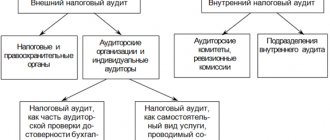

Counter tax audit

One of the methods of tax control popular among inspectors and, to say the least, unloved among business representatives is a tax audit.

Article 87 of the Tax Code distinguishes between desk and field audits. The first are carried out upon submission of virtually any report - controllers simply study the data contained in it, and sometimes they may request additional documents confirming certain figures. The second type of audit is carried out directly in the company itself, where all accounting documents related to the situation being audited are studied. Several years ago, the same article of the code highlighted another type of audit - a counter tax audit. This is a term that is currently excluded from the main tax document of the country, however, events of this type are quite carried out, both as part of an on-site and desk audit. https://youtu.be/NP-bGQoG5VM

Using the Counter Verification Method

A counter tax audit is a procedure in which not the taxpayer himself, but his counterparty, is subjected to a desk or on-site audit.

Questions from inspectors may be raised by a specific transaction or a group of transactions of the taxpayer being inspected. It also happens that in order to understate the tax base, non-existent transactions or transactions with non-existent counterparties are shown in accounting. One way or another, in such situations, inspectors may request from persons connected within the framework of these transactions their copies of documents that were reflected in the records of the inspected payer of taxes and fees. The very fact of the existence of such counterparties, as well as the correspondence of transaction documents from one and the other party, will indicate the correctness of the reflection of data in the accounting and tax records of the audited entity.

Counter verification of documents

This is the possibility of conducting a so-called counter audit, and it is based on the right of the tax inspector conducting the audit, enshrined in Article 93.1, to request these documents or information from the counterparty or other persons who have documents or information relating to the activities of the taxpayer being audited. Inspectors can request the necessary documents at any time during desk or field inspections, as well as upon their completion, for example, at the stage of making a decision upon consideration of the inspection results by the head of the inspection.

In this case, the inspection that conducts an on-site or desk audit of a specific taxpayer for whom doubts have arisen about the correctness of the data reflection must send an order to the Federal Tax Service Inspectorate at the place of registration of its counterparties, from whom it is planned to request counter documents. This instruction indicates why the need to provide documents arose. If controllers need information on a specific transaction, then this request provides information that allows it to be identified. Thus, at this stage of the procedure, only interaction between two tax inspectorates occurs.

Then, within 5 days from the receipt of such an order, the Federal Tax Service Inspectorate at the place of registration of the company or individual entrepreneur who must provide certain documents, sends to its territorially subordinate taxpayer a request for the provision of these papers. The request is accompanied by the above-mentioned instruction from the inspectorate, from which the initiative to conduct a counter-inspection initially came.

The deadline for providing documents on a counter-verification by a taxpayer who has received such a request is also 5 days. During this period, the inspection must be informed about the lack of necessary information if the taxpayer does not have the required documents.

What to do during a counter tax audit if the company or entrepreneur still has documents regarding the transaction of interest to the inspectors? In such a situation, they must be submitted to the inspectorate at your registration address in person, sent by registered mail, transmitted via telecommunication channels or through the taxpayer’s personal account - if there is an appropriate electronic signature.

The response to the tax authorities’ demand is traditionally formalized in an explanatory note. In this case, requesting documents as part of a counter-inspection is no exception. The sample explanatory note in this case should be drawn up in free form. The document can provide information in text form at the request of controllers, provide an inventory of transferred documents, and provide other important information within the framework of the received requirement.

What documents do tax authorities have the right to request when conducting a counter audit?

When conducting counter audits, tax inspectors are given the right to demand any documents relating to the activities of a specific taxpayer.

This is stated in the letters of the Ministry of Finance of Russia dated 10/09/2012 No. 03-02-07/1-246 and dated 10/08/2012 No. 03-02-07/2-136.

According to the internal instructions of the Federal Tax Service, such documents can be contracts, invoices, acceptance and delivery certificates, invoices and other documents that may contain the necessary information about transactions between the organization being inspected and with its counterparties.

Tax authorities may also require the counterparty to provide information about the organization being audited.

Please note that if documents or information are not relevant to the subject of the audit, then tax inspectors do not have the right to demand their provision.

Deadlines for requesting documents for counter verification

Since a request for documents as part of an audit from a counterparty is not actually a tax audit of the person from whom counter documents are requested, there is some kind of legislative conflict in this issue. The limitation of the period of three calendar years preceding the inspection does not apply to these situations, and there are no separate deadlines for requesting information for these cases. So they can also request earlier documents within the general retention period for such papers.

Let us remind you that for primary documents, as well as invoices, which, as a rule, inspectors require as part of counter-inspections in order to confirm transactions, a four-year retention period is established at the end of the tax period in which the document was recorded. Thus, if you receive a request for a document that has already been destroyed due to the expiration of the storage period, then you should inform the inspectors about this in a response letter. It would be advisable to attach confirmation to it, in particular an act of destruction of documents.

Counter tax audit: what to expect from the inspectorate and how to behave?

The Federal Tax Service Inspectorate has received a request to provide a list of documents - invoices, invoices, payment slips, reconciliation statements, etc. - although your company is not currently being audited? Don’t be surprised – the tax authorities are simply conducting a counter-check.

Counter verification is a fairly common occurrence. It’s not as scary as, for example, visiting. However, there are a number of pitfalls, knowing which you will be able to pass the counter check with minimal losses.

Counter check

– this is one of the tax control activities, during which the Federal Tax Service Inspectorate requests information on the activities of the company being inspected from its counterparties.

You will not find such a concept as a “counter audit” in the Tax Code. The essence of a counter audit is that tax authorities try to find violations in the activities of the company being inspected by requesting information and documents about its activities from third parties - counterparties. Therefore, if you receive a request to submit documents or information, this means that one of your counterparties (buyer or supplier) is either already being checked or is planning to be checked by the tax authorities. Inspectors can assign a counter-check of documents to verify a transaction and make sure it exists.

