- After the heading, the contents of the letter are written, which reveals the essence of the explanations in the form of a list of factors confirming the data presented for consideration in its original form. If a person admits a mistake, he must also record this in part, which corrected documents were provided and where exactly the corrections were made. If several explanations need to be provided in a letter, they are compiled in the form of a numbered or unnumbered list.

- After the main part of the document, it is necessary to give the second heading “Appendices”, and then provide a list of the names of the attached copies of documents that confirm the accuracy of the corrected information.

- The explanatory note is sealed with the signature of its compiler or the head of the legal entity, after which the date of preparation is indicated. The date, month and year in this letter are a very important addition, since they show the taxpayer’s compliance with regulatory deadlines in case the audit period is delayed. Document code 1777 explanatory note sample to the tax office can be seen on many sites where people post them based on experience in writing such documents previously.

Consequences of ignoring tax requirements

If neither after 5 nor after 15 working days the inspection receives a letter of explanation from an individual, individual entrepreneur or legal entity, the following penalties may be applied to him:

- Imposition of a fine in the amount of 5,000 rubles if this situation occurred for the first time in the history of relations with the taxpayer.

- Penalties in the amount of 20,000 rubles when a person has been repeatedly found to have failed to comply with the legal requirements of the Federal Tax Service inspection.

- In the event of a total lack of any reaction on the part of the taxpayer, including failure to pay a fine, the inspectorate reserves the right to apply to the judicial authorities with a statement against the person and oblige him to fulfill all requirements through a court decision.

Important! If a request comes from the tax office, and the taxpayer accepts it, then he is obliged, even if not in compliance with all regulatory deadlines, to respond to it.

Simplified taxation system

Only legal entities can be subject to these types of penalties. This is due to the fact that when a company is self-supporting, it must involve professionals in tax matters, and in the case of a citizen, this is not at all necessary, since he has a completely different interest, and providing documents to the tax office is only a one-time need for him.

In conclusion, it should be said that when starting relationships and document flow with the tax authorities, it is better to complete all questions and provide the necessary explanations, especially considering that they are mostly legal and justified. This will further save the taxpayer from many troubles with the bureaucratic machine of our state.

If you received a letter from the tax office demanding clarification, this means that the tax authorities did not like something in the reports you submitted. The fact is that the Federal Tax Service carries out a desk audit of all received declarations and financial statements automatically. And if errors are identified in the reporting (contradictions between the information in the submitted documents, discrepancies between the submitted information and the information available to the tax authority), the Federal Tax Service will require the submission of appropriate explanations (clause 3 of Article 88 of the Tax Code of the Russian Federation).

In addition, tax authorities have the right to request clarification during a desk audit of a declaration in which losses are declared. And, as a rule, explanations are actually requested for each such declaration.

If you have submitted an updated declaration, in which the amount of tax payable to the budget is reduced compared to the amount declared in the initial declaration, then the tax authorities have the right to request explanations justifying the change in indicators (clause 3 of Article 88 of the Tax Code of the Russian Federation).

Explanations during the desk audit

To submit explanations, you have 5 working days from the date of receipt of the request from the tax office (clause 3 of Article 88 of the Tax Code of the Russian Federation). If you do not provide an explanation, you will face a fine of 5,000 rubles. (Clause 1 of Article 129.1 of the Tax Code of the Russian Federation).

If you decide that there are errors in the reporting you submitted, instead of explanations, you can submit an updated tax return (calculation). And in this case, there will certainly be no fine for failure to provide explanations.

You can submit clarifications to the tax office:

- or by submitting it in person through the office;

- or by sending a letter by mail with a list of the contents;

- or by sending via TKS.

As for the explanations for VAT, if you are required to submit a declaration for this tax in electronic form, you must also submit explanations exclusively electronically - explanations on paper will not be taken into account by the tax authorities (clause 3 of Article 88 of the Tax Code of the Russian Federation).

Established deadlines and features of requesting documents

The legislation establishes a clear period during which it is necessary to collect documents and prepare a response to the request of the Federal Tax Service.

Papers need to be provided:

- within 5 days, if you need information about a specific transaction concluded by the object of inspection;

- within 5 working days, if you need to provide explanations regarding the corrected and updated declaration, if a desk tax audit is being conducted;

- within 10 working days, if the person is the subject of an inspection and a corresponding requirement has been made against him.

