Budget Classification Codes (BCC) 2019

To designate budget expenses, a twenty-character code is also used, which is somewhat different from the revenue code in its structure. Their only similarity is that in both codes (as, indeed, in the KBK of sources of deficit coverage), the first three digits classify the main manager (administrator) of budget funds, and the last three digits correspond to certain KOSGU.

- To pay tax on the income of a tax agent, the following BCC is generally used - budget revenue administrator code “182”, group “1”, subgroup “01”, income item “02”, subarticle “010”, element “01”, subtype code “ 1000”, KOSGU “110”, for payment of penalties for this tax the subtype changes from “1000” to “2000”, for fines - to “3000”.

- For entrepreneurs, private notaries and persons engaged in private practice, the code is as follows - administrator “182”, group “1”, subgroup “01”, income item “02”, subarticle “020”, element “01”, subtype code “1000” ", KOSGU "110", for fines and penalties subtype in the same way as for other taxes "2000" and "3000", respectively.

- For individuals to pay tax on income received in the cases specified in Article 228 of the Tax Code, the BCC is the administrator “182”, group “1”, subgroup “01”, income item “02”, subarticle “030”, element “ 01”, subtype code “1000”, KOSGU “110”.

https://youtu.be/sm3wxK2dt5E

KVR and KOSGU in 2020 for budgetary institutions

In 2020, the accounting treatment of some expenses for KOSGU has changed. Thus, the costs of ensuring measures to reduce industrial injuries and occupational diseases, starting from 2020, do not relate to subsection 213. Such expenses included activities, for example, to carry out certification of workplaces, labor safety training for certain categories of workers, purchase of special clothing and personal protective equipment for workers engaged in work with harmful and (or) dangerous working conditions, as well as in work in special temperature conditions. conditions, and a number of similar expenses. The accrual of insurance contributions for compulsory social insurance against industrial accidents and occupational diseases remained in subarticle 213. The specified position is given in the positions of the Ministry of Finance: Order No. 65n and Letter dated 02/16/2017 No. 02-07-07/8786.

- costs of payments to personnel in order to ensure the performance of functions by state (municipal) bodies, government institutions, management bodies of state extra-budgetary funds;

- procurement of goods, works and services to meet state (municipal) needs;

- social security and other payments to the population;

- capital investments in state (municipal) property;

- interbudgetary transfers;

- provision of subsidies to budgetary, autonomous institutions and other non-profit organizations;

- servicing state (municipal) debt;

- other appropriations.

How to recalculate the cost of an operating system - procedure

The revaluation process must be carefully prepared:

- First of all, this is the study of information about fixed assets - what initial cost is subject to adjustment.

- The commission is assembled on the basis of the order of the head.

- The range of fixed assets subject to revaluation is determined.

- The process itself is carried out according to the chosen method.

- The results obtained are then reflected in the company's accounting.

Methods

Today, due to changes in legislation, only one recount option is used - direct recalculation.

In this case, information is used as a base from the following sources:

- data from the database of manufacturers of similar objects;

- data regarding price levels from government or statistical sources;

- expert assessment of independent specialists.

The abolition of the index deflator established by Decree No. 315 of 1996 occurred as a result of the adoption of Decree of the Government of the Russian Federation No. 121 of 2002, which abolished the previous version.

But new indices were not installed, so the index method has lost its relevance, although it is used in some companies.

Documenting

According to the algorithm, the revaluation of fixed assets should be carried out on the basis of an order from the manager, and a list of objects with a brief description should also be generated - the date of acquisition, the date of acceptance for accounting and an indication of the current price.

In addition, other documents on this object are being studied. An accounting certificate for the revaluation is generated, which indicates the relevance of the event.

Based on the results of the inspection, a report on the work done is drawn up, indicating the price indicated by the commission.

New data is also recorded in the OS-6 inventory card for the facility.

Sample order

The manager's order is formed taking into account the requirements for the preparation of such documentation and its sample is fixed in the accounting policy of the organization.

