Accounts receivable inventory

“Accounting in budgetary and non-profit organizations”, 2012, N 24

Article 12 of the Federal Law of November 21, 1996 N 129-FZ “On Accounting” provides for the mandatory inventory of property and liabilities in non-profit organizations, which is not only the most important measure of economic activity organization, but also an element of its accounting policy.

On January 1, 2013, Federal Law No. 402-FZ dated December 6, 2011 “On Accounting” (hereinafter referred to as Law No. 402-FZ) comes into force. Article 11 of Law N 402-FZ also obliges non-profit organizations to conduct an inventory. All property and all types of financial obligations of the organization are subject to inventory.

The procedure for conducting an inventory is defined in the Guidelines for the inventory of property and financial obligations, approved by Order of the Ministry of Finance of Russia dated June 13, 1995 N 49. To carry out an inventory, a permanent inventory commission is created in the organization.

Before conducting an inventory, the manager issues an order indicating the timing of the inventory, the property being inspected and obligations, as well as the personal composition of the inventory commission. The unified order form is form N INV-22, approved by Resolution of the State Statistics Committee of Russia dated August 18, 1998 N 88 “On approval of unified forms of primary accounting documentation for recording cash transactions and recording inventory results.”

An inventory of settlements is carried out in order to document the existence of receivables and obligations, establish the timing of their occurrence and repayment, and clarify the assessment. When making an inventory of settlements, the status of settlements is checked for each debtor and creditor (for each buyer, customer, supplier, contractor), for each contract, for each employee, accountable person, for each tax and the budget to which it is paid. Before starting an inventory of settlements with debtors, it is necessary to draw up a debt reconciliation report between organizations. The reconciliation report is drawn up for each debtor in two copies. The first copy remains in the accounting department, and the second is sent to the debtor with whom the reconciliation was carried out.

An inventory of settlements with banks and other credit institutions, with the budget, accountable persons, employees, other debtors and creditors, a cash inventory consists of checking the validity of the amounts listed in the accounts. Inventory of settlements with suppliers (contractors) and buyers (customers) is a check of the validity of the amounts reflected in accounts 60 “Settlements with suppliers and contractors”, 62 “Settlements with buyers and customers”, 76 “Settlements with various debtors and creditors”, etc. .

Based on debt to employees of the organization, unpaid amounts of wages that are subject to deposit are identified, as well as the amounts and reasons for overpayments to employees.

When inventorying accountable amounts, reports of accountable persons on advances issued are checked, taking into account their intended use, as well as the amount of advances issued for each accountable person (date of issue, intended purpose). When inventorying receivables, the inventory commission must establish the size of receivables, including those confirmed and not confirmed by debtors.

To document the results of the inventory of settlements with buyers, suppliers and other debtors and creditors, an act in form N INV-17 is used. It is formed on the basis of a certificate drawn up by type of debt in the context of synthetic accounts.

The act specifies:

- name of the debtor's organization;

- accounting accounts in which the debt is recorded;

- amounts of debt agreed and not agreed with debtors;

- amounts of debt for which the statute of limitations has expired.

Based on the results of the inventory, receivables for each obligation, taking into account the repayment period and based on the terms of the concluded agreements, can be classified as debt for which the repayment period has expired or has not yet occurred.

The signing by the debtor of the act of reconciliation of mutual settlements interrupts the limitation period for the debt recognized by him. After a break, the limitation period begins anew; the time elapsed before the break is not counted towards the new period (Article 203 of the Civil Code of the Russian Federation).

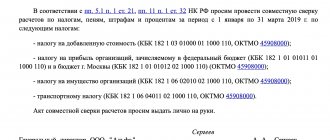

Before drawing up annual financial statements, it is necessary to reconcile calculations for taxes and duties with the tax authority, the results of which are formalized in an act of joint reconciliation of calculations for taxes and duties, penalties and fines in the form approved by Order of the Federal Tax Service of Russia dated August 20, 2007 N MM-3-25/ [email protected]

From the financial statements for 2011, non-profit organizations are required (in the presence of doubtful debts of debtors) to form a reserve for doubtful debts.

If during the year an organization does not reflect a reserve for doubtful debts in its accounting accounts and reporting, it faces a fine of 10,000 rubles. (in subsequent periods for this violation the fine increases to 30,000 rubles).

