What has changed in the rules for SZV-M

The unified form of monthly pension reporting in the SZV-M form is familiar to all accountants, without exception.

This report has been submitted to the Pension Fund of the Russian Federation for more than two years. However, as of October 1, 2018, officials approved a number of innovations in the procedure for preparing and submitting pension reporting. The key change is that the procedure for submitting reporting information to the Pension Fund has been adjusted. Now the report is considered submitted if an official notification is received from the Pension Fund of Russia about its acceptance. That is, if the organization submitted the report on time (by the 15th day of the month following the reporting month), but the notification was not received, then the SZV-M is considered not submitted. In this case, the institution faces a fine of 500 rubles for each insured person in an unaccepted reporting form.

Another important innovation: the Russian Ministry of Labor resolved disputes that lasted several years. In Letter No. 17-4/10/B-1846 dated March 16, 2018, officials approved that information on the sole founder of the company must be submitted to the Pension Fund. That is, if the organization does not have employees, and there is only one general director, who is the sole founder, then information must be submitted to him.

Let us recall that the current procedure, approved by Order of the Ministry of Labor dated December 21, 2016 No. 766n, was adjusted by Order of the Ministry of Labor of Russia dated June 14, 2018 No. 385n. The changes come into force on 10/01/2018.

General information about the SZV-STAZH report

“SZV-STAZH” documentation means a separate type of report that must be submitted to the Pension Fund of the Russian Federation at the place of registration in order to provide the fund with information about the hired persons for whom the company makes insurance contributions. This form is a successor to the RSV-1 form.

It is also appropriate to note such a report as SZV-M, which is structurally and semantically closely correlated with SZV-STAZH. However, the second form contains more complete information regarding staff representatives, revealing not only general information about the subject, but also specifying the frequency of his work with the employer in question, taking into account the periods when he was actually on the staff of the enterprise, but did not perform prescribed duties (vacations, sick leave sheets, etc.).

The deadline for submitting SZV-STAZH is until March 15 annually. That is, in 2020, these reports must be submitted exclusively before the specified date, Friday, March 15. If the specified date falls on a weekend, the report must be submitted on the next next working day.

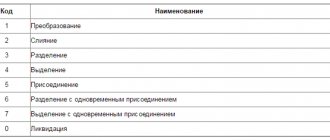

The algorithm for registration of SZV-STAZH consists of the following stages:

First of all, you need to identify the insured. It is assumed that at the top of the report you should enter information about its name, individual registration number assigned to the Pension Fund of the Russian Federation, as well as Taxpayer Identification Number (for individual entrepreneurs) and checkpoint for legal entities.- Below is a line to indicate the reporting calendar year.

- Next, you should record information about the direct work activities of specific personnel representatives. It is important to emphasize that the person responsible for drawing up the document must be familiar with the list of codes that are designed specifically to simplify the subsequent verification and classification of papers. This list is given in the instructions for filling out the SZV-STAZH.

- Information about contributions accrued for employees. Moreover, this block of the document is drawn up only in those circumstances when the subject is applying for a pension. Completing this section involves checking the appropriate boxes.

Among other things, it is important to emphasize that the submitted SZV-STAZH form does not imply the presence of adjustments or corrections; the report must initially be drawn up correctly and in accordance with all the rules for the official execution of such documents. However, as practice shows, quite often mistakes are made at enterprises due to the presence of the human factor. This may be the reason for a negative response from the employees of the Pension Fund of the Russian Federation regarding the acceptance of the report, or for modifications.