The structure of the document is as follows:

- Name of the organization;

- title of the document with justification, for example, “On the revaluation of fixed assets”;

- date and document number;

- then the main part of the manager’s order is indicated, where the reason for the recalculation is initially indicated - “Due to a significant change in prices, I order a revaluation of fixed assets for real estate”;

- after which the list can be indicated in a tabular version - the name of the objects, inventory number and cost during the period of acceptance for production;

- Next, you should indicate what cost should be taken for the initial, for example, cadastral value;

- after this, responsible persons are appointed, and responsibility for each stage may be assigned to different employees.

At the end of the document there must be signatures of the manager and persons related to the revaluation process.

KVR: transcript

All public sector institutions pay mandatory taxes and fees in accordance with the general procedure. In the budget laws you can find this item of expenditure provided for government institutions. In addition to the traditional land tax and corporate property tax, for example, the payment of transport tax, which is present in the decoding of KVR 852, can be carried out.

- Codes of the main managers of budget funds. Approved by order of the Ministry of Finance of the Russian Federation. There is no abbreviated name. Expenditures are grouped by department.

- Codes of sections and subsections. Approved by order of the Ministry of Finance of the Russian Federation. The abbreviated name is KFSR. Expenditures are grouped by industry: education, culture, healthcare, and so on.

- Expense type codes. Approved by order of the Ministry of Finance of the Russian Federation. The abbreviated name is KVR. In deciphering the concept, it is noted that the types of expenses indicate the directions for spending funds, which authorities and government agencies are required to comply with.

- Codes of target expense items. Approved by order of the financial authority. The abbreviated name is KTSSR. Costs for the implementation of various target programs are grouped.

- General government sector transaction codes. Approved by order of the Ministry of Finance of the Russian Federation. The abbreviated name is KoSGU. Indicate direct items of expenditure, which include estimates of government agencies and authorities. Subject to strict coordination with the CWR. Deciphering and checking the linkage is usually carried out during audits and allows one to draw conclusions about the targeted or inappropriate spending of budget funds.

Kvsr in the budget is a transcript of 2019

The list of main managers is established by law (decision) on the corresponding budget as part of the departmental expenditure structure. This means that the budget law has an appendix called “Departmental structure of expenditures” and this appendix lists all the main managers of this budget and the expenditure classification codes associated with them (section, subsection, target item, type of expenditure). Each financial authority independently approves the codes of the main managers for its budget. In AS “Budget”, the abbreviation KVSR (departmental expense item code) is used to indicate the code of the main manager. You can also find the abbreviation PPP.

· Order of the Federal Treasury dated October 10, 2008 N 8n “On the procedure for cash services for the execution of the federal budget, budgets of the constituent entities of the Russian Federation and local budgets and the procedure for the implementation by territorial bodies of the Federal Treasury of certain functions of the financial bodies of the constituent entities of the Russian Federation and municipalities for the execution of the relevant budgets” (as amended July 30, December 25, 2009, October 29, 2010).

CVR 242 and 244: reflecting expenses in the field of information and communication technologies

Often in public sector institutions the question arises about attributing certain expenses to the field of information and communication technologies, which in turn are subject to payment at the expense of CVR 242. We will consider the procedure for attributing expenses to CVR 242 or 244 in this article.

We recommend reading: Vsk Accident Osago

In general, the possibility of using KVR 242 is provided for by the corresponding informatization plan. A similar opinion is expressed in paragraph 2 of the Submission of the Accounts Chamber of the Russian Federation dated November 25, 2020 No. PR 10-322/10-03, letters of the Ministry of Finance of Russia dated September 15, 2020 No. 02-05-10/59626, dated July 18, 2020 No. 02-05- 10/45717, letter of the Ministry of Finance of Russia and the Federal Treasury dated May 17, 2020 No. 09-01-08/30262/07-04-05/03-425.

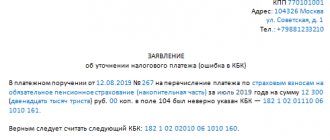

DECODING OF KBK CODES AND THEIR CLASSIFICATION 2019

- 1-3 Code indicating the addressee for whom the cash receipts are intended

- 4 Show a group of cash receipts

- 5-6 Reflects tax code

- 7-11 Elements revealing the item and subitem of income

- 12-13 Reflect the level of the budget into which funds are planned to be received

- 14-17 Indicate the reason for the financial transaction

- 18-20 Reflects the category of income received by a government department

KBK is an abbreviation for “budget classification code.” Budget classification codes are approved by the Russian Ministry of Finance. This is a long chain of numbers, representing a special code of 20 digits, which are combined into 7 groups. Each number in this sequence of numbers encodes a specific target group of budget revenues into the financial system of the Russian Federation.