If the amount of the unformed reserve is more than 10% on balance sheet lines 1230 “Accounts receivable”, 1370 “Retained earnings” (uncovered loss), a fine of 2,000 to 3,000 rubles will be imposed on the official responsible for accounting.

An organization's receivables are considered doubtful if they are not repaid or with a high degree of probability will not be repaid within the time limits established by the agreement and are not secured by appropriate guarantees.

At the end of the reporting period, from the moment the decision to form a reserve is made, it is necessary to consider each counterparty individually.

All counterparties of the organization can be divided into reliable (whose reputation for solvency has been formed over the years), ordinary, unreliable and critical.

Doubtful debts are also subject to a certain gradation:

- receivables not repaid within the period established in the agreement;

- receivables for which payment has not yet become due, but the probability of late payment is high.

Receivables that are not repaid within the time period established in the contract are included in the reserve in full, and receivables that have not yet become due for payment, but the probability of late payment is high, are determined by expert means. Accounting can use a scale used to create a reserve for doubtful debts:

- if the expected delay in payment is no more than 30 days, 10% of the debt amount will be included in the reserve for doubtful debts;

- if the expected delay in payment is from 30 to 90 days - 30%;

- if the expected delay in payment is from 90 to 180 days - 60% of the debt, etc.

The accounting entry to the debit of account 91 “Other expenses” and the credit of account 63 “Provisions for doubtful debts” in the context of each counterparty forms the total amount of the reserve.

If the counterparty pays its debt (part of the debt) to the organization, the reserve will be restored to the amount of payment, taking into account the coefficient or percentage that was applied when creating the reserve in relation to this counterparty. In this case, reverse wiring is done: D-t. 63 “Provisions for doubtful debts” Account. 91 “Other income”.

The write-off of a bad debt, previously recognized as doubtful in accounting, for which a reserve was formed, is reflected in the debit of account 63 “Provisions for doubtful debts” in correspondence with account 62 “Settlements with buyers and customers” (or accounts 60, 66, 67 and 76) .

A bad debt in an amount exceeding the reserve created for this debt is written off as a debit to account 91 “Other income and expenses.”

This reflection in accounting complies with the norms of clause 70 of the Regulations on accounting and financial reporting in the Russian Federation, approved by Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n (hereinafter referred to as Order N 34n), according to which, if before the end of the reporting year following the year creating a reserve for doubtful debts, this reserve will not be used in some part, then the unspent amounts are added to the financial results when drawing up the balance sheet at the end of the reporting year.

In the financial statements, accounts receivable are reflected minus the amount of the created reserve.

Accounts receivable for which the statute of limitations has expired, and other debts that are unrealistic for collection, are written off for each obligation and are credited accordingly to the reserve for doubtful debts or to increase expenses of a non-profit organization (clause 77 of Order No. 34n).

Write-off receivables must be reflected in off-balance sheet account 007 and in a certificate of the presence of valuables recorded on off-balance sheet accounts for 5 years from the date of write-off.

To carry out its business activities, an organization has to purchase various goods, materials, and services from other organizations—suppliers. To summarize information on settlements with suppliers and contractors in accounting, account 60 “Settlements with suppliers and contractors” is used. This account displays data on payments to suppliers for:

— inventory items received, work performed, services consumed;

— surplus inventory items identified during acceptance;

— transport services;

— inventory items, works or services for which payment documents have not been received from suppliers.

All transactions related to settlements for acquired material assets, accepted work or consumed services are reflected in account 60 “Settlements with suppliers and contractors”, regardless of the time of payment.

Analytical accounting for account 60 “Settlements with suppliers and contractors” is maintained for each submitted invoice, and settlements in the order of scheduled payments are maintained for each supplier and contractor. At the same time, the construction of analytical accounting should ensure the possibility of obtaining the necessary data on: suppliers on accepted and other payment documents for which the payment period has not yet arrived; to suppliers for payment documents not paid on time; to suppliers for uninvoiced deliveries; advances issued; to suppliers on bills issued, the payment period of which has not yet arrived; to suppliers for overdue bills of exchange; to suppliers for received commercial loans, etc.

Accounting for settlements with suppliers and contractors within a group of interrelated organizations, about the activities of which consolidated financial statements are prepared, is maintained on account 60 “Settlements with suppliers and contractors” separately.

