Form 5 financial statements

Current as of: December 11, 2020

We talked about the composition of financial statements for 2020 in our consultation. At the same time, it was pointed out that the approved forms of annexes to the balance sheet and the financial results statement are provided by Order of the Ministry of Finance dated July 2, 2010 No. 66n, a report on changes in capital, a cash flow report, and for non-profit organizations also a report on the intended use of funds. What is considered Form 5 (Appendix to the Balance Sheet)?

Reporting 2020

Report forms are regulated by the current Order of the Ministry of Finance No. 66n dated July 2, 2010, and include:

- The balance sheet itself.

- Reports on financial activities, cash flow, changes in the authorized capital, and the use of the targeted nature of the proceeds.

- Explanations for reporting financial results in text or table form at your discretion.

Important! The obligation to provide explanations is assigned to all organizations and enterprises engaged in business activities, with the exception of those belonging to the category of small businesses. Small businesses attach explanations to the report if desired, if necessary.

What a balance sheet is is explained simply and clearly in the following video:

Post Views: 78

Why do you need Appendix 5 to the balance sheet and who should draw it up?

The main objective of accounting reporting is to provide complete and reliable information about the company's activities to all interested users. The balance sheet form itself cannot always provide all the necessary data, since the indicators in it are presented in an aggregated form.

Consider, for example, the article “Fixed assets”. In the balance sheet this is one figure, but in fact it can hide dozens, hundreds and even thousands of different objects. The same applies to debt indicators, financial investments and some other balance sheet items. Form 5 (Appendix No. 3 to the balance sheet) is used to detail them.

All legal entities must fill it out, except for those who are granted the right to conduct simplified accounting by the Law “On Accounting” dated December 6, 2011 No. 402-FZ. We are talking about the following organizations:

- Participants of the Skolkovo project.

The list of these persons was approved by clause 4 of Art. 6 of the above law.

Application or Explanation?

Let us immediately make a reservation that the concept of “form No. 5” is not used in the currently used accounting reporting forms. This form was valid until 2011 in accordance with Order of the Ministry of Finance dated July 22, 2003 No. 67n, which has now lost force. Form No. 5 was called “Appendix to the Balance Sheet” and consisted of the following sections:

- intangible assets;

- fixed assets;

- profitable investments in material assets;

- expenses for research, development and technological work;

- expenses for the development of natural resources;

- financial investments;

- accounts receivable and accounts payable;

- expenses for ordinary activities (by cost elements);

- provision;

- government assistance.

Currently, the Appendix to the Balance Sheet is not used as an independent approved form of reporting. At the same time, Appendix No. 3 to the Order of the Ministry of Finance dated 07/02/2010 provides an example of the preparation of explanations to the balance sheet and financial performance statement, which is recommended to be used when preparing explanations in tabular form (clause 4 of the Order of the Ministry of Finance dated 07/02/2010 No. 66n) .

The composition of these explanations is in many ways the same form No. 5 that was previously used. Only if previously it was a mandatory form of reporting, now it is submitted as an explanation for reporting if the organization considers it necessary to provide this type of information. The given example of explanations to the balance sheet and profit and loss statement, relatively speaking “Form No. 5,” now contains the following sections:

- intangible assets and expenses for research, development and technological work (R&D);

- fixed assets;

- financial investments;

- stocks;

- accounts receivable and accounts payable;

- production costs;

- estimated liabilities;

- securing obligations;

- government assistance.

You can prepare explanations for the balance sheet and profit and loss statement in Excel format here.

Composition of the reporting form

The statement of changes in equity for 2020 consists of the following sections:

- 1 “Movement of capital”;

- 2 “Adjustments due to changes in accounting policies and correction of errors”;

- 3 “Net assets”.

The movement of capital in the form is presented with a breakdown by type of capital presented in Section III of the Balance Sheet:

- authorized capital

- own shares purchased from shareholders;

- Extra capital;

- Reserve capital;

- retained earnings (uncovered loss).