“g) in the case of allocation of funds to the main managers, recipients and budgets of municipal districts and city districts of the Nizhny Novgorod region from the reserve fund of the Government of the Nizhny Novgorod region, the fund for the support of territories, subsidies and other interbudgetary transfers to the budgets of municipal districts and city districts allocated on the basis of legal acts of the Government of the Nizhny Novgorod region;

4) in paragraph 2.8, the words “in terms of classification codes of income, expenses and sources” are replaced with the words “in terms of classification codes of expenses and sources”, the words “control and accounts chamber of the Legislative Assembly of the Nizhny Novgorod region, the department of state financial control of the Nizhny Novgorod region” are replaced with the words “ Chamber of Control and Accounts of the Nizhny Novgorod Region";

In addition, this subsection includes expenses associated with the direction, management and provision of support for such activities as the development of general policies, plans, programs and budgets, as well as other activities in the field of national security and law enforcement activities not classified as other subsections.

This section also reflects expenses for the prevention and mitigation of the consequences of emergencies and natural disasters, civil defense, migration policy, applied scientific research in the field of national security and law enforcement, as well as other activities in this area.

DISPOSAL OF FIXED ASSETS.

Recognition of an asset is terminated in the event of disposal of property as a result of sale, conclusion of a lease agreement providing for the transfer of significant operational risks and benefits to the user (lessee), transfer to another public sector organization, other organizations free of charge, on other grounds involving termination of the right to operational management of property , as well as in case of disposal of property as a result of write-off.

Disposal of fixed assets is reflected in the credit of the corresponding balance sheet accounts of fixed assets.

When recording the disposal of fixed assets, the following criteria must be met:

1. The accounting entity has transferred all significant operational risks and benefits associated with the disposal (ownership, use) of the property reflected in the fixed assets.

2. The accounting entity no longer participates either in the disposal of the retired asset or in its actual use.

3. The amount of income (expense) from disposal of an asset can be reliably estimated.

4. The projected economic benefits or utility potential associated with the asset, and the costs incurred or expected, can be estimated reliably.

Income receivable on disposal of fixed assets is subject to initial recognition at fair value.

The financial result arising from the disposal of an asset is reflected as part of the financial result of the current period. It is defined as the difference between the disposal proceeds, if any, and the residual value of the fixed asset.

Justification of funding volumes by expenses

We report the following: The Budget Expenditure Classification Code (BSC) consists of 20 digits. The code for the functional classification of budget expenditures of the Russian Federation (KFKR) takes 14 characters, including:

section code – 4–5 digits;

subsection code – 6–7 digits;

target article code – 8–14 digits;

expense type code – 15–17 digits.

KTSSR - code of the target item for the classification of expenses (8–14 categories).

The rationale for this position is given below in the materials of the Glavbukh System

1. Recommendation: How recipients of budget funds can create balance sheet accounts for budget accounting

Attention: the recommendation was prepared taking into account the changes introduced by Order of the Ministry of Finance of Russia dated December 16, 2014 No. 150n.

Normative base

Budget accounting (including the formation of balance sheet accounts) is carried out by government institutions and other recipients of budget funds in accordance with the provisions of the Budget Code of the Russian Federation, Law of December 6, 2011 No. 402-FZ, Instruction to the Unified Chart of Accounts No. 157n, Instruction No. 162n, other regulatory legal acts regulating accounting.

This is stated in paragraphs 2, 21 of the Instruction to the Unified Chart of Accounts No. 157n, paragraph 4 of Order No. 162n of the Ministry of Finance of Russia dated December 6, 2010, paragraph 1 of Instruction No. 162n.

The unified chart of accounts was approved by order of the Ministry of Finance of Russia dated December 1, 2010 No. 157n. It is the basis for the formation of balance sheet accounts:

government bodies (state bodies), local government bodies;

management bodies of state extra-budgetary funds;

state and municipal institutions.

