What it is?

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem , contact a consultant:

+7 (499) 110-43-85 (Moscow)

+7 (812) 317-60-09 (Saint Petersburg)

8 (800) 222-69-48 (Regions)

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FREE !

Arithmetic errors made when an accountant determines the amount of wages for employees of an organization are called calculation errors.

Similar shortcomings arise when performing elementary mathematical operations (addition, subtraction, multiplication) with computational errors.

Documentation

Upon receipt of the grounds for the return of funds in favor of the company, the company’s accountant must properly document this procedure in the financial documents. In particular, for this, form No. 0504833 is drawn up. In addition, the procedure for entering information about crediting to the company’s account will depend on how the funds were reimbursed, as well as for what period of time they were calculated.

If we are talking about withdrawing the amount for the current year, then the required amount of money will be automatically withdrawn from the employee’s salary next month. If we are talking about repaying debts over the past years, then the employee can also contribute the required difference from income to the enterprise’s cash desk. If we are talking about automatic deduction of funds, then you need to take into account the deduction of personal income tax. When money comes through the cash register, it is considered income of the enterprise and implies payment of taxes by the company itself.

What rules of law govern it?

The Labor Code of the Russian Federation in Article 137 provides for the possibility of deducting from an employee’s salary excess amounts previously paid to him due to the presence of an error in the calculations.

However, the Russian Labor Code does not provide a clear definition of the concept of a counting error.

This term is considered:

- In the Letter of Rostrud dated October 1, 2012 No. 1286-6-1

- In the Supreme Court Decision No. 59-B11-17 dated January 20, 2012

Retention of funds

If the employee voluntarily provided an agreement to withhold funds from the next salary, or when a court decision was made to satisfy the employer’s request, then only in this case the amount can be withheld from the next salary. In addition to the costs of accounting errors, the following funds may be additionally deducted from the employee’s salary:

- alimony (based on a court decision, the required amount is automatically sent to the account of the legal recipient of the funds);

- income tax, as well as tax to the pension fund, which are automatically sent to the controlling budgetary structures;

- amounts previously paid by the company (for example, taking all vacation days off before the end of the calendar year when terminating the employment agreement).

What doesn't apply here?

An accountant's error is not considered an accounting error if:

- he re-transferred any payment to the employee;

- when calculating wages, they did not take into account the employee’s unpaid rest time;

- a larger amount of income tax was deducted from the employee’s salary than required;

- a bonus or allowance was erroneously paid without the appropriate order from management.

Thus, an uncountable error occurs when the employer incorrectly applies legislation or local rules adopted in the organization, as well as when double accrual occurs.

Technical errors associated with incorrect data entry are also highlighted.

An accountant's error, by a court decision, may be recognized as technical, rather than accounting, if it arose due to low qualifications or negligence of an accounting employee.

Methods of proof

The court, as a rule, is on the side of the employee, and therefore the accountant and the management of the enterprise need to be properly prepared to prove their point of view in court. In addition, you need to prepare the following package of papers:

- a petition from the head of the enterprise with a detailed description of the problem that has arisen, as well as indicating the reasons and amounts of charges in excess of the norm;

- explanation of the person responsible for entering data into computer accounting (accountant);

- an act that was drawn up when a financial inaccuracy was identified;

- salary slip indicating the amount of the employee’s income for the previous month when the mistake was made, and the next;

- math worksheets;

- conclusion of an IT specialist (when a counting error occurred due to a malfunction of programs).

If the error in payroll calculation is counting

If, upon detection of a computational error when calculating wages, it was discovered that the employee received less money than he earned, it is necessary to accrue the remaining funds.

When transferring an amount greater than the required amount, it is withheld, with the consent of the employee.

Should the employee return it?

According to the norms of the second part of Article 137 of the Labor Code, the amount overpaid to the employee must be withheld from him.

Procedure

If a counting error is detected and excess funds are transferred to one of the employees, a corresponding report on the discovery of the error is drawn up.

Overpayment of money to an employee as a result of a calculation error when calculating wages must be withheld from him within one calendar month after payment.

But before this, it is necessary to obtain the employee’s consent to withhold, and then issue an appropriate order. If consent is not obtained, the employer, if there is appropriate evidence of excessive payment as a result of a calculation error, may go to court.

Our article will help you write a power of attorney to receive salary. Should alimony be calculated from the 13th salary? Find out here.

Conditions for withholding funds

Withholding from an employee by the employer can be made in the case where the employee agrees with the basis for the deduction of funds and the amount of this amount, as well as with the very possibility of withholding overpaid funds.