Section 1 provides information about the reasons for the increase or decrease for each type of capital of the organization and the amounts of such changes. Information on capital movements in the Report is provided for the previous and reporting year, as required by the general rules for preparing financial statements (clause 10 of PBU 4/99).

The second section of the Report reflects data on capital adjustments due to changes in accounting policies or correction of errors.

When filling out section 3 “Net assets” in the capital flow statement, you must be guided by the Procedure for determining the value of net assets, approved by Order of the Ministry of Finance dated August 28, 2014 No. 84n.

We talked about the relationship between the indicators of the Statement of Changes in Capital and the Balance Sheet in 2017-2018 in a separate material.

You can download the 2020 Statement of Changes in Capital form in Excel format with the “Code” column here.

Share: Subscribe to our channel in Yandex. Zen

Appendix to the balance sheet is an important element of reporting

The importance of transcripts and explanations to the balance sheet cannot be overestimated. The meager figures in accounting reports can tell the interested user little, and only in applications does this information appear in all its useful diversity.

Form 5 is one such necessary application. The balance sheet is directly related to it: each line begins with the “Explanations” column, which indicates the numbers of the corresponding sections of Form 5.

Without filling out Form 5 as an appendix to the balance sheet, accounting will not always be able to fully fulfill its main function - to provide interested users (shareholders, investors, etc.) with important information about the financial position of the organization. But the scope of transcripts presented in this application may vary.

IMPORTANT! The opportunity to independently determine the level of detail of Form 5 is given to companies maintaining simplified accounting (clause 6 of the order “On the forms of financial statements of organizations” dated 07/02/2010 No. 66n).

For information about who has the right to prepare simplified statements, read the article “Simplified accounting financial statements - KND 0710096”.

If a company maintaining simplified accounting wants to minimize the amount of information in the appendices to the reporting, one should not forget that the simplified balance sheet, together with the explanations, must comply with the general requirements for reporting.

Read more about these requirements in the material “What requirements should accounting records satisfy?”.

Still have questions? You can consult on any of them on our forum! For example, here we look at the nuances of forming a liquidation balance sheet and its annexes.

Form 4 balance sheet

A Form 4 balance sheet is the common name for the cash flow statement. It contains information about the organization's cash flows for the reporting and previous years. Cash flows are detailed in the context of current, investment and financial transactions. For each type of activity, the receipt and expenditure of funds are shown.

At the same time, current operations include operations related to the implementation of ordinary activities. For example, receipts include sales proceeds and rental payments, while payments include payments to suppliers and wages. Investment transactions are those related to the acquisition, creation or disposal of non-current assets.

As cash flows from financial transactions, flows from operations related to attracting financing on a debt or equity basis, leading to a change in the size and structure of the capital and borrowed funds of the organization (credits, borrowings, deposits, etc.) are classified.

The procedure for filling out the report is described in detail in PBU 23/2011 “Cash Flow Report” (approved by Order of the Ministry of Finance of the Russian Federation dated 02.02.2011 No. 11n).

You can also download its form on our website.

How are the balance sheet and Form 5 related?

The amount of information in the appendix to the balance sheet (Form 5) depends on which lines are filled in the balance sheet. Let's explain this with an example.

LLC "Rhapsody" has been operating for 2 years, does not fall under the criteria of a small enterprise and prepares a balance sheet and all other reports, including Form 5 - an appendix to the balance sheet. Considering the period of operation of the company, the balance sheet figures will be presented for the current and previous periods.

| Explanations | Indicator name | Code | As of 12/31/2017 | As of 12/31/2016 | As of 12/31/2015 |

| ASSETS | |||||

| Fixed assets | |||||

| Reserves | |||||

| 5.1–5.2 | Accounts receivable | ||||

| Financial investments (excluding cash equivalents) | |||||

| ODDS | Cash and cash equivalents | ||||

| BALANCE | 1 020 | ||||

| PASSIVE | |||||

| OIC | Authorized capital | ||||

| OFR, OIC | retained earnings | ||||

| 5.3–5.4 | Accounts payable | ||||

| BALANCE | 1 020 | ||||

The code indicated in the “Explanations” column is the table number in Form 5.

