Home / Taxes

Back

Published: 05/22/2020

Reading time: 7 min

0

96

The mineral extraction tax is levied on all subsoil users and is a federal tax.

- Legal and regulatory framework for mineral extraction tax

- Objects of taxation

- Taxpayers

- Mineral extraction tax rates

- Methods for calculating mineral extraction tax

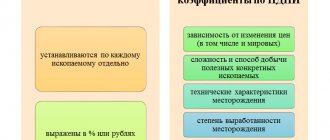

- Ktd coefficient

- Changes in the procedure for calculating mineral extraction tax regarding losses during oil production

- Other changes

- How to fill out a mineral extraction tax declaration

Dear readers! To solve your problem, call hotline 8 or ask a question on the website. It's free.

Ask a Question

What is the mineral extraction tax and who pays it?

The mineral extraction tax is a federal tax that is regulated by Chapter 26 of the Tax Code of the Russian Federation.

Also, its legal framework includes the Law of the Russian Federation “On Subsoil”. Taxpayers are organizations and individual entrepreneurs who are engaged in the extraction of mineral resources on the basis of a license. To extract minerals, you need to obtain a license to use a subsoil plot. After this, taxpayers must register with the tax office at the location of the site within 30 calendar days. If the site is located outside of Russia, then registration is carried out at the location of the organization.

Object of taxation[ | ]

The objects of taxation of the mineral extraction tax are recognized (Article 336 of the Tax Code of the Russian Federation):

- minerals extracted from the subsoil on the territory of the Russian Federation on a subsoil plot provided to the taxpayer for use in accordance with the legislation of the Russian Federation;

- minerals extracted from waste (losses) of mining production, if such extraction is subject to separate licensing in accordance with the legislation of the Russian Federation on subsoil resources;

- minerals extracted from the subsoil outside the territory of the Russian Federation, if this mining is carried out in territories under the jurisdiction of the Russian Federation (as well as leased from foreign states or used on the basis of an international treaty) on a subsoil plot provided to the taxpayer for use.

The following are not recognized as objects of taxation:

- common minerals and groundwater not listed on the state balance sheet of mineral reserves, extracted by an individual entrepreneur and used directly by him for personal consumption;

- mined (collected) mineralogical, paleontological and other geological collection materials;

- minerals extracted from the subsoil during the formation, use, reconstruction and repair of specially protected geological objects that have scientific, cultural, aesthetic, sanitary or other public significance. The procedure for recognizing geological objects as specially protected geological objects that have scientific, cultural, aesthetic, sanitary, health or other public significance is established by the Government of the Russian Federation;

- minerals extracted from the mine's own dumps or waste (losses) and related processing industries, if, when extracted from the subsoil, they were subject to taxation in the generally established manner;

- drainage groundwater not taken into account on the state balance sheet of mineral reserves extracted during the development of mineral deposits or during the construction and operation of underground structures;

- Coal bed methane.

What is covered by the mineral extraction tax?

The following minerals are considered the object of taxation:

- extracted from the subsoil on the territory of the Russian Federation;

- extracted from mining waste, subject to separate licensing;

- extracted from the subsoil outside the Russian Federation.

But there are also minerals for which there is no need to pay taxes. These include:

- common minerals. These also include groundwater extracted by an individual entrepreneur for personal consumption;

- mineralogical, paleontological and other geological collection materials;

- extracted from the subsoil during the use, reconstruction and repair of specially protected geological objects that have scientific, cultural, aesthetic, sanitary and other public significance;

- minerals extracted from their own dumps or waste.

Object of taxation of mineral extraction tax

The following minerals are recognized as the object of taxation:

- extracted from the subsoil on the territory of the Russian Federation on a subsoil plot provided by law (including from hydrocarbon deposits);

- extracted from waste (losses) of mining production, subject to separate licensing;

- extracted from the subsoil outside the Russian Federation in territories leased or used under international treaties, as well as under the jurisdiction of the Russian Federation.