Documents are usually required if the counterparty is already undergoing verification. Information – if the inspection is just being planned, and the inspectors need information about your relationship, i.e. the counterparty is still being “worked through” for the purpose of subsequent verification. Therefore, having received a request to provide information, you can “delight” your business partner - most likely, he needs to prepare for a trip.

How does the counter check work?

The inspectorate, which is checking or is still studying your counterparty, sends an order to request documents or necessary information to your Federal Tax Service. In the order, inspectors must indicate during which tax control activity there was a need to submit documents for a tax audit (and when requesting information regarding a specific transaction, also indicate information allowing the identification of this transaction).

Based on this instruction, your “native” Federal Tax Service issues you a requirement to submit documents. In this case, the inspectors attach a copy of the order to the request.

Within 5 days after receiving the request, you must comply with the inspection requirement.

Important!

For failure to submit documents or even being late, the company faces a fine on counter inspection - 10,000 rubles. (clause 2 of article 126 of the Tax Code of the Russian Federation). Moreover, the amount of the fine in this case does not depend on the number of unsubmitted documents.

Failure to provide information requested by the inspection is also punishable by a fine of 5,000 rubles. If such a violation is committed again within a year, the fine increases fourfold - up to 20,000 rubles. (Article 129.1 of the Tax Code of the Russian Federation).

Safety rules for counter inspection

Obviously, a counter tax audit is a headache for accounting due to the large amount of additional work (you will have to prepare copies of all requested documents). If there is an audit of some large trading company, it will not seem enough to certify a copy of each invoice.

Therefore, if you have received a “chain letter” from the tax office, we advise you not to panic and do not rush to send documents for a tax audit to the Federal Tax Service.

By recklessly complying with the requirements of the tax office, there is a high probability of finding yourself in the field of view of inspectors and triggering an audit in your company (if there are discrepancies with the counterparty’s documents).

Also, if some documents could not be found (or you don’t really want to give them to the inspectorate), you should not hastily compose a response to the counter inspection - “explanatory” letters to the tax office. By writing too much, you can only provoke increased interest in your company.

https://youtu.be/DVWJxDBBIIw

The surest way in this situation is to consult with competent tax lawyers about what documents to provide for a tax audit and in what volume, what written explanations to give, and also whether it is possible to refuse the inspectors (yes, yes, sometimes it is not only possible to refuse the inspection , but also quite legal).

By the way, our tax experts provide such consultations free of charge.

On my own behalf, I’ll give you some simple tips that will help you survive a counter tax audit with minimal losses.

Firstly, never send documents for a tax audit without an inventory - it is very important to make accompanying statements listing the documents submitted.

Secondly, do not neglect answers with banal “closing phrases”. That is, if the inspection writes: “We also ask you to provide other documents related to...”, then in the response message write: “We are sending the following documentation, which was drawn up in relations with the counterparty. If you need to provide additional information, please be more specific...”

Responsibility of the person participating in the counter-inspection

It is interesting that refusal to cooperate in such a situation and failure to provide the requested documents or violation of the 5-day deadline is recognized as a tax offense, despite the fact that the taxpayer in this case is not subject to an audit. The amount of fines provided for in such a case is 10,000 rubles for failure to submit documents on time (clause 6 of Article 93.1, clause 2 of Article 126 of the Tax Code of the Russian Federation), 5,000 rubles for the submission of documents containing false information (clause 6 of Art. 93.1, clause 1 of Article 129.1 of the Tax Code of the Russian Federation), and 20,000 rubles - if the required information is not reported repeatedly during the calendar year (clause 6 of Article 93.1, clause 2 of Article 129.1 of the Tax Code of the Russian Federation).

Responsibility for failure to provide documents

Tax legislation provides for penalties for evading the requirement to submit documents, and officials of organizations and entrepreneurs may incur administrative liability.

If an organization does not comply with the requirements for the submission of documents, evades their submission, or provides knowingly false information, then the liability specified in Article 126 of the Tax Code arises. This offense entails a fine of 5 thousand rubles.

Regulatory regulation

Since January 1, 2007, Article 93.1 of the Tax Code of the Russian Federation has been in force, regulating the request for documents (information) about a taxpayer or information about specific transactions (introduced by Federal Law No. 137-FZ of July 27, 2006).

But the name remains: in practice, the tax authority’s request from one company for documents (information) about another company (about transactions with a counterparty) continues to be called a counter-inspection.

In addition to this article, this procedure is also regulated by the Procedure for the interaction of tax authorities on the implementation of orders to request documents, approved by Order of the Federal Tax Service of Russia dated December 25, 2006 No. SAE-3-06/ [email protected]

Let us take a closer look at what the so-called counter-inspection consists of, what its features are and what measures of liability can be applied to a construction organization based on its results.

Request procedure

In accordance with paragraph 1 of Art. 93.1 of the Tax Code of the Russian Federation, when conducting tax audits, the tax authority that conducts such an audit has the right to request documents.

That is, it is this tax authority that has the right to send an order to the tax office where the organization that has the necessary information about the activities of the company being inspected is registered.

Such and other rules regarding ongoing tax audits are enshrined in Article 93.1 of the Tax Code of the Russian Federation and the Procedure for interaction of tax authorities on the implementation of orders for the requisition of documents (information), approved by Order of the Federal Tax Service of Russia dated 05/08/2015 No. ММВ-7-2/ [email protected]

The counter-verification procedure in accordance with these standards is as follows:

- First, the tax inspectorate sends an order to the tax authority at the place of registration of the organization that has the necessary information about the company being inspected. In this case, the order must be in writing and must contain a request for documents or information (possibly both) from this organization.