But Form 5 to the balance sheet does not decipher all lines that have a numerical indicator. For example, it does not explain the line “Cash and cash equivalents”, so the link for explanations is given not to Form 1, but to the cash flow statement (CFDS).

Also, the specified appendix to the balance sheet does not decipher the indicators of the authorized capital and retained earnings - their detail is contained in other reports. Thus, the size of the authorized capital and retained earnings by period is reflected in the statement of changes in capital (OIC) and in the statement of financial results (OFR) in terms of net profit.

In the example under consideration, form 5 will be filled out only for sections numbered 2, 3, 4 and 5. Let's look at the features of filling them out.

Read about the registration of ODDS and OIC in the article “Filling out forms 3, 4 and 6 of the balance sheet.”

How to fill out financial reporting forms correctly

Currently, there are several forms of accounting reporting.

Form No. 1 is a balance sheet, that is, a way of summarizing the current assets of the economy and the sources of their formation. It is worth noting that it is the balance sheet that allows you to most accurately characterize the financial position as of a certain date. The main thing is that Form No. 1 of the financial statements must reflect data on material assets, the size of the company, the state of payments, and the company’s investments. When filling out this reporting form, as a rule, there are no difficulties: to do this, specialists must fill out two main parts - about assets and liabilities. The balance sheet asset consists of two parts – non-current and current assets. The balance sheet liability consists of three sections - short-term liabilities, capital and reserves, long-term liabilities. Another important accounting document is Form No. 2, that is, the company’s profit and loss statement, which allows you to accurately characterize the financial results of the organization’s activities for a specific time period. In order to calculate these indicators, it is enough to analyze the total expenses and income of the enterprise. To avoid mistakes, remember: in Form No. 2 of the financial statements you must indicate: - revenue from the sale of goods, services, works, products; — income from participation in other enterprises; - extraordinary income; — interest receivable; — other operating income.

When preparing financial statements in Form 2, you must adhere to the requirements of PBU 9/99 “Income of the organization.” It is also worth taking into account that when reflecting certain types of income in the profit and loss statement, each of which can constitute five or even more percent of the total income, it must reflect the part corresponding to each type of expense. Accounting statements in Form No. 3 are a report on changes in capital. In order to draw up these reports correctly, it is necessary to adhere to the provisions given in the letter of the Ministry of Finance of the Russian Federation, published on December 23, 1992 N 117 “On the reflection in accounting and reporting of transactions related to the privatization of enterprises.” If such information is not reflected in the balance sheet, it should be provided as a transcript to the article “Authorized (share) capital” in Form No. 3. In this report, it is necessary to indicate item-by-item information about the organization’s capital, not only about its receipt and use, but also about the presence of its balances. Another accounting document is Form No. 4, that is, the cash flow statement. The accountant must reflect here information about cash flows, that is, about their receipt and direction, taking into account balances at the end and beginning of a specific reporting period. When preparing financial statements in Form 4, it is worth taking into account the following data: the activity of an organization that pursues making a profit as its main goal can be considered current. Form No. 5 is an appendix to the balance sheet. The form must be filled out in accordance with the requirements of Order of the Ministry of Finance of the Russian Federation dated January 13, 2000 N 4n “On forms of financial statements of organizations.”

Features of filling out an appendix to the balance sheet

In the example under consideration, the first line of the balance sheet is devoted to fixed assets, and the 2nd section of Form 5 explains it. The link to the table of clause 2.1 of Form 5 indicates that the company provides additional information only to the balance sheet indicators about fixed assets, the remaining assets are from this section (income investments and other current assets) she does not have.

Table 2.1 of Form 5 shows the initial cost and depreciation of fixed assets at the end and beginning of the period, taking into account all receipts and disposals, as well as the result of revaluation (if it is carried out).