The maximum amount of possible deduction from salary cannot be more than 20% of the amount of money received by the employee and is represented by the following formula:

Withholding < 20% (Accrued salary – income tax)

This requirement is also contained in Part 1 of Art. 137 of the Labor Code of the Russian Federation and in the clarification of the Ministry of Health and Social Development of the Russian Federation dated November 16, 2011 N 22-2-4852 On the amount of deductions from wages.

Documenting

Documentation of the operation to return money overpaid to the employee is carried out according to one of the presented options:

| Option 1 | Option 2 |

| The employer obtains written permission from the employee to return the funds. | The employer issues a decree to withhold funds from the employee's salary |

| A corresponding order is issued | The employee signs the issued decree |

| Based on the order, deduction is made | Withholding is carried out on the basis of a decree |

Collection period

The amount of overpayment, with the consent of the employee, must be returned within a month after the accounting error.

If there is no agreement and the employer goes to court, the statute of limitations for debt repayment is three years.

Reflection of returns in accounting

In accounting, the return of overpaid amounts is formalized by the following entries to the credit of the account intended for settlements with personnel for wages (account 70).

| Debit | Credit | Operation |

| 50 (51) | 70 | The amount of overpaid wages was returned to the organization’s cash desk (to its current account) |

| 91-2 | 70 | The unreturned amount of the excess (if the Court refused to collect or the statute of limitations has expired) is written off. |

The unreturned amount of the excess (if the Court refused to collect or the statute of limitations has expired) is written off.

Correction of personal income tax calculations

Funds overpaid as a result of a counting error are not recognized as a material benefit of the employee, and it is unlawful to qualify them as an interest-free loan and tax them at an increased rate of 35%.

If, when a counting error is detected, the employee agrees to withhold the amount of overpayment from him, personal income tax at a rate of 13% is not charged, since this amount of money will be returned to the cash desk or to the organization’s current account.

If the employee has already left the organization, or does not agree to return the excess funds received, and the trial drags on for a long time (more than 12 months), the employer submits information about the impossibility of withholding tax on the income paid to the employee to the Tax Inspectorate.

Should changes be made to the RSV-1 Pension Fund?

Based on Letter of the Ministry of Health and Social Development of the Russian Federation dated May 28, 2010 N 1376-19, changes to the RSV-1 Pension Fund of the Russian Federation (calculation of accrued and paid insurance premiums) do not need to be made if a calculation error is detected by drawing up updated calculations.

This error will be reflected in the corresponding document for the period in which it was discovered.

Thus, if erroneous payments were already included in the tax base for the previous quarter (for example, 1), but this was discovered in the next period (for example, 2), then the error is reflected in the period of its discovery (in the 2nd quarter).

Technical oversight

Incorrect data entry is considered a technical error. This is how courts often characterize a mistake made by an accountant. In this case, the overpayment by the employee is not refunded.

Such errors, for example, include:

- misapplication of tax benefits;

- choosing the wrong coefficient when calculating salaries;

- entering incorrect initial data for calculations, etc.

It is almost impossible to reclassify such deficiencies as counting ones.

In judicial practice, the following are recognized as technical errors:

- incorrect entry of information into the program;

- double transfer of earnings and other payments;

- payment of remuneration for a period on various grounds;

- failure to comply with the rules established by regulatory documents.

The employer must remember that in the event of a counting error, withholding an overpayment from an employee’s earnings without his consent is illegal (Part 3 of Article 137 of the Labor Code).

To obtain consent from the employee, you must prepare a notice to him in writing. The employee can write an application for a refund or fill out the appropriate notification fields. The worker must write that he agrees with the reason and amount of the withholding.

Upon receipt of approval from the employee, the employer can set a certain period for him to return the money, for example, 3 days, as for travel expenses. Upon expiration of the period, the manager has the right to issue an order to withhold the amount within a month. The order is issued only with consent.

If the employee refuses or misses a month's deadline, the overpayment can only be returned by a court decision.

Admission of technical errors excludes all options by which it is possible to recover the amount of excessive wages from the employee. And courts, as practice shows, often refuse to satisfy employers’ requests, citing these reasons. Errors due to which funds are not withdrawn include:

- incorrect entry of initial data;

- indication of incorrect calculation grounds (salary, sick leave, vacation);

- erroneous payment of two salaries at the same time;

- indication of excess benefits or incorrect percentages.

If the error is of a different type

If an error is made in the calculations that is not related to accounting, the employer has the right to notify the employee that such an error has been discovered and ask to return the money accrued by mistake.