The procedure for applying the Unified Chart of Accounts is established by the Instructions approved by Order of the Ministry of Finance of Russia dated December 1, 2010 No. 157n (hereinafter referred to as the Instructions for the Unified Chart of Accounts No. 157n).

Account structure

All balance sheet accounts of the budget chart of accounts have 26 digits. The structure of any account is the same for all budgets. It is presented as follows:

| Rank | |||||

| 1–17 | 18 | 19–21 | 22 | 23 | 24–26 |

| Analytical code according to the classification criteria of receipts and disposals | Code of type of financial support (activity) | Synthetic account of an accounting object | Code for the classification of operations of the general government sector (KOSGU) | ||

| Synthetic account code | Analytical account code | ||||

| group | view | ||||

In categories 1–17, indicate depending on the situation:

budget income classification code (KDB);

code for classification of budget expenditures (KRB);

classification code for sources of financing the budget deficit (CIF).

Please indicate these codes in accordance with Appendix 2 to Instruction No. 162n. It should be taken into account that the codes in the account number are indicated without the classification of operations of the general government sector (KOSGU). After all, this code is indicated in the last digits of the account.

Digits 18 to 26 represent the nine-digit budget accounting account code.

In place of category 18, depending on the type of financial support (activity) under which this or that operation falls, indicate the following codes (KFO):

1 – activities carried out at the expense of the corresponding budget of the Russian budget system (budgetary activities);

3 – funds at temporary disposal.

The Treasury of Russia (financial authorities) to reflect cash service operations of budgetary and autonomous institutions, other non-profit organizations that are not participants in the budget process, indicate in place of the 18th category:

8 – funds of non-profit organizations on personal accounts (in terms of operations with the institution’s own funds, funds in temporary disposal and subsidies for the implementation of state or municipal tasks);

9 – funds of non-profit organizations in separate personal accounts (in terms of transactions with subsidies for the purpose of making capital investments and with subsidies for other purposes).

In place of categories 19–23, indicate the five-digit code of the synthetic account in accordance with the Unified Chart of Accounts.

In place of the last three digits 24–26, indicate the code for the classification of operations of the general government sector (KOSGU).

Such rules for the formation of accounts are established by paragraph 21 of the Instructions to the Unified Chart of Accounts No. 157n, paragraph 2 of Instructions No. 162n.

KRB structure

The twenty-digit code for the classification of budget expenditures (KRB) consists of three parts: * 1. Code of the main manager of budget funds. 2. Code of section, subsection, target item and type of expense. 3. KOSGU code for budget expenditures.

In the diagram it looks like this:

| Code of the main manager of budget funds | Section code | Subsection code | Target article code | Expense type code | Code of the article (subarticle) of the classification of operations of the general government sector related to budget expenditures | ||||||||||||||

| program (non-program) direction of expenses | subroutine | direction of expenses | group | subgroup | element | ||||||||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 |

| 1 | 2 | 3 | |||||||||||||||||

| Forms the 1st–17th digits of the account number | Not included in account number | ||||||||||||||||||

In place of categories 1–3, indicate the code of the main manager of budgetary funds.* The list of the main managers of funds from the federal budget and state budgets of extra-budgetary funds is given in Appendix 9 to the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n. The list of main managers of budget funds of a constituent entity of the Russian Federation (local budget) is established by law (decision) at the regional or local level.

In this case, the main manager of budget funds (federal, subject of the Russian Federation, local), who has the powers of the chief administrator of the revenues of a given budget, is assigned a code of the main manager corresponding to the code of the chief administrator.

This is stated in paragraph 2 of section III of the instructions approved by order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n.

The second part of the expense classification code takes 14 characters, including:

section code – 4–5 digits;

subsection code – 6–7 digits;

target article code – 8–14 digits;

expense type code – 15–17 digits.*

The classification of expenses contains 14 sections. Sections reflect the allocation of funds to perform the main functions of the state. In turn, the sections are detailed by hundreds of subsections, which specify the direction of budget funds to perform state functions within the sections. The codes of sections and subsections are given in Appendix 2 to the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n. The rules for allocating expenses to the relevant sections and subsections are established by subclause 3.2 of Section III of the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n.