IMPORTANT! If the company has undergone a revaluation, in the column “Initial cost” you need to indicate the current market value (note 3 to Appendix No. 3 of Order No. 66n dated 07/02/2010).

Table 3.1 refers to the 3rd section of Form 5 and explains information on financial investments (lines 1170 and 1240 of the balance sheet): their initial cost, taking into account receipts and disposals, accrued interest. Information is reflected by breakdown into long-term and short-term types of assets.

If financial investments are pledged or pledged to third parties (except for sale) or are used in any other way, the table in clause 3.2 “Other use of financial investments” is completed.

A similar approach to filling out Section 4 “Inventories”: information on the availability and movement of inventories (including reserves) is entered into the table of clause 4.1 of Form 5, and if there are unpaid stocks and stocks as collateral - in the table of clause 4.2.

Section 5 is devoted to deciphering accounts receivable (including the provision for doubtful debts) and accounts payable.

Results

Form 5 (appendix to the balance sheet) details the balance sheet and allows users to provide the necessary information about individual types of assets and liabilities in a clear and accessible form. Not all of the tables included in it can be used, but only those that are necessary to disclose the figures shown in the balance sheet.

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

An important and additional appendix to the balance sheet is Form No. 5, which details the sections of the balance sheet. This type of documentation is clarifying in nature. Previously, they tried to cancel this document, but then they returned it because there was confusion in the data.

Form 5 of financial statements and its sample

Explanations to the balance sheet and financial results statement - this is form No. 5 and its purpose is to detail the reflected indicators and enter clarifying information.

The official Form No. 5 can be downloaded here.

An up-to-date example of filling out the Explanations to the Balance Sheet and the Statement of Financial Results can be downloaded here in pdf format.

The following entities may not fill out Form No. 5 of the financial statements:

- small business, the audit of which cannot but be carried out;

- non-profit organizations;

- public organizations that are not engaged in commercial activities.

Thus, you can see a clearer picture of the state of finances of a particular organization, since all data in the explanations is divided into types and groups according to financial affiliation.

Why do you need form No. 5?

It is assumed that an enterprise may have many different data that require reflection in accounting with explanations. This requires a separate documentation format to allow this to happen. An appendix to the balance sheet made it possible to provide explanations for reporting losses and profits. The feasibility of filling it out was decided on an individual basis, since individual companies or institutions simply have nothing to add to the application, that is, there was no need to fill it out. Organizations submitting reports under the simplified taxation regime, if necessary, use Appendix No. 5, Order No. 66n of the balance sheet and reporting of losses and profits of small businesses. Such an application is submitted only if there is relevant data that needs to be detailed, without which it is impossible to make an objective assessment of the financial condition of the organization.

Form No. 5 details the organization’s balance sheet indicators with a breakdown into groups and individual types. All main indicators are combined into the following groups of sections:

- assets classified as intangible;

- fixed assets taking into account depreciation;

- investments in material assets;

- expenses spent on research and development activities;

- expenses associated with the development of natural resources;

- investments in securities, authorized capital of other organizations, bonds, etc.;

- debt (payable and receivable);

- expenses associated with ordinary activities;

- types of security;

- government subsidies.

The photo shows a sample of the first page of this application:

The form also contains free lines where you can enter additional information to be reflected in one or another section of the document.

Important! Information included as explanations in the Appendix to the balance sheet must completely duplicate what is stated in the main report.

Appendix 5 to the balance sheet: structure and filling procedure

Let's take a closer look at the groups into which financial indicators are divided.

Section on intangible assets

The section “Intangible assets” is clarifying information on the balance sheet, recorded in line 110. Intangible assets are registered at their original cost. The data is reflected according to the principle:

Cost of intangible assets at the beginning of the reporting period + receipt - disposal = cost of intangible assets at the end of the reporting period

In Form 5, amounts reflecting retired intangible assets are written with parentheses. This block also describes the amounts for depreciation of intangible assets at the beginning and end of the reporting year. There are also lines for types of intangible assets:

Section "Fixed assets"

This section details all information relating to the movement of fixed assets and their availability, and deciphers line 120 of the balance sheet. The data presented in analytical accounting for accounts 01 and 02, where fixed assets and their depreciation are registered, are needed to reflect the indicators of this block. Indicators for fixed assets are filled in at cost, called initial or replacement.