Pension Fund error codes

| Error code | What is the problem |

| 20 | The TIN control digits of an individual must be a number calculated using the algorithm for generating the TIN control number. |

| The TIN element of the insured person must be completed. | |

| 30 | The SNILS contained in the insurance certificate is indicated. |

| The full name contained in the insurance certificate is indicated. | |

| The status of the ILS in the “Insured Persons” register as of the date of the document being checked should not be equal to the value of “UPRZ”. | |

| At least one of the Last Name or First Name elements must be specified. | |

| 50 | The file being checked must be a correctly filled XML document. |

| The file being checked must comply with the XSD schema. | |

| The electronic signature must be correct. | |

| Element "Registration number". The number under which the policyholder is registered as a payer of insurance premiums is indicated, indicating the codes of the region and district according to the classification adopted by the Pension Fund. | |

| The taxpayer identification number must be indicated in accordance with the Pension Fund data. | |

| When providing information about insured persons with the “initial” form type, there should not be previously provided information with the “initial” type for the reporting period for which the information is provided. | |

| The period for providing SZV-M must be no earlier than April 2016. | |

| For all types of SZV-M forms, the reporting period for which the form is submitted must be less than or equal to the month in which the audit is carried out. |

How to fix error code 30 in SZV-STAZH

The solution to error 30 in SZV-STAZH lies in submitting to the Pension Fund of Russia an additional SZV-STAZH report with the “Additional” type for those employees for whom the Pension Fund of the Russian Federation did not accept data. The remaining employees for whom no errors were identified do not need to be included in this report. The “additional” report must be sent within five working days after receiving the protocol with the detected error.

If your report included only one insured person, and it resulted in error code 30 in SZV-STAZH, then there is no point in sending a “supplementary” report. In this case, it is necessary to fill out SZV-STAZH with the “Initial” type with the correct data, as well as ODV-1 with the “Initial” type.

If you discovered error code 30 in SZV-STAZH using special programs, then you are not constrained by the 5-day period. Correct all errors in the basic report and send it to the Pension Fund. This will be enough to solve the problem.

Correcting errors in SZF-STAZH

What happens if you send corrections before notifying the Pension Fund

So, there are two ways to correct an error in reporting:

- on its own initiative, that is, when the institution independently identified an inaccuracy and sent corrective information to the Pension Fund;

- or the error was identified by the Pension Fund, then the inaccuracy must be corrected within 5 business days from the date of receipt of the notification from the Pension Fund.

IMPORTANT! The “5 working days” rule now applies only to those errors pointed out by regulatory authorities. It will not be possible to correct other defects. There will be penalties for “newly discovered” errors.

How to act before notifying the Pension Fund of the Russian Federation about an error in SZV-M? Self-identified inaccuracies can be corrected without a fine only if two conditions are met: the report with the error was submitted in a timely manner and accepted by the Pension Fund, and the organization independently sent corrective information to the Pension Fund of the Russian Federation before notification.

If you forgot an employee, you can avoid a fine only if you submit an additional report form before the 15th. If you do this later, you cannot avoid a fine.

Advice: generate and submit reports in the SZV-M form before the due date (15th day of the month following the reporting month). This way, the organization will have more time to correct inaccuracies and errors without applying penalties.

General rules for passing SZV-M

Information about insured individuals in the SZV-M form (approved by Resolution of the Pension Fund of the Russian Federation Board dated 01.02.2016 No. 83p) must be submitted to the Pension Fund by the results of each month by all policyholders. That is, all organizations that have full-time and freelance workers (insured persons). The form includes information about all insured individuals who perform work on the basis of employment or civil law contracts.

It does not matter whether the organization carried out actual activities or not, and whether there were payments to people in the reporting month or not. You must submit the SZV-M form in any case. This follows from the provisions of paragraph 2.2 of Article 11 of the Law of 01.04.1996 No. 27-FZ.

SZV-M is handed over to the territorial offices of the Pension Fund of the Russian Federation at the place of registration of the policyholder, that is, the employer organization.

The form can be submitted:

- on paper or electronically – if the number of individuals included in the report is less than 25 people;

- only in electronic form – if the number of people included in the report is 25 or more.

SZV-M is submitted monthly, no later than the 15th day of the month following the reporting month (clause 2.2 of Article 11 of Law No. 27-FZ dated 04/01/1996).

Errors with code 10, 20

These are the most harmless mistakes that an insured can make. Therefore, if they are available, the report is still considered submitted.

If the SZV-M inspection protocol contains warnings with code 20, this means that there was:

- <or> the TIN of the insured person is incorrectly specified, which is checked using the TIN control number;

- <or> the TIN of the insured person is not indicated at all.