- The local tax office is given time - 5 working days - to formalize and send the request to the counterparty of the organization being inspected. This requirement, which specifies the list of requested documents and information, must be accompanied by a copy of the original order received from the tax inspector.

- The counterparty, in turn, is also given 5 working days to respond to the local tax authority. Within this period, the counterparty must either provide all the requested documents or report the absence of the requested documents.

Subject and purposes of the inspection

A counter audit is one of the tax control measures (clause 1 of article 82, clause 1 of article 93.1, clause 6 of article 101 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated April 16, 2007 No. ШТ-13-06/ [email protected] ).

Its essence lies in the provision of information by companies about each other or the receipt by tax authorities of the necessary information from third parties.

The objectives of such an audit are:

– confirmation of the reality of the existence of the counterparty and the transactions performed by the taxpayer;

– confirmation of the coincidence of data on financial and economic transactions of the counterparty and the taxpayer being audited.

Based on the results of the counter audit, no decisions are made that are binding on the taxpayer. But the materials obtained are used as evidence of tax offenses.

A tax official conducting a tax audit of any organization has the right to request these documents (information) from the counterparty or other persons who have documents (information) relating to the activities of the taxpayer being inspected.

Request for documents (information) can be carried out:

– as part of an on-site or desk tax audit;

– as part of additional tax control measures when considering tax audit materials;

– outside the framework of tax audits, if the tax authorities have a justified need to obtain information regarding a specific transaction.

A request for the submission of documents (information) as a counter-verification may be sent to:

– the counterparty of the taxpayer being audited;

– another person who has the documents (information) necessary for tax authorities concerning the activities of the taxpayer in respect of whom the audit is being carried out (clause 1 of Article 93.1 of the Tax Code of the Russian Federation).

As you can see, the demand can be sent to almost any person.

What you need to know ↑

During a desk inspection, inspectors may have questions related to the activities of enterprises in relation to other persons.

The tax office requests the documents it needs to clarify the situation. Counter audits by tax authorities are carried out only as part of desk or on-site audits.

The basis for it is the presence of a document - a written request (covering letter), which is drawn up by the tax authority.

Situations when an inspection may be ordered:

- there are suspicions of double documentation;

- fictitious documents or unreliable facts;

- the quarter in the reporting does not match;

- assumptions that the taxpayer hides real income and does not fully reflect it in the reporting.

Also, the reason for starting a counter check may be the absence of an agreement between the partners or its incorrect execution.

How is it carried out? The inspection employee and his agent may be registered with different services.

The Tax Code of the Russian Federation does not establish which tax service should conduct a counter audit.

The taxpayer should know the following points:

- a counter audit is carried out in such a way as to obtain information from one taxpayer about another;

- without a desk check, a counter check cannot be carried out;

- subject – information, documentation about financial and economic relations of several persons;

- Without a written request, tax authorities cannot require documents.

Basic Concepts

| Tax audit | A procedural action carried out by tax authorities in order to detect offenses. During the audit, tax control data is compared with the data in the reporting declarations |

| Declaration | An act of a legal nature that formulates the principles and goals of the two parties |

| Counter tax audit | This is an audit carried out by tax authorities to study the activities of counterparties |

| Document | A carrier of material that has details. It records all information about activities |

| Counterparty | One of the parties to the contract being concluded. This is an individual or legal entity that must perform certain duties |

Pursued goal

Unlike a desk audit, a counter audit does not apply to tax audits. Its essence is to provide companies with information about each other.

The objectives are as follows:

- Confirm the existence of counterparties and the implementation of transactions by the taxpayer.

- Reconcile information and data on financial and business transactions carried out by counterparties and the taxpayer.

- Check the authenticity of documents.

- Confirm the legality of use and record keeping.

The main purpose of the counter audit is to identify the details of the transaction and the proceeds received from it.

The tax inspector conducts this audit if he believes that the taxpayer has unlawfully used the goods of the transaction or has hidden the real amount of proceeds.

Normative base

When exercising control over citizens who pay taxes, tax services are guided by several documents - the Constitution, the Tax Code, and regulations.

Article number 87 of the Tax Code of the Russian Federation states that if the tax authority has questions related to the activities of organizations, then they have the right to order a counter-inspection.

It is not independent and can only be appointed in accordance with a desk audit.

The Tax Code and the Constitution do not establish a counter audit; it is independent. This is more of a right than an obligation. There is an exception to this rule.

The Order of the Tax Service, signed on December 27, 2007 (No. BG - 3 - 03/461), states that the management of the tax inspectorate can schedule a counter audit within 10 days.

On January 1, 2007, Article No. 93.1 came into force, approving the right of tax services to demand documents from the taxpayer.

Also, the Tax Code does not establish deadlines for reporting requirements. According to Article 129.1, if the taxpayer fails to present documents, he will be subject to a fine.

It amounts to approximately 20,000 rubles. The counter audit must be carried out in accordance with Articles 93 and 94 of the Tax Code of the Russian Federation.

A counter audit may be appointed in accordance with paragraph 2 of Article 31 of the Tax Code. The procedure for its implementation is provided for in Chapter 14 of the Tax Code.

Requested documents

The judges supported the tax authorities, agreeing that the sales book may contain information about the business transactions of the taxpayer being audited. By ruling of the Supreme Arbitration Court of the Russian Federation dated January 19, 2012 No. VAS-17466/11, the transfer of this case to the Presidium of the Supreme Arbitration Court of the Russian Federation for review in the supervisory order was refused.