The tables also reflect changes in the indicated value of fixed assets that were reconstructed, completed or liquidated. Figures for retired OS are written with parentheses. OS taking into account depreciation is also deciphered in a separate table in this section:

Section on financial investment amounts

This section details the amounts on lines 140 and 250 of Form No. 1. Indicators for investments of short-term and long-term funds are reflected here, their types are described and separated into groups. Also subject to submission are financial investments that have the status of “pledged” and for which there has been a transfer to other persons:

Conventionally, the following groups of financial investments can be distinguished:

- investing in funds that form the authorized capitals of other organizations;

- state and municipal securities;

- securities of other enterprises, which also includes debt securities (bonds, bills);

- loans issued;

- deposits and others.

Section “Securing Obligations”

This section details information regarding the information specified in the Certificate of Availability of Valuables that is presented on off-balance sheet accounts. Separately indicate information on collateral that was issued and received at the beginning and end of the reporting year:

Section "Production costs"

This block clarifies information on costs and expenses associated with the production process, as well as any changes in balances relating to work in progress, deferred costs and deferred inventories.

General information about the enterprise is indicated, but turnover within the enterprise is not taken into account. It may include expenses related to the transfer of goods, products or work and services that relate to the enterprise’s own goals:

Section "State aid"

This section applies to enterprises that received government assistance during the reporting period. These include subventions, subsidies, government loans, as well as other assets of the enterprise - land plots, natural resources, other real estate:

Debt section

This section provides clarification of lines 230 and 240 of the asset and lines 510, 520, 610, 620, 630 and 660 of the liability of the balance sheet, which include the amounts of the enterprise's debt to creditors and debt of debtors. All debt figures that have short-term and long-term status are recorded. They are divided by type at the beginning and end of the reporting year:

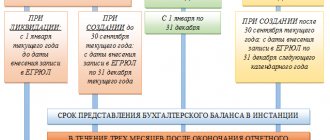

In accordance with Art. 14 of Law 402-FZ, the accounting (financial) statements include a balance sheet, a statement of financial results, or a report on the intended use of funds (instead of a statement of financial results), appendices to them, including a statement of changes in capital and a cash flow statement , report on the intended use of funds, explanations, audit report (for organizations subject to mandatory audit).

Fig. No. 3. Forms of financial statements

The balance sheet (form No. 1) is a method of grouping and generalized reflection in monetary terms of the economic assets of an enterprise by composition and location, as well as by the sources of their formation as of a certain date. Graphically, the balance sheet is a table that is divided vertically into two parts to separately reflect the types of funds and their sources. The left side of the table shows funds by composition and placement, and the right side shows the sources of their formation. The left side is called the asset, the right side is called the liability. Each separate type of funds in an asset and their sources in a liability is called a “balance sheet item.” The totals of the amounts of assets and liabilities of the balance sheet are always equal to each other, since they reflect the same funds.

The rules for evaluating balance sheet items are established by the regulations on accounting, financial statements and instructions (directives) for the preparation of financial statements.

The profit and loss report (form No. 2) contains in its sections information for the reporting and previous periods:

— about profits (losses) from the sale of goods, products, works and services;

— on operating income and expenses, highlighting interest receivable and payable;

— on non-operating income and expenses and net (undistributed) profit (loss) of the reporting period.

For reference, the report provides data for the reporting and previous periods on dividends per preferred and ordinary share. The breakdown of individual profits and losses provides data for the reporting and previous periods on individual types of profits and losses.

The statement of changes in capital (form No. 3) consists of four sections and a certificate.

Section I “Capital” shows the balance at the beginning of the year, receipts, expenses and the balance at the end of the year of the components of equity capital.

