Gross violation of accounting and reporting rules

A gross violation of the rules of accounting and reporting is understood to mean an understatement of the amounts of accrued taxes and fees by at least 10 percent due to distortion of accounting data or distortion of any article (line) of the accounting reporting form by at least 10 percent.

For committing these actions, the accountant may be subject to a fine of 2,000 to 3,000 rubles (Article 15.11 of the Administrative Code).

Previously, punishment for committing this offense could not be avoided. However, on November 1, 2013, the amendments introduced by the Federal Law of October 21, 2013 No. 276-FZ to Article 15.11 of the Code of Administrative Offenses of the Russian Federation came into force (read more in the article “Accountant and the Code of Administrative Offences: the presumption of innocence”, magazine “Practical Accounting”, no. 12, 2013).

Important

Now the accountant is exempt from administrative liability in the case of submitting an updated declaration (calculation) and paying on its basis unlisted amounts of taxes and fees, as well as corresponding penalties, in compliance with the requirements of Article 81 of the Tax Code.

Therefore, a fine can be avoided by submitting an amended return if the previously submitted reports do not fully reflect the information or there are errors that lead to an underestimation of the tax amount. If the deadline for filing and paying the tax is missed, then in order to avoid punishment it is necessary not only to provide an “adjustment”, but also to pay the missing amount of tax and the corresponding penalties. Moreover, in both situations, all actions must be carried out before errors are identified by inspectors or the organization becomes aware of the appointment of an on-site inspection.

Exemption from liability is also possible when the “clarification” is submitted after an on-site inspection. However, in this case, during the audit, tax authorities should not discover errors that would lead to an understatement of tax;

In addition, administrative liability can be avoided by correcting errors (including the submission of revised financial statements) before the approval of the financial statements by the founders or shareholders.

Errors are corrected in accordance with PBU 22/2010 (approved by order of the Ministry of Finance of Russia dated June 28, 2010 No. 63n). According to this document, errors are divided into significant and non-significant. The first category includes those errors that, individually or in combination with other errors for the same reporting period, affect decisions made on the basis of financial statements. The organization independently determines the significance of the error and, depending on this, as well as the time when it was identified, makes corrections to the reporting.

Gross acts

The most undesirable thing for a calculation specialist is an accounting violation , which the law recognizes as gross. Fines for it are provided for in Art. 120 Tax Code of the Russian Federation.

The fine for gross violation of accounting records varies from 10 to 30,000 rubles. of accounting violations plays a role here . And that’s not all: if there was an underestimation of the tax base (from 2020, also for insurance premiums), 20% of the underpayment will have to be paid into the budget. Then you definitely cannot avoid the minimum fine for violating accounting rules - 40,000 rubles.

From 2020 Art. 120 of the Tax Code of the Russian Federation is fully applied to the base for calculating insurance premiums.

Violations of accounting rules themselves , which the law recognizes as gross, are quite standard. This includes the lack of “primary” documents, invoices, accounting registers, ineffective or incorrect work with accounting accounts, and violations with financial statements .

Violation of the registration deadline

Based on Article 83 of the Tax Code, an organization must register with the tax authorities at its location, at the location of its separate divisions, real estate and vehicles owned by it, as well as in other cases provided for by tax legislation.

For example, an organization that includes separate divisions is required to register at the location of each division within one month after its creation.

If the filing deadline is missed, then in accordance with paragraph 1 of Article 15.3, a fine in the amount of 500 to 1000 rubles may be imposed on the accountant. If this is the first offense or the deadline for filing an application is not too late, then he may be given a warning.

If registration is not done intentionally, that is, there is direct intent, then the fine will be from 2000 to 3000 rubles (clause 2 of article 15.3 of the Administrative Code).

When will the fine be less?

We hasten to reassure you: there is almost always the possibility that the sanction for accounting violations will be at least two times less. The relevant mitigating facts are named in Art. 112 of the Tax Code of the Russian Federation. However, you don’t need to focus only on them, because this list is open.

Here is what is not mentioned in the Code, but will almost certainly work in your favor in the event of violations in financial statements and accounting in general:

- the violation occurred for the first time;

- a company in financial crisis;

- the business has a bad loan in front of the bank;

- the accounting violation comes from the previous bosses;

- the company promptly and on its own initiative paid additional taxes, penalties, and fines in accordance with the requirements of the Federal Tax Service;

- the fine is too high in relation to the violation.

Violation of the deadline for notification of bank accounts

The organization is obliged to notify the tax office in writing about the opening or closing of accounts (subclause 1, clause 2, article 23 of the Tax Code of the Russian Federation). Accounts include settlement (current) and other bank accounts opened on the basis of a bank account agreement, to which funds are credited and from which funds can be spent.