Digits 8–14 form the code for the target expense classification item. In this case, digits from 8 to 9 form a code for the program (non-program) direction of expenses. Bit 10 – subroutine code. Digits from 11 to 14 are a code for the direction of expenses, which specifies (if necessary) individual activities. This is stated in paragraph 4.2.1 of section III of the instructions approved by order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n.

Codes of target items of the federal budget and budgets of state extra-budgetary funds are formed using the alphanumeric series: 1, 2, 3, 4, 5, 6, 7, 8, 9, B, G, D, F, I, L, P, F, Ts, Ch, Sh, E, Yu, Ya (clause 4.1 of section III of the instructions approved by order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n).

The lists and rules for the application of target items for the classification of expenditures of the federal budget and budgets of state extra-budgetary funds are established by subclause 4.2.2 of Section III of the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n. The list of universal areas of expenses that can be used in various target items is established by subclause 4.2.4 of Section III of the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n. The structure of linking universal areas of expenditure with the corresponding programs (non-program area of expenditure) is given in subclause 4.2.1 of Section III of the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n.*

The 15th–17th digits form the type of expenses. They detail the direction of financing budget expenditures for target items of the KRB. The list and rules for applying the types of expenses common to all budgets of the budget system are given in subclause 5.2 of Section III and Appendix 3 of the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n.

Such rules are established by subclause 5.1 of section III of the instructions approved by order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n.

The 18th–20th digits of the expense classification code contain the KOSGU code related to expenses (Appendix 4 to the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n).

The linkage between expense type codes and KOSGU codes is given in Appendix 5 to the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n (subclause 5.1 of Section III of the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n).

Creating an account with KRB

In the working chart of accounts, create a 26-digit budget accounting account from a 20-digit budget expense classification code as follows:

| Code of the main manager of budget funds | Section code | Subsection code | Target article code | Expense type code | Code of the article (subarticle) of the classification of operations of the general government sector related to budget expenditures | ||||||||||||||||

| program (non-program) direction of expenses | subroutine | direction of expenses | group | subgroup | element | ||||||||||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 (24) | 19 (25) | 20 (26) | ||

| Code of type of financial support (activity) | Synthetic account code | ||||||||||||||||||||

| accounting object | groups | kind | |||||||||||||||||||

| 18 | 19 | 20 | 21 | 22 | 23 | ||||||||||||||||

An example of the formation of a budget account by a government agency using a code for classifying expenses by budget

>What is CVR - general information, explanation of the concept.

RECOGNITION OF OBJECTS OF FIXED ASSETS.

In Section III of the Standard, the acceptance of fixed assets for accounting in institutions is designated by the concept of “recognition”. This does not change the essence of the provisions presented in it, which are partly similar to some provisions of Instruction No. 157n. Let's look at the main points of this section.

The unit of accounting for fixed assets in institutions (OS) is an inventory object. Each inventory item is assigned an inventory number in the manner established by the accounting policy of the institution, taking into account the provisions of the Standard and Instruction No. 157n. The inventory number is retained by the object for the entire period of its stay in the institution. After disposal of an object, the inventory number assigned to it is not assigned to anyone.

An OS object is recognized as an object of property with all fixtures and accessories, or a separate structurally isolated object intended to perform certain independent functions, or a separate complex of structurally articulated objects that constitute a single whole and are intended to perform a specific job.

A complex of structurally articulated objects is one or more objects of the same or different purposes, having common devices and accessories, common control, mounted in a single complex (on the same foundation), as a result of which each object included in the complex can perform its functions only as part of the complex , and not independently.

Fixed assets whose useful life is the same, and the cost is not significant (for example, library collections, peripheral devices and computer equipment, furniture used for the same period of time (tables, chairs, cabinets, other furniture used for furnishings) one room)), according to Instruction No. 157n, can be combined into one inventory object - a complex of OS objects.

A unit of fixed assets accounting can also be recognized as a part of a property. This is possible if part of the object has a different useful life from the remaining parts and its cost is significant.

A property (or part thereof) leased and intended for sublease may be recognized as investment property.

A cultural heritage asset is taken into account as part of the asset if it can be used to obtain economic benefits or useful potential, or if its useful potential is not limited to cultural value.