Settlements with suppliers can be carried out both in non-cash form - through a current account, and in cash, as a rule, through the organization's cash desk. When making such payments, both receivables and payables may arise.

When accounting for settlements with suppliers, it is first necessary to ensure:

— the correctness of execution of contracts with suppliers, compliance of the terms of the contract with respect to delivery time, quantity, cost and other conditions of the actual situation;

— compliance of settlements, regardless of the form (which can be either monetary or non-monetary) with suppliers, with the current legislation of the Russian Federation;

— the correctness of the reflection of the transaction in accounting, the correspondence of this data to the received primary documentation;

— ensuring timely repayment of accumulated receivables or payables;

— timely write-off of overdue debts.

The main task of conducting an inventory is to establish by the inventory commission, through documentary verification, the correctness and validity of the amounts of receivables and payables listed in the accounting records, including receivables and payables for which the statute of limitations has expired.

When conducting an inventory of settlements with suppliers, reconciliation reports are drawn up, which are intended to analyze the status of settlements, identify debts, overpayments and the sources of their formation. These acts are drawn up for each counterparty, and they can be generated both for all contracts concluded with the supplier, and for each contract separately, for the audited period. The act also contains data on the status of settlements at the beginning of the period, turnover for the period - separately the occurrence of debt and separate repayment, as well as debt at the end of the period of formation of the reconciliation act. This act is signed by representatives of both organizations, certified by seals and includes information about the status of the verified payments from the supplier. If discrepancies with supplier data are identified, it is necessary to identify the reasons for the discrepancies and make the necessary corrections. The balance at the end of the period must match the supplier's data.

It is also necessary to check the following types of calculations:

- in situations where the goods have been paid for, payment documents for them have been received, but they themselves have not yet been delivered by the supplier, i.e. are on the way;

- in situations where payment and settlement documents have not been received for goods and services received - uninvoiced deliveries.

During the verification of settlements with suppliers for goods in transit, it is necessary to identify their quantity and value, the results obtained must be entered into the “Act of Inventory of Inventory in Transit” ( form INV-6) .

When taking inventory of settlements with suppliers for uninvoiced goods, it should be remembered that such deliveries are accepted for accounting at the price specified in the contract, and subsequent clarification of the cost is assumed.

Regardless of the moment of receipt of payment and settlement documents, received inventory items must be capitalized during an inventory of calculations, the quantity and cost of these assets is determined on the basis of the “Acceptance Certificate of Materials” in form No. M-7 , “Act of Acceptance of Goods Received Without supplier accounts" in the form TORG-4 .

In accordance with the Instructions for the use of the Chart of Accounts, accounting for such transactions can occur in the usual manner, i.e.:

- Debit 10 “Materials”, 41 “Goods” - Credit 60 “Settlements with suppliers and contractors” - reflects the debt to the supplier for received materials and goods.

- Or using account 15 “Procurement and acquisition of material assets” and 16 “Deviation in the cost of material assets.” However, the use of this accounting method by enterprises in practice is not common.

If it is necessary to adjust the cost of received uninvoiced inventory items upon receipt of payment and settlement documents, the following entries must be made in accounting:

Debit 10 “Materials” subaccount depending on the type of material Credit 10 “Materials” subaccount “Uninvoiced materials” - reflects the cost of uninvoiced materials after receiving payment and settlement documents from the supplier;

The amount of debt to the supplier is adjusted by one of the following entries:

Debit 10 “Materials”, subaccount “Uninvoiced materials” - Credit 60 “Settlements with suppliers and contractors”;

Debit 60 “Settlements with suppliers and contractors” - Credit 10 “Materials”, subaccount “Uninvoiced materials”.

If, during the inventory, accounts payable with an expired statute of limitations were identified in the accounting records, the following entry must be made:

Debit 60 “Settlements with suppliers and contractors” - Credit 99 “Profits and losses”.

All results obtained when conducting an inventory of settlements with suppliers and contractors are entered into the “Act of Inventory of Settlements with Buyers, Suppliers and Other Debtors and Creditors” in the INV-17 form .

What is debt inventory?

The procedure involves reconciliation with counterparties in order to clarify the amounts of the parties’ obligations to each other, as well as to identify overdue debts.