In practice, there may be objective reasons preventing the provision of information. In this situation, it is acceptable to submit a request for a deferment. The procedure must be completed no later than 24 hours from the date of receipt of the request. To complete the procedure, you will need to prepare a notification and send it to the tax authority. The document must reflect a list of reasons preventing the provision of documentation on time. Additionally, you are required to indicate within what period of time you will be able to satisfy the requirements and provide documents. When the notification is received, the tax service will review it and make a decision within 2 days.

Video

How to correctly write an explanation to the tax office

Explanations at the Federal Tax Service are drawn up in any form, with the exception of explanations during a desk audit of a VAT return (you will read about this below).

If, in your opinion, there are no errors, inaccuracies or contradictions in the submitted reports, then indicate so in the explanations:

“In response to the request from XX.XX.XXXX No. XX, we inform you that the declaration for such and such a tax for such and such a period does not contain errors. In this regard, there are no grounds for making corrections to the declaration for the specified period.”

If you discover that you actually made a mistake in the submitted return, but this mistake does not entail an understatement of tax (for example, a technical error when specifying a code), then in response to the tax office’s request for explanations, you can:

- or indicate in the explanations that they made a mistake, that the correct option is such and such, but such a mistake did not result in an understatement of the tax base or the amount of tax payable;

- or submit an updated declaration.

But if there is an error in the declaration that results in an underestimation of tax, you need to submit an updated declaration as quickly as possible. In this situation, it is pointless to submit explanations (clause 1 of Article 81 of the Tax Code of the Russian Federation; Letter of the Federal Tax Service dated November 6, 2015 No. ED-4-15/19395).

Explanation to the tax office regarding losses

The attention of tax authorities will be drawn to losses incurred over 2 or more years. In response to a request for reasons for losses, you can send a letter of explanation to the tax office, justifying in it why expenses exceed income. For example, an organization has recently been registered, there are still few clients, but the costs of renting premises, maintaining staff, etc. are already significant. In your explanations, emphasize that all expenses are economically justified and documented. You can prepare a table indicating the main types of expenses and their amount per year by type. Below is an explanatory note to the tax office regarding losses (sample).

Sample explanation of insurance contributions to the tax office.

The company independently generates explanations, without relying on an established template, since it is not regulated by tax legislation. We invite you to submit clarifications to the tax office on questions regarding insurance premiums.

Below is a sample explanation to the tax office regarding insurance premiums:

When forming it, you must adhere to the following scheme for filling out the document:

- in the upper right corner indicate the name of the addressee - the tax office, whose request is being explained;

- indicate the full details of the company (if the document is not drawn up on letterhead), otherwise it is enough to provide brief details;

- below, enter the outgoing document data - date and number;

- record the details of the requirement for which an explanation is given;

- provide detailed explanations on the questions asked by the tax inspectorate, indicating legal norms (if possible). This section must be filled out not only from the descriptive side, but also add to it a list of documents confirming certain points;

- affix signatures and full names of officials.

You can fill out explanations on insurance contributions to the tax office using this link.

Explanation to the tax office about discrepancies in declarations

Tax authorities can compare the data from one declaration (for example, for VAT) with the data for another declaration (for example, for income tax) or with financial statements. And ask to explain the reason for the discrepancies between similar indicators (in particular, revenue).

It is easy to justify such discrepancies. After all, accounting rules differ from tax accounting rules. And the procedure for determining the tax base for different taxes has its own characteristics.

For example, the tax base for VAT may not coincide with the amount of income in the profit declaration, since some non-operating income is not subject to VAT (penalties, dividends, exchange rate differences) (Article 250 of the Tax Code of the Russian Federation).

Justified differences

However, they must be included in other income and expenses for income tax purposes. In this regard, there are no errors in the declaration, and the taxpayer in an explanatory note to the tax office upon request, a sample of which can be easily found in Internet resources, simply needs to indicate this circumstance, referring to an article of the tax code. There is no need to submit updated declarations in such cases.

We often receive requests about discrepancies between the financial results statement and the income tax return. You should not be afraid of such requests. The reason for the discrepancies is the difference between accounting and tax accounting. An example of an explanatory note to the tax office upon request in this case could be a reasoned reference to different principles of reporting and accounting.