Section II “Reserves for future expenses” and Section III “Evaluated reserves” show the balances at the beginning and end of the reporting period, and the movement of reserves for future expenses and estimated reserves available in the organization.

Section IV “Changes in capital” contains information for the reporting and previous periods on the amount of capital at the beginning of the period, its increase, decrease and the amount of capital at the end of the reporting period.

The “Certificate” indicates data on net assets at the beginning of the end of the reporting year and on funds received from the budget and extra-budgetary funds, not expenses for ordinary activities and expenses for capital investments in non-current assets.

Since 1996, organizations have been preparing a cash flow statement (Form No. 4). The report consists of four sections:

— Cash balance at the beginning of the year.

— Funds received – total and including by type of income

— Funds sent – in total, including by expense areas

— Cash balance at the end of the reporting period. Information on cash flows is presented in the currency of the Russian Federation, rubles - according to accounts 50 “Cash”, 51 “Current account”, 52 “Currency account”, 55 “Special accounts in banks”. Cash flow is shown by type of activity - current, investment, financial.

The appendix to the balance sheet (form No. 5) consists of seven sections.

Section 1 “Movement of borrowed funds” shows balances at the beginning and end of the reporting period, debts received and repaid, short-term loans and loans with the allocation of those not repaid on time.

Section 2 “Receivables and payables” contains data on balances and movements for the year on short-term and long-term receivables, highlighting overdue and separately those lasting more than three months, as well as data on received and issued collateral.

Section 3 “Depreciable property” reflects the balances at the beginning of the reporting year and data on receipts and disposals for each type of intangible assets and fixed assets and property for leasing and presented under a rental agreement.

Section 4 “Movement of funds for financing long-term investments and financial investments” contains information about the organization’s own funds and attracted funds by type. At the end of the section, information about unfinished construction and investments in subsidiaries and dependent companies is provided for reference.

Section 5 “Financial Investments” indicates the amount of balances at the beginning and end of the reporting year for each type of long-term and short-term financial investments.

Section 6 “Expenses for ordinary activities” reflects costs by element for the reporting and previous years and data on changes in work in progress balances, deferred expenses and reserves for future expenses.

Section 7 “Social Indicators” provides data on contributions to state extra-budgetary funds and contributions to non-state pension funds.

The report on the intended use of funds received (Form No. 6) contains data for the reporting and previous years on the balance of funds at the beginning of the year, receipt of funds by type, use of funds by type and the balance of funds at the end of the year.

The explanatory note to the annual financial statements must contain essential information about the organization, its financial position, comparability of data for the reporting and preceding years, valuation methods and significant items of the financial statements.

Filling out Form No. 5 Explanation of the Balance Sheet and Profit and Loss Statement

Task 1. Based on the balance sheets, fill out form No. 5 Explanations to the Balance Sheet and Profit and Loss Statement for 2012:

Initial data: during 2012 in the organization

— patent for invention sold;

— acquired the exclusive right to the software;

— the loss from the impairment of production secrets (know-how), recognized in 2011, was restored in full.

The secret of production (know-how) is not depreciated, since it has an indefinite useful life.

The organization does not overvalue intangible assets.

Turnover - balance sheet for account 04, analytical accounting by types of intangible assets, for 2012 (rub.)

| Intangible assets by type | Balance at the beginning of the period | Turnover for the period | balance at the end of period | ||

| Debit | Credit | Debit | Credit | Debit | Credit |

| Patents for inventions | 950 000 | 950 000 | |||

| Computer programs | 1 140 000 | 1 032 000 | 2 172 000 | ||

| Secrets of production (know-how) | 748 000 | 748 000 | |||

| Total | 2 838 000 | 1 032 000 | 950 000 | 2 920 000 |

Balance sheet for account 05, analytical accounts of depreciation by type of intangible assets, for 2012 (rubles)

| Intangible assets by type | Balance at the beginning of the period | Turnover for the period | balance at the end of period | ||