In the “receivables” part, debts and advances to:

- suppliers and contractors;

- staff;

- accountables;

- founders;

- budget and extra-budgetary funds.

When taking inventory of accounts payable, the following is determined:

- obligations to pay for goods (works, services) received;

- debt to personnel;

- status of settlements with the budget;

- status of settlements for deliveries of goods received from counterparties on account of advances.

To carry out an inventory, the head of the company must form an inventory commission operating on a permanent basis with the specified composition. To do this, an appropriate order should be issued. The commission can include employees of accounting departments, administrative departments or audit structures. If the volume of liabilities and assets is small, the audit commission has the right to carry out the procedure.

The procedure for conducting an inventory of receivables and payables must be prescribed in the accounting policies of the organization.

The objectives of the inventory are:

- documentary evidence of the amounts of existing debt;

- an assessment of how likely the debt is to be repaid.

What are the goals of the remote sensing inventory?

Carrying out an inventory of remote control should help solve problems such as:

- Determining the actual presence of debt in an enterprise - it is necessary to make sure that the amounts of debts reflected in accounting and reporting are real and are actually existing debts (and not, for example, the result of accounting errors or slow reflection of data in accounting).

IMPORTANT! When carrying out an inventory of remote control, the debit balance of not only account 62 is analyzed, but also other accounts intended for accounting for settlements with contractors and personnel: 60, 70, 71, 73.

How to analyze accounts receivable, read in this material.

- Identification of counterparties that are not actually debtors: for example, if the same counterparty has both receivables and comparable payables and it is possible to set off. Offsetting homogeneous claims

- Reflection of correct inventory data in enterprise accounting.

For more information on how to reflect inventory results, see the article “Reflecting inventory results in accounting .

- Development of methods for obtaining (collecting) actually existing doubtful debts:

- claim work;

- agreeing on the possibility of installment plans or debt restructuring with the counterparty;

- lawsuits if pre-trial measures have not yielded results;

- possibility of selling debts.

- Identification of a debt that can no longer be collected, for example, the statute of limitations has passed (Article 196 of the Civil Code of the Russian Federation) or the debtor organization has been liquidated (Article 419 of the Civil Code of the Russian Federation). Such debt then undergoes a separate write-off procedure.

When receivables are considered overdue, find out here.

- Based on the results of the inventory, a set of measures for effective control and management of remote sensing in the future can also be developed and implemented.

IMPORTANT! In addition to balance sheet accounts, the inventory of receivables must also cover off-balance sheet accounts. Account 007 is intended to record written off bad debts for which there may still be a chance to receive something. When drawing up an overall picture of debts, data on account 007 should also be taken into account.

How is inventory carried out?

The procedure for conducting an inventory of receivables and payables was approved by order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49 (clauses 3.44-3.48). During the event, the inventory commission is obliged to:

- establish the correctness of the organization’s settlements with contractors, hired personnel, the state budget, and founders;

- determine the validity of debt for shortages and thefts listed in the accounting accounts;

- establish the real amount of receivables and payables (including those with an expired statute of limitations).

During the inventory, you need to check the account “Settlements with suppliers and contractors”. Special attention is paid to the analysis of information about goods that have already been paid for, but are still “on the road.” You should also examine the status of settlements with suppliers for uninvoiced deliveries.

An inventory of debt to employees involves identifying unpaid amounts of wages that are subject to transfer. They also analyze the amounts of overpayments to workers and the reasons for such overpayments.

When checking accountable amounts, members of the commission study the reports of accountable persons on advances issued. The amounts of advances issued for each accountant are checked.

It is imperative to clarify the amount of debt to the tax service and banks.

If, during the inventory, discrepancies were discovered in the amounts of debt between the organization’s data and the data of its counterparties, which had not been eliminated at the date of drawing up the balance sheet, each party shows in the balance sheet those amounts of debt that can be confirmed by accounting data. To resolve disagreements, you should contact the relevant authorities (arbitration court, etc.).

How to spend

To analyze the real volumes of accounts receivable, you need to reconcile the calculations for each counterparty.

It is required to review each agreement and each basis for legal relations with the debtor, be it a supply agreement, provision of services or performance of work.

Traditional accounting accounts, which reflect settlements with counterparties, are:

- 60;

- 62.