Explanation from the Federal Tax Service on VAT

Submitting explanations to the Federal Tax Service regarding VAT has its own characteristics. As we have already noted, explanations for VAT must be submitted electronically if the payer’s responsibilities include submitting an electronic declaration (clause 3 of Article 88 of the Tax Code of the Russian Federation). In addition, these explanations must be presented in the approved format (approved by Order of the Federal Tax Service dated December 16, 2016 N ММВ-7-15/ [email protected] ). And if the payer submitted explanations electronically, but in the wrong format, then he was threatened with a fine (clause 1 of Article 129.1 of the Tax Code of the Russian Federation). True, in September 2020, the Federal Tax Service issued a decision (Federal Tax Service Decision dated September 13, 2017 No. SA-4-9 / [email protected] ), which states that the payer should not be fined for the incorrect format of explanations.

If you have the right to submit a VAT return on paper, then it is more convenient to give explanations using the forms developed by the Federal Tax Service (Appendices 2.1-2.9 to the Letter of the Federal Tax Service dated July 16, 2013 No. AS-4-2/12705). But using these forms is a right, not an obligation.

If necessary, you can attach copies of individual invoices, extracts from sales and purchase books to the explanations.

Counter check - what documents to provide?

The explanatory note must be in writing and accompanied by supporting documents.

If you have received a notice from the tax service with a request to provide an explanation, this means that the tax officer is not satisfied with something in the report.

Typically, requests are sent during periodic checks. Desk inspection is carried out using special programs in automatic mode.

Situations when a tax organization has the right to request clarification:

- If there are errors in the reporting or different data between the tax service data and the data in the report.

- If in the updated reporting the tax amount is lower than in the original one.

- If reporting on fees is reported at a loss.

When tax reports contain errors, companies and entrepreneurs can send updated reports rather than an explanatory note.

Any explanatory note is drawn up in free form; there are no strict forms for its preparation.

The document is submitted in one of the following ways:

- By contacting the tax office.

- By mail.

In relation to explanatory notes, there is an electronic option for submission. But it applies only to the VAT explanation and only when the organization submits VAT reporting electronically.

In order to avoid possible mistakes when writing an explanation, you need to clearly know what the tax service is asking from you.

Since there are no clear requests for writing a note, the process is simplified, but you need to remember the following points:

- The note must be registered under a specific number.

- The explanation must include the name of the authority to which you are sending the note.

- In the note you need to write the tax office request number.

- In the text of the document it is necessary to highlight sections and subsections.

- Attachments to the note must be properly completed.

If an error recorded by tax officials is present in the report, but does not affect the final result and does not reduce the tax base, the company or entrepreneur can indicate in the explanatory note that this error does not reduce payments to the budget or submit an updated declaration.

But here is a very interesting situation. Tax liability for failure to comply with the inspection's requirement to provide explanations to the Tax Code of the Russian Federation has not been established. Art. 126 of the Tax Code of the Russian Federation does not apply to this situation, since we are not talking about the requisition of documents (Article 93 of the Tax Code of the Russian Federation), but Art. 129.1 is not applicable, since this is not a counter check (Article 93.1 of the Tax Code of the Russian Federation).

Administrative liability under Art. 19.4 of the Code of Administrative Offenses of the Russian Federation in this case cannot be attracted either. This article applies for failure to appear at the tax authority, and not for refusal to give explanations, which the Federal Tax Service of the Russian Federation itself draws attention to (see clause 2.3 of the letter of the Federal Tax Service of Russia dated July 17, 2013 No. AS-4-2/12837).

Thus, inspectors have no right to fine for failure to submit explanations. But still, despite the absence of legal grounds for the fine, it is more appropriate to provide explanations, since this is in the interests of the taxpayer himself. After all, refusal to do so may result in additional tax charges and sanctions, which you will then have to spend both time and money on appealing.

Such transactions may raise questions among inspectors, the answers to which can be found during the so-called counter audit, which is carried out by the tax authority in order to exercise additional control over the activities of enterprises and organizations, as well as assess the correctness of their tax accounting.

When conducting such an audit, tax officials cannot make any decisions that are binding on the organization being inspected. However, the current legislation does not contain the concept of “counter verification”. Until 01/01/2007 it was recorded in Art.

87 of the Tax Code of the Russian Federation, but then the norm was abolished and was replaced by Art. 93 of the Tax Code of the Russian Federation, which provides for the possibility of requesting from the taxpayer documents drawn up during the implementation of specific transactions.

In practice, the actions of tax officials aimed at working with the documents of the counterparty of the inspected enterprise are still called a counter audit.