In accordance with Article 1109 of the Civil Code of the Russian Federation, if the employee does not agree to the return, even the judicial authorities do not have the right to recover these amounts from the employee of the organization.

However, the unrefunded amount must then be subject to personal income tax.

Non-insurance periods on sick leave - what is it? Find out from our article. Read about marginal profit analysis here.

What do the salary codes on the payslip mean? See here.

Deduction from employee income

| Tax Code of the Russian Federation, clause 4, art. 226 | The employer is obliged to withhold personal income tax from the employee’s salary. Article 226. Peculiarities of tax calculation by tax agents |

| RF IC Art. 109 | The organization must deduct alimony from the employee’s income and transfer it to the recipient’s account. The basis for this is a writ of execution or an agreement certified by a notary. Article 1109. Unjust enrichment that is not subject to return Article 109. Obligation of the organization’s administration to withhold alimony |

| Law on enforcement proceedings No. 229-FZ dated 02.10.07 | Based on clause 3 of Art. 98, the debtor’s employer must make deductions from his earnings according to the writ of execution in accordance with the requirements contained therein. |

| Law on state benefits for citizens with children No. 81-FZ of May 19, 1995 | Art. 19 obliges the company to withhold from the income of employees overpayment of benefits resulting from the fault of the workers. For example, due to concealment of information affecting the size and purpose of payments, provision of false papers. |

| Law on social insurance No. 255-FZ of December 29, 2006 | Clause 4 of Art. 15 states that overpaid amounts of benefits from the Social Insurance Fund are recovered from the recipient if the fact of his dishonesty is revealed or if an accountant makes a calculation error. |

In Art. 137 of the Labor Code states that deductions from a worker’s earnings to pay off a debt to the company are possible in the following cases:

- to reimburse an advance that was issued against earnings and was not worked out;

- to repay unspent and not returned on time advances issued for a business trip, official trip or other purposes;

- to return an overpayment to an employee due to a counting error or when the authorized body recognizes the worker’s guilt in non-compliance with labor standards or downtime;

- when an employee is dismissed before the end of the period for which he has already taken paid leave.

The employer must make a decision to return the overpayment within a month from the moment when the advance should have been returned, the debt was repaid, or an accounting error was identified. The employee must agree to the withholding.

Example

In accordance with Art. 138 of the Labor Code, the amount of all deductions from an employee’s monthly salary cannot exceed 20%.

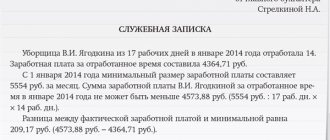

For April 2020, plumber V.V. Kholopov LLC received a salary of 16 thousand rubles. By order of the manager, for this period he is entitled to a bonus of 4,800 rubles.

A month later, the accountant discovered a calculation error when calculating wages in the amount of 1,740 rubles. (19,836 – (20,800 – 13%)).

To record the fact of a counting error, a commission was created in the LLC, to which the accountant wrote an explanatory note. The mistake was ruled to be arithmetical. They decided to collect it from the employee’s earnings for May 2020.

A notification about this was sent to V.V. Kholopov and he confirmed his agreement with the situation.

Examples

In August 2020, Anna Valentinovna Mironova, an employee of the sales department of Orion LLC, was transferred 20 thousand rubles instead of 10 thousand rubles (salary) due to the fault of the accountant. The amount of money was sent twice by mistake. The employee was asked to return the funds, but she refused; it turned out to be impossible to collect the funds. The error was not a counting one.

In February 2020, Anatoly Anatolyevich Ivanov, an employee of a trading enterprise, was credited with 28,000 rubles instead of the required 27,000 rubles. The accountant explained that the extra 1,000 rubles were accrued as a result of an error when adding up payments due to an employee of the organization for providing additional paid services to customers. Ivanov A.A., after familiarizing himself with the error report, wrote a written authorization to return the excessively transferred funds. The incident was settled, as 1,000 rubles were deposited by the employee into the organization’s cash desk.

Reflection in accounting

If the employee agrees to return the excess amount given to him to the cashier, the accountant must reflect this in postings.

| Operation | Dt | CT |

| Overpayment identified and repaid in a given year | ||

| Excessively accrued income reversed | 401 20 211 – wage costs | 302 11 730 – salary creditor increased |

| Overpayment of previous years revealed | ||

| In the current period, earnings were accrued in the amount of the previously identified overpayment | 205 81 560 - receivables for other receipts increased | 401 10 180-other costs |

| The employee deposited the excess into the cash register | 201 34 510 - money received | 205 81 660 - receivables for other expenses were reduced |

We invite you to familiarize yourself with a sample internal order on appointing yourself as responsible

The detected overpayment is confirmed by a certificate f. 0504833, on the basis of which the amount is reflected in the accounting registers. Overpayments from previous periods are counted as income. The employee returns the amount minus personal income tax.