| Debit | Credit | Debit | Credit | Debit | Credit |

| Patents for inventions | 260 000 | 290 000 | 30 000 | ||

| Computer programs | 640 000 | 274 000 | 914 000 | ||

| Total | 900 000 | 290 000 | 304 000 | 914 000 |

Balance sheet for account 05, analytical accounts for accounting for impairment by types of intangible assets, for 2012 (rubles)

| Intangible assets by type | Balance at the beginning of the period | Turnover for the period | balance at the end of period | ||

| Debit | Credit | Debit | Credit | Debit | Credit |

| Secrets of production (know-how) | 300 000 | 300 000 | |||

| Total | 300 000 | 300 000 |

Fragment of Form 5 Explanations to the Balance Sheet and Profit and Loss Statement for 2011:

Form 5. Explanation of the Balance Sheet and Financial Results Report for 2012

Section 1. Intangible assets and expenses for research, development and technological work (R&D)

1.1. Availability and movement of intangible assets

Task 2. Based on the initial data, fill out section 5 Accounts receivable and payable of form No. 5 Explanations to the Balance Sheet and Profit and Loss Statement for 2012:

Initial data: during 2012, the organization knows the following accounting data for settlement accounts in terms of short-term receivables (rub.)

| Index | As of 12/31/2012 |

| 1. Debit balance of account 62 | 4 456 000 |

| 2. Account debit balance 60 | 236 000 |

| 3. Account debit balance 70 | 28 200 |

| 4. Debit balance of account 71 | 14 000 |

| 5. Debit balance of account 73 | 101 000 |

| 6. Account debit balance 76 | 1 180 000 |

| 7. Account credit balance 63 | 300 000 |

The following transactions occurred in 2012:

1. Settlements with suppliers and contractors:

Suppliers' debts were transferred from long-term to short-term - RUB 800,000.

The debt of suppliers and contractors was repaid - RUB 879,000.

2. Settlements with buyers and customers:

Transferred customer debt from long-term to short-term—RUB 500,000.

The debt of buyers and customers for shipped products, goods, works, services is reflected - RUB 3,706,000.

The debt of buyers and customers is reflected in the form of sanctions for violation of the terms of contracts - 250,000 rubles.

The debt of buyers and customers was repaid - 1,000,000 rubles.

The debt was written off using reserve funds - RUB 100,000.

The debt was written off for the financial result - 100,000 rubles.

A reserve for doubtful debts has been created - 250,000 rubles.

3. Settlements with employees of the organization (wages):

The amount of advances paid to employees is included in labor costs - RUB 35,000.

Advances were paid to employees - RUB 28,200.

4. Settlements with accountable persons:

Issued on account - 14,000 rubles.

Accepted advance reports from accountable persons - 10,000 rubles.

5. Settlements with employees of the organization for other operations (compensation for damage, interest-free loans, etc.):

The debt of employees for other operations is reflected - 101,000 rubles.

The employees repaid the debt on other transactions - 159,000 rubles.

6. Settlements with various debtors (counterparties under intermediary agreements, lease agreements, etc.):

The debt of debtors is reflected - 1,080,000 rubles.

The debt of debtors was repaid - RUB 3,540,000.

A reserve for doubtful debt has been created - 50,000 rubles.

Less receivables generated and repaid (written off) in one reporting period.

Fragment of the Explanations to the Balance Sheet and Profit and Loss Statement for 2011:

Form 5. Explanation of the Balance Sheet and Financial Results Report for 2012

Section 5 Accounts receivable and payable

5.1 Availability and movement of receivables

Task 3. Based on the initial data, fill out section 2 Fixed assets of form No. 5 Explanations to the Balance Sheet and Profit and Loss Statement for 2012:

Initial data: during 2012, the organization knows the following data:

— equipment worth RUB 560,000 was purchased;

— a passenger car worth 300,000 rubles was purchased;

— the truck was retrofitted (the original cost increased by 50,000 rubles);

— equipment sold with an original cost of RUB 1,289,697. with accumulated depreciation RUB 304,000;

— vehicles were sold with an original cost of RUB 677,723. with accumulated depreciation 37,000 rubles;

— office equipment with an original cost of 30,000 rubles was sold. with accumulated depreciation of 2000 rubles;

— at the end of 2012, fixed assets were revalued. As a result, the replacement cost of the building was increased by 140,000 rubles, and depreciation by 20,000 rubles.