Due to the fact that the list of documents is not clearly defined, disputes are possible. It should be noted that the court in each specific case will clarify the real connection of the requested documents (information) with the activities of the taxpayer being audited. However, arbitration practice is developing in favor of inspectors (resolutions of the FAS North-Western District dated July 9, 2010 No. A56-43641/2009, FAS Central District dated September 11, 2008 in case No. A09-844/2008-16, FAS Ural District dated May 19, 2008 No. Ф09-3423/08-С3).

So a construction company, if the inspection requests from it any documents about the counterparty, should treat this carefully.

Moreover, tax authorities have the right to request from the organization documents (information) relating not only to the taxpayer being audited, but also to persons who are not in a contractual relationship with him, if these documents are related to the activities carried out by him.

In particular, such third parties may be subcontractors. Although they do not have a contractual relationship with the customer under a construction contract, the documents drawn up under subcontract agreements relate to the customer’s activities in the construction of the relevant facility. This is confirmed in the decisions of the Seventh Arbitration Court of Appeal dated June 2, 2010 No. 07AP-3648/10, FAS Moscow District dated November 16, 2009 No. KA-A40/11998-09.

It must be remembered that, as part of a counter-inspection, it is prohibited to repeatedly request documents about counterparties that were presented by the taxpayer during a desk (on-site) audit against him.

An exception is cases where documents were previously submitted to the tax authority in the form of originals, which were then returned to the person being inspected, as well as when documents sent to the tax authority were lost due to force majeure (clause 5 of Article 93, clause 5 of Article 93.1 of the Tax Code of the Russian Federation).

Requests when checking a counterparty

The procedure for requesting information from a taxpayer when checking its counterparty is regulated by Article 93.1 of the Tax Code of the Russian Federation. This article establishes what can be demanded in such a situation, and also defines the procedure for submitting a demand. Let's start with a description of this procedure.

Request direction

A taxpayer who has received such a request must take into account that in the vast majority of cases it is initiated not by the “native” Federal Tax Service, but by the tax authority with which its counterparty is registered. However, the requirement itself, according to the rules of Article 93.1 of the Tax Code of the Russian Federation, is sent by “its own” inspection. That is why the request made by “their” Federal Tax Service must be accompanied by a copy of the order from the inspection initiator of the request.

Receive requests from the Federal Tax Service for free and send the requested documents via the Internet

Without this copy, a request can be sent only in one case: when the taxpayer being audited and the addressee of the request are registered with the same Federal Tax Service (i.e., the inspection initiating the request coincides with the inspection that sent the request). In this case, the Federal Tax Service does not give itself any instructions and, accordingly, a copy of the instruction is not attached to the request (letter of the Federal Tax Service of Russia dated December 16, 2014 No. ED-4-2/26018, resolution of the Federal Antimonopoly Service of the North-Western District dated January 18, 2008 in case No. A26 -1964/2007).

Let us note that a copy of the order is a very useful document for the taxpayer. So, from it you can find out during which tax control event the tax authorities required documents and information. This copy also allows you to check whether the information requested by your “own” Federal Tax Service corresponds to the instructions of the inspection initiator of the request. After all, judicial practice proceeds from the fact that in such a situation the requirement to provide documents (information) is drawn up on the basis of an order and cannot go beyond its scope. This means that if documents are requested that are not specified in the copy of the order, such a requirement is illegal in the relevant part (resolutions of the Federal Antimonopoly Service of the Ural District dated January 27, 2012 No. F09-8983/11 and the Moscow District Federal Antimonopoly Service dated March 26, 2009 No. KA-A40/2089- 09).

At the same time, it should be taken into account that if the inspection does not attach a copy of the order to the request, the court may not recognize this as a gross procedural violation (Resolution of the Federal Antimonopoly Service of the Ural District dated May 19, 2008 No. F09-3423/08-S3). Therefore, we do not advise ignoring the requirement to provide documents (information) just because a copy of the order is not attached to it. But it is quite possible to appeal such a requirement. If the court considers it illegal, the taxpayer will be able to demand reimbursement of expenses for fulfilling such a requirement in the manner prescribed by article of the Tax Code of the Russian Federation.

Contents of the requirement

As for the content of the requirement related to the verification of the counterparty, practice here proceeds from virtually complete permissiveness for tax authorities. The fact is that in the Tax Code of the Russian Federation for this case there are no restrictions at all, either on the composition of the requested documents (information), or on the circle of persons from whom they can be demanded. Based on this, the courts consider disputes about the right of the Federal Tax Service to request certain information about counterparties.

Check the counterparty for signs of a shell company

Thus, the Arbitration Court of the Ural District indicated that in its requests the Federal Tax Service is not limited to documents relating to the first counterparty of the taxpayer being inspected. This means that such demands can also be sent to counterparties of the second, third and subsequent levels (resolution dated 02.08.18 No. F09-4001/18).

And the judges of the Far Eastern District explained that Article 93.1 of the Tax Code of the Russian Federation does not limit the list of requested documents (information) only to those that, according to the rules of the Tax Code of the Russian Federation, are the basis for the calculation and payment (withholding and transfer) of taxes and fees. Therefore, the Federal Tax Service can request absolutely any documents (any information) regarding the taxpayer being audited. Including those that are not directly related to confirming the correctness of calculation and timely payment (withholding and transfer) of taxes and fees (Resolution of the Federal Antimonopoly Service of the Far Eastern District dated July 25, 2018 No. F03-2969/2018). There are also no restrictions on the form of the requested data - the Federal Tax Service can legally require information in the form of explanations (Resolution of the Federal Antimonopoly Service of the Far Eastern District dated June 17, 2014 No. F03-1810/2014).

At the same time, tax authorities are not required to justify their demands and prove that the requested information is really necessary when checking the counterparty (resolution of the Arbitration Court of the North-Western District dated 05.21.18 No. F07-4963/2018). Thus, the Arbitration Court of the Moscow District recognized the legality of the request for data on the IP addresses of counterparties, indicating that this data can be used to determine signs of interdependence and coordination of actions of taxpayers. This means that they are related to the inspection and were legally requested (resolution dated 03/05/19 No. F05-1297/2019).