To obtain the necessary information, a representative of the tax office sends a request to the enterprise to provide documents. Within 5 days from the receipt of such a request, the authorized person is obliged to send the required package of documentation to the tax office. There is no need to send the originals - it is enough to send the inspector copies of the papers certified by the head of the enterprise or another authorized person.

The legislator does not determine the exact list of documents to be submitted to the Federal Tax Service when conducting this type of inspection; therefore, it depends on the nature and content of the transaction. As a rule, tax authorities require copies of concluded contracts, appendices to them, invoices, specifications, acceptance certificates, invoices, etc.

According to the position set forth in letter No. 03-02-07/1-246 of the Ministry of Finance of the Russian Federation dated October 9, 2012, tax authorities have the right to demand from the taxpayer any documents directly related to the execution of a specific transaction. If the document is not related to the subject of the audit, the requirement to submit it to the Federal Tax Service may be considered unlawful - this point of view is shared by the Federal Antimonopoly Service of the East Siberian District in its resolution dated February 25, 2013 No. A10-2227/2012, referring to the provisions of paragraph 1 Art. 93.1 Tax Code of the Russian Federation.

Tax burden: explanation

If the tax authorities ask you for clarification due to the fact that your tax burden is low compared to the industry average, then you can answer them something like this:

“In the declaration for such and such a tax for such and such a period, there is no incomplete reflection of information or errors that would lead to an underestimation of the tax base. In this regard, the organization has no obligation to clarify tax liabilities for the specified period.

As for the tax burden on the main type of activity of the organization, its decrease in such and such a period is caused by the following circumstances: a decrease in income and an increase in the organization’s expenses.”

And then state how much the amount of revenue has decreased and expenses have increased for the requested period compared to previous periods. And what caused this (decrease in the number of buyers, increase in purchase prices, etc.).

We talked in more detail about the clarifications requested by tax authorities in connection with the reduction of the tax burden in a separate consultation, where we also provided a sample format for the corresponding clarifications.

When the tax office asks for clarification

The reasons why tax officials may have questions for a taxpayer during a desk audit are listed in clause 3 of Art. 88 of the Tax Code of the Russian Federation:

- Reason 1 – the camera revealed errors in the reporting or contradictions between the reporting data and the information available to the tax authorities.

What the Federal Tax Service will require is to provide clarifications or make corrections to the reporting.

- Reason 2 – the taxpayer submitted a “clarification” in which the amount of tax payable, compared to the previously submitted report, became less.

What the Federal Tax Service will require is to provide explanations justifying the change in indicators and the reduction in the amount of tax payable.

- Reason 3 – unprofitable indicators are stated in the reporting.

What the Federal Tax Service will require is to provide explanations justifying the amount of the loss received.

Having received a similar request from tax authorities to provide an explanation to the tax office (a sample can be seen below), it should be answered within 5 business days. There are no penalties for failure to submit, but you should not ignore the tax authorities’ requirements, since, without receiving a response, the Federal Tax Service may assess additional taxes and penalties.

Please note: if the taxpayer belongs to the category of those who are required to submit a tax return electronically in accordance with clause 3 of Art. 80 of the Tax Code of the Russian Federation (for example, on VAT), then he must ensure the receipt from the Federal Tax Service of electronic documents sent during the desk audit. This also applies to requests for explanations - within 6 days from the date of sending by the tax authorities, the taxpayer sends an electronic receipt to the Federal Tax Service Inspectorate confirming receipt of such a request (clause 5.1 of Article 23 of the Tax Code of the Russian Federation). If receipt of the electronic request is not confirmed, this threatens to block the taxpayer’s bank accounts (Clause 3 of Article 76 of the Tax Code of the Russian Federation).

In what situations is there a requirement to submit documents to the tax office?

According to the law, the tax office can only put forward relevant demands if there are grounds. The list of inspections carried out by the Federal Tax Service is enshrined in paragraph 1 of Article 87 of the Tax Code of the Russian Federation.

Please note: There are desk and field checks. The first are organized at the location of the Federal Tax Service on the basis of materials and documents submitted by the taxpayer, which are available to the authorized body. A desk audit is carried out within 3 months after receiving documentation from the person paying taxes. The period cannot be extended or suspended.

