09.09.2018 Category: Payments

Regardless of what taxation system the organization uses, maternity benefits (Part 1, Article 3 of Law No. 255-FZ of December 29, 2006).

The procedure for paying for the first three days of incapacity at the expense of the organization does not apply to maternity benefits. Pay the benefit from the funds of the Federal Social Insurance Fund of Russia for all the days that the employee was on maternity leave. This follows from Part 1 of Article 3 of the Law of December 29, 2006 No. 255-FZ.

A collective and (or) employment agreement may provide for additional payments to maternity benefits up to the actual average earnings of the employee (Article 9 of the Labor Code of the Russian Federation). This amount is not a benefit (Article 8 of the Law of May 19, 1995 No. 81-FZ, Article 14 of the Law of December 29, 2006 No. 255-FZ). The organization pays it from its own funds.

An example of how to determine the sources of payment of maternity benefits

Cashier of the organization A.V. Dezhneva submitted a sick leave certificate to the accounting department confirming her maternity leave. The duration of the vacation is 140 calendar days (from January 15 to June 3, 2020 inclusive).

The collective agreement of the organization provides for additional payments up to the actual average earnings for the period of maternity leave. In this case, the actual average earnings are calculated based on the period of 365 days preceding maternity leave.

Dezhneva’s earnings in 2014 amounted to 630,000 rubles, contributions to the Social Insurance Fund of Russia were paid from an amount equal to 624,000 rubles. And in 2020, Dezhneva was accrued earnings in the amount of 680,000 rubles, contributions to the Social Insurance Fund of Russia in 2020 were paid from an amount equal to 670,000 rubles.

The employee worked in full for 2015. Thus, her actual average earnings (for calculating the additional payment for maternity benefits) for the period from January to December 2020 inclusive is equal to: 680,000 rubles. : 365 days = 1863.01 rub./day.

The calculation period for calculating benefits includes 2014 and 2020.

The number of calendar days in 2014-2015 is 730.

Ivanova did not have any calendar days excluded from the billing period.

The average daily earnings for calculating benefits were: (624,000 rubles + 670,000 rubles): 730 days. = 1772.60 rub./day.

The amount of maternity benefits reimbursed by the Russian Social Insurance Fund is: 1,772.60 rubles/day. × 140 days = 248,164 rub.

And the benefit, calculated based on Dezhneva’s average earnings for the last year preceding the insured event, is: 1863.01 rubles/day. × 140 days = 260,821.40 rub.

Thus, the organization pays an additional 12,657.40 rubles from its own funds. (RUB 260,821.40 - RUB 248,164).

Accounting: accrual and payment

In accounting, record the accrual and payment of maternity benefits with the following entries:

— maternity benefits accrued;

Debit 70 Credit 50 (51)

— maternity benefits were issued to the employee.

An example of how to reflect maternity benefits in accounting

The organization paid Ivanova maternity benefits in the amount of 107,956.52 rubles.

The accountant made the following entries in the accounting:

Debit 69 subaccount “Settlements with the Social Insurance Fund for social insurance contributions” Credit 70

— 107,956.52 rub. — maternity benefits accrued;

Debit 70 Credit 51

— 107,956.52 rub. — the benefit was transferred to Ivanova’s bank card.

How to reflect the accrual and payment of maternity benefits in accounting

The collective agreement of the organization provides for additional payments up to the actual average earnings for the period of maternity leave.

In this case, the actual average earnings are calculated based on the period of 365 days preceding maternity leave. A collective and (or) employment agreement may provide for additional payments to maternity benefits up to the actual average earnings of the employee (Article 9 of the Labor Code of the Russian Federation). This amount is not a benefit (Article 8 of the Law of May 19, 1995 No. 81-FZ, Article 14 of the Law of December 29, 2006 No. 255-FZ). The organization pays it from its own funds.

https://youtu.be/FSpZa07WqXU

Accrual procedure

The full amount of the benefit must be accrued and reflected in accounting within 10 days after the employee brings the documents necessary to calculate the benefit. Such documents are a completed sick leave certificate and, if necessary, certificates of earnings from previous places of work for the last two years (Part 1 of Article 15, Part 5 of Article 13 of the Law of December 29, 2006 No. 255-FZ).

The benefit must be paid after it has been assigned within the earliest period established for the payment of wages (Part 1, Article 15 of the Law of December 29, 2006 No. 255-FZ).

Based on materials from open sources

Maternity payments almost always cause difficulties for accountants. What entries need to be reflected in accounting for calculating maternity benefits - this is one of the many questions that arise in the process of making a payment to the expectant mother.

Maternity benefits in 2020 posting

A collective and (or) employment agreement may provide for additional payments to maternity benefits up to the actual average earnings of the employee (Article 9 of the Labor Code of the Russian Federation). This amount is not a benefit (Article 8 of the Law of May 19, 1995 No. 81-FZ, Article 14 of the Law of December 29, 2006 No. 255-FZ). The organization pays it from its own funds.

If we consider the situation of unemployment, then the calculation of benefits is based on the minimum wage. The possibility of payment is a good support; in such cases, money is not superfluous. Speaking in numbers, the situation is approximately like this:

Maintenance services up to one and a half years

The benefit until the child is one and a half years old is paid from the Social Insurance Fund. To do this, the accountant will make the following entries:

- Dt 69-1 Kt 70 accrual.

- Dt 70 Kt 50 payment.

Additional payment before actual earnings:

The employment contract may provide for additional payment up to actual earnings at the expense of the organization; this is not a benefit, so the employer will have to pay.

- Debit 20 (23, 25, 26, 44...) Credit 70 – an additional payment has been added to maternity benefits up to the actual average earnings;

- Debit 70 Credit 50 (51) – an additional payment was issued to maternity benefits up to the actual average earnings.

Example of calculating maternity benefits

- The employee went on maternity leave on July 3, 2020, the billing years will be 2015 and 2020, the vacation period is 140 days

- Income of a woman in 2020 amounted to one hundred twenty thousand rubles in 2016. one hundred forty-four tons, total two hundred sixty-four tons../ 731, we get 361.15 rubles. average daily earnings.

- 361.15 *140=50561 rub. Total our allowance.

Accrual of maternity benefits in 2020 postings

From 01/01/2020, insurance premiums in case of temporary disability and in connection with maternity must be paid to the Federal Tax Service. And for reimbursement of benefits, as before, you must contact the Social Insurance Fund. In case of illness of an employee, he is paid temporary disability benefits (Article 183 of the Labor Code of the Russian Federation). In this case, the first 3 days of illness are paid at the expense of the employer, and from the 4th day - at the expense of the Social Insurance Fund (clause 1, part 2, article 3 of the Federal Law of December 29, 2006 No. 255-FZ)

Finally, the amount of the benefit (the final payment for sick leave) is calculated by multiplying the daily benefit by the number of days of incapacity for work (clause 5 of Article 14 of Law No. 255-FZ). How to make work easier? We have developed useful services for an accountant to make your work easier and faster: a VAT calculator, a KBK and payment card directory, a payroll and personal income tax calculator, a posting bank, etc.

Reflection of information on accrued benefits in regulated reporting

To reflect in the regulated reporting on insurance premiums information about accrued benefits for child care up to 1.5 years old, it is necessary to register the document Contribution Accounting Operation. This document is used to record social security benefits and adjust accounting data for insurance contributions.

- Section Salaries and Personnel - Insurance Contributions - Contribution Accounting Operations.

- Click on the Create button.

- The Organization field is filled in by default. If more than one organization is registered in the information base, then you must select the organization in which the employee is registered (Fig. 4).

- In the Date field, enter the date the document was posted.

- In the Employee field, select an employee to whom benefits have been accrued for up to 1.5 years.

- In the Month of calculation field period, indicate the month in which child care benefits up to 1.5 years were accrued.

- On the Child care benefits tab, enter a new line using the Add button: in the Start of leave column, indicate the start date of parental leave for a child up to 1.5 years old. In our example - 01/15/2016.

- in the Employment type column, select the employee’s type of employment: Main place of work, External part-time job or Internal part-time job. In our example, indicate the Main place of work;

- in the column For the first child (Total/At the expense of the Federal Fund), indicate the amount of benefits paid at the expense of the Social Insurance Fund of the Russian Federation and at the expense of the federal budget for caring for the first child (if the benefit was paid in excess of the established norms). In our example, the benefit amount is 11,117.07, because This is the employee’s first child;

- in the column On the second and last. children (Total/At the expense of the FB) indicate the amount of benefits paid at the expense of the Social Insurance Fund of the Russian Federation and at the expense of the federal budget for the care of the second (subsequent) child (if the benefit was paid in excess of the established norms). In our example, this field is not filled in;

- column Basis financier. In our example, there is no need to fill in due to FB. The column indicates the legal basis for the additional payment if the benefit is paid in excess of the established norms. Such payments are financed from the federal budget in the form of transfers from the Federal Social Insurance Fund of the Russian Federation.

Figure 4.

Starting from February 2020, the child care benefit for children under 1.5 years old will be accrued in full - RUB 20,272.30.

Source: www.1c-usoft.ru/article/1s-bukhgalteriya-8-redaktsiya-3-0-nachislenie-ezhemesyachnogo-posobiya-po-ukhodu-za-rebenkom-do-dost/

Accrual of maternity benefits in 2020 postings

In our article we will look at specific examples of how to calculate sick leave in 2020 in a new way; an example calculation for each case will help you quickly figure out how to calculate sick leave and how long to take Calculation of sick leave in 2020. as well as the calculation of sick leave in 2020, it is carried out in a certain order.

Maternity leave is granted to the employee for 140 calendar days from 01/26/2013 to 06/14/2013. The accrued wages, from which insurance contributions were calculated to the Federal Social Insurance Fund of the Russian Federation, amounted to: for 2011 - 180,000 rubles. for 2012 - 216,000 rubles.

Accounting for maternity benefits in 2020

A one-time payment to women who register with medical organizations in the early stages is assigned and paid at the place of destination and payment of maternity benefits. To do this, the employee must provide the organization with an application for appointment, a certificate from the antenatal clinic or another medical organization that registered the woman early (clauses 5, 21, 22 of the Procedure).

This amount, like the amount of a one-time maternity benefit paid from the budget of the Social Insurance Fund of the Russian Federation, is not an expense of the organization (in relation to clause 2 of the Accounting Regulations “Organization Expenses” PBU 10/99, approved by Order of the Ministry of Finance of Russia dated 06.05 .1999 No. 33n) and applies to settlements with the Federal Social Insurance Fund of the Russian Federation.

Income tax

Do not take into account childcare benefits for children under 1.5 years of age when calculating income tax. This amount is fully reimbursed by the Russian Social Insurance Fund, therefore it is not recognized as an expense of the organization (Article 252 of the Tax Code of the Russian Federation).

An example of how to take into account child care benefits up to 1.5 years old. The organization applies a general taxation system

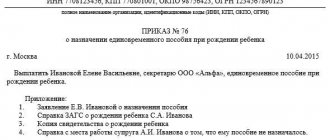

Alpha LLC applies a general taxation system. Employee of the organization E.V. Ivanova went on maternity leave on February 1, having submitted all the necessary documents on January 31. Ivanova's first child.

On February 4, the head of the organization issued an order granting her child care benefits for children up to 1.5 years old. The amount of the benefit, calculated based on Ivanova’s average earnings, amounted to 7995.62 rubles. Employees are paid on the 5th of every month.

Along with the salary for February, the accountant accrued Ivanova’s allowance:

Debit 69 subaccount “Settlements with the Social Insurance Fund for social insurance contributions” Credit 70 - 7995.62 rubles. – child care benefits up to 1.5 years old have been accrued.

The benefit was paid to her on the day the salary was paid:

Debit 70 Credit 50 – 7995.62 rub. – a child care allowance was issued to the employee from the cash register.

The accountant did not take into account the amount of child care benefits when calculating income tax. He also did not withhold personal income tax from the benefit amount and charge contributions for compulsory pension (social, medical) insurance and insurance against accidents and occupational diseases.

Situation: how to take into account when taxing additional payments to child care benefits up to 1.5 years before the actual average earnings (official salary)? The organization applies a general taxation system.

Withhold personal income tax from the amount of additional payments, calculate insurance premiums, as well as contributions for insurance against accidents and occupational diseases. Include additional payments in income tax expenses, provided that they are provided for in the collective agreement.

An organization may provide in a collective agreement for additional payments to child care benefits up to the actual average earnings or salary (Articles 22, 41, 57 of the Labor Code of the Russian Federation). That is, on your own initiative, pay benefits in an amount higher than provided by law.

Withhold personal income tax from the amount of such additional payments (clause 1 of Article 210 of the Tax Code of the Russian Federation).

In addition, for the amount of additional payments, add contributions for compulsory pension (social, medical) insurance, as well as contributions for insurance against accidents and occupational diseases (part 1 of article 7 of the Law of July 24, 2009 No. 212-FZ, paragraph 1 Article 20.1 of the Law of July 24, 1998 No. 125-FZ). This is explained by the fact that such additional payments are not provided for in the list of non-taxable payments (Article 9 of the Law of July 24, 2009 No. 212-FZ, Article 20.2 of the Law of July 24, 1998 No. 125-FZ).

Advice: the organization may not charge insurance premiums for the amounts of additional payments to the child care benefit provided for by the collective agreement. But this will most likely lead to a dispute with the inspectors. The judges are on the side of the organizations.

Although there is an employment relationship between the organization and the employee, these additional payments are not remuneration for work. The supplement to the maintenance allowance is a social payment. It does not depend on the qualifications of the employee, the volume and quality of work performed by him. This means that such additional payment cannot be recognized as remuneration. There is no need to make contributions to it. After all, there is no object for taxation of contributions provided for in Part 1 of Article 7 of the Law of July 24, 2009 No. 212-FZ.

The correctness of this approach is confirmed by the judges (see, for example, the resolution of the Federal Antimonopoly Service of the Ural District dated June 17, 2014 No. F09-2974/14). However, the very existence of judicial practice indicates that inspectors require that contributions be calculated. Therefore, the organization will most likely have to defend its point of view in court.

When calculating income tax, include the additional payment provided for in an employment or collective agreement in expenses on the basis of paragraph 25 of Article 255 of the Tax Code of the Russian Federation.

The Russian Ministry of Finance holds a similar point of view regarding additional payments:

– up to the actual average earnings (letters of the Ministry of Finance of Russia dated December 27, 2012 No. 03-03-06/1/723, dated October 26, 2009 No. 03-03-06/1/691);

– up to the official salary (letters of the Ministry of Finance of Russia dated April 28, 2014 No. 03-03-06/1/19699, dated May 18, 2012 No. 03-03-06/1/254, dated February 24, 2012 No. 03 -03-06/1/98).

How to calculate sick leave for pregnancy and childbirth

The basis for calculating maternity benefits is the average daily earnings of the expectant mother for the billing period. Usually they take the last 2 years, but if at that time the maternity leave was on another maternity leave, then, according to her application, the years in the calculations can be changed.

- If, when going on maternity leave, a woman is employed by the same employers as in the previous 2 years, benefits are calculated and paid to her separately for each place of work. In this case, 2 sick leaves are issued.

- If, when going on maternity leave, a woman is employed by some employers, and in the previous 2 years she worked in other companies, she is paid benefits for one job of her choice. From other employers she is required to provide certificates of income for the billing period and confirmation that they did not accrue maternity benefits to her.

- If during the billing period a woman worked both for her current employers and for others, then she can use both the first and second options for paying benefits.

Personal income tax and insurance premiums

Since the child care allowance for children under 1.5 years of age is a state benefit, its amount is not taxed:

- Personal income tax (clause 1 of article 217 of the Tax Code of the Russian Federation);

- contributions for compulsory pension (social, medical) insurance (clause 1, part 1, article 9 of the Law of July 24, 2009 No. 212-FZ);

- contributions for insurance against accidents and occupational diseases (subclause 1, clause 1, article 20.2 of the Law of July 24, 1998 No. 125-FZ).

Attention: if the Federal Social Insurance Fund of Russia does not accept the amount of child care benefits as offset, then mandatory insurance contributions must be calculated for this amount.

Based on the results of the audit, auditors of the Federal Social Insurance Fund of Russia will refuse to reimburse child care benefits if they were paid in violation of legal requirements. In particular, if the relevant supporting documents are missing (incorrectly completed).

In this case, the benefit amount is not considered insurance coverage for compulsory social insurance. Consequently, it does not apply to payments for which mandatory insurance contributions are not charged (clause 1, article 9 of the Law of July 24, 2009 No. 212-FZ). Therefore, it is subject to insurance premiums on a general basis.

The procedure for accounting for benefits when calculating other taxes depends on what taxation regime the organization applies.

Accrual of maternity benefits in 2020 postings

The article contains Social Insurance benefits in 2020: size, calculation examples, compensation. Accountants are already accustomed to the fact that starting from the new year, the size of fixed social benefits for employees should change - for the birth of a child, for registration in the early stages of pregnancy, etc. Since the indexation of Social Security benefits has occurred from year to year over the past ten years.

Temporary disability benefits are provided to the insured person in the form of material support, which fully or partially compensates for the loss of wages (income) in the event of one of the insured events: 04) caring for a child under the age of three or a disabled child under the age of 18 years of age in case of illness of the mother or another person who is looking after this child;

We recommend reading: Tariff Rates of Labor for 2020 Guarantor

What payments are a woman entitled to during pregnancy and after childbirth?

Federal law states that a significant portion of child benefits can be obtained by anyone who is actually raising a child. Most often, the biological mother takes custody, less often - the father, grandmothers and other close relatives. But it is important to know that B&R payments are something of an exception to the rule - they are only due to the biological mother.

In such situations, it is recommended to file a lawsuit to prove the impossibility of receiving payments at the place of work. For a woman who is pregnant or has recently given birth, legal proceedings can cause a lot of trouble (both physical and psychological), therefore, the law allows legal proceedings to begin within six months after the end of maternity leave.

Postings for maternity benefits

Payment of sick leave for pregnancy and childbirth is regulated by Law No. 255-FZ of December 29, 2006. The usual duration of disability associated with childbirth is 140 days. But it happens that an employee continues to work after the start date of sick leave. In this case, only those days that the employee actually used as maternity leave are subject to payment. For the remaining days, regular wages are paid.

For organizations taking part in the FSS pilot project “Direct Payments”, the absence of a maternity worker will be clear only from the working time sheet. There are no entries in the accounting records for calculating maternity benefits, since the full payment is made by the Social Insurance Fund directly to the employee. But the obligation to store the entire package of documents for assigning benefits remains with the employer.

Amount of payments for children

In 2020, the size of the BiR one-time benefit in accordance with the law for women will be:

- 100% of the average salary of a working woman

- 100% of the amount of monetary allowance - for military personnel under contract

- In the minimum amount based on the minimum wage for everyone else, including the unemployed

For women giving birth who received high wages, for example a million a year, there is a limit on the payment of benefits, for example:

- RUR 266,191.8 - in general; RUB 368,865.78 – during multiple pregnancy; • 296,613.72 rub. - during complicated childbirth.

A sick leave certificate for pregnancy and childbirth is issued to a woman at 30 weeks.

For normal births, the certificate of incapacity for work is given for a period of 140 days, for complicated ones for 156 days, and if the pregnancy is multiple, then 194 days. The payment is calculated based on wages for the previous 2 years before the onset of maternity leave, for example, an employee left in 2020, which means For the calculation we take 2020 and 2020.

Postings for the calculation and payment of maternity benefits

Now it is recommended for legal entities to use the status “01”, and individual entrepreneurs – “09”. The list of types of state control in which a risk-based approach is applied has been expanded. Now this list also includes checks for compliance with labor legislation requirements carried out by the labor inspectorate. From 01/01/2020, insurance premiums in case of temporary disability and in connection with maternity must be paid to the Federal Tax Service.

The benefit is calculated on the basis of sick leave for pregnancy and childbirth. However, there are a number of important restrictions that apply to this benefit. In particular, the amount of earnings that is taken into account when assigning benefits should not exceed the maximum amount subject to contributions for compulsory social insurance (in the part transferred to the Social Insurance Fund of Russia). What documents are needed to apply for maternity benefits? What are the features of maternity pay? How are maternity benefits calculated? What is the maximum and minimum period of maternity leave?

Maternity benefit in 2020

After the woman provides a package of necessary documents, the policyholder will assign her a benefit within ten calendar days. If the maternity benefit is paid by the employer, it is issued along with the next salary. If the benefit is provided by social security authorities, then payment is made by mail or through a bank no later than the 26th day of the month following the month in which documents were received. A production calendar will help you meet the deadlines for assigning and paying maternity benefits.

Please note: maternity benefits in 2020 are paid only for the period of maternity leave. This means that if a woman does not take advantage of the right to the specified leave and continues to work (and, accordingly, receive wages), then she is not entitled to benefits. In this situation, the employer does not have the right to provide the woman with two types of payments at once: both salary and benefits. Therefore, wages will be paid for days worked. As soon as a woman decides to exercise the right to maternity leave and it is issued, the payment of wages will stop and the employer will accrue benefits.

The procedure for calculating sick leave for different regions

A sick leave can be issued for various reasons, but to calculate and make entries it is enough to distinguish 3 groups of reasons:

- by illness;

- in connection with pregnancy and childbirth;

- as a result of a work injury.

Payment for days missed due to illness is calculated depending on length of service and is paid in part by the employer.

The amounts of sick leave payments in the two remaining cases are made entirely from the Social Insurance Fund budget and do not depend on length of service.

Accounting entries are formed based on whether the region in which the company operates participates in the FSS pilot project.

From the point of view of calculating the amount due for days of incapacity, all regions of the country are divided into two categories: those participating in the FSS pilot project and those not.

If a region participates in a pilot project of the Social Insurance Fund, then the enterprise’s accounting department calculates and pays only part of the benefit paid by the employer, which is 3 days for illness. The rest will be considered by the Social Insurance Fund and paid directly to the account of the employee who provided the sick leave and the application for its payment.

If the region in which the company operates does not participate in the pilot project, then both parts of the sick leave are calculated and paid by the employer, and the Social Insurance Fund subsequently reimburses the amounts paid.

Let's look at the accounting entries for a certificate of incapacity for work using an example. The employee received compensation for 10 days of illness in the amount of 5,000 rubles. The employee received payments for the period of incapacity for work during pregnancy and childbirth in the amount of 145,000 rubles.

| Posting Contents | Debit | Credit | Amount, rub. | Primary document |

| The amount of payment for days of incapacity for work has been determined and personal income tax has been calculated. | 70 | 68.01 | 650 | Certificate of incapacity for work, certificate of accounting calculation |

| Amount due to employer | 20 (25, 26, 44) | 70 | 1305 | Certificate of incapacity for work, certificate-calculation |

| Amount due to the Social Insurance Fund | 69.01 | 70 | 3045 | Certificate of incapacity for work, certificate-calculation |

| Sick leave benefits paid in cash from the cash register | 70 | 50 | 4350 | Expense cash order, payroll |

| Reimbursement received from FSS | 51 | 69.01 | 3045 | Bank statement |

| Maternity benefits accrued | 69.01 | 70 | 145 00 | Certificate of incapacity for work, certificate-calculation |

| Financial assistance allowance was transferred from the current account | 70 | 51 | 145 000 | Payment order, bank statement |

| Reimbursement of financial and economic benefits received from the Social Insurance Fund | 51 | 69.01 | 145 000 | Bank statement |

| Posting Contents | Debit | Credit | Sum. rub. | Primary document |

| Sickness benefits accrued at the expense of the employer | 20 (25, 26, 44) | 70 | 1500 | Sick leave, certificate-calculation |

| Personal income tax accrued on sick leave amount | 70 | 68.01 | 195 | Help for accounting calculations |

| Payment of sick leave benefits in cash from the cash register | 70 | 50 | 1305 | Expense cash order, payroll |

| Payment of sick leave benefits from a current account | 70 | 51 | 1305 | Payment order, payroll |

If the payment is made through a current account, then the posting will be D 70 K 51 in the amount of 1305 rubles.

Sick leave issued for pregnancy does not generate a statement, since it is fully paid at the expense of the Social Insurance Fund. The same applies to payments in connection with an accident at work.

The maximum annual earnings taken into account when calculating disability benefits for 2020 is 865,000 rubles; in 2018, the same figure was 815,000 rubles, and in 2017 - 755,000 rubles.

We suggest you read: If a woman is divorced with two children, can they receive benefits?

The maximum average daily earnings for calculating maternity benefits in 2020 is 2,150.68 rubles.

The minimum wage from January 1, 2019 is 11,280 rubles.

https://www.youtube.com/watch?v=V1LEz_ewroM

The maximum amount of payment for temporary disability due to an accident at work or occupational disease in 2020 is 309,135.44 rubles for a full month.