Calculation

The service guarantees confidentiality and protection of personal data. Only numbers are used for calculations - no personal data needs to be entered.

For individual entrepreneurs throughout Russia, insurance premiums are calculated the same way - according to the federal minimum wage. There are no benefits.

The cost of an insurance year for individual entrepreneurs is determined based on the rate of 26% (Article 425 of the Tax Code of the Russian Federation), and not at the rates for hired employees (22%)

Online accounting in which you can calculate individual entrepreneur payments and other taxes and send reports via the Internet. (advertising)

Result..Total you need to pay:

| You chose 2020: The age of the individual entrepreneur since 2014 does not matter. Contribution for the full year - 2020 (minimum wage does not matter). The fixed payment to the pension fund in 2020 for individual entrepreneurs amounted to ( a total of 12 full months ): for the insurance part of the pension: = Since 2014, the Pension Fund of Russia has been paying only the insurance portion in one payment (regardless of age). Also, since 2014, when accumulating income exceeding 300,000 (since the beginning of the year), the individual entrepreneur pays 1% to the Pension Fund of the Russian Federation on the amount of income exceeding 300,000 rubles (per year)... That is. if the income is 400,000 rubles. then you need to pay 400,000 -300,000 rubles = 100,000 *1% = 1000 rubles. |

Opening a personal account

To access the online tax payment function through the official website of the Federal Tax Service, you need to register on it. The whole procedure boils down to creating a taxpayer’s personal account. This can be done in two ways: using a login-password combination or an electronic digital signature (EDS).

The first parameter is the individual taxpayer number indicated in the certificate of registration with the Federal Tax Service (TIN), the password is displayed in the entrepreneur’s registration card. The second combination of numbers is extremely difficult to remember, because it is an automatically generated machine code. Therefore, if possible, it is better to immediately replace it with lighter encryption (not forgetting about security).

We recommend you study! Follow the link:

How to generate a receipt for the Pension Fund for individual entrepreneurs and what details to use to pay insurance premiums

The sequence of actions on how to pay taxes for individual entrepreneurs via the Internet using a login and password comes down to the algorithm:

- contact any branch of the Federal Tax Service;

- present identification;

- receive a registration card;

- register a taxpayer’s personal account on the website, indicating the required login and password;

- remit payment.

The registration process is greatly facilitated by an electronic digital signature, which is a person’s real signature, but translated into the appropriate format. Its creation will cost the business owner approximately 3,000 rubles.

But through it you can easily perform a number of operations over the network:

- pay taxes and fees for individual entrepreneurs;

- submit financial statements;

- participate in tenders and trades;

- optimize document flow in the organization by transferring part of the exchange of information into electronic format;

- file complaints and other actions, which in most cases take a fair amount of time.

To obtain an electronic signature, you will need the owner’s passport, INN, SNILS, and individual entrepreneur registration number (OGRN). They must be submitted to the Certification Center, which issues electronic keys.

https://youtu.be/aYcu3DH_ihA

Reducing individual entrepreneur taxes on contributions

| Tax regime | Entrepreneurs working without hired staff | Entrepreneurs working with hired personnel | Base |

| USN (object of taxation “income”) | The single tax can be reduced by the entire amount of insurance premiums paid in a fixed amount | The single tax can be reduced by no more than 50 percent. Contributions paid by the entrepreneur for hired employees and for his own insurance are accepted for deduction. | subp. 1 clause 3.1 art. 346.21 Tax Code of the Russian Federation |

| Payment for the year can be used: for 1 quarter - no more than 1/4, for half a year - no more than 1/2, for 9 months - no more than 3/4 of the annual amount of contributions, for a year - the entire amount of insurance premiums of an individual entrepreneur. See the simplified tax system + declaration calculator. Many people find it difficult to calculate the simplified tax system together with the Pension Fund deduction and divide it by quarter. Use this automated simplification form in Excel (xls). The form is already ready for 2020 with an additional insurance premium for individual entrepreneurs. | |||

| USN (object of taxation “income minus expenses”) | You can reduce your income by the entire amount of insurance premiums paid. | clause 4 art. 346.21 et sub. 7 clause 1 art. 346.16 Tax Code of the Russian Federation | |

| UTII | The single tax can be reduced by the entire amount of insurance premiums paid in a fixed amount | You can reduce UTII by no more than 50 percent. Contributions paid by the entrepreneur for hired employees, benefits and for his own insurance are accepted for deduction (from the age of 13 to 17, you could not reduce your contributions for employees) | subp. 1 item 2 art. 346.32 Tax Code of the Russian Federation |

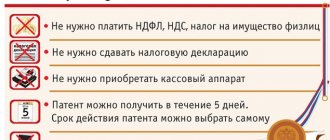

| Patent | The cost of the patent does not decrease | Art. 346.48 and 346.50 Tax Code of the Russian Federation | |

| BASIC | Individual entrepreneurs on OSNO have the right to include a fixed payment in personal income tax expenses | NK Art. 221 | |

2018, 2020 and 2020

In 2020 RUB 32,385 (+15.7%)

In 2020 RUB 36,238 (+11.9%)

In 2020 RUB 40,874 (+12.8%)

The amount of insurance premiums is now directly stated in the tax code. And even 3 years in advance - for 2018-2020.