If the TIN of the insured person is indicated incorrectly

Despite the fact that the report was accepted by the Pension Fund, it is better to correct the incorrect TIN. To do this, you need to simultaneously submit two SZV-M forms: canceling (with the “cancel” type) and supplementing (with the “addition” type). In the first, indicate the data on an individual with an incorrect TIN, and in the second, indicate the data on him, but only correct ones. It is safer to correct all shortcomings before the end of the reporting campaign, i.e. before the 10th day of the next month (in 2020 - before the 15th day). If this is not done, then for each “erroneous” employee you will have to pay 500 rubles. fine (Article 17 of Law No. 27-FZ).

Note! It is quite possible that in order to correct the TIN, your Pension Fund branch will only need to receive one complementary form instead of two. This point should be clarified with fund specialists.

Example. The accountant of Retro LLC in SZV-M for December 2020 mistakenly swapped the last two digits in the TIN of Igor Semenovich Parfenov. It should be 760700613663, but he wrote down 760700613636. See below how the accountant corrected the error.

You can find out a person’s TIN at. Follow the “All services” link on the main page. From the proposed list of electronic services, select “Find out TIN”. Fill in the full name, date and place of birth, and passport details of the citizen. After submitting your request, you will receive his TIN. If the identification number is missing, it means the person did not apply to the tax authority to obtain it.

If the TIN of the insured person is not indicated

This situation is possible if the “physicist” did not provide his TIN. Therefore, the policyholder simply has nothing to record in the corresponding column of the form and leaves it blank. In accordance with paragraph 3, paragraph 2.2, Article 11 of Law No. 27-FZ, the TIN of the insured person in the SZV-M is optional and is indicated only if available. Therefore, even if the Pension Fund warns about the absence of such information in the report, nothing needs to be corrected.

Note! An employer does not have the right to demand a TIN from an employee just because he now provides such information to the Pension Fund. The list of mandatory documents for employment is defined in Article 65 of the Labor Code of the Russian Federation. And the TIN certificate is not named in it.

By the way, if the policyholder has data on the TIN of the citizens working for him, but does not indicate it in the report, then the Pension Fund of the Russian Federation will definitely reveal this when reconciling with the tax authorities. Then there is a high probability that the payer of contributions will be fined under Article 17 of Law No. 27-FZ for unreliability of the information provided (). Therefore, if information about the TIN is available, it must be included in the form. This is the requirement of clause 3, clause 2.2, article 11 of Law No. 27-FZ.

How to make an RSV adjustment

Question: The employee works under a GPC agreement, the agreement with him was signed on December 25, 2018, and payment was made on January 10, 2019.

Insurance payments were accrued in December, the DAM report was completed for the year, and 6-NDFL appears in the report for the first quarter. How to adjust the RSV? Answer: No adjustment is required. The payment date is the day the employee is accrued. If remuneration and contributions from it are accrued in the 2018 calculation period, then they must be reflected in the DAM for 2020. The situation is different with the calculation of personal income tax. The date of receipt of income is the day of payment or transfer to the taxpayer’s account. Therefore, for remuneration accrued in December but paid in January, tax must be withheld on the day of payment and transferred no later than the next day. Since these actions were carried out in the tax period “2019”, they are reflected in the calculation of 6-personal income tax for the first quarter of 2020.

Question: We passed the zero RSV. The founder and general director of the enterprise are the same person; he did not enter into an employment contract with himself, so he was not paid a salary. The Federal Tax Service inspector said that it is necessary to submit the RSV adjustment. Will it be correct to reflect the director as an insured person in the DAM?

Answer: Labor relations arise as a result of appointment to a position or confirmation in a position - in your case they arose due to the fact that the founder appointed himself as a director (Article of the Labor Code of the Russian Federation). In accordance with the laws on compulsory insurance, the general director is insured. Therefore, in lines 160, 170 and 180 of subsection 3.1 of section 3, the attribute “1” should be indicated. The number of insured persons in line 010 in Appendices 1 and 2 to Section 1 must be equal to one. If there are no payments, subsection 3.2 of section 3 is not completed.