Balance sheet for account 01, subaccount “Assets in operation”, analytical accounting by asset groups, for 2012:

| OS groups | Balance at the beginning of the period | Turnover for the period | balance at the end of period | ||

| Debit | Credit | Debit | Credit | Debit | Credit |

| Building | 5 180 000 | 140 000 | 5 320 000 | ||

| Machines, equipment | 6 510 657 | 560 000 | 1 288 697 | 5 781 960 | |

| Vehicles | 1 264 763 | 350 000 | 677 723 | 937 040 | |

| Office equipment | 350 000 | 30 000 | 320 000 | ||

| Total | 13 305 420 | 1 050 000 | 1 996 420 | 12 359 000 |

Balance sheet for account 03, analytical accounting by asset groups, for 2012:

| OS groups | Balance at the beginning of the period | Turnover for the period | balance at the end of period | ||

| Debit | Credit | Debit | Credit | Debit | Credit |

| Machines, equipment | 3 200 000 | 3 200 000 | |||

| Total | 3 200 000 | 3 200 000 |

Balance sheet for account 02, subaccounts “Depreciation of fixed assets” and “Depreciation of income-generating investments in material assets”, analytical accounting by groups of fixed assets, for 2012:

| OS groups | Balance at the beginning of the period | Turnover for the period | balance at the end of period | ||

| Debit | Credit | Debit | Credit | Debit | Credit |

| Subaccount “Depreciation of fixed assets” | |||||

| Building | 777 000 | 125 000 | 902 000 | ||

| Machines, equipment | 483 970 | 304 270 | 270 300 | 450 000 | |

| Vehicles | 92 873 | 37 000 | 83 926 | 139 799 | |

| Office equipment | 46 437 | 2 000 | 25 462 | 69 899 | |

| Total | 1 400 280 | 343 270 | 504 688 | 1 561 698 | |

| Subaccount “Depreciation of profitable investments in material assets” | |||||

| Machines, equipment | 872 727 | 290 904 | 1 163 631 | ||

| Total | 872 727 | 290 904 | 1 163 631 |

Fragment of Form No. 5 Explanations to the Balance Sheet and Profit and Loss Statement for 2011:

Form 5. Explanation of the Balance Sheet and Financial Results Report for 2012

Section 2. Fixed assets

2.1 Availability and movement of fixed assets

Paper format, sizes A0, A1, A2, A3, A4, A5, A6

If you offer a printing house to print a non-format product, you will most likely have to overpay for paper that will end up in the trash, or, at best, recycled. This mainly applies to papers intended for digital and offset printing. But, for example, designer cardboards and papers in most cases have a size of 700x1000 mm (approximately B1 format 707x1000mm). When printing on such papers, you need to be more careful about the size of the product, since the cost of such materials is orders of magnitude higher. I will try to describe as briefly but informatively as possible the format of the A series printed sheet, as one of the main ones in the world. Understanding the difference in sizes, it will be much easier for you to communicate with printing house managers.

Paper size table (dimensions in mm), ISO 216 standard

| A6 – 105x148 | A2 – 420x594 |

| A5 – 148x210 | A1 – 594x841 |

| A4 – 210x297 | A0 – 841x1189 |

| A3 – 297x420 |

Paper size chart (dimensions in cm)

| A6 – 10.5x14.8 | A2 – 42x59.4 |

| A5 – 14.8x21 | A1 – 59.4x84.1 |

| A4 – 21x29.7 | A0 – 84.1x118.9 |

| A3 – 29.7x42 |