The following are not subject to taxation:

- common minerals, incl. groundwater extracted by an individual entrepreneur and used directly by him for personal consumption;

- mined (collected) mineralogical, paleontological and other geological collection materials;

- extracted from the subsoil during the formation, use, reconstruction and repair of specially protected geological objects that have scientific, cultural, aesthetic, sanitary or other public significance;

- minerals extracted from the mine's own dumps or waste (losses) and related processing industries;

- drainage groundwater;

- Coal bed methane.

What are the tax rates?

There are two types of mineral extraction tax rates:

- Ad valorem rates are applied to the value of the extracted mineral. Calculated as a percentage.

- Specific rates are applied in relation to the amount of minerals extracted. Calculated in rubles per ton.

The rates themselves are regulated by Article 342 of the Tax Code of the Russian Federation.

But there are also pleasant sides. The tax has a zero rate. It is used for mining:

- mineral resources in terms of regulatory losses;

- associated gas;

- mineral resources in the development of substandard or previously written-off mineral reserves;

- groundwater extracted during the development of mineral deposits, as well as during the construction and operation of underground structures;

- mineral waters used for medicinal and spa purposes;

- groundwater used by the taxpayer for agricultural purposes;

- minerals that are extracted from overburden and host rocks, mining waste.

Tax rates

Rates are established for each type of minerals by Article 342 of the Tax Code of the Russian Federation.

Betting in 2020

- 0%.

- from 3.8% to 8% for various minerals, the tax base for which is determined based on their value;

- 919 rubles for the period from January 1, 2020 for 1 ton of extracted desalted, dehydrated and stabilized oil. In this case, the specified tax rate is multiplied by a coefficient characterizing the dynamics of world oil prices (Kts). The resulting product is reduced by the value of the indicator Dm, which characterizes the features of oil production. The value of the indicator Dm is determined in the manner established by Art. 342.5 Tax Code of the Russian Federation. The formula for determining the coefficient Dm was amended by the new edition of the Tax Code N 204 dated December 28, 2016: the value Kk was added, which reduces the indicator. Kk for the period from January 1 to December 31, 2017 inclusive is equal to 306, 357 - for the period from January 1 to December 31, 2020 inclusive, 428 - for the period from January 1 to December 31, 2020 inclusive, 0 - from January 1, 2020 . In 2016, the oil rate was 857 rubles;

- 42 rubles per 1 ton of extracted gas condensate from all types of hydrocarbon deposits. In this case, the specified tax rate is multiplied by the base value of a unit of standard fuel, by a coefficient characterizing the degree of complexity of extracting combustible natural gas and (or) gas condensate from hydrocarbon deposits, and by an adjustment coefficient;

- 35 rubles per 1,000 cubic meters of gas when extracting natural combustible gas from all types of hydrocarbon deposits. In this case, the specified tax rate is multiplied by the base value of a unit of standard fuel and by a coefficient characterizing the degree of complexity of extracting combustible natural gas and (or) gas condensate from hydrocarbon deposits. The resulting product is summed with the value of the indicator characterizing the costs of transporting natural combustible gas. If the amount received is less than 0, the tax rate is assumed to be 0.

- 47 rubles per 1 ton of mined anthracite.

- 57 rubles per 1 ton of mined coking coal;

- 11 rubles per 1 ton of mined brown coal;

- 24 rubles per 1 ton of mined coal, with the exception of anthracite, coking coal and brown coal;

- 730 rubles per 1 ton of multicomponent complex ore mined in subsoil areas located entirely or partially in the Krasnoyarsk Territory, containing copper and (or) nickel and (or) platinum group metals;

- 270 rubles per 1 ton of multicomponent complex ore not containing copper, and (or) nickel, and (or) platinum group metals, mined in subsoil areas located wholly or partially in the Krasnoyarsk Territory.

Tax rates for coal are multiplied by deflator coefficients, which are determined and subject to official publication in the manner established by the Government of the Russian Federation (Resolution of the Government of the Russian Federation of November 3, 2011 N 902 “On the procedure for determining and officially publishing deflator coefficients for the production tax rate minerals in coal mining").

Deflator coefficients for the 1st quarter of 2020 will be:

- for anthracite - 1.102;

- for coking coal - 1.668;

- for brown coal - 0.996;

- for coal, with the exception of anthracite, coking coal and brown coal - 1.132.