In other cases, a cultural heritage asset is reflected in off-balance sheet accounts at a conditional valuation of one ruble.

OS objects can be moved from one group to another (reclassified). The disposal of an object from one group and its inclusion in another group must be reflected in accounting simultaneously. Reclassification does not lead to a change in the value of fixed assets.

What is KVR - deciphering the concept

Regardless of the purposefulness of spending money from the state budget, municipal institutions are required to constantly monitor compliance with the targeted and targeted nature of spending the allocated money.

The use of classification in accordance with the requirements of Order of the Ministry of Finance No. 87-N allows you to accurately reflect the structure of the institution’s budget expenditures in the following points:

- Payments upon dismissal due to staff reduction or liquidation of an institution;

- Payment of contributions to social security, the compulsory medical insurance fund, and the Pension Fund;

- Dividing payments into cash or in kind;

- Division of payments taking into account the category of recipients;

- Allocations for payments to citizens in cases where there is no employment contract or similar documents;

- Provisions for business trips;

- Detailed description of budgetary capital expenditures;

- Provisions for administering the execution by authorities of various public obligations;

- Provisions for the payment of taxes.

Correct decoding of the CVR makes it possible to carefully and objectively analyze the expenditure of budget money.

Basic concepts of KVR and KOSGU

Starting from 2020, KOSGU is used only in work plans, reporting and accounting of government organizations and institutions. The KOSGU classification consists of the following groups:

- 100 – income;

- 200 – expenses;

- 300 – receipt of non-financial assets (NA);

- 400 – given to NA;

- 500 – incoming financial assets (FA);

- 600 – spent FA;

- 700 – emergence of new obligations;

- 800 – reduction in work commitments.

In 2020, state and government institutions began to use expense type codes (CWR), divided into several groups:

- Workers' compensation costs;

- Payment for goods, works and services necessary to meet government needs;

- Social and other payments to the population;

- Costs for major repairs of various state-owned facilities;

- Funds passed through interbudgetary transfer;

- Subsidy;

- Servicing the national debt, as well as other appropriations.

Classification of expenses by expense type codes when preparing reports is one of the responsibilities of municipal (state) institutions. Therefore, it is necessary to be extremely careful about the distribution of expenses into appropriate categories.

DISCLOSURE OF INFORMATION ABOUT PE IN THE REPORTING.

For each group of fixed assets, the following information is disclosed in the accounting (financial) statements:

a) the methods used to calculate depreciation;

b) applied methods for determining useful life;

c) the amount of the book value, as well as the amount of accumulated depreciation in combination with the amount of accumulated losses from impairment of fixed assets at the beginning and at the end of the period by groups of fixed assets;

d) reconciliation of the residual value at the beginning and end of the period.

Additionally, for each group of fixed assets, the following information is disclosed in the reporting:

- the presence and size of restrictions on property rights or other rights granted, including the value of real estate and especially valuable movable property that cannot be used by the accounting entity as security for obligations, as well as the residual value of fixed assets transferred as security at the beginning and end of the reporting period period;

- the amount of costs included in the cost of fixed assets during construction at the beginning and end of the reporting period;

- the amount of contractual obligations for the acquisition (construction) of fixed assets at the end of the reporting period;

- the amount of compensation due from third parties in connection with the impairment, loss or transfer of fixed assets included in income of the current period.

The following information is disclosed in relation to investment properties:

- description of investment properties;

- criteria for distinguishing between investment property and property occupied by an institution and property held for sale in the ordinary course of business;

- amounts recognized as income from the rental of investment property;

- amounts recognized as expenses (including repairs and ongoing operation) associated with investment real estate, income from the rental of which is reflected in the financial result of the reporting period;

- amounts recognized as expenses (including repairs and ongoing maintenance) associated with investment property that was not leased;

- the presence of restrictions regarding the possibility of selling investment real estate or receipts of economic benefits (income) from disposal, as well as the amount of these restrictions.

The explanatory note presented as part of the accounting (financial) statements additionally reflects the following information:

- on the balance sheet and residual value of temporarily idle fixed assets;

- on the book value of fixed assets that are in operation and have zero residual value;

- on the book value and residual value of fixed assets withdrawn from operation and held until their disposal.