Question: It is necessary to submit the DAM adjustment for 2018, since accruals under the GPC agreement for five employees were taxed not at 10%, but at 22%. What sections need to be adjusted when correcting the amount of the base and contributions for employees so that there is no doubling of accruals for employees with the adjustment in the Federal Tax Service base?

Answer: In the updated calculation in Section 3 for these employees, it is necessary to reduce the amount of the base (columns 220 and 230) and the amount of contributions (column 240). Payments that exceed the maximum base amount and contributions calculated from them are not reflected in the personalized information. In subsection 1.1 of Appendix 1 to Section 1, amounts that exceed the maximum base value must be indicated in line 051, and contributions from these amounts at a rate of 10% - in line 062. Contributions in line 061, accrued at a rate of 22%, must be reduced by the corresponding amount and adjust the values in lines 030–033 of section 1 in accordance with line 060 of subsection 1.1. In order for the updated calculation to be correctly loaded into the Federal Tax Service database, you need to change the adjustment number in line 010 of section 3 from “0” to “1”, and in line 040 leave the number that was in the primary calculation.

Question: In the first quarter the company was on the simplified tax system, so they passed the DAM with tariff code “02”, and in the second quarter the company switched to OSNO. Do I need to make an adjustment to the DAM for the first quarter with code “01” and recalculate contributions?

Answer: Tariff codes “02” and “01” are used by insurance premium payers who apply the basic tariff established by Art. 425 Tax Code of the Russian Federation. Since the tariff rates for these codes are the same, and the amounts of the base and calculated contributions were not underestimated, there is no need to recalculate the contributions. But it is better to submit an updated calculation with tariff code “01” without section 3, since nothing changes in the personalized information. This will avoid misunderstandings if the Federal Tax Service checks calculations on a cumulative basis from the beginning of the year by tariff code.

Question: Is it necessary to submit an adjustment according to the DAM if an employee from Armenia has been assigned the status “Equal to citizens of the Russian Federation”, but the VPNR code was mistakenly entered in the IS?

Answer: The category codes of the insured person NR (hired employee) and VPNR (temporarily staying in the territory of the Russian Federation) refer to the same tariff for calculating pension contributions. An error in specifying the code does not lead to an underestimation of the calculated contributions to the compulsory pension insurance, so you can do without adjustments. But please note that if you use a program to fill out the calculation, which is configured to auto-calculate indicators of other subsections depending on the category, then the VPNR code may lead to distortion of the amounts:

- payments in subsection 1.2 (temporarily staying foreigners are not insured in the compulsory medical insurance system);

- social insurance contributions for temporary disability and in connection with maternity in Appendix 2 (temporarily staying foreigners contributions are calculated at a rate of 1.8%, not 2.9%).

Question: The employee’s last name in SNILS was entered with an error. He changed the documents and reported this to the Federal Tax Service, but recently it turned out that in the DAM report it goes through twice: once with the correct data, the second time with incorrect data. We sent an adjustment to include this employee in Section 3 twice: with the wrong last name (zero amounts) and with the correct last name. Now the accruals for the “wrong” employee have been reset to zero, but he is still listed in the Federal Tax Service database, so the number of insured persons between the company and the tax office does not agree. How to submit an RSV adjustment?

Answer: In order for an individual’s data to be permanently deleted from the Federal Tax Service database, it is necessary to indicate the sign “2” in adjustment section 3 (with an adjustment number other than zero) with zero amounts in lines 160, 170, 180 - not insured.

Question: An individual employee worked unofficially for an individual entrepreneur from 11/01/2006 to 06/01/2018. Now he is retiring, and he needs to include this period in his length of service. The contributions have been calculated, paid to the MRI, and now you need to submit a report with adjustments for 2020. How to fill out the DAM adjustment for previous years, where to indicate this employee and how to assign his length of service?