The grounds for conducting a desk audit and requesting documents are:

- the organization wants to take advantage of the benefits established by tax legislation;

- the company wants to return to paying VAT;

- the organization makes tax payments in connection with the use of natural resources;

- It is necessary to resolve issues related to tax control.

The tax authority has no right to send a request on other grounds. An on-site inspection is carried out directly on the taxpayer’s premises. The period of such verification does not exceed 2 months. However, the period can be extended to 4 months if there are objective reasons. In exceptional cases, extensions of the period up to six months are permissible. If an on-site tax audit is suspended, by law it is impossible to request documents or make a demand for their provision. Other actions are considered a violation of the law.

Video

https://youtu.be/tH7EjpDcIeY

From the above it follows that the requirement to submit documents to the tax office may be in the following cases:

- when conducting a desk audit based on a declaration previously submitted to the tax authority;

- during an on-site inspection;

- during a counter tax audit.

How to write explanations to the tax office

There is no officially approved sample explanatory letter sent in response to the Federal Tax Service's request for clarification. Explanations can be made in any form, indicating the following information:

- name of the tax authority and taxpayer, his INN/KPP, OGRN, address, telephone;

- heading "Explanations";

- mandatory reference to the originating number and date of request from the tax office,

- direct explanations on the requested issue with their justification,

- if necessary, list attachments to the letter confirming the correctness of the reporting indicators,

- manager's signature.

If an error made in reporting did not lead to an understatement of tax, the explanatory note to the tax office must contain this information. Write about this, indicating the nature of the error (for example, a typo or technical error) and the correct value, or provide an updated declaration or calculation. An error due to which the tax amount was underestimated can be corrected only by submitting a “clarification” - explanations alone will not be enough for tax authorities in this case.

When, in the taxpayer’s opinion, there are no errors in the reporting, and therefore there is no need to submit an “adjustment”, it is still necessary to provide explanations to the tax authorities, indicating the absence of errors in the declaration or calculation.

Response to counter check

When writing responses to requests, you must comply with certain conditions related to the nature of the requirement. If a company receives a request for a counter-verification, the company is obliged to provide the necessary documentation. In this case, a sample explanatory note to the tax office at the request of a counter audit will look like a list of copies of the submitted materials. Of course, it is necessary to mention the name, INN/KPP of the company, and the period being checked.

It is not recommended to provide information that is not asked for, even if you want to share. The responsible person must answer the questions very briefly and clearly, strictly according to the points of the requirement. A lot of bewilderment is usually caused by the desire of tax officials to find out the nature of the counterparty’s activities, additional contacts, and staffing.

Lawyers do not recommend providing such information, citing the fact that the organization is not obliged to be aware of what is happening with the counterparty. Therefore, in the explanatory note to the tax office, upon request, the sample will be a reference to the information contained in the agreement with the counterparty.

Letter of explanation to the tax office: sample for losses

Taxpayers may be interested in the company's unprofitable activities, in which case the taxpayer's explanations must fully disclose the reason for the loss in the requested reporting period. To do this, the letter deciphers income and expenses for a certain period of time.

Also, explanations to the tax office (see sample below) must contain instructions on why expenses exceeded income. For example, a company has just been established, operations have just begun and revenue is still small, but current expenses are already significant (rent, employee salaries, advertising, etc.), or the company has incurred urgent large expenses for repairs, purchase of equipment, etc. The more detailed the reasons for the loss are, the fewer new questions the tax authorities will have.

All information provided must be documented by attaching copies of accounting documents, contracts, invoices, bank statements, tax registers, etc. to a written explanation for the tax office.

Similarly, explanations can be given in response to a request for reasons for reducing the tax burden, in comparison with the industry average.

Sample letter to the tax office to provide explanations in connection with a loss:

Why write an explanation?

The letter to the tax authorities should begin as follows: “In response to your request for clarification regarding __ No. __, we inform you of the following: …” Next, you need to write down specific information depending on the essence of the request.

For example, a number of incomes are not subject to VAT, but are taken into account when determining the amount of income tax. Therefore, it will be enough to point out this circumstance with reference to specific provisions of the law.

When applying for VAT refund, as practice shows, clarification will be required.

When tax authorities require an explanation of a loss in a declaration, it is necessary to justify the reason for its occurrence. Therefore, it is necessary to provide documentary evidence of income and expenses, explain how the calculation took place, and also justify the occurrence of this loss. Extracts from accounting registers, contracts with suppliers, contracts with clients, etc. are suitable for documentary evidence.