Carry out automatic reconciliation of invoices with counterparties

There are also no restrictions on the period of verification of the counterparty in connection with which documents or information are requested. According to the courts, the question of whether specific documents relate to the taxpayer being inspected, as well as the range of circumstances established with the help of these documents, is exclusively within the competence of the Federal Tax Service (Resolution of the Moscow District Arbitration Court dated September 13, 2018 No. F05-14465/2018). At the same time, the inspection is not obliged to explain to the addressee of the request the connection of these documents with the inspection being carried out. It is enough just to indicate this circumstance in the requirement. Thus, the fact that the documents requested for the counterparty relate to a period that is not covered by the audit does not exempt the organization from fulfilling the requirement (Resolution of the Arbitration Court of the Volga District dated January 16, 2019 No. F06-41326/2018).

It should also be taken into account that tax authorities have the right to request documents even if they contain personal data of third parties (including employees of the organization). The basis is the provisions of subparagraphs 1 and 4 of paragraph 1 of Article of the Federal Law of July 27, 2006 No. 152-FZ “On Personal Data”. From these norms, it happens that the processing of personal data can be carried out without the consent of the subject of personal data if it is necessary for the execution of the powers of federal executive authorities. (See also paragraph 3 of Roskomnadzor’s clarification dated December 14, 2012 “Issues relating to the processing of personal data of employees, applicants for vacant positions, as well as persons in the personnel reserve”). And the tax authorities are precisely one of the federal executive authorities (Decree of the President of Russia dated May 15, 2018 No. 215). Thus, a reference to the fact that the requested documents contain personal data will not exempt from a fine for failure to provide these papers (letter of the Ministry of Finance of Russia dated 10/09/12 No. 03-02-07/1-246, see “Tax officials have the right to request that an organization provide full-time schedule and orders for sending employees on business trips to the taxpayer being audited”).

Determine the likelihood of an on-site tax audit and receive recommendations on the tax burden

Whose requirement to fulfill?

The Tax Code of the Russian Federation does not provide for such a procedure.

The organization with which the organization is registered (that is, its own inspection) must request the necessary documents relating to the activities of a company being inspected by another inspection, on behalf of the tax authority carrying out the inspection or other tax control activities (clause 3 of Article 93.1 Tax Code of the Russian Federation).

Based on the received instruction, the relevant tax authority, within five days, sends a request to the construction organization to submit documents (information) with a copy of the instruction to request documents (information).

If both organizations (the one in which the audit is being carried out and its counterparty, from whom the tax authorities want to receive additional information about the activities of the company being inspected) are registered with the same tax inspectorate, then the requirement to submit documents is made by this inspectorate itself.

Features of working with subaccounts in 1C Accounting

Now let's see how not to make mistakes when working with subaccounts in 1C Accounting. To begin with, I will give a simple example of a document in which you need to indicate subconto values. A document of the Manual Operation type is shown in the screenshot below.

The figure shows that all accounts indicated in the postings have only one subaccount. By the way, in 1C Accounting, where subcontos are required to be indicated, they can often be designated as Subconto 1, Subconto 2, Subconto 3. This usually occurs in tabular sections, like the one shown in the figure above. And here is another example of filling out a subconto. This time it is one of the tabs in the Expense Report.

Only Subconto 1 is also indicated here.

Sometimes it is necessary to indicate not the value of the subconto itself, but the type of subconto. That is, for example, not a specific counterparty, but the subaccount type “Counterparties”. The screenshot below shows a fragment of the Subconto Analysis report. Since the program itself does not know which specific subaccount the 1C Accounting user wants to receive information about, this parameter must be specified.

In this example, two types of subcontos are indicated: Items and Warehouses (just a type, not specific values).

Verified period

Accordingly, in their opinion, inspectors have the right to request documents relating to periods that do not coincide with the period controlled within the framework of a desk (on-site) inspection (letter of the Ministry of Finance of Russia dated November 23, 2009 No. 03-02-07/1-519).

At the same time, judges may disagree with this. Thus, the resolution of the Federal Antimonopoly Service of the Central District dated August 9, 2010 in case No. A68-13557/09 states that the request for documents that do not coincide with the inspection period is unlawful. The arbitrators recognized this requirement as arbitrary, that is, the taxpayer is not obliged to comply with it. And on the basis of this, the inspectorate’s decision to hold the organization accountable was canceled.

Deadlines and forms of submission

But if the company does not submit the documents and ignores the requirement, this will be a tax offense, liability for which is provided for, as mentioned earlier, by Article 129.1 of the Tax Code of the Russian Federation. In addition, for failure to provide information necessary for tax control, paragraph 1 of Article 15.6 of the Code of Administrative Offenses of the Russian Federation establishes a fine for officials in the amount of 300 to 500 rubles.

The requirement can be submitted to the head (representative) of the organization personally against signature or electronically via telecommunication channels (TCS). If it is impossible to transmit the demand using the indicated methods, it is sent by registered mail and is considered received after six days from the date of sending.

Please note: judges believe that the organization is obliged to fulfill the demand, even if the deadlines for sending it are violated, considering this circumstance as insignificant and not resulting in a violation of the rights of the counterparty. This conclusion is contained, in particular, in the resolution of the Federal Antimonopoly Service of the West Siberian District dated March 2, 2009 No. F04-623/2009 (1322-A75-49).

Submission of documents on paper is made in the form of copies certified by the organization itself. The requirement for notarization of copies (unless otherwise provided by the legislation of the Russian Federation) is not allowed. If the requested documents are compiled in electronic form in established formats, the organization is allowed to send them to the tax authority electronically via telecommunication channels. › |

If necessary, tax authorities have the right to familiarize themselves with the original documents (Clause 2 of Article 93 of the Tax Code of the Russian Federation).

Desk inspections 2020: what is changing due to COVID‑19

According to the Decree of the Government of the Russian Federation dated 04/02/2020 No. 409, until May 31, 2020 inclusive, the issuance of decisions on the appointment of on-site tax audits and the conduct of already scheduled audits are suspended. Inspections in the field of transfer pricing and foreign exchange legislation of the Russian Federation are also suspended (except for cases where inspections that have already begun reveal violations, the statute of limitations for bringing administrative liability for which expires before June 1, 2020).

In addition to on-site inspections, all deadlines established by the Tax Code for these inspections are also suspended.

At the same time, despite the fact that the reporting deadlines for a number of taxpayers are being shifted, desk departments, control and analytical departments of tax inspectorates and departments that carry out pre-audit analysis continue to work.

Previously, Order of the Federal Tax Service of the Russian Federation dated March 20, 2020 N ED-7-2 / [email protected] suspended until May 1, 2020 checks of compliance with the requirements of the legislation on the use of cash register systems and the use of special bank accounts for making payments.

Postponement of deadlines for submitting documents upon request

Resolution No. 409 made some adjustments to the process of desk audits and fulfillment of requirements for the submission of documents. And therefore, a business that receives any documents from the tax authorities - notices of summons, summonses for questioning, etc., should know that the deadlines for submitting documents at the request of the tax authorities are:

- for 10 working days

For this period, a deferment has been provided for the submission of documents and explanations on the requirements sent as part of desk audits on the NSD and received from March 1 to May 31, 2020 inclusive.

- for 20 working days

The submission of documents and explanations for all other requirements received during this period is shifted to this period.

Thus, the deadlines are increased due to the fact that the period prescribed in the Resolution is added to the standard deadline established by the Tax Code.

Taking into account the announcement of non-working days until the end of April, for companies that do not work during the specified period, the deadline for responding to the requirements of the tax authority is extended even further. However, if the company continues to operate even on non-working days, including remotely, the period of non-working days established by presidential decree is not included in this period.

Clause 7 of Resolution No. 409 indicates the prohibition that is imposed on the application of sanctions for tax offenses under Art. 126 of the Tax Code of the Russian Federation, committed in the period from March 1 to May 31, 2020. That is, if you, as a taxpayer, did not submit documents as part of the audit that is being carried out in relation to your company, or did not submit documents (information) upon request sent as part of counter audits, then liability will not apply.

However, if the application of Art. 129.1 of the Tax Code of the Russian Federation, which relates to failure to comply with requirements directed outside the framework of tax control, that is, for specific transactions, the risk of prosecution remains. In practice, a business may encounter a problem when even more such demands begin to arrive. These requirements may disguise questions that tax authorities usually ask during interrogation.

Tax lawyer Maria Loetskaya, drawing the attention of companies to this fact at the webinar “COVID‑19 Pandemic: Taxes and Tax Control,” asks them to pay more attention to such requirements and analyze their legality. Moreover, it should be expected that after the end of the quarantine period, the tax authorities will exercise enhanced control: the pandemic will affect a radical reduction in tax revenues, while the task of replenishing the budget will not go away.

As experts note, despite the fact that on-site tax audits have been suspended, in practice companies continue to receive demands for the audited period, but with reference to Part 2 of Art. 93.1 Tax Code of the Russian Federation. This is illegal, and if such actions are taken against your company, then you are not obligated to comply with such requirements.

How to respond to demands during a pandemic

Some companies have transferred employees to remote work and continue to operate on declared non-working days. It may happen that the accounting department receives a request from the tax office to present certain documents located in the office. That is, accountants do not have access to documents.

Will the extension of the deadline for providing documents upon request apply to such a company? And what local regulatory act should be used to prove the fact that the accounting department could not fulfill the requirement?

Algorithm of actions

If a company has transferred employees to remote mode, it must have a corresponding order. Since the request was not sent as part of a desk audit on VAT, and the documents are requested outside the scope of the audit, the deadline for its execution is 10 working days. But as mentioned above, Resolution No. 409 extended the deadline for submitting documents, and therefore another 20 are added to the standard 10 working days. Thus, the company has 30 working days to respond to the tax authorities.

During this period, it is necessary to inform that by order of the general director, the company has established a remote work mode for accounting employees and the necessary documents are in the office, there is no access to them.

If the work schedule is not canceled within 30 days due to circumstances, then an answer should be given about the impossibility of submitting documents on time. This must be done to ensure that sanctions are not applied to the company.

A request has been sent as part of an on-site inspection - what to do?

In such a situation, it is logical to refer to Resolution No. 409, within the framework of which all on-site inspections are suspended.

If you receive a counterclaim under Art. 93.1 of the Tax Code of the Russian Federation in connection with an on-site inspection of your counterparty or any third party, it makes sense to refer to the provisions of Resolution No. 409 that all on-site inspections are suspended, and therefore you are part of a counter inspection from March 1 until May 31, they are not required to respond to any counterclaims.

It is also important to remember that the principle of suspending on-site inspections applies to all companies, regardless of the mode in which they continue to operate.

Registration of inspection results

The article was published in the journal “Accounting in Construction” No. 5, May 2013.

Protect yourself from tax audits. An online course from a former employee of the Department of Economic Crimes, and now a well-known tax consultant, is now with a 50% discount. Now for only 2750 rubles.

You will learn to withstand the pressure of tax authorities, behave competently during interrogations and seizures, and protect yourself from criminals and subsidiaries.

Lots of practical advice and a minimum of theory. Training is completely remote, we issue a certificate. Hurry up to buy (we have five more courses at a discount).

A counter tax audit is carried out only as part of an on-site or desk audit.

Purpose of counter check

A counter tax audit is necessary if, during a transaction, the tax authorities need to determine the completeness of the posting of goods received or funds received by the company. To do this, the Federal Tax Service must have reason to believe that the taxpayer did not capitalize the goods received or did not record revenue when providing services, performing work or selling goods.

Important! Tax authorities have the right to check how the counterparty reflected the offset and other transactions carried out with the taxpayer.

This means that the object of such an audit can be not only the taxpayer himself, but also the counterparty who has the necessary information about his financial and economic activities. Both of them may be registered with different tax authorities. Therefore, not only the Federal Tax Service with which the taxpayer is registered and which has the right to carry out an on-site or desk audit can conduct a counter-inspection. At the motivated request of another tax authority, the Federal Tax Service with which the counterparty is registered can also check. The counterparty may be required to provide any information related to the activities of the taxpayer being audited. Conditions for conducting Tax authorities have the right to conduct such events subject to mandatory compliance with two conditions:

- the activities of the company and the audited counterparty are interconnected;

- The counterparty is undergoing an on-site or desk inspection.

If at least one of these conditions is not met, Federal Tax Service employees do not have the right to demand documents for a counter check. When the tax office tries to request from the audited company documents regarding a company cooperating with it, which is not undergoing a tax audit, then these actions of the Federal Tax Service are unlawful.

Oncoming traffic

Material provided by the magazine “Raschet” (No. 9, 2003) You can familiarize yourself with the contents of the issue in the “Periodicals” section or directly on the magazine’s website www.raschet.ru

Nowadays you can buy any accounting documents and company seals. Therefore, tax officials do not put much faith in primary documents and, in particularly suspicious cases, organize counter-inspections.

What is a counter?

Counter audits are mentioned in Article 87 of the Tax Code. It states that tax authorities may demand from the counterparties of the audited company any documents that relate to its activities. And they can do this only as part of an on-site or desk inspection. That is, before the start of any of them, inspectors do not have the right to collect information about the company from its business partners.

As a rule, tax authorities conduct counter audits if the company’s documents raise doubts (not clearly filled out, many corrections, etc.). The main goal of the inspectors is to compare the data in these documents with the data of the company’s counterparties and determine whether there are discrepancies between them.

Sometimes a collision is inevitable. Thus, tax authorities must conduct counter-inspections of all suppliers of exporters. They are obligated to do this by the internal order of the Ministry of Taxes of September 3, 2001 No. BG-14-03/106dsp.

The general rule is this: the more buyers or sellers your company has, the more likely it is that you will encounter oncoming traffic. Either they will ask you for documents, or, conversely, from your business partners.

It's better to be available

Most often, counterparties are “scattered” across different regions and even cities. Therefore, the inspector is obliged to send requests to the tax authorities, in which the partners of the company being inspected are registered. Having received a request, the inspectorate must conduct a counter-check and then report the results to the requesting tax officer.

If the company being inspected and its partners are registered with the same tax office, the same inspector will conduct the counter and main audits.

There is no procedure for appointing and conducting counter audits in the Tax Code. Therefore, tax authorities act according to the general rules of “requesting documents.” Article 93 of the Tax Code is devoted to them.

First of all, the inspector draws up a written request with a list of papers that the partner of the inspected company must submit within five days. Otherwise, he will be fined five thousand rubles. If the counterparty company still does not bring the documents, they will be taken forcibly. This right is given to tax officials by Article 94 of the Tax Code.

Tax officials prefer to present the request in person in order to know for sure whether they will bring papers from the company or not. They will call you and ask you to come to the inspection. If they don’t get through by phone, they will send the demand by mail to the legal address of the company. If it does not coincide with the actual address, then arrange to be notified of incoming correspondence. Otherwise, you won’t find out about the requirement, and your company will be fined.

It is preferable if the tax authorities contact you by phone. In this case, you can check with them the list of required documents and even ask them to wait a little. Inspectors usually agree to this because a few days are not of much importance to them. You can spend it for the benefit of yourself and your partners: check the documents again and make sure that everything is “clean”. Therefore, if your company’s phone number has changed, please notify the tax office in the taxpayer registration department.

There is no point in hiding from the tax authorities, since the company from which documents are requested is, in principle, in no danger: it is not they who are checking. However, if they notice anything suspicious in the documents received, tax authorities may include you in the schedule of on-site inspections for the next quarter. But such cases are quite rare.

Help your neighbor

Of course, it is best if you, as a partner, contact the audited company before submitting the papers to the tax office. This will kill two birds with one stone.

First, find out whether the company is actually undergoing an audit (sometimes tax officials conduct counter meetings before the start of an on-site or desk audit, which is illegal).

And secondly, coordinate your actions with her and decide which papers should be carried and in what form. Perhaps, by putting aside a couple of “extra” documents, you will provide your partner an invaluable service and in a similar situation you can also count on his help.

Coordinated actions during a counter-inspection are very important, since if the data of counterparties for some reason does not coincide with the data of the company being inspected (which is undergoing an on-site or desk audit), the consequences for it can be very undesirable. Tax authorities will be happy to charge her additional taxes, penalties and fines.

In this situation, the task of the audited company is to come up with the most acceptable explanation for the discrepancy. For example, we can say that the accountant of the counterparty, from whom the tax authorities requested documents, made an arithmetic or technical error, lost some papers, etc. (this does not threaten the counterparty in any way).

Tax authorities, of course, will still charge additional taxes, penalties and fines to the company being inspected, but most likely they will not be able to prove anything in court. According to Article 3 of the Tax Code, all irremovable doubts about the guilt of the company must be interpreted in its favor.