This was established by Order of the Ministry of Economic Development of Russia dated January 18, 2017 N 8 “On deflator coefficients for the mineral extraction tax rate for coal mining.”

Last year, the conditions under which the Kkan coefficient is equal to zero in relation to subsoil areas located entirely or partially in the Caspian Sea improved. These conditions are included in a separate subclause 9 of clause 4 of Article 342.5 of the Tax Code of the Russian Federation.

In relation to oil produced in these subsoil areas, the Kcan coefficient remains zero until the 1st day of the month following the one in which one of the circumstances listed in the Tax Code of the Russian Federation occurred. Such a circumstance is, for example, the achievement of a certain level of accumulated oil production (with the exception of the accumulated volume at new offshore fields in a given subsoil area). From 2020, this limit is 15 million tons instead of 10 million tons, as was previously established.

When calculating the mineral extraction tax on gas, the coefficient Kgp is used, which characterizes export profitability. Let us recall that the base value of the mineral extraction tax rate in relation to gas condensate from all types of hydrocarbon deposits is multiplied by the coefficient Kkm, as well as by the base value of a unit of standard fuel Eut and the coefficient Kc, characterizing the degree of complexity of extracting combustible natural gas and (or) gas condensate from hydrocarbon deposits raw materials.

The value of the correction factor has changed as amended by Federal Law No. 401-FZ dated November 30, 2016.

From January 1, 2020, paragraph 15 of Article 342.4 states that the Kkm coefficient is equal to the result of dividing the number 6.5 by the value of the Kgp coefficient. The Kgp new norm is set as follows: 1.7969 - for the period from January 1 to December 31, 2020 inclusive, 1.4022 - for the period from January 1 to December 31, 2020 inclusive, 1.4441 - for the period from January 1 to December 31 2020 inclusive - for taxpayers - owners of objects of the Unified Gas Supply System, or participants with an ownership interest;

For other taxpayers, Kgp is equal to 1.

What is the tax base?

The tax base is:

- quantity of minerals extracted during mining:

oil

- natural gas

- gas condensate

- coal

- multicomponent complex ores in the Krasnoyarsk Territory;

The tax base is determined by the taxpayer independently in relation to each mineral resource extracted. That is, if a company extracts marble and granite, then its own tax base is calculated for each.

The cost of extracted minerals is determined:

- based on the sales prices of extracted minerals;

- based on sales prices without taking into account subsidies from the budget to compensate for the difference between the wholesale price and the estimated cost;

- based on the estimated cost of extracted minerals.

Important

: the latter method of assessment is applied in the event that there is no sale of mineral resources in the corresponding tax period.

The tax base

The tax base for mineral extraction tax is determined as the cost of extracted minerals for each type, taking into account the various established rates. It is determined separately for each mined mineral.

The cost of hydrocarbon raw materials extracted from a new offshore hydrocarbon raw material field is determined in a special way. How to determine the tax base based on it is stated in Article 340.1 of the Tax Code of the Russian Federation. The federal executive body responsible for maintaining the state balance of mineral reserves informs the tax authorities about such deposits.

In relation to other types of extracted hydrocarbon raw materials, as well as coal, the tax base is determined as the amount of minerals extracted in physical terms.

The general procedure for assessing the value of extracted minerals when determining the tax base is specified in Article 340 of the Tax Code of the Russian Federation.

How to calculate the cost of extracted minerals?

It is easier to use special accounting programs and calculators here. The calculation mechanism itself looks like this:

- 1. We calculate the cost of the extracted mineral:

- 2. Unit cost can be calculated in two ways:

- 3. Revenue is calculated as follows:

Cost of extracted mineral = Quantity x Unit cost

Cost of a unit of extracted mineral = Revenue from sales ÷ Quantity sold

Or

Cost per unit of mineral extracted = Estimated cost ÷ Quantity extracted

Sales revenue = Price excluding VAT and excise duty – Amount of delivery costs

What else needs to be taken into account when determining the estimated value of extracted minerals? Direct and indirect costs.

Direct costs:

- material costs;

- labor costs;

- depreciation costs of fixed assets used in mining;

- amounts of insurance premiums.

Expenses for the tax period are distributed between the extracted minerals and the balance of work in progress.