If the deterioration in indicators was not reflected in the previous statements, but losses immediately began in this one, then it all looks very controversial and suspicious. In this case, in response to the tax demand, it is necessary to explain the following:

- reveal the dynamics of the requested accounting item, that is, clearly show in figures what led to the loss.

- Give a brief written explanation of the reasons for what happened.

Do tax authorities have the right to demand explanations for losses from previous years? Expert opinion

Of course, they may be different for each company and in each individual industry, but the following can be considered the main ones:

- reduction in production or sales due to the crisis, unstable market and economic situation;

- a fall in demand for products and, as a consequence, a forced reduction in prices;

- a large exchange rate difference, that is, an increase in costs due to the depreciation of the ruble against foreign currencies;

- large expenses (repairs, redesign, purchase of equipment, long-term investments, etc.).

It is better to confirm all the reasons indicated in the explanations with documentation. With everything you can - extracts, decisions of the board of directors, invoices and other documents provided for in paragraph 4 of Art. 88 Tax Code of the Russian Federation. This will help prevent further questions from the tax office and a possible on-site audit of the company.

A unified form for such letters of explanation has not been developed, so draw up an explanatory note to the tax inspectorate in any form at the request of the tax inspectorate. You can use the sample attached below as a basis. The download link is also attached.

Before writing a response to the tax office’s request for clarification (there is a sample above), look at the letter of the Federal Tax Service of the Russian Federation dated January 27, 2015 No. ED-4-15/1071. It lists cases in which the company should be notified of receipt of a claim. Also, do not be alarmed if the letter does not have the stamp of the tax office, this is provided for by letter of the Federal Tax Service of the Russian Federation dated July 15, 2015 No. ED-3-2/ [email protected]

Now let's see how to write a letter to the tax office in response to a request. As mentioned above, there is no unified form of answer for giving explanations, so you can compose it in any form. If you don’t know how to format a letter to the tax office in response to a request, take the sample attached above.

Remember that the form of the answer and the arguments themselves should be short, concise, without unnecessary prefaces or digressions. Follow the standard rules for writing official letters. So, the header of the note should contain the following data:

- First, on the right (you can do this on the left, it doesn’t matter) you need to indicate the addressee, the branch of the exact tax office where you are sending the answer. Indicate all contact information: department number, its district, the locality to which it belongs.

- Next, indicate the sender of the letter: write the name of the company, its address (actual), as well as a contact phone number where you can be contacted and clarify possible questions. Of course, write in the genitive case.

- Next, in your response, you should refer to the request number (carefully review the letter that was sent to you, there must be an outgoing number), and indicate the date of your response. Also try to briefly outline the essence of the issue. Usually written in brackets, see the fragment attached below.

After the header is designed, proceed to describe the situation and arguments. They should be written in as much detail as possible, with all the necessary links to documents, laws, regulations, etc. The more carefully this part of the answer is prepared, the greater the chance that the tax office will be satisfied with it.

Important: under no circumstances submit unreliable or deliberately false information - they will be discovered fairly quickly and immediate sanctions will follow.

After the response is completed, confirm it with the signature of the chief accountant, and the document must also be signed by the head of the company.

Quite often, tax specialists have various questions based on the results of reports submitted by a tax agent. In such situations, inspectors send a letter to the organization asking for clarification. Most often, problems arise due to any contradictions, inaccuracies and errors identified in the declarations, inconsistencies between the data available in the tax and indicated in the reporting documentation of the enterprise, as well as due to the lack of profit based on the results of work in the reporting period, and even less especially with obvious losses.

Lack of income and losses of organizations is not such a rare occurrence as it might seem to an uninitiated person. They can be associated with a variety of circumstances. They can be caused by a general financial crisis, a decline in demand for products (including due to seasonal factors), an excess of expenses over profits (for example, when purchasing expensive equipment, major repair work, etc.), problems in production , ineffective company management, re-profiling of the enterprise and development of new markets and many other reasons.

Explanations about losses must be given. Moreover, this should be done in writing and no later than five days after receiving the corresponding request from the tax authority.

Despite the fact that no punishment is provided for the lack of explanations in the legislation of the Russian Federation, ignoring letters from tax officials can have very dire consequences for the organization. In particular, additional taxes may be assessed or any administrative measures may be taken.