If during the verification of information any inaccuracies were identified, the enterprise is obliged to make appropriate adjustments and reflect the changes in the month in which they were identified.

At this stage, it is extremely important to correctly determine the amount of doubtful and overdue debts, as well as to determine whether a reserve for doubtful debts is available for formation.

Each debit amount on the above accounts (in terms of the specific reasons for the appearance of receivables) must be analyzed for its doubtfulness.

In addition to the debts of counterparties, accounts receivable for payment of labor activities, as well as for money issued on account, are also subject to inventory.

Inventory on the following basis is carried out according to the following accounts:

- 70;

- 71.

They usually check whether the company’s employees were fired during the last period, which employees did not report on advances issued, etc.

At the final stage, debit balances on accounts 68 and 69 are subject to analysis in order to identify overpayments to extra-budgetary and tax funds.

Documenting

The verification results are usually recorded in the inventory report in form No. INV-17 and the certificate attached to it. Documents should be filled out carefully, without marks. You can use blue or black ink, or fill out inventory documents using a computer. The organization must have all primary documents confirming the occurrence of the debt specified in the act.

The act reflects information about the “debtor” and “creditor” in the context of accounting accounts, the amount of debt and the date of its occurrence. The document contains information about the type of debt: confirmed or not confirmed by debtors (creditors), including those with an expired statute of limitations.

The attached certificate includes information deciphering the debt data given in the inventory report:

- name and address of each debtor (creditor);

- for what and from what time the debt is registered;

- amount of debt;

- name and details of the document confirming the existence of the debt.

Additionally

Because the inventory of settlements with debtors and creditors is carried out, among other things, to identify doubtful and hopeless obligations, it makes sense to add additional information to the appendix to the act.

1. To establish doubtful obligations:

- the period of overdue payment in days;

- availability of collateral.

In the line “What is the debt for?” a mark is placed: whether debt obligations are associated with the sale of goods, services and works or not, because this criterion is the most important condition for classifying a debt as doubtful.

2. To uncover bad debts:

- the beginning of the countdown of the limitation period (in most cases, this date does not coincide with the period of occurrence of the debt, which is determined by the terms of the agreement);

- information about the interruption of the limitation period (date and basis);

- data on the expiration of the limitation period (including interruption);

- reasons why the debt is considered bad.

The above information will help you easily calculate the amount of doubtful accounts receivable in order to create reserves for doubtful debt obligations, as well as establish the amount of bad debt for subsequent write-off. In addition, the results of checking the calculations will be very useful in the process of managing the company.

What accounts are analyzed during inventory?

To identify the actual size of receivables, the calculations are reconciled for each debtor and agreement separately. Members of the commission analyze the status of settlements on the following accounts:

- “60” (amount of advances paid);

- “62” (customers’ debt for goods and “69” (overpayment of taxes, contributions to extra-budgetary funds and other payments);

- “70” (overpayment of wages);

- “71” (amounts reported, but not confirmed by advance reports);

- “75” (the amount of debt that the founders did not pay for contributions to the authorized capital);

- “76” (claims presented to suppliers; the amount of VAT calculated upon receipt of advances).

To obtain information on accounts payable, records on the credit of accounts are analyzed:

- “60” (amount of debt for goods received and (amount of advances received from buyers);

- “66” (liabilities for uncovered loans and borrowings, interest to credit institutions);

- “68”, “69” (debt for transfer of taxes and insurance contributions);

- “70” (the amount of accrued but not paid wages, vacation pay, etc.);

- “71” (amounts of cash overexpenditures according to advance reports);

- “75” (amount of dividend payment debt to the founders);

- “76” (debt to other counterparties; VAT accepted for deduction when paying advances to suppliers).

The procedure for writing off accounts payable

The write-off process also contains several steps:

- Drawing up documentation confirming the fact of delay.

- The amount to be paid is agreed upon.

- The delivery note is being checked.

- The work completion certificate is being checked.

- Documentation is drawn up to allow the debt to be verified.

- An inventory of settlements with debtors and creditors is compiled.

- Documents are certified by the General Director.

Inventory of calculations: procedure and timing of inventory

As a general rule, before drawing up the final financial statements for the year, the organization is obliged to conduct an inventory of total assets and liabilities (clause 27 of the Regulations on accounting and financial reporting in the Russian Federation, approved by order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n), in particular settlements with debtors and creditors.

In addition, the inventory can be carried out in other cases by decision of the manager. Such a case, for example, could be the preparation of reports for a potential investor or board of directors, at which strategic issues of the company’s development will be decided.

At the same time, it is important for the company to objectively understand what volumes of debt receivable can be counted on and in what period, as well as what the actual volumes of the company’s creditors to counterparties are. In other words, it is necessary to correctly conduct an inventory of settlements with debtors and creditors.

Inventory of calculations consists of reconciling the values listed in the relevant accounting accounts, assessing the validity of their reflection, as well as checking the debt for overdue status.

The inventory of settlements is carried out within the time limits specified in the internal document (clause 2.1 of the Methodological Instructions for Inventory, approved by Order of the Ministry of Finance of Russia dated June 13, 1995 No. 49).

In order to carry out an inventory of payments, the company, as a general rule, must form a special inventory commission operating on an ongoing basis (clause 2.2 of the Methodological Instructions). Such a commission may include employees of the administrative departments of the company, accounting, as well as other departments (legal, financial, etc.). At its discretion, the company has the right to include employees of audit structures (both internal and external) in the commission.

The inventory of settlements is formalized by order of the manager (form INV-22), which, in particular, indicates the grounds for its implementation, the timing, and the composition of the commission.

IMPORTANT! If at least one member of the commission is not present during the actual inventory, the results of such an inspection will be considered invalid (clause 2.3 of the Guidelines).

After reconciling settlements with debtors and creditors and identifying the current scale of debt, the company must correctly document the results of the inventory of settlements. For this purpose, unified forms of primary documents are provided in the appendices to the Methodological Instructions.

One of these forms (Appendix 16) is the act of inventory of settlements with suppliers, buyers and other debtors and creditors (Form INV-17). It is advisable for the company to formalize the results of checking the volume of debt with this act.

If an inventory of calculations is carried out before preparing annual reports, then its results must be reflected in the financial statements for the year. If the inventory of calculations is carried out for other reasons, then its results are subject to reflection in the accounting and reporting of the month in which it was completed (clause 5.5 of the Methodological Instructions approved by Order of the Ministry of Finance of Russia dated June 13, 1995 No. 49).

We carry out an annual inventory of obligations and reflect it in accounting

Before drawing up annual financial statements, an inventory of the organization's assets and liabilities is carried out.

In particular, an inventory of obligations must be carried out no earlier than December 1 <*>.

The inventory of obligations consists of several stages.

Stage 1. We check the correctness and validity of the calculation amounts that are listed in the accounting records <*>

| Checking calculations | Check | Verification process and required information |

| With banks and other organizations | 66, 67 | We check documentation for obtaining loans and borrowings |

| With a budget | 68 | We compare accounting data with data from tax returns, insurance reporting and check the transferred amounts |

| With FSZN | 69 | |

| With Belgosstrakh | 76-2 | |

| With buyers, clients | 62 | We check contracts and primary accounting documents (TTN, TN, acts, payment orders, bank statements and other documents) for the fulfillment of obligations |

| With suppliers, contractors | 60 | |

| With other debtors and creditors | 76 | |

| With accountable persons | 71 | We check: — primary accounting documents (advance reports and cash receipts); — compliance of issued and returned funds with accounting data; — targeted use of the amounts spent; — availability of supporting documents; - amounts for which the deadline for submitting reports has expired |

| With employees | 70, 73 | We check: — primary accounting documents (salary statements, personal accounts, etc.); — the presence of wages not paid to employees on time due to their failure to appear and undeposited; — presence of amounts of deposit debt for which the statute of limitations has expired |

| With the founders | 75 | We check: — constituent documents; — minutes of meetings of participants (founders); — cash and bank documents, invoices, acceptance certificates and other documents confirming settlements with the founders for contributions to the authorized funds and for the payment of income to them |

Note: It is better to reconcile settlements with counterparties on accounts 60, 62 and 76 in advance (as of November 1) and draw up settlement reconciliation reports <*>.

The organization can develop the form of the statement of reconciliation of calculations independently. The prepared document is signed by the manager. Usually it also includes the signature of the chief accountant to confirm the information specified in the act. If the organization works using a seal, then you can put its stamp in the statement of reconciliation of calculations. But not necessarily. But it is necessary to include in the act information about contracts and primary accounting documents on the basis of which the debt arose. This will give the act legal force <*>.

To reconcile settlements with banks, data from bank statements on loans provided is compared with data from accounts 66 “Settlements for short-term loans and borrowings” and 67 “Settlements for long-term loans and borrowings”. To do this, the bank issues statements to the organization as of January 1. The organization confirms the data in them in writing <*>.

To check the calculations with the budget, you also need an extract. Only from tax authorities’ accounting data on calculated and paid amounts of taxes, fees (duties), and penalties. To receive it, the organization submits a written application to the tax authority at the place of registration <*>.

Bilateral reconciliation statements are not drawn up with employees and accountable persons.

During the verification of calculations, errors may be identified. They are corrected in accordance with Ch. 4 NAS N 80. An accounting certificate-calculation is prepared <*>.

Correction of errors is reflected by additional accrual or reduction of liabilities <*>.

Stage 2. Determine the status of the debt : current, overdue, expired, impossible (unrealistic) for collection.

To do this you need:

— establish the date and reasons for the formation of the debt;

— analyze the terms of settlement agreements, etc.;

— if necessary, check the data on the location of the counterparty in the process of liquidation and request information from the Unified State Register.

Stage 3. We check the correctness and validity of other types of obligations and reserves for upcoming expenses <*>

| Verifiable obligations | Check | Verification process and required information |

| Reserves for future expenses established by law and the organization’s accounting policies | 96 | We check: — formation of reserves; — use of reserves according to estimates and calculations; - other |

Stage 4. We draw up the inventory results

Based on the results of the inventory, an inventory of calculations report, form 14-inv, and a certificate for it are drawn up. Identified debts with an expired statute of limitations are written off on the basis of a decision made by the manager <*>. Write-off of accounts payable is reflected as follows:

| Wiring | Contents of operation |

| Dt 60, 62, 66, 67, 76, etc. - Kt 90-7, 91-1 | Accounts payable with an expired statute of limitations that arose in connection with the implementation of current, investment or financial activities were written off |

The write-off of accounts receivable depends on whether a reserve for doubtful debts has been created <*>:

| Wiring | Contents of operation |

| Dt 63 - Kt 62 | Bad accounts receivable are written off against the allowance for doubtful debts |

| Dt 90-10 - Kt 62 | Write-off of the balance of bad receivables if the amount of the created reserve was not enough |

| Dt 90-10, 91-4 - Kt 62, 60, 76, etc. | Write-off of bad receivables if no reserve for doubtful debts was created |

| Dt 007 | The written-off amount is taken into account on the balance sheet for 5 years from the date of write-off |

Note: Inventory results are reflected no later than December 31 <*>.

Identified errors must be corrected in tax accounting : recalculate the tax base and submit declarations with the changes and additions made.

If the written-off accounts payable have expired, they must be taken into account when taxing profits as part of non-operating income <*>.

Losses from writing off accounts receivable are included in non-operating expenses <*>.

Inventory of settlements with debtors and creditors

Sample order for inventory of receivables and payables

The norms of domestic legislation establish the obligation for enterprises to conduct an inventory of settlements with debtors and creditors, tangible and intangible assets, fixed assets and inventory items. The order and procedure for conducting such inspections have been developed by government bodies of the Russian Federation and are mandatory both when assigning activities and when they are carried out or completed.

Inventory of receivables and payables (sample act INV-17)

An inventory of calculations must be documented after all operations to identify current DZ and KZ are completed. For this purpose, an act of inventory of settlements with buyers and customers, suppliers and other debtors and creditors should be generated in the INV-17 form or a form independently developed by the organization, as well as a certificate - an appendix to the act. Moreover, such an act must be drawn up in two copies.

The settlement inventory report in form INV-17 can be downloaded on our website.

The completed settlement inventory report must be signed by the responsible members of a specially created commission.

Inventory

The Federal Law “On Accounting” calls an inventory of an organization’s assets and liabilities as one of the elements of accounting.

Paragraph 3 of Article 11 of the said normative act provides for the following types of inspections:

- mandatory inventory of accounts receivable and other assets;

- initiative reconciliation carried out by an enterprise at its own request without instructions from the law.

The Ministry of Finance of the Russian Federation, by its Order dated June 13, 1995 N 49, introduced the Methodological Instructions. Clause 1.5 provides a whole list of cases when an inventory is mandatory, for example:

- the enterprise transfers property for temporary use, lease, buys or sells it;

- this check is carried out before the formation of the annual report;

- conducting an inventory of receivables and payables, as well as assets, is mandatory in the event of appointing a new person responsible for the safety of inventory items;

- force majeure circumstances resulting in loss of assets;

- detection of loss, damage or theft of inventory items;

- if the owners of the legal entity have decided on its voluntary liquidation.

Each enterprise has the right to assign and conduct an inventory at other times not related to the events specified above.

It should be borne in mind that the responsibility for taking inventory of debtors and creditors, as well as the assets of the enterprise, rests exclusively with legal entities. Individual entrepreneurs do not have to check the compliance of actual indicators with accounting data.

It is important to note that the norms of domestic legislation do not limit the maximum number of inventories carried out by an economic entity during a calendar year.

Types of debt

Carrying out an inventory of settlements with debtors and creditors will reveal whether you have outstanding debt obligations subject to penalties. In addition, you should make sure that this debt is accounted for correctly, since it comes in several types:

- short-term (delay less than 1 year);

- long-term (non-payment longer than 12 months);

- overdue (counted separately).

In the process of checking settlements with banking institutions, credit agreements are first checked. Among other things, when taking inventory of settlements with creditors and debtors, the following agreements (if any) are checked:

- rent;

- commissions;

- assignment of rights of claim (cession);

- instructions.

Carrying out an inventory

In accordance with paragraph 2.2 of the Methodological Instructions put into effect by Order of the Ministry of Finance of the Russian Federation dated June 13, 1995 N 49, each enterprise that intends to conduct an inventory must create an appropriate commission and appoint its members from among the organization’s employees. It is allowed to involve third-party auditors.

Without compliance with this instruction, the inventory of debt, as well as other indicators, will not be considered completed. This body is permanent and operates until the expiration of its appointment or until the formation of a commission with a new composition.

It is important to take into account that, provided that the volume of liabilities and assets is small, the audit commission can conduct an inventory.

The creation of a commission is formalized by an order to conduct an inventory of receivables. It is important to take into account that the publication of another administrative document is allowed.

order to conduct an inventory of receivables and payables

The results of the inspection should be reflected in the inventory records. These forms must be filled out carefully, without erasures or blots, on the computer or by hand. Acceptable ink colors:

In blank lines, dashes are placed, and the forms themselves are signed by all members of the relevant commission.

Regardless of the inventory object, the requirements indicated above are general and mandatory. Their strict observance will significantly reduce the risks of claims regarding the procedure and registration of the inspections carried out.

Order for inventory of receivables and its sample

An order to conduct an inventory check is issued and signed by the head of the institution.

The order must contain the following provisions:

- that the manager orders an inventory check to be carried out;

- about what exactly should be inventoried;

- timing, procedure and provision of final results;

- composition and head of the inventory commission.

Note! Information on the procedure for carrying out an inventory can be included directly in the order, or it can be issued in a separate act attached to the order.

Speaking of commissions. A local regulatory act may establish a permanent commission for inventory activities.

If one is created, the order may not indicate the name list of persons taking part in it. It is enough to make a reference to the corresponding local act.

In the same case, if the composition of the commission is approved each time before an inventory check, the order must contain a complete list of persons, indicating their full names and positions.

The order must also contain:

- an indication of the person responsible for control over the inventory;

- signature of the manager, transcript of the signature, date of signing the document.

A standard sample of an inventory order can be found at this link.

act of inventory of settlements with suppliers and customers. Form and form INV-17

Sample of filling out the unified form INV-17 in 2020

Help supplement to form INV-17

Sample of filling out the certificate

Download sample forms for inventory at the enterprise: INV-1 Inventory listINV-1a Inventory list of intangible assets INV-3 Entering data into the inventory list INV-4 Inventory of shipped ]INV-5 Inventory of goods and materials accepted for storage[/anchor] INV-6 Inventory of goods and materials on the wayINV-15 Inventory of cash availability INV-18 Comparison sheet of inventory resultsINV-19 Comparison sheet of inventory items INV-22 Order for inventory INV-26 Accounting for inventory resultsHow is an inventory of materials carried out?