Indirect costs:

- other material expenses;

- expenses for repairs of fixed assets;

- expenses for the development of natural resources;

- expenses for liquidation of fixed assets being decommissioned;

- expenses associated with mothballing and re-mothballing production facilities and facilities.

Indirect costs are distributed between the costs of mining and the costs of other activities of the taxpayer. The amount of indirect costs is fully included in the estimated cost of extracted minerals for the tax period.

Mineral extraction tax: rate

In addition to the period, the most important characteristic of this tax is its rate, which allows us to determine the size of the tax burden of economic entities.

Mineral extraction tax is subject to tax rates that vary depending on the type of resource, as well as the difficulty of obtaining it. The mineral extraction tax rate is reflected in Art. 342 of the Tax Code of the Russian Federation.

Let's look at some types of rates that apply to individual resources extracted from the subsoil. So, for example, in paragraph 1 of Art. 342 of the Tax Code of the Russian Federation provides for a zero rate for resources within the limits of their standard losses.

Companies and entrepreneurs receiving peat or shale are required to calculate tax at a rate of 4%.

For various types of standard non-ferrous metal ores, a rate of 4.8% is provided.

A rate of 6% is used when taxing bituminous rocks, and the extraction of non-ferrous and rare metal ores is taxed at a rate of 8%.

The full list can be found in Art. 342 of the Tax Code of the Russian Federation.

Thus, the specific value of the mineral extraction tax rate depends on the type of subsoil extracted by a company or entrepreneur.

When to pay tax?

At the end of the month, tax is calculated separately for each type of mineral resource extracted. The entire amount must be paid to the budget at the location of each subsoil plot provided to the taxpayer for use.

The tax is paid no later than the 25th day of the month following the expired tax period.

The tax return for mineral extraction tax is submitted for each period to the tax authorities at the location or place of residence of the taxpayer. This must be done no later than the last day of the month following the expired tax period.

The amount of tax on minerals mined outside of Russia is subject to payment to the budget at the location of the organization or the place of residence of the individual entrepreneur.

Procedure and deadlines for tax payment, reporting

At the end of the month, the amount of tax is calculated separately for each type of extracted minerals. The tax is payable to the budget at the location of each subsoil plot provided to the taxpayer for use.

The tax is paid no later than the 25th day of the month following the expired tax period.

Subsoil users pay regular payments quarterly no later than the last day of the month following the expired quarter, in equal shares in the amount of one-fourth of the payment amount calculated for the year (RF Law of February 21, 1992 N 2395-1).

The procedure and conditions for collecting regular payments for the use of subsoil from subsoil users are established by the Government of the Russian Federation, and the amounts of these payments are sent to the federal budget.

The mineral extraction tax declaration is submitted to the tax authority at the location of the Russian organization, the place of residence of the individual entrepreneur, the place of activity of the foreign organization through branches and representative offices established on the territory of the Russian Federation.

The obligation to submit a tax return arises starting from the tax period in which the actual extraction of mineral resources began. Submitted no later than the last day of the month following the expired tax period. The tax return for mineral extraction tax can be submitted both in paper and electronic form.

Please pay attention!

Taxpayers whose average number of employees for the previous calendar year exceeds 100 people, as well as newly created organizations whose number of employees exceeds the specified limit, submit tax returns and calculations only in electronic form. The same rule applies to the largest taxpayers.

More information about submitting electronic reporting

A complete list of federal electronic document management operators operating in a certain region can be found on the official website of the Office of the Federal Tax Service of Russia for the constituent entity of the Russian Federation.

What are the features?

For some types of minerals, special rules for calculating the mineral extraction tax have been established. All of them are enshrined in the Tax Code of the Russian Federation.

- Peculiarities of oil taxation - Article 342.5 of the Tax Code of the Russian Federation.

- Peculiarities of gas taxation - subparagraphs 2, 13, 18 and 19 of paragraph 1 of Article 342 of the Tax Code of the Russian Federation.

- Features of taxation of coal - Article 343.1 of the Tax Code of the Russian Federation.

- Features of taxation of precious metals - Article 342.3 of the Tax Code and Federal Law No. 41-FZ “On Precious Metals and Precious Stones”.