Article 430 of the Tax Code of the Russian Federation (as amended by Federal Law dated November 27, 2017 N 335-FZ):

a) paragraph 1 should be stated as follows:

"1. Payers specified in subparagraph 2 of paragraph 1 of Article 419 of this Code pay:

1) insurance contributions for compulsory pension insurance in the amount determined in the following order, unless otherwise provided by this article:

if the payer’s income for the billing period does not exceed 300,000 rubles - in a fixed amount of 26,545 rubles for the billing period of 2020, 29,354 rubles for the billing period of 2020, 32,448 rubles for the billing period of 2020;

if the payer’s income for the billing period exceeds 300,000 rubles - in a fixed amount of 26,545 rubles for the billing period of 2020 (29,354 rubles for the billing period of 2019, 32,448 rubles for the billing period of 2020) plus 1.0 percent of the payer’s income exceeding 300,000 rubles for the billing period.

In this case, the amount of insurance contributions for compulsory pension insurance for the billing period cannot be more than eight times the fixed amount of insurance contributions for compulsory pension insurance established by paragraph two of this subclause;

2) insurance premiums for compulsory medical insurance in a fixed amount of 5,840 rubles for the billing period of 2020, 6,884 rubles for the billing period of 2020 and 8,426 rubles for the billing period of 2020.”;

How to calculate the extra 1%

To calculate the additional 1%, you need to determine your income depending on the applicable tax system.

For the simplified tax system, this is all income received during the year (column 4 of section I of the book of accounting for income and expenses). Expenses are not taken into account, even if you apply the simplified tax system for income minus expenses.

For UTII, this is the total imputed income for the year (the sum of the values on line 100 of section 2 of the UTII declaration for each quarter).

For the patent system, this is the potentially receivable income indicated in the patent (line 010). If the patent is issued for a period of less than 12 months, then the income must be divided by 12 and multiplied by the number of months for which the patent was issued (line 020).

If you combine several tax regimes, then the income from each of them is summed up.

The calculation of individual entrepreneur contributions differs depending on whether he pays them for himself or for his employees.

In 2020, insurance premiums are fixed amounts and depend on the income that the individual entrepreneur received for the year (Article 430 of the Tax Code of the Russian Federation):

- The insurance premium for health insurance in 2020 is a fixed amount of 5,840 rubles.

- The pension insurance contribution in 2020 is 26,545 rubles. An additional contribution of 1% is transferred if the individual entrepreneur’s income from the beginning of the year exceeds 300,000 rubles. Individual entrepreneurs' insurance premiums payable in excess of the established amount can be calculated by multiplying the amount of income from the beginning of the year, reduced by 300,000 rubles, by 1%.

Insurance premiums are calculated from the income of individual entrepreneurs minus the non-taxable amounts listed in Art. 422 of the Tax Code of the Russian Federation. The amount of insurance premiums for individual entrepreneurs paying them for employees is generally determined by the following rates (Article 426 of the Tax Code of the Russian Federation):

- Pension insurance – 22%. From the amount of taxable payments to an employee exceeding 1,021,000 rubles – 10%.

- Contributions for compulsory health insurance – 5.1%. The maximum base for contributions to compulsory medical insurance has not been established.

- Insurance premiums for temporary disability and maternity – 2.9%. If payments to an employee exceed 815 thousand rubles, this contribution is not paid.

- Contributions for “injury” are paid at rates assigned depending on the class of professional insurance (Article 21 of Law No. 125-FZ of July 24, 1998).

If there are grounds, reduced and additional rates of insurance premiums may be applied (Articles 427, 428 of the Tax Code of the Russian Federation).

MORE: Account 69 - accounting entries using the example of 2020 || Insurance premiums accrued for wages posting

Additional percentage

If you are on OSNO or simplified tax system, then you pay an additional percentage on your income. If you are on PSN or UTII, be sure to read the table below (then it is not paid from real income).

In 2020, the contribution will be: 40,874 rubles (pay by December 25). With an income of 300,000 rubles (cumulative total for the year), you will need to pay additionally plus 1% (pay before July 1) of the difference (total income - 300,000 rubles), but no more than based on 8 minimum wages (for the Pension Fund of Russia ). Those. the maximum payment will be: 8 * 32,448 = 259,584 rubles (in 2020).

In 2020, the contribution will be: 36,238 rubles (pay by December 25). With an income of 300,000 rubles (cumulative total for the year), you will need to pay additionally plus 1% (pay before July 1) of the difference (total income - 300,000 rubles), but no more than based on 8 minimum wages (for the Pension Fund of Russia ). Those. the maximum payment will be: 8 * 29,354 = 234,832 rubles (in 2019).

In 2020, the contribution will be: 32,385 rubles (pay by December 25). With an income of 300,000 rubles (cumulative total for the year), you will need to pay additionally plus 1% (pay before July 1) of the difference (total income - 300,000 rubles), but no more than based on 8 minimum wages (for the Pension Fund of Russia ). Those. the maximum payment will be: 8 * 26,545 = 212,360 rubles (in 2018).

In 2020, the contribution will be: 7,500 rubles * 12 * (26% (PFR) + 5.1% (MