What is included in average earnings

Many payments due to employees in accordance with labor legislation are calculated based on average earnings: vacation pay, compensation for unused vacation, payment for days on a business trip, etc. When calculating average earnings, all payments provided for by the remuneration system are taken into account (clause 2 of the Regulations, approved by Decree of the Government of the Russian Federation of December 24, 2007 N 922). This is, of course, a general formulation. Therefore, let’s try to understand in more detail what is included in the average earnings, that is, what payments should be taken into account when calculating it.

- allowances and additional payments to tariff rates and salaries - for length of service, length of service, combination of professions, team management, etc.;

- payments related to working conditions. For example, increased wages for heavy work, for night work, etc.;

- bonuses and rewards in accordance with the remuneration system.

Calculation of vacation pay

The average daily earnings for vacation pay are determined for the last 12 calendar months by dividing the amount of accrued wages by 12 and by 29.4 (Article 139 of the Labor Code of the Russian Federation).

This article provides, if the interests of employees require it, the possibility of establishing in a collective agreement or local regulatory act a different billing period for these purposes, if this does not worsen the situation of employees.

1. List of payments included in the calculation of average earnings

To calculate the average salary, all types of payments provided for by the remuneration system and applied in the relevant organization are taken into account, regardless of the sources of these payments (Article 139 of the Labor Code of the Russian Federation).

That is, when calculating average earnings, all wage payments that are provided for by the organization’s regulations on remuneration of workers are taken into account.

If, for example, in an organization, in addition to the remuneration system, one-time bonuses are paid under separate orders for the performance of particularly important work, despite the fact that this is an element of wages, such bonuses are not taken into account when calculating average earnings.

Clause 2 of the Regulations on Average Earnings provides an approximate list of these payments:

– basic wages at tariff rates (salaries), piece rates, as a percentage of revenue, etc.;

– incentive bonuses and additional payments to tariff rates, official salaries for professional excellence, qualification category, expansion of service areas, performance of duties of a temporarily absent employee and others provided for by the payment regulations;

- compensation payments and additional payments related to working conditions, - payments determined by regional regulation of wages (based on coefficients and percentage bonuses), increased wages for heavy work, work with harmful and (or) dangerous and other special working conditions, for work at night, payment for work on weekends and non-working holidays, payment for overtime work;

– bonuses and remunerations provided for by the provisions on payment (bonuses) for employees of organizations, etc.

Let us consider the positions that arise in specific situations that need or do not need to be taken into account when calculating average earnings for vacation pay.

Monetary compensation paid by an employer to an employee if the first one fails to pay the wages on time.

The average daily earnings for vacation pay are determined based on accrued wages (Article 139 of the Labor Code of the Russian Federation).

Wages are remuneration for work depending on the qualifications of the employee, complexity, quantity, quality and conditions of the work performed, as well as compensation and incentive payments. Compensation payments are understood as payments related to the employee’s performance of a labor function (Article 129 of the Labor Code of the Russian Federation).

Monetary compensation provided for in Art. 236 of the Labor Code of the Russian Federation on this basis, is the financial responsibility of the employer and is paid as a percentage of the amount of wages not paid on time.

That is, this compensation is not wages, and there are no grounds for including it in the calculation of average earnings.

Should compensation for innovation proposals be taken into account when calculating average earnings?

Payment of remuneration for an invention is provided for by the Patent Law of the Russian Federation dated September 23, 1992 No. 3517-1 (as amended and supplemented).

In this case, the amount of remuneration and the procedure for its payment are determined by an agreement between the author and the employer, which is one of the types of civil law contracts.

In accordance with the Methodological Recommendations for organizing and conducting rationalization work at enterprises of the Russian Federation (letter of Rospatent and the Ministry of Industry of Russia dated June 25, 1996 No. 6/7), remuneration for a rationalization proposal is calculated and paid in the amount, procedure and terms established at the enterprise.

Rewards for inventions and innovation proposals do not relate to remuneration for labor, nor to payments of a compensatory and incentive nature, and therefore are not wages.

Based on the above, remuneration to inventors and innovators should not be taken into account when calculating average earnings.

What is the mechanism for accounting for overtime payments to employees if they are not accrued at the time of calculating vacation pay?

In the above situation, the average earnings are calculated without taking into account overtime pay, and after the corresponding amounts are calculated, a recalculation is made with an additional payment.

Due to production needs during the billing period, the employee was transferred for a period of one month to a lower-paid job not stipulated by the employment contract, with payment based on average earnings. Is it necessary to include additional payment up to average earnings in the calculation of average earnings?

In accordance with clause 4 of the Regulations on Average Earnings, for cases provided for by the Labor Code of the Russian Federation, time is excluded from the calculation period, as well as amounts accrued during this time, if the employee maintained average earnings according to the legislation of the Russian Federation.

Payment for work in connection with a transfer to a lower-paid job for production reasons not lower than the average earnings for the previous job is provided for in Art. 72.2 of the Labor Code of the Russian Federation, therefore, in the above situation, average earnings are calculated without taking into account periods of work during transfers and amounts accrued during this time in the amount of average earnings.

Is the calculation of the average earnings of an employee of a joint-stock company included payment for work on a day off in excess of normal working hours and in what amount - single or double?

According to Art. 139 of the Labor Code of the Russian Federation, to calculate average earnings, all types of payments provided for by the remuneration system used in the organization are taken into account, including payment for work on weekends and non-working holidays (subclause “l”, paragraph 2 of the Regulations on average earnings).

And since, on the basis of Art. 135 of the Labor Code of the Russian Federation, organizations of the extra-budgetary sector of the economy independently establish all types and amounts of remuneration for labor, then when calculating average earnings they are taken into account in the amounts that are established in the organization.

As for payment for work in conditions that deviate from normal conditions, including on weekends, the amount of additional payments for such work is in accordance with Art. 149 of the Labor Code of the Russian Federation cannot be lower than those established by laws and other regulatory legal acts.

Should additional payments to employees for food provided for by the collective agreement be included in the calculation of average earnings for vacation?

Average earnings for vacation pay are calculated based on the actual accrued wages for the billing period, i.e. from the remuneration that the employer pays to the employee for his work function.

Since food subsidies are not paid for work and are not wages, they should not be taken into account when calculating average earnings for vacation pay.

An employee of the plant is involved in training and advanced training of personnel in production and receives payment for training. Should it be included in the calculation of vacation pay?

Payment for training is not remuneration for work and should not be taken into account when calculating average earnings.

The employee was underpaid for 10 months (the long service bonus was erroneously not accrued for the period from May 2006 to March 2007). The underpaid amount was credited to him in full in June 2007, and on July 5 the employee went on annual leave. Is this payment taken into account when calculating the average salary for vacation pay?

In the above situation, the billing period will be July 2006 - June 2007. If in the billing period the amount of underpaid wages is accrued for months not included in the billing period, then this amount should not be included in the accrued wages to determine average earnings grounds, the preservation of the average salary in cases established by law is carried out taking into account the amount of funds earned in the billing period.

The amount of additional payment due to the months of the billing period is taken into account when calculating average earnings.

Thus, the calculation of average earnings for vacation pay does not include additional wages for the period from August 2006 for May and June 2006.

When calculating average earnings, is the bonus for shift work established for the employee in accordance with the law taken into account?

Payment of bonuses for shift work is provided for in Art. 302 “Guarantees and compensation for persons working on a rotational basis” of the Labor Code of the Russian Federation. That is, the bonus for shift work is compensation and, according to this article, is paid in exchange for daily allowance, similar to business trips.

The payment of a bonus for shift work is not related to work beyond the normal duration of daily work, taking into account the special work schedule on the shift. The hours of daily (between shifts) rest that are underused in this case, as well as the days of weekly rest, are summed up and provided in the form of additional days off from work (days of inter-shift rest) during the accounting period, which are paid in the amount of the tariff rate (salary), unless otherwise established labor or collective agreement.

This allowance is also not associated with work in special climatic conditions. Workers who travel to perform work on a rotational basis in the regions of the Far North and equivalent areas from other areas are set a regional coefficient and are paid percentage bonuses to wages in the manner and amount that are provided for persons permanently working in areas of the Far North and equivalent areas. localities (Article 302 of the Labor Code of the Russian Federation). Percentage bonuses and the regional coefficient are paid monthly and are calculated on the employee’s actual monthly earnings without limiting its maximum amount.

Since the bonus for shift work is compensation and is paid in accordance with Art. 302 of the Labor Code of the Russian Federation, not for a labor function carried out under special working conditions, but instead of daily allowance to reimburse additional expenses due to the special nature of the work; it is not taken into account when calculating average earnings.

This position is confirmed by the decision of the Supreme Court of the Russian Federation dated March 20, 2003 No. GKPI 2003-195.

2. Determination of the billing period

As a general rule, the calculation period for paying vacations and paying compensation for unused vacations is the last 12 calendar months.

The employee was dismissed from the organization on June 28, 2007, June 29 and 30 are Saturday and Sunday. Will June be included in the calculation period for payment of compensation for unused vacation?

The day of dismissal is the last day of work. When determining the billing period in this case, one should proceed from the work schedule of a particular employee. If Saturday is his non-working day according to the schedule, then June is considered fully worked and, therefore, will be included in the billing period. If according to the schedule Saturday is a working day, then this month has not been fully worked out and will not be included in the billing period.

An employee with piecework wages goes on vacation according to the schedule from April 3, 2007. The billing period is April 2006 - March 2007. Work orders for the last days of work in March were not processed, and the employee’s wages were not accrued for them. Is it possible in this case to take March 2006 – February 2007 as the calculation period?

The absence of an exact amount of wages at the time the employee goes on vacation cannot serve as a basis for changing the payroll period. When calculating the average daily earnings to pay for vacation, one should proceed from the already known part of the employee’s salary for March. Subsequently, the average daily earnings are recalculated taking into account the final amount of wages for March and the employee is paid accordingly.

This situation is due to the fact that employees who go on vacation on different days of the same month (at the beginning of the month, in the middle or at the end) should be treated on equal terms when determining their average daily earnings.

The organization underwent a reorganization with the separation of two independent legal entities. After working there for two months, the employee was fired due to staff reduction. What calculation period should be used to calculate the employee’s average earnings to pay compensation for unused vacation?

In this case, a reorganization took place, therefore, labor relations with employees are not interrupted. Therefore, the average earnings for payment of compensation to a dismissed employee are calculated taking into account the period of work before the reorganization.

How to determine the calculation period for calculating average earnings for payment of compensation for part of the vacation exceeding 28 calendar days, in accordance with Art. 126 of the Labor Code of the Russian Federation?

In this case, the calculation period will be three calendar months before the month in which the specified compensation was accrued.

The billing period has not been fully worked out

Clause 4 of the Regulations on Average Earnings lists the periods excluded from the calculation. These are periods when the employee did not work with the knowledge of the employer, and periods of work when the employee retained his average earnings:

– the employee retained his average earnings in accordance with the legislation of the Russian Federation;

– the employee received temporary disability benefits or maternity benefits;

– the employee did not work due to downtime due to the fault of the employer or for reasons beyond the control of the employer and employee;

– the employee did not participate in the strike, but due to it was not able to perform his work;

– an employee raising a disabled child was provided with additional paid days off;

– the employee in other cases was released from work with full or partial retention of wages or without payment in accordance with the legislation of the Russian Federation;

– the employee was provided with days of rest (time off) in connection with work beyond the normal working hours under the rotation method of organizing work and in other cases in accordance with the legislation of the Russian Federation.

That is, these are periods of absence from work for good reasons with full, partial retention of wages or without pay, and periods of work with preservation of average wages.

Example

An employee in the calculation period for calculating average earnings for vacation pay (January - December 2006) was sick throughout December. In this case, the calculation period will be 11 months: January – November 2006.

Example

During the billing period, the employee was sick: from January 23 to February 6 and from March 1 to March 10, 2007.

In this case, calculations will be made for 9 full months and for the periods from January 1 to 22, from February 7 to 28 and from March 11 to 31.

If the employee did not work during the billing period for reasons not provided for in clause 4 of the Regulations on Average Earnings (participation in a strike, absenteeism due to the employee’s fault, etc.), then this time is not excluded from the calculation.

Example

The employee went on vacation in April 2007, and in January 2007, the month of the calculation period for calculating average earnings, took part in a strike for 15 days.

Since the employee did not work during the billing period for reasons not provided for in clause 4 of the Regulations on Average Earnings, the 15 days during which he took part in the strike are not excluded from the calculation.

Is Sunday included in the number of calendar days of the pay period if the employee was sick in one of the months and was discharged on Saturday?

The number of calendar days in months not fully worked is calculated through the five-day period worked using a coefficient of 1.4.

Is the time an employee is on leave without pay excluded from the calculation period and for what duration?

When calculating average earnings in accordance with subparagraph. “e” clause 4 of the Regulations on Average Earnings excludes from the calculation period the time the employee is released from work without pay in accordance with the legislation of the Russian Federation. Therefore, if such leave is granted on the basis of Art. 128 of the Labor Code of the Russian Federation for family circumstances and other valid reasons on the basis of a written application, regardless of the duration of such leave, it is completely excluded from the billing period.

When calculating vacation pay for an employee, the accountant encountered difficulties, due to the fact that due to the suspension of work on the basis of Art. 142 of the Labor Code of the Russian Federation (delay in payment of wages for a period of more than 15 days), the employee did not work all the days according to the schedule in the billing period for vacation pay. How is vacation pay calculated for him in this case?

The legislator did not oblige the employer to maintain the employee’s wages or average earnings in whole or in part during the period of suspension of work in accordance with Art. 142 Labor Code of the Russian Federation.

Therefore, if during the billing period the employee did not work for the specified reason, wages for this time are not accrued (unless otherwise established by the collective agreement).

At the same time, periods excluded from the calculation when determining average earnings, including for vacation pay, are listed in clause 4 of the Regulations on Average Earnings. Periods of suspension of work at the will of the employee, including due to delay in payment of wages in accordance with Art. 142 of the Labor Code of the Russian Federation, are not mentioned in it.

Thus, in the above situation, the time of suspension of work is not excluded from the billing period.

The employee goes on vacation in March 2007. The calculation period includes the time of forced absence. Is this time excluded from the billing period?

In accordance with Art. 394 of the Labor Code of the Russian Federation, on the basis of a decision of the body considering an individual labor dispute, the employee is paid the average salary for the entire period of forced absence. According to clause 4 of the Regulations on Average Earnings, the time when the employee maintains average earnings in accordance with the legislation of the Russian Federation is excluded from the billing period. Therefore, calculations of average earnings saved during vacation are made without taking into account the period of forced absence.

During the billing period, the employee did not have actual accrued wages or actually worked days, or this period consisted of time excluded from the billing period in accordance with clause 4 of the Regulations on Average Earnings.

If during the billing period the employee did not have actually accrued wages or actually worked days, or this period consisted of time excluded from the billing period in accordance with clause 4 of the Regulations on Average Earnings, the average earnings are determined based on the amount of actually accrued wages for the previous period of time equal to the calculated one.

Example

The employee had been on maternity leave since January 2005, then on parental leave, returned from child care leave on April 26, 2007, and took annual leave on April 28. In this case, in accordance with clause 5 of the Regulations on Average Earnings, the average daily earnings are determined based on the amount of accrued wages for the 12 calendar months before maternity leave - January - December 2004.

During the billing period and before the billing period, the employee did not have actual accrued wages or actually worked days.

If during the billing period and before the billing period the employee did not have actually accrued wages or actually worked days, the average earnings are determined based on the amount of wages actually accrued for the days actually worked by the employee in the month of vacation.

Example

The employee began work on February 1, 2007, and from February 21 he is granted study leave lasting 10 calendar days.

Since the employee has no earnings during the billing period and before it, calculations are made for the period from February 1 to February 20.

The employee was dismissed from his position on April 13, 2007 with payment of compensation for unused vacation. On April 26, 2007, he was hired by the same organization for a different position. On April 30, 2004, he was granted another leave in advance. What billing period should I use for my calculations?

Since in the above situation the employee was dismissed from the organization with payment of due compensation for unused vacation, and was not transferred to another job with his consent, labor relations arose again on April 26, 2004.

The calculation period for calculating average earnings for vacation pay will be the period from April 26 to April 29.

3. Calculation of vacation pay for a fully worked pay period

Generally established procedure

If, before the entry into force of the Labor Code, the average daily earnings for paying vacations and paying compensation for unused vacations were calculated by dividing the wages of the billing period by the number of calendar days per hour worked in the billing period, then from February 1, 2002, it is calculated using the average monthly number of calendar days, since the duration of almost all vacations is currently calculated in calendar days. Salary for the last 12 calendar months is divided by 12 and 29.4.

Example

The employee goes on vacation on April 13, 2007 for 14 calendar days.

The billing period for its payment is April 2006 – March 2007.

In the billing period, the employee was accrued wages accepted for calculation - 52,000 rubles.

The average salary for vacation pay will be:

52,000 rub. : 12 months : 29.4 days

x

14 days = 2063.49 rub.

Calculation of vacation pay for part-time employees.

Since Art. 139 of the Labor Code of the Russian Federation in relation to employees working part-time does not establish any specifics for calculating average earnings; their vacation pay is calculated in the generally established manner for the last three calendar months by dividing the amount of accrued wages by the number of months of the billing period and by 29.4.

That is, if an employee is assigned part-time working hours (and it doesn’t matter whether it’s part-time or part-time) and he worked the last three months before the vacation completely in accordance with his schedule, the billing period is considered fully worked.

Example

The employee has a three-day work week: Monday, Tuesday, Wednesday. He was granted annual leave from April 10, 2007. During the billing period, the schedule was fully worked out. Salaries for the months of the billing period are accrued in accordance with the time worked in the amount of 32,000 rubles.

The average daily earnings to pay for vacation will be:

32,000 rub. : 12 months : 29.4 days = 90.70 rub.

Example

The employee works in an organization that has a 5-day work week. In accordance with the schedule, the employee is granted leave in May 2007 for 28 calendar days. It is necessary to determine the amount of average earnings to be maintained for this period if his monthly salary is 2,400 rubles, and from March 1, at his personal request, he was given a part-time working day (4 hours) with payment in proportion to the time worked.

Average earnings will be:

(2400 rub.

x

8 + 1200 rub.

x

2) : 12 months.

: 29.4 days x

28 days = 1714.28 rubles.

Calculation of average earnings for payment of vacations provided in working days.

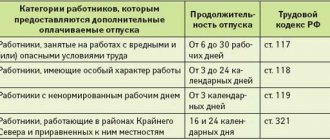

Employees who have entered into an employment contract for a period of up to two months, as well as seasonal workers, are granted annual leave at the rate of two working days per month of work (Articles 291, 295 of the Labor Code of the Russian Federation).

The average daily wage for paying for vacations granted in working days, in cases provided for by the Labor Code, is determined by dividing the amount of accrued wages for the time worked by the number of working days according to the calendar of a six-day working week that fall on the time worked.

Example

The employee was hired by the organization on April 1, 2007 to carry out temporary work for a period of 1 month, until April 30 inclusive.

In the above situation, the employee has the right to leave for 2 working days.

Let’s assume that the employee’s salary for the time worked was 2800 rubles.

Thus, vacation pay will be:

2800 rub. : 25 days

x

2 days = 224 rubles,

where 25 is the number of working days according to the calendar of a 6-day working week that fall within the time worked.

Example

The employee worked temporarily in the organization from March 16 to April 20, 2007, her salary for the time worked amounted to 3,000 rubles.

When an employee is granted leave, vacation pay will be:

3000 rub. : 30 days

x

2 days = 200 rub.

Vacation pay for employees who have a summarized recording of working time.

Payment of vacations and payment of compensation for unused vacations to employees for whom a summarized recording of working time is established, in connection with the decision of the Supreme Court of the Russian Federation dated July 13, 2006 No. GKPI 06-637, is made in the generally established manner on the basis of average daily earnings, which in accordance with Art. 139 of the Labor Code of the Russian Federation (as amended by Federal Law No. 90-FZ of June 30, 2006) is calculated for the last 12 calendar months by dividing the amount of accrued wages by 12 and by 29.4 (the average monthly number of calendar days).

In addition, when calculating average earnings, you should be guided by the Regulations on Average Earnings, which apply to the extent that does not contradict current legislation.

In accordance with clause 9 of this Regulation, when one or more months of the billing period are not fully worked out or time is excluded from it in accordance with clause 4 of the Regulation, the average daily earnings are calculated by dividing the amount of actually accrued wages for the billing period by an amount consisting from the average monthly number of calendar days (29.4), multiplied by the number of fully worked months, and the number of calendar days in incompletely worked months. The number of calendar days in months not fully worked is calculated by multiplying the working days on the calendar of a five-day working week per hour worked by a factor of 1.4.

This mechanism for calculating the number of calendar days in months not fully worked is applied regardless of the work schedule of a particular employee. Thus, as a general rule, the number of calendar days in the months of the billing period that are not fully worked is also calculated for employees with a summarized accounting of working time.

In accordance with paragraph 2 of Art. 253 of the Civil Procedure Code of the Russian Federation, establishing that the contested normative legal act or part thereof contradicts a federal law or other normative legal act that has a broader

greater legal force, the court recognizes the normative legal act as ineffective in whole or in part from the date of its adoption or another time specified by the court.

The decision of the Supreme Court of the Russian Federation No. GKPI06-637 dated July 13, 2006 does not indicate the time from which the court declared paragraph four of clause 13 of the Regulations on the specifics of the procedure for calculating average wages, approved by Decree of the Government of the Russian Federation dated April 11, 2003 No. 213, invalid.

By virtue of Art. 253 of the Civil Procedure Code of the Russian Federation, a court decision to recognize a normative legal act or part thereof as invalid shall enter into legal force according to the rules provided for in Art. 209 of this Code, and entails the loss of force of this normative legal act or part thereof, as well as other normative legal acts based on the recognized ineffective normative legal act or reproducing its content.

According to Art. 209 of the Civil Procedure Code of the Russian Federation, court decisions come into force upon the expiration of the period for appeal or cassation appeal, if they have not been appealed.

Thus, in our opinion, the above decision of the Supreme Court of the Russian Federation should be followed from the date of its entry into force.

Example

An employee with a cumulative accounting of working hours in October 2006 (the month of the billing period) was sick from October 16 to the end of the month.

For the period from October 1 to October 15, 2006, he worked 90 hours according to the schedule.

But regardless of the number of shifts worked during this period and their duration, the number of calendar days in this month accepted for calculating vacation pay will be:

10 days

x

1.4 = 14 days, where 10 are working days according to the calendar of a 5-day working week, falling on the time worked in the period from October 1 to October 15.

4. Calculation of vacation pay when the billing period is not fully worked out

In the event that one or more months of the billing period are not fully worked out or time is excluded from it in accordance with clause 4 of the Regulations, the average daily earnings for vacation pay are calculated by dividing the amount of actually accrued wages for the billing period by the amount consisting of the average monthly number of calendar days days (29.4), multiplied by the number of fully worked months, and the number of calendar days in months not fully worked (clause 9 of the Regulations on average earnings).

In addition, this Regulation also defines a new mechanism for calculating the number of calendar and working days according to the calendar of a six-day working week in months that are not fully worked: the number of calendar days in months that are not fully worked is determined by multiplying the working days according to the calendar of a five-day working week that fall on the time worked, by a factor of 1.4.

Example

The employee is granted annual leave from April 2, 2007. The organization has established a billing period of 3 calendar months. In the billing period, January and March were fully worked; from February 14 until the end of the month, the employee was sick.

The amount of accrued wages in the billing period was, for example, 6,000 rubles.

Thus, the average daily earnings to pay for vacation will be:

6000 rub. : (29.6 days

x

2 + 9 days

x

1.4) = 71.8 rub.

Example

The employee went on vacation lasting 30 calendar days in May 2007. In the billing period (3 calendar months) February: fully worked, from March 15 to 17 the employee was sick, from April 22 to 30 he was on a business trip.

In the billing period, the employee received a salary in the amount of 18,000 rubles.

Let's calculate the number of calendar days per hour worked in March and April:

March: 19 days

x

1.4 = 26.6 days;

April: 15 days

x

1.4 = 21 days.

Find the average salary to pay for vacation:

18,000 rub. : (29.6 + 26.6 + 21) days

x

30 days = 6994.82 rub.

Example

An employee who has a four-hour working day is granted annual leave from April 19, 2007. In the billing period (3 calendar months), January was fully worked, from February 1 to February 11 the employee was on a business trip, and from March 15 to the end of the month he was sick.

The amount of accrued wages in the billing period was, for example, 7,000 rubles.

Business trip time and sick time based on clause 4 of the Regulations on Average Earnings are excluded from the calculation period. Since the billing period has not been fully worked, the average daily earnings are determined by dividing the amount of accrued wages in the billing period by the total number of calendar days determined for fully worked months (29.6) and falling on the time worked in incompletely worked months.

From February 12 to the end of the month, the employee worked all working days according to his schedule, so this period is considered worked. The same is true from March 1 to March 15 - the time was worked completely in accordance with the schedule.

Thus, the average daily earnings to pay for vacation will be:

7000 rub. : (29.6 + 11

x

1.4 + 9

x

1.4) days = 121.53 rubles.

How is the number of calendar days in not fully worked months of the pay period determined for those working on a six-day working week calendar?

The number of calendar days in months of the billing period that are not fully worked when paying for vacations is calculated by multiplying the working days on the calendar of a five-day working week per hour worked by a factor of 1.4, regardless of the established length of the working week.

Are vacation pay included in the calculation of average earnings?

Hello, Raisa. When calculating the average daily earnings for vacation pay, the excluded periods are: the time the employee is on a business trip, vacation, and the period of temporary disability (clause “a”, clause 5 of Regulation No. 922, approved by the Decree of the Government of the Russian Federation of December 24, 2007, Letter of the Ministry of Labor No. 14-1 /В-608 dated 08/13/2020 N 14-1/В-608, Letter of the Ministry of Labor No. 14-1/В-351 dated 04/15/2020). That is, when calculating average earnings to accrue vacation pay to your employee, you must exclude all of the above periods, including the previous vacation.

Hello, Lydia. I don’t want to repeat myself, since there is already a similar topic on the forum. Look at the forum topic “Calculation of vacation pay for an incomplete year of work.” There is a very detailed formula for calculating vacation pay for the fully worked year option and for the option with excluded periods.

Are vacation pay included in the calculation of average earnings?

Average earnings is the average salary of an employee for a particular period of time. This figure is needed in calculations related to vacation payments, cash benefits for disabled employees and when calculating the amount of pension savings.

In 2007, a decree was issued that prescribed new rules for calculating the average salary of an employee. The calculations include absolutely all payments to the employee from the employer, which are taken into account in determining the tax base for the Unified Social Tax, transferred to the Social Insurance Fund of the Russian Federation. In this regard, one point has always been unclear for accounting employees: what to do with vacation pay that was paid to an employee in the current year, because they are also subject to accounting for the unified social tax.

Is vacation pay included in the new vacation calculation?

If during the 12 months of the accounting year there were some months when the employee was absent for some reason or income that was not subject to inclusion in the payroll was deducted, the SDZ calculation is calculated by dividing the total amount of accrued wages for the previous accounting period by the average monthly value of calendar days (29.4), multiplied by the number of full months and calendar days in partially worked months.

In addition, at enterprises there are additional permanent bonuses and purely internal additional payments, fixed by the collective agreement and individual employment contract. All wages and additional payments and remunerations included in the collective agreement according to the collective agreement are accepted for calculating vacation pay. The specifics of including bonuses in wages based on the results of a quarter or year are explained in detail in the regulation “On the specifics of the procedure for calculating average earnings.”

More to read: According to Article 228.1, 320 Hours of Work were assigned

Calculation of average wages - formula, example and how to calculate vacation pay

- Salary according to the staffing schedule, or payment for hours of work (according to the tariff);

- Allowances for working at night, as well as on weekends and holidays;

- Bonuses and allowances for combining job responsibilities and expanding service areas;

- Payment according to orders for piecework;

- Incentive payments;

- Long service allowances;

- Allowances for working with information containing government documents. secret;

- Bonuses for having a certificate of honor or an academic degree;

- Payment for checking notebooks and written work;

- Payments to state and municipal employees;

- Regional coefficient, northern allowances;

- Payment in kind.

- Temporary disability;

- Annual paid vacation;

- Maternity leave;

- When an employee performs outside work, by order of the manager, but at the same time his earnings are retained (public works, negotiations);

- When calculating severance pay when reducing a position in the staffing table;

- In case of dismissal, when calculating the final payment;

- When calculating travel expenses;

- When calculating vacation pay for the period of study;

- When forced downtime occurs due to the fault of the authorities;

- Salary calculation for the day of the donor;

- Payment for days to undergo a mandatory medical examination;

- During the period of military retraining.

Calculation of average earnings for vacation pay

Now you need to correctly calculate the number of days in months that are not fully worked. To do this, you need to use the formula: 29.3 / K * (K - IskD), where K is the number of calendar days in an incompletely worked month, IskD are calendar days that are excluded from this month.

Every officially employed employee has the right to annual paid leave. This is stated in Art. 114 Housing Code of the Russian Federation. In addition, the vacation must be paid by the employer, based on average earnings for the last year. We are not talking about calendar years, but about working years. Each working year begins on the date on which the employee entered into an employment contract with the employer.

Right to annual leave

Every person, even those who are especially sensitive to their work responsibilities, needs rest, since strength needs to be restored, and personal issues also need to be resolved, all of which naturally takes time.

For these purposes and tasks, the legislator provides for annual paid leave. The key word in this phrase is “annual”, especially this time period is important for those who got a job not so long ago, as it will be when they can take a break from routine everyday life.

According to the current legislation in our country, the minimum period after which an employee can go on another vacation is 6 months. But what should you do if a person has not worked for a new employer for six months, and you need a vacation now?

Meanwhile, official documents also take into account this scenario, because there is a clarification that leave can be issued earlier with the agreement of the parties, that is, the employee and the employer.

Regardless of what time period has passed since the conclusion of the employment contract, if necessary, you should try to negotiate a vacation with management, but you need to take into account one important aspect: if the cherished 6 months have not yet expired, then the vacation can only be administrative, that is, unpaid.

Rules for calculating average earnings for vacation pay, examples with formulas

The average salary of an employee is the main indicator necessary when calculating the amount of vacation pay. You need to understand the specifics of calculating this indicator: which days should be taken into account in the calculation and which should not, how changes in salary and the amount of bonuses paid affect the calculation, how to calculate the average earnings of an employee hired in the current month, and much more. In the article we will talk about calculating average earnings for vacation pay and give examples with explanations.

- Step 1. Determine the period for calculating average earnings. According to the Tax Code, such a period is a calendar year (12 months). If an employee goes on vacation in March 2020, then the billing period for him will be February 2020 - February 2020 (02/01/16 - 02/28/17).

- Step 2. Calculate the employee's income for the pay period. To do this, sum up the salary paid to the employee, as well as the amounts of additional payments, compensations, bonuses provided for by the remuneration system. The employee’s total income for the billing period will be an indicator of annual earnings.

- Step 3. Calculate your average daily earnings according to the formula given above. When calculating, take into account the monthly average of calendar days: for 2020 it is 29.3.

Also read: At what age can energy drinks be sold?

Calculation of average daily earnings for accrual of vacation pay

When calculating vacation compensation, we must use the following formula:

- SDZ – average daily earnings;

- FZP - actual accrued wages for the 12 months preceding the accrual of vacation pay;

- RP – billing period, number of months worked for this year;

- 29.3 – average number of days in a month.

The billing period is usually twelve months; it is used when calculating travel allowances, study leave, and annual paid leave. But in case of dismissal, it may be less than 12, that is, the employee has not fully worked the conditional working year.

For example, an employee was hired on March 11, 2005. The period for calculating annual leave is considered to be 12 months (from March 11, 2020 to March 10, 2020). If the employee quits on February 2, 2020, then the pay period will be considered 10 months (from March 11, 2020 to January 10, 2020)

Example of vacation pay calculation:

Employee Ivanov I.I. went on vacation by order from February 15, 2017. Before the vacation, Ivanov I.I. I didn’t get sick, I didn’t go on a business trip, I didn’t take vacation at my own expense. His salary for 12 months amounted to 45,600 rubles.

We calculate the average daily earnings: 45,600 rubles/351.6 days. = 129.69 rub.

The amount of payment for vacation will be: 129.69 rubles * 28 days. = 3631.32 rub.

351.6 days – this is the average number of days for 12 months. (29.3*12).

When dismissing an employee, the accountant is required to issue a certificate 182n. 2-NDFL. With their help, the accountant at his next place of work will be able to calculate the FFP.

EWP is an economic indicator that reflects the ratio of the real income received by an employee to the real time he worked.

In all cases when its calculation is required, the accountant must remember that the size of the FFP cannot be lower than the minimum wage. installed in the Russian Federation.

How is the average salary for vacation calculated?

- wages at tariff rates, work performed at piece rates;

- commissions and interest received from the sale of goods or services;

- wages paid in non-monetary form;

- allowances and additional payments for experience, specific skills, craftsmanship, and so on;

- coefficient for working conditions;

- bonuses if they are included in the wage system and fall within the pay period;

- financial assistance up to 4,000 rubles.

The length of the rest period does not affect the calculation of average earnings for vacation pay, but it does affect the overall total amount. The accountant needs to remember that if he takes the total number of days allotted to an employee in parts, for example, ten days in May and twenty in August, he needs to carefully monitor their total number. Because in the example from the previous sentence, two days for such an employee will already go towards the future pay period, which he has not yet worked.

Calculation procedure

The calculation of average earnings and the accrual of funds before the vacation takes place according to a certain algorithm. To do this, accounting takes the period of time worked that has passed since the end of the previous vacation.

When an employee has not worked long enough and has not yet gone on vacation, the time he has worked since his employment is taken as the basis.

For example , the last vacation ended on October 1, and the start of a new one is planned for July 1 of the next year. Accordingly, when the application is approved by management, it is necessary to accrue funds. The established procedure includes accounting for the period of all time worked.

Based on the above example, a period of eight months will be taken into account. This is the time that will pass from October 01 to July 01 . Accordingly, it is this period that will be taken into account when calculating average earnings and vacation pay.

- Then you need to sum up all payments indicated for a certain period . If a period of eight months is taken for the calculation, then the accounting department adds up the entire amount of funds received for the specified time.

- Then the average daily income is calculated . To do this, the volume of transferred funds is divided by the number of days actually worked over eight months.

In this case, those days when the employee took time off at his own expense or was on sick leave are not subject to recording.

As stated above, the accounting department will only take the days actually worked, which are noted in the monthly timesheets.

What is included in the calculation

It is necessary to understand that an employee’s entire income consists of various types of payments. Consequently, the funds that were accrued to him as vacation pay must be taken into account.

They are taken into account additionally, in addition to the amounts indicated above.

However, transfers for the last vacation are the result of previous calculations. Therefore, their non-inclusion in the amount of vacation pay for the current year will lead to a decrease in the actual amount of income. Consequently, this will entail a violation of labor rights and the accrual of smaller payments when going on vacation.

In addition to previous vacation pay, the following payments are taken into account:

- Regular salary . This is a standard salary that is paid to the employee monthly. It includes salary and allowances. They can be very different - for high qualifications, for length of service, for rank, for the complexity and intensity of the work, and so on;

- Premiums paid during the billing period . If bonuses were transferred between vacations, they are included in the total income;

- Payment for sick leave . These transfers are also taken into account and summed up along with the rest of the employee’s income.

Accounting includes in the total amount of transferred funds all payments that were made.

The following algorithm is used:

- First you should set the exact period of time for which transfers will be made;

- It is necessary to combine all earnings into one amount . This will be the baseline value, along with the actual time worked;

- The amount of income is divided by the number of days actually worked during the specified period of time;

- The resulting value will become the average daily income;

- Then the number of rest days is taken, which is set by the human resources department , based on a number of criteria. This is the total length of service, allotted additional days, etc.;

- The average income per day worked is multiplied by the length of the rest period.

Are bonuses taken into account when calculating holiday pay?

Each employee, when going on a well-deserved paid vacation, is interested in fully receiving the required accruals. A pressing question arises whether the bonus is calculated in the average salary for vacation. This aspect is especially in demand for those workers for whom bonuses are the basis of their salary.

Bonuses are taken into account when calculating vacation pay in 2020 based on the period worked and the number of vacations taken. In this matter, it is worth noting that working years and calendar years are different concepts. In the first case, the reference day is the date of conclusion of the employment contract. All other periods, such as month, quarter, year, are calculated accordingly.

Average earnings for calculating vacation pay

Since I.P. Konovalova goes on vacation on July 6; the average daily earnings should take into account payments for the past 12 calendar months, that is, from July 2020 to June 2020. Amounts not related to wages are not taken into account. In this case, this is the cost of training and treatment. Thus, the accruals taken into account amount to RUB 345,000. (394,000 rubles - 24,000 rubles - 25,000 rubles). Average daily earnings are 981.23 rubles/day. (345,000 rubles: 12 months: 29.3 days), and vacation pay in 2020 - 13,737.22 rubles. (981.23 RUR/day x 14 days)

Clause 5 of the Regulations indicates the time that you must exclude from the billing period. These are all periods for which the employee was paid based on average earnings. Namely: time of illness, vacation, business trip, etc. Also exclude amounts accrued during this time from the calculation.

06 Aug 2020 stopurist 1191

Share this post

- Related Posts

- Gestational age maternity benefit

- How to expel a child from his father’s apartment without the mother’s consent

- How to use maternity capital to buy a home without a mortgage

- How far away can I park from the bus stop?

Payments excluded from annual wages for calculating SDZ

According to the article of the Labor Code of the Russian Federation, calendar days are excluded from the billing period for calculating SDZ along with payment:

- regular leave and leave without pay;

- being on a business trip;

- temporary disability benefits;

- maternity leave;

- downtime and organized strikes.

The non-inclusion of previous holidays in the calculation of subsequent holiday pay corresponds to the principle of the inadmissibility of double payment for one period.

Payments that do not take part in the formation of SDZ include social payments:

- one-time financial assistance;

- payment for travel tickets, food and recreation;

- Payment of utility services;

- social help;

- payment for workwear;

- compensation of interest on loans under corporate agreements;

- dividends from shares.