Answer: For each reporting period from 2006 to 2016, you need to submit information about the employee using the SZV-KORR form with the “OSOB” type, where you indicate the amounts of payments, accrued contributions and periods of service. In the adjusting RSV-1 for 2020, additional accrued contributions must be reflected in line 120 of section 1 and in section 4 (section 6 should not be included in the adjusted calculation). For 2020 and 2020, information about periods of work must be submitted for the employee using the SZV-STAZH form with the “Additional” type. And information about the amounts of payments and contributions must be reflected in the updated calculations for insurance premiums (submitted to the Federal Tax Service for each reporting period of 2020 and for the first quarter and half of 2020) in section 3 of the employee.

Reporting on employees: mass operations and filters.

To learn more

Errors with code 30, 40

If the policyholder received an inspection report from the Pension Fund of Russia with error code 30, it means that inaccuracies were made when indicating the full name and/or SNILS of the individual. They must be written down exactly as on the insurance certificate. In this case, the report is considered partially accepted, i.e. the program will allow employees with correct information to pass, but not those with incorrect information.

Notice! The TIN in SZV-M is optional, but the SNILS of the insured person must always be present (clause 2 and clause 3, clause 2.2, article 11 of Law No. 27-FZ). This is how the Pension Fund identifies a person. Therefore, indicate it without errors.

The fine for incorrect SNILS and/or full name is 500 rubles. for each employee (Article 17 of Law No. 27-FZ).

You can check the correctness of SNILS on the website of the FSS of Russia. To do this, you need to enter an 11-digit number without spaces or dashes into the search form. However, this check will not provide any other data, such as full name, amount of pension savings, etc. An employer cannot independently find out SNILS via the Internet, for example, as an INN based on the full name and passport data of an individual, since this is confidential information.

To correct an erroneous SNILS, you need to submit a canceling and supplementing SZV-M on the same day. The first report cancels all incorrect information, the second one adds new information. Although local fund specialists note that it is enough to submit only the form with the “additional” type (read, for example,). So it is better to consult your Pension Fund branch on this issue.

Corrections must be completed by the 10th day (before the 15th day in 2017) of the month following the reporting month. If the policyholder does not make it on time, then penalties will be applied to him under Article 17 of Law No. 27-FZ.

An incorrect full name can be corrected in the same way. By the way, the last name, first name and patronymic must be entered in the nominative case. Otherwise the program will throw an error. But extra dots and spaces in your full name will no longer interfere with passing the SZV-M.

Note! If the policyholder incorrectly indicated both SNILS and full name and TIN for the same individual, then the fine will still be 500 rubles, since the sanctions are established by Article 17 of Law No. 27-FZ in relation to each insured person with false information, and not in regarding each deficiency.

The program will show an error with code 30 even if the SZV-M contains only the last name of the insured person, but not the first name.

Also, information on an employee will not be accepted if the status of his individual personal information in the “Insured Persons” register on the date of the document being checked is equal to the value of “UPRZ”. The value "UPRZ" is assigned to an insurance number when it becomes irrelevant (i.e. when it is discontinued).

Types of errors in SZV-M, how to decipher codes and correct errors

Hello! In this article we will talk about common errors in SZV-M and the rules for eliminating them.

Today you will learn:

- How to decipher error codes;

- What errors will the protocol be accepted with?

- How to avoid paying fines for mistakes.

- The employee's full name is indicated in Latin letters;

- an empty column for entering a TIN;

- the letter “е” is printed;

- use of open/close quotes, parentheses, hyphens, apostrophe and other special characters;

- an error in the first name, last name or patronymic associated with the use of letters from two alphabets: Latin and Russian;

- dot among the letters full name;

- error in TIN;

- no middle name.

Features of SZV-M adjustment

Any enterprise is obliged to make pension contributions to the Pension Fund. This rule also applies to the activities of individual entrepreneurs.

Regardless of the employee’s form of work, payments must be made. Contributions to the Pension Fund are mandatory for all employees: employed, part-time or under contract. Since they receive official earnings, the employer must ensure timely payments to the extra-budgetary fund.

Data on employees is generated in the form of a report, which is sent to the fund. The document can be created electronically or on paper. The latter option can only be used by a company whose number of employees does not exceed 24 people. If the staff consists of 25 or more hired employees, then an electronic report is generated.

What to do with a specific type of error

There are several codes that contain a decoding of the error made. For each type of inaccuracy, the system assigns a certain score, which should be taken into account to correct specific errors. To make this information easy to understand, we have prepared a table for you.

Code Protocol Status What needs to be done

10 – 20PositiveThe document is accepted

Repeated submission of the report is not typical. This means that SZV-M will be received with errors. Errors are minor or non-existent.

20 - 30 Positive Pension Fund Form accepted

It is necessary to correct only the mistakes made and resubmit the report only for employees whose information has been corrected

30 – 40PositiveReport is partially taken into account

It is necessary to correct all incorrect data on employees and send only corrected information for verification

50PositiveRefusal to accept the form

Any inaccuracies should be corrected and the report sent again.

If the encoding is 10 or 20, then such a report is accepted by the fund and does not require any clarification.

These numbers may draw your attention to minor inaccuracies, taking into account which you will need to submit the form for the next month. The protocol is a kind of assessment of the work of the employee who generated the report.

It identifies errors in the SZV-M form and dictates consequences for supplementary or secondary reports.

Errors 30 and 40 imply resending the report only for employees whose information contained errors. An error with code 50, identified during the check, means that your report has not been accepted in full, and you need to redo it again for all insured personnel.

Codes 10 - 20

Let's look at which sending errors are encrypted under the numbers 10 - 20:

The organization that compiles the report does not always have all the data on employees. The most common example is the lack of a TIN. His employee may simply forget to bring it; it is also possible that the number is not in the tax office database.

In this case, no information is entered in the report, that is, the columns remain empty. The system will send the code with an error, but this does not mean that you need to insert zeros into the columns. This will also be considered an error.

If the employer has data on the TIN of employees, then they must be maintained correctly. This follows from the fact that the Pension Fund contains all the data on the company’s employees. And if the fund is aware that the employee has a tax identification number, but you did not indicate it, then such an invoice will not be accepted.

Another common reason for cats 10 - 20 is a mistake in the surname in SZV-M. Use only letters of the Russian alphabet.

Error code 30 - 40

The list of inaccuracies, encrypted under the digital interval 30 - 40, is as follows:

- large space between words;

- a period placed after the surname;

- the hyphen is surrounded by a space;

- a hyphen placed after the full name;

- the checkpoint is incorrectly marked;

- SNILS number is not true;

- the numbers indicating the line number are not in ascending order;

- zeros instead of TIN;

- missing first or last name;

- space before the TIN or SNILS number.

To clarify the correctness of the entered SNILS, you can go to the website of the insurance fund. In the “Benefits” section you will enter 11 digits, and the system will produce a result that will tell you whether such SNILS is in the database.

You will not receive any information about the employee, knowing his SNILS number, from this request to the site. This is considered confidential information. In other words, you can only find out whether such a combination of numbers actually exists.

SZV-M error code 50

If the protocol is negative with number 50, then the form contains the following errors:

- incorrect structure of the file itself;

- electronic signature is not in the correct format;

- The TIN of an individual entrepreneur or company contains numbers that do not correspond to reality;

- in the adjusted report, instead of the mark “additional”, “output” is indicated;

- incorrect numbers in the registration number assigned by the Pension Fund;

- error in the period (the reporting period is indicated incorrectly (for the next month, for example).

The report is sent in the form of an XML document, which must include:

- registration number of the fee payer;

- code of the Pension Fund that accepts the form;

- date of compilation (first put the year, then the month and day);

- an identifier that allows you to determine the degree of uniqueness of the compiled electronic form.

What is provided for those who made a mistake

Inaccuracies when sending a report are punishable by fines. If the Pension Fund does not accept your form, then expect penalties.

The fine amount is 500 rubles. It is charged for each employee for whom there is an inaccuracy. No matter how many errors there are in the report for one employee, the amount of the fine does not change. And if you made gross errors about 10 employees in one report, then you will pay 500 * 10 = 5000 rubles. Errors in the process of processing the report are summed up for each employee.

If the company has a small number of employees, then the fine will not be impressive. But for companies with several dozen people on their staff, this amount can be large. Therefore, carefully fill out all the fields to avoid unpleasant consequences.

Penalties for errors are assessed not only for the codes specified in the protocol, but also for late submission of the report. Try to approach the question of filling out the form in advance.

How to fix errors without penalties

To prevent the system from giving you a negative protocol, follow the recommendations:

- Submit your report strictly before the 15th;

- Correctly use the marks “iskhd”, “o;

- To preview the generated report and eliminate errors during verification, download the free program owned by the Pension Fund of Russia - CheckPFR. The download link can be found on the PF website. The SZV-M error will be identified by you even before sending the report. Changes are periodically made to the program, so do not forget to update it on your computer in a timely manner.

Source: https://IDeiforbiz.ru/vidy-oshibok-v-szv-m-kak-rasshifrovat-kody-i-ispravit-oshibki.html

Error code 50

These are the most dangerous mistakes. If they are in the inspection protocol, then the report has not been accepted (even partially). The SVO will need to be corrected and resubmitted for the same month.

Critical errors with code 50 include the following:

1. Incorrect policyholder registration number; it must contain codes that indicate that the company belongs to a specific region of the Russian Federation (the first 3 digits of the number) and the district of this region (the second 3 digits) in accordance with the classification of the Pension Fund of Russia.

On a note! The registration number is taken from the notification that the Pension Fund issues when registering as an insurer. But if you don’t have it at hand, you can find out the number using the electronic service “Business risks: check yourself and your counterparty.” To do this, in the search form, a legal entity will need to enter their OGRN or TIN, and an individual entrepreneur/peasant farm will need to enter their OGRN or TIN, or full name and region of residence.

2. Incorrect TIN of the policyholder; it must correspond to the number contained in the Pension Fund database.

3. Re-submission of SZV-M for the reporting period with the form type “source” in the case where the primary report for the same period was successfully accepted by the Pension Fund. In other words, for each month the policyholder can submit only one initial SZV-M form. And if he received a positive report, then the report was verified. In the event that something needs to be corrected in the information already submitted, canceling (with the “cancel” type) and/or supplementing (with the “additional” type) forms for the same period are submitted.

4. Indication of the reporting period earlier than April 2020. For the first time in 2020, SZV-M had to be completed in April. Therefore, there simply cannot be a report for a month earlier than indicated.

5. Indication of the reporting period later than the current month. That is, SZV-M cannot be imagined for the future. The deadline for reporting is the current month. It is not necessary to wait for it to complete. The form can be submitted early.

A few more serious errors of a purely technical nature, due to which SZV-M will not be accepted:

- incorrect filling of the XML document;

- the file does not comply with the XSD schema;

- incorrect electronic signature.

How to find out whether a report has been accepted or not

If errors are detected in the information provided, the program will generate a protocol indicating the result of the check.

Let's use an example to clarify.

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

Example

After submitting the SZV-TD for April 2020, TransStroy Logistics LLC received an inspection report from the Pension Fund of Russia. It indicated that the report did not pass format-logical control (check code AF.SH 1.1 error 50 in SZV-TD).

A protocol with such text means that the Pension Fund did not accept the submitted SZV-TD and the errors need to be corrected.

With the AF.SH 1.1 verification code, the XSD error may be:

- in the format of the entered data (for example, extra spaces, hyphens, zeros, etc. crept into the indicators);

- inaccurately entered information (incorrect registration number or TIN);

- unfilled sections in the required details (for example, the code of the territorial body of the Pension Fund of the Russian Federation is not specified separately).

HR specialists identified an error (an extra zero was indicated in the company registration number), issued a new SZV-TD and submitted it to the fund.

Thus, the protocol received from the Pension Fund of Russia is the main source of information about whether the SZV-TD was accepted or not.

Next, we will tell you how to understand why the report was not accepted and where to look for the error.

Form

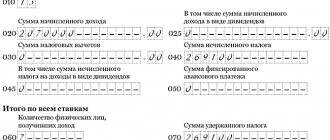

The SZV-M form was developed at the end of January.

Form SZV-M in Word(doc) 77 kb.

Form SZV-M in Excel (xls) 34 kb.

Example (sample) of filling out SZV-M:

Form SZV-M in Word(doc) 77 kb.

Form SZV-M in Excel (xls) 34 kb.

How to fill it out?

Registration number in the Pension Fund of Russia, INN and KPP (it is only for organizations, individual entrepreneurs are not needed) - you can also find out.

Employees' full names must always be entered in full.

Check your SNILS well, because for an error even in 1 digit there is a 500 fine. SNILS must be written as “123-456-789 01” (two dashes and a space in the middle).

Employees indicate their TIN only if they have a TIN. If you wrote the TIN in the 2-NDFL certificate, then you need to write it in the SZV-M, otherwise the fine is 500 rubles. If the employee does not have a TIN, then leave the field blank (without dashes).

Who to include?

You must include in the list any employees working under employment or civil contracts (even if they did not receive remuneration this month), as well as freelancers, part-time workers, etc. external, maternity leave, students, those on probation.

The founding director must also be included in the calculation.

You need to include any employees with whom the contract was valid during the reporting month. Those. if the employee arrived at the end of the month or quit this month, then he must be included in the calculation.

Zero

There cannot be a zero SZV-M even if there is only one founder and no one else - it must be included in the form.

Corrections

If you need to correct an error (for example, incorrect full name or INN or SNILS), then you need to submit two forms - o) and a supplementary one (in paragraph 3 “additional”). Only erroneous data is provided in the cancellation form. In the supplementary one, similar data is written down, only correct. These forms are submitted at the same time.

If you forgot to enter an employee, submit only the supplementary form (in paragraph 3 “additional”).

If an employee has changed her last name (got married, for example), then you need to enter the last name that is in SNILS (even if she has already changed her passport and the SNILS is old).

If you included an employee by mistake, submit only the cancellation form (in paragraph 3 “cancel”).

Before 2020, there were 2 weeks to correct errors. From 2020, this period has been reduced to 5 working days.

What does code 20 mean?

There is another group of errors detected when checking SZV-TD. It is assigned code 20. If you find error 20 in the SZV-TD inspection report, the program has identified the following shortcomings:

Errors with code 20 are not critical - the Pension Fund of Russia will accept such a report. This code means logical inconsistencies. For example, you mistakenly included in the SZV-TD for March an event that was already reflected in the February report.

Deadlines

June 6 is the deadline to submit a canceling or supplementing SZV-M (PFR letter dated May 4, 2020 No. 04/406/1984).

The deadline for submitting new monthly reports to the Pension Fund is no later than the 10th (15th from 2020) of the next month. For example, the first report for April 2020 must be submitted by May 10.

| Month for which reporting is submitted | Submission deadline |

| December 2016 | from January 1 to January 17, 2017 |

| January 2017 | from 1 to 15 February 2017 |

| February 2017 | from March 1 to March 15, 2017 |

| March 2017 | from April 1 to April 17, 2017 |

| April 2017 | from May 1 to May 15, 2017 |

| May 2017 | from 1 to 15 June 2017 |

| June 2017 | from July 1 to July 17, 2017 |

| July 2017 | from 1 to 15 August 2017 |

| August 2017 | from 1 to 15 September 2017 |

| September 2017 | from October 1 to October 16, 2017 |

| October 2017 | from November 1 to November 15, 2017 |

| November 2017 | from December 1 to December 15, 2017 |

| December 2017 | from January 1 to January 15, 2018 |

* If the date of submission of reports to the Pension Fund falls on a weekend (or non-working) day, the deadline is postponed to the next working day

In advance

You can submit from the 1st (May) of the following month. However, the law does not prohibit submitting reports in advance (early). Therefore, the Pension Fund of Russia will begin accepting such reports on April 15. However, you need to submit such a report before the end of the month only if you are sure that you will not have another employee (any) before the end of the month. Otherwise, you will still have to submit an amendment or pay a fine of 500 rubles. for every new one.