It is possible that tax authorities cannot conduct counter audits because they have not found a counterparty. Many people think that nothing could be worse than this. But life proves the opposite: if your counterparties are fly-by-night companies that exist only on paper, you are not afraid of oncoming traffic at all. Any court will say that the company is not responsible for its suppliers. There is confirmation of this in the form of extensive judicial practice. For example, the resolution of the Federal Arbitration Court of the North-Western District dated September 24, 2001 No. A56-3855/01 or the resolution of the Federal Arbitration Court of the Moscow District dated March 19, 2003 No. KA-A41/1306-03.

Let's reduce appetites

The rights of tax officials during counter audits are not unlimited. Firstly, they cannot not only seize, but also demand those documents that are not related to the counterparty being inspected. Therefore, if you are asked for extra papers, you have the right to refuse.

If tax authorities go to court to collect a fine, they will waste their time. In this case, the courts take the side of the companies (for example, resolution of the Federal Arbitration Court of the North-Western District dated May 21, 2002 No. A42-1401/0223).

Secondly, in their requirement, tax authorities should not limit themselves to general formulations like “Submit all documents related to the activities of LLC (ZAO, JSC)...”. They must indicate specific papers that should be brought to the company. Otherwise, the inspectors cannot fine you either (resolution of the Federal Arbitration Court of the North-Western District of May 14, 2001 No. A42-4625/00-5).

Sometimes tax officials are in a hurry and indicate in the request deadlines for submitting documents, which are less than five days from the date of receipt by the company. You shouldn’t follow their lead, since they still won’t be able to collect the fine through the court (Resolution of the Federal Arbitration Court of the North-Western District of May 21, 2002 No. A42-1401/0223).

Tax authorities will not be able to collect a fine through the court even if they have not drawn up a written demand. Without it, the company is not obliged to bring documents to the inspection.

You have every right

Quite often, inspectors ask not only to provide certified copies of any documents, but also to draw up various summary tables. Thus, they want to shift part of their work on analyzing and checking papers to you. You can immediately refuse such a request, and there will be nothing to fine you for, since pivot tables are not considered a document.

Or you can not refuse the tax authorities and try to “exchange” the tables for additional time or reduce the number of documents submitted, which are sometimes unreasonably numerous.

In general, a counter check is not as scary as it seems. And above all, this is a very good test for the company itself. After going through it, you will understand how harmonious your partnership is and whether it is worth continuing it further.

| New generation berator PRACTICAL ENCYCLOPEDIA OF AN ACCOUNTANT What every accountant needs. The full scope of always up-to-date accounting and taxation rules. Connect berator |

Order of conduct

What to do if Federal Tax Service employees decide to conduct a counter-inspection and within what time frame can they do this?

The Tax Code of the Russian Federation does not regulate this procedure and does not set deadlines for it. The tax periods it may cover are also not specified. The law also does not limit the number of repeated events of this type for the same types of tax for the same audited tax period. The general approach to this event was developed on the basis of judicial practice. The judicial authorities believe that during the inspection process, the Federal Tax Service official is obliged to be guided by the general norms of Art. 93 Tax Code. This allows him to issue written requests to the taxpayer to provide a specific list of documents that will directly confirm the economic ties of the taxpayer with the counterparty. Such requirements can be sent by registered mail with notification and confirmation of receipt or transferred to the head of the company against signature. In a specific situation, it all depends on whether the tax authorities legally requested the documents.

General information about subconto

Subconto are analytical accounts. That's all, actually! So if you come across this concept in 1C Accounting (and you will definitely encounter it), then you should keep in mind that in this part of the program we are talking about “analyst”, i.e. clarification. For example, you indicated a counterparty in the document. In this case, you will also need to indicate a specific agreement with this counterparty.

Below is a fragment of the chart of accounts from 1C Accounting 8. The picture shows that the number of analytical accounts (sub-accounts) for different synthetic (numbered) accounts may vary.

In 1C Accounting, an account can have no more than three subaccounts . No more - that means there are accounts that have no subaccounts at all! There is nothing special here, just different accounts require different levels of accounting detail. Examples of accounts without subaccount: 84.01, 82,000.

There are quite a lot of subconto types themselves. Some of them can be seen in the picture below.

What are the consequences of a counter tax audit?

If, during a counter-inspection of a counterparty, Federal Tax Service employees discovered distortions in certain business or financial transactions that directly affected the determination of the tax base, then the materials of this inspection are attached to the report of an on-site or desk audit, or to the decision that was made based on the results of their consideration. After this, they can be used as evidence in an administrative case initiated against the tax payer being inspected for committing a tax offense. How tax authorities reflect the results of a counter audit Clause 1.10.2 of the Instruction of the Federal Tax Service of the Russian Federation No. 60 provides for the procedure for drawing up an on-site tax audit report. It states that its introductory part must contain the following information:

- on conducting counter checks by employees of the Federal Tax Service;

- about documents and objects seized by inspectors;

- on inspection of premises, territory, inventory of property;

- about the examination and other actions taken.

Important! The on-site inspection report is accompanied by materials that were collected after the counter inspections.

In order to properly understand these issues and not fall under tax sanctions after any types of audits, you should seek help from professional lawyers in the field of tax relations. They will advise on counter-inspection issues and help draw up a complaint in case of violation of tax legislation by employees of the Federal Tax Service.

ATTENTION! Due to recent changes in legislation, the information in this article may be out of date! Our lawyer will advise you free of charge - write in the form below.

Results of a counter audit by the tax inspectorate

The indicators of the counter-inspection are drawn up in a separate act and attached to the act (decision) of the on-site or desk inspection. If a tax audit reveals violations, the on-site inspection report will serve as evidence of these violations.

However, the person subject to the on-site or desk inspection is responsible for these violations. In this case, the counterparty may only be liable for failure to submit documents for counter-verification.

https://youtu.be/seBqAyyICpg