But the most unpleasant thing, which is also quite possible, is that the lack of a logical and clear picture of the company’s financial activities can lead to an on-site tax audit, during which all documentation for the last three years will be “shooked up,” and this is fraught with completely different, more serious sanctions. It has been noticed that tax authorities are very willing to include companies with regular losses in the schedule of on-site inspections.

The explanation can be written in any form. The main thing is that the structure of the document meets the norms and rules for drawing up business documentation, and the text of the explanatory note itself is clear, understandable and fully reflects the real state of affairs at the enterprise.

If some events characteristic of the entire economy led to losses: for example, a crisis, then sometimes it is enough to simply formulate this correctly, pointing out a decline in demand and a forced reduction in prices (attaching reports, price lists and other documents indicating this to the explanation). But if the reason for the lack of profit was, for example, large expenses of the taxpayer with a simultaneous decrease in sales, then this information must be supported by more serious documents (contracts and agreements on termination of contracts, acts, tax extracts, etc.). If possible, you should also provide a detailed report of expenses and income.

If losses arose as a result of any emergency situations (fires, floods, thefts, etc.), then certificates from the relevant government agencies (police, Ministry of Emergency Situations, management company, etc.) must be attached to the explanation.

The document will also include a description of the measures that the organization’s employees are taking to prevent further losses (they will indicate the desire of the enterprise management to correct the unfavorable situation).

It should be noted that large companies’ explanations sometimes reach several dozen pages, which is understandable, since the more accurate the explanatory note, the fewer claims from tax authorities may appear in the future and the lower the likelihood of an on-site tax audit.

If the tax office has sent you a request to provide explanations for losses, take into account the above recommendations and look at the example - based on them you can easily write your own document.

- First, in the explanatory note you need to indicate the addressee (on the right or left at the top of the form), i.e. the tax office where this letter will be sent.

- Then the sender is indicated: the name of the company, its details and contact information,

- After that, go to the main section. First of all, provide here a link to the request for clarification received from the tax office.

- Next, describe in as much detail as possible the circumstances in connection with which the losses occurred.

- After that, move on to explanations in numbers. Here you need to provide data on income and expenses, as well as provide links to documentary evidence (indicating their name, number and date).

- After the explanatory note has been generated, do not forget to sign it.

Most often, the tax office considers losses received over several years. Explanations are drawn up by legal entities whose enterprises have been registered for more than 2 years.

This is not required of new companies; losses are a normal process for new companies. An explanatory note on losses is written to explain the occurrence.

Therefore, the note needs to disclose the following information:

- About the income and expenses of the company, calculate and show as a result of which the organization operated at a loss.

- About what caused it to happen.

Explanatory note to the tax office: sample for VAT

Since January 24, 2017, the Federal Tax Service order dated December 16, 2016 No. ММВ-7-15/682 on approval of the format of explanations to the VAT return in electronic form has been in force. This format is used by all VAT payers who submit electronic reports. The procedure for a taxpayer's actions upon receipt of a request to provide explanations on the VAT return is described in detail in the letter of the Federal Tax Service of the Russian Federation dated November 6, 2015 No. ED-4-15/19395.

How to write an explanatory note to the tax office regarding VAT? Only electronically. Explanations on VAT presented in “paper” form are not considered submitted, and in this case this may be regarded by tax authorities as an unlawful failure to provide the requested information, which threatens with a fine of 5,000 rubles (Clause 1 of Article 129.1 of the Tax Code of the Russian Federation).

Whatever the request from the tax inspectorate: about detected errors, contradictions between reporting forms, about a reduction in the amount of tax in an updated declaration, or about the reasons for the loss, in any case it is necessary to respond to the request. For reporting submitted exclusively via telecommunication channels, an electronic format for submitting explanations is provided at the request of tax authorities.

Why do you need to respond to demands?

A tax requirement comes to an enterprise in different ways:

- by mail;

- through an electronic document management system;

- on purpose.

You will be interested in: “Baltinvestbank”: reviews, deposits, payments

According to current legislation, starting from 2020, the company is obliged to respond to requests from the Federal Tax Service. If previously inspectors recommended not to ignore their requests, since such companies could arouse increased interest on the part of control authorities, then from 2020, the absence of an explanatory note to the tax office upon request within the period established for the response will lead to the imposition of a fine of 5,000 rubles for the first offense . Repeated delay in response within a year increases penalties to 20,000 rubles. In addition, the Federal Tax Service may block the company’s bank accounts.