Notification in form No. S-09-1 (approved by order of the Federal Tax Service of Russia dated June 9, 2011 No. ММВ-7-6/362) is submitted to the tax office within seven days from the date of opening (closing) the account. The period is calculated in working days.

If the accountant does not send this message, then he faces a warning or a fine in the amount of 1,000 to 2,000 rubles (Article 15.4 of the Code of Administrative Offenses of the Russian Federation).

Violation of reporting deadlines

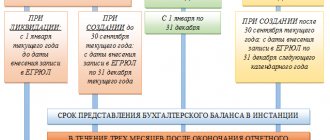

Tax returns (calculations) are submitted to the inspectorate at the place of registration. The deadlines for submission are defined in the Tax Code. For example, an organization’s property tax declaration is sent to the tax office no later than March 30 of the year following the expired tax period (Article 386 of the Tax Code of the Russian Federation).

The declaration (calculation) can be submitted to the tax office in person or through a representative, sent by mail with an inventory of the contents, or transmitted via telecommunication channels.

When the declaration is sent by mail, the day of submission is the date of dispatch of the postal item, and when transmitted via telecommunication channels, the date of dispatch.

For late submission of declarations, an accountant may receive a warning or a fine in the amount of 300 to 500 rubles (Article 15.5 of the Code of Administrative Offenses of the Russian Federation).

Please note that if a company violates the deadline for submitting a declaration by more than 10 working days, the tax authorities have the right to block its current account (Clause 3 of Article 76 of the Tax Code of the Russian Federation).

When exactly will you be fined?

Let's get closer to life and give several cases that many accountants encounter (see table).

| Type of gross accounting violation | What is expressed in |

| There is no necessary “primary” | The accountant took into account the value of the transaction invoices (TN, TTN) and the agreement with the seller |

| An accounting error led to a tax reduction | The specialist incorrectly set the initial cost of the OS. This ultimately affected the property tax of organizations: it is 10% less than the real value |

| Due to an error, the figure in the financial statements is incorrect by 10% or more | The company does not create a reserve for doubtful debts in accounting. As a result, the amount of assets in the balance sheet is incorrect |

| There are imaginary objects in registers | The accountant took into account the costs of construction work that was not carried out at all |

| The registers contain sham transactions | For example, the management decided to cover the rental of premises with contributions from the founders to the fixed capital |

| There is a difference between movement in accounts and data in accounting registers | A typical example of a “gray” and/or “black” salary |

| Mismatch between accounting records and data from registers | Sometimes this is done to increase the company’s chances of receiving borrowed funds from the bank. |

| Storing accounting documents for less than the period established by law | This is how they get rid of an operating system: written off from the balance sheet, the contract for its purchase is “lost forever” |

Failure to provide information

In this case, an offense is failure to submit within the prescribed period or refusal to submit to the tax authorities documents or other information necessary for tax control, as well as submission of such information incompletely or in a distorted form.

The procedure for requesting documents is regulated by Article 93 of the Tax Code. The requirement to submit documents must be fulfilled within 10 days from the date of its receipt by the company. If an organization sends a negative response to the tax office, then the accountant cannot avoid liability. He will be issued a fine in the amount of 300 to 500 rubles (Clause 1 of Article 15.6 of the Code of Administrative Offenses of the Russian Federation).

If any problems arise due to which it is impossible to submit documents on time, then it is best to agree with the inspectorate on changing the deadlines or submitting documents in parts, in order to avoid liability.

What is an offense

So, a violation is considered to be understatement due to distortion of accounting data of the amounts of accrued taxes and fees, as well as distortion of any article (line) of the accounting reporting form. Moreover, liability will arise when the amount of understatement/distortion is at least 10 percent. It is obvious that the object of the administrative violation in question is the rules for maintaining records of property, liabilities and business transactions, the procedure for compiling and presenting comparable and reliable information about the property status of the organization, its income and expenses. This means that in order to be held accountable under Article 15.11, officials need to establish the fact that the amounts of accrued taxes and fees have been understated by at least 10 percent precisely as a result of violation of established accounting rules. And also to determine which norms regulating the procedure for maintaining accounting and presenting financial statements have been violated.

A tax return is not included in the list of elements of financial statements, according to Law No. 402-FZ.

However, a company's correct accounting practices have a direct impact on the tax returns it submits, since errors made in accounting can be transferred by taxpayers to their tax returns. Therefore, we can conclude that a gross violation in the sense of Article 15.11 of the Code of the Russian Federation on Administrative Offenses should be understood as the reflection of deliberately incorrect, unreliable data not only in accounting, but also in tax reporting, which led to an understatement of the tax amount by at least 10 percent.

However, it remains unclear whether acts that can be classified as gross violations of accounting rules, such as:

- lack of primary documents;

- lack of accounting registers;

- lack of financial statements;

- systematic (twice or more times during a calendar year) untimely and incorrect reflection in primary documents, accounting accounts and financial statements of business transactions, tangible assets, intangible assets and financial investments;

- violation of the procedure and deadlines for storing financial statements established by law;

- violation of the deadlines for submitting financial statements established by accounting legislation.

Or such acts should be qualified as failure to provide information necessary for tax control.

Please note that from January 1, 2020, tax authorities may suspend transactions on the accounts of a taxpayer-organization in case of failure to submit a tax return within 10 days after the deadline. The decision to suspend operations can be made within three years from the date of expiration of the specified period.

In cases of failure to submit accounting (financial) statements to the tax authorities, such measures are not provided for by tax legislation (letter of the Ministry of Finance of Russia dated July 4, 2013 No. 03-02-07/1/25590).

Procedure for bringing to responsibility

If violations are detected (for example, during tax audits or when submitting reports), inspectors draw up a protocol on the commission of an offense.

The protocol on the commission of an offense is drawn up by tax inspectors (clause 5, part 2, article 28.3 of the Code of Administrative Offenses of the Russian Federation). In this case, the inspection must notify the accountant of the time and place of drawing up the protocol.

After drawing up, this document is submitted to the magistrate’s court for consideration (Article 23.1 of the Code of Administrative Offenses of the Russian Federation). In this case, the accountants must be notified of the time and place of the trial.

If an accountant believes he is innocent, he must provide evidence of this.

What will the judge take into account?

Firstly, the fact that the offense was committed on the instructions of the head of the organization. In this case, the accountant must provide documents confirming that the offense was not committed voluntarily. For example, an order from the general director.

Secondly, the absence in the employment contract and job description of the obligation to perform certain actions. If the mentioned documents do not indicate, for example, that the chief accountant must submit declarations, then it is impossible to hold him accountable for failure to fulfill or improper performance of such duties.

If the accountant committed an offense intentionally or through negligence, then the judge, taking into account all the circumstances of the case, including mitigating ones, makes a decision in administrative cases. This document indicates the amount of the fine the chief accountant should pay.

The resolution comes into force on the day it is issued and the fine must be paid within 60 days from this moment (Article 32.2 of the Code of Administrative Offenses of the Russian Federation).

For failure to pay a fine on time, a fine of at least 1,000 rubles may also be imposed (Clause 1, Article 20.25 of the Code of Administrative Offenses of the Russian Federation).

Significant errors

Corrections to the annual financial statements are made only for significant errors. These are errors that can lead to a distortion of the overall picture of the financial and economic situation of the company and lead to the adoption of incorrect management decisions by the founders.

The organization establishes how to determine the significance of an error in its accounting policies. You can, for example, write: “an error is considered significant if its value distorts the indicator of any line of the report by more than 10%.”

To correct, all financial reporting indicators must be recalculated under such conditions as if the detected error had never been committed. This method is called the retrospective recalculation method. Firms that maintain simplified accounting have the right not to use the retrospective method of recalculation.

Let's take a closer look at typical errors in financial statements.

Balance Sheet Inconsistency

The balance sheet data as of the 1st day of the reporting year does not coincide with the last year’s balance sheet data as of December 31 of the previous year.

If you have identified a significant error in the previous reporting year, you need to correct it in the current reporting period.

Corrections are made in accordance with clause 9 of the Accounting Regulations “Correcting errors in accounting and reporting” (PBU 22/2010):

- it is necessary to make a correction to the relevant accounting accounts in the current reporting period in correspondence with account 84 “Retained earnings (uncovered loss)”;

- comparative financial statements for the current reporting year must be recalculated as if the error of the previous reporting period had never been made (retrospective restatement).

Incorrect disclosure of debt

If an organization is indebted to a counterparty, an accountant may mistakenly “offset” these amounts and present the balanced result in the reporting as receivables or payables. This cannot be done. The balance sheet must reflect detailed information about the company's assets and liabilities based on analytical accounting data.

Error in reflecting short-term and long-term indicators

When preparing annual reports, questions may arise regarding the correct qualification of loans that are concluded for several years.

In accordance with paragraph 19 of PBU 4/99, according to the maturity date in the balance sheet, liabilities are divided into short-term (with a maturity date of no more than 12 months after the reporting date) and long-term (other liabilities).

If there are no more than 12 months left until the loan obligations are repaid, the loan payables are reflected in the balance sheet as part of short-term liabilities.

If the terms of the agreement provide for the payment of interest simultaneously with the repayment of the loan itself at the end of the agreement, the obligations are also considered short-term. Debt for interest payments is initially considered short-term if there are no special features regarding the timing of interest payments.

Lack of provision for doubtful debts

Absolutely all companies, including small businesses, are required to form reserves for doubtful debts. If there are grounds for creating reserves for doubtful debts, the amount of reserves must be included in financial results in the event that receivables are recognized as doubtful. The basis for recognizing a debt as doubtful are two conditions:

- the debt is overdue (with a high probability of being overdue);

- the debt is not secured by guarantees.

All types of doubtful accounts receivable, including advances paid to suppliers, as well as loans issued, must be reserved in the balance sheet.

There is a debt with an expired statute of limitations

The company’s obligation is to write off receivables and payables for which the statute of limitations has expired.

There is no correspondence between the indicators of the financial reporting forms

Compliance of indicators of reporting forms to monitor the correctness of filling out the balance sheet and verifying the correctness of accounting. This is an important procedure that completes the preparation of financial statements.

When an accountant is innocent

The chief accountant cannot be held administratively liable for offenses committed by his predecessor. This directly follows from the provisions of Article 1.5 of the Code of Administrative Offenses of the Russian Federation, which states that a person can be held accountable only for those offenses for which his guilt has been established. Accordingly, if such an offense is detected, the accountant who worked at that time will be held accountable.

Also, administrative liability will not occur if the statute of limitations for bringing to it has expired. In cases of violations of legislation on taxes and fees, this period is one year. It is calculated from the moment the administrative offense was committed, and not from the moment it was discovered by the tax authorities.

If the offense was committed while the chief accountant was absent from work (for example, he was sick), then the employee who temporarily performed his duties will bear responsibility.

When you shouldn't be fined

Some accounting violations can be avoided without a fine. Here are some real life examples.

Reports were submitted with approximate amounts

This happens when you are about to give up, but there is no initial information. The result is underpayment of taxes. We definitely advise you to immediately pay the required amounts and submit an updated declaration. The second way: if you're lucky, eliminate all inaccuracies before the financial statements are approved.

The employee quit, but did not receive a 2-NDFL certificate

It is customary to provide an income certificate for the employee who asked for it. Three working days are given for this. Please note: if such an application is received on the last day of work, the three-day rule continues to apply. You can cook it all this time.

Also see “Applying for a 2nd personal income tax certificate”.

What else is the answer for?

The chief accountant, like any other employee, may be subject to disciplinary action. This type of responsibility is provided for by labor legislation. Thus, for failure to perform or improper performance of job duties, disciplinary sanctions may be applied to an accountant: reprimand, reprimand or dismissal on appropriate grounds.

The accountant may also be held financially liable. In this case, the condition of full financial responsibility must be contained in the employment contract or in an additional agreement to it. If such a condition is absent, then damages can only be recovered from the chief accountant in the general manner, that is, within the limits of average monthly earnings.

I.D. Shilov

, lawyer, for the magazine “Practical Accounting”

What mistakes should you not make?

The berator “Encyclopedia of Accounting Errors” examines 300 of the most common accounting errors. For each, you receive recommendations: how to correct them in tax and accounting, and how to prevent them in the future. Use other people's experience to your advantage! Find out more >>

Material liability

The head of the organization bears full financial responsibility for direct actual damage caused to the organization (Part 1 of Article 277 of the Labor Code of the Russian Federation). Moreover, such responsibility for the manager occurs regardless of whether the employment contract with him contains a condition on full financial responsibility or not (clause 9 of the resolution of the Plenum of the Supreme Court of the Russian Federation dated November 16, 2006 No. 52 “On the application by courts of legislation regulating the financial liability of employees for damage caused to the employer”, hereinafter referred to as Resolution No. 52).

Full financial liability occurs for direct actual damage caused to the organization (Article 242 of the Labor Code of the Russian Federation).

Direct actual damage means:

- a real decrease in the available property of the employer (organization) or deterioration in the condition of the said property (including the property of third parties held by the employer, if the employer is responsible for the safety of this property);

- the need for the employer (organization) to make expenses or excessive payments for the acquisition, restoration of property or compensation for damage caused by the employee to third parties (Article 238 of the Labor Code of the Russian Federation).

Part 2 of Art. 277 of the Labor Code of the Russian Federation establishes that in cases provided for by federal laws, the head of an organization compensates the organization for losses caused by his guilty actions. In this case, the calculation of losses is carried out in accordance with the norms provided for by civil law.

In accordance with the requirements of civil law, losses are understood as expenses that a person whose right has been violated has made or will have to make to restore the violated right, loss or damage to his property (real damage), as well as lost income that could have been received by the person if normal conditions of civil circulation, if his right had not been violated (lost profit) (Article 15 of the Civil Code of the Russian Federation).

The financial responsibility of the chief accountant must be established in the employment contract. If the employment contract does not stipulate that in case of damage he bears financial responsibility in full, in the absence of other grounds giving the right to hold this person to such liability, he can be held liable only within the limits of his average monthly earnings (clause 10 of the resolution No. 52).