Arbitrage practice

Modern judicial practice regarding the recognition of an accountant's accounting error and the recovery of the excess amount received from an employee is quite contradictory.

However, in most cases, only an error that arose during the incorrect application of mathematical rules is considered countable.

Erroneous or repeated entry of data for payroll calculations in most cases is not recognized as a calculation error.

If the employer is confident that the error in charging the wrong amount of money to the employee occurred as a result of a calculation error (accounting), and the employee voluntarily refuses to make a refund, going to court should have a positive result.

To apply to the judicial authorities, the accountant draws up an explanatory note with mathematical calculations, which clearly shows the calculation that resulted in an incorrect calculation, and also attaches pay slips, statements and other supporting documents.

If the error arose as a result of a failure of the accounting program, you will need to provide an opinion from an IT specialist stating that the accounting error arose precisely because of problems in the operation of the program installed on the computer.

If the employer, without the written consent of the employee, deducted previously overpaid funds from his salary, even if there is a justification for this action (for example, an error in calculations), he will be obliged to return the withheld funds in full with compensation for moral damage to the employee (if he applied to the Court, finding retention without consent).

Thus, when calculating employee wages, accounting department employees should be especially careful.

Correcting counting errors can take a lot of time and effort. In some cases, if an employee is assigned financial responsibility for errors, the amount of funds overpaid to any employee can be recovered from the financially responsible accountant.

Attention!

- Due to frequent changes in legislation, information sometimes becomes outdated faster than we can update it on the website.

- All cases are very individual and depend on many factors. Basic information does not guarantee a solution to your specific problems.

That's why FREE expert consultants work for you around the clock!

- via the form (below), or via online chat

- Call the hotline:

- Moscow and the Region

- St. Petersburg and region

- Regions - 8 (800) 222-69-48

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

Salary

Arithmetic inaccuracies

In Russian regulations there is no specific definition of the concept of what a counting error is, but in accounting practice it is customary to use the following designation: this is an oversight made when performing all kinds of arithmetic operations with wage amounts. In this case we are talking about elementary mathematical operations: multiplication and division, summation and subtraction.

An error in calculation can be made either in favor of the employee or vice versa. If it turns out that the employee was underpaid in the amount of cash support, then the enterprise is obliged to reimburse the withheld amount with the subsequent payment of wages. Even if this error is discovered much later when filing documents for dismissal, the company must pay for the losses. The situation is much more complicated if a mistake made caused an excessive payment.

The law determines that an employer can retain the required amount of funds in two legal ways:

- with the written consent of the employee himself;

- on the basis of an appropriate court decision (this method can be applied to both employed persons and already dismissed employees).

In addition, it is necessary to pay attention to the list of features that exclude mistakes made from counting errors and the possibility of deducting funds from the employee’s income. In particular:

- accidental entry of incorrect data into the payroll accounting program;

- if the violation was committed by the accountant due to his low qualifications or professional negligence;

- a violation in the operation of the payment program (with the exception of cases when a computer equipment service specialist draws a conclusion that a failure in the program actually led to overtime payments);

- technical errors.

We invite you to familiarize yourself with Compensation upon dismissal by agreement of the parties 2020: amount of severance pay, taxes and contributions

Taxation

Income tax is withheld from all types of income from employees, the amount of which depends on the amount of wages, so a counting or technical error entails a violation in the deduction of personal income tax. How the adjustment occurs depends on which direction the error was made. If we are talking about missing wages and, as a result, paying less tax, then next month, when the employer pays a larger amount, the amount of taxation will be proportionately greater.

If an oversight was made in favor of the employee, and a larger amount of tax was withdrawn from his account, then, if it is necessary to return these funds to the enterprise, the employee must be reimbursed for the amount of tax deductions. To do this, you should send a corresponding application to the accounting department. And, based on the statement, next month the amount of personal income tax will be less.

In addition to possible options for obtaining excess contributions from the employee (personal consent, court decision), you can additionally provide for this clause in the employment agreement. Thus, signing an employment contract is the employee’s automatic consent to the withdrawal of excessive payments if they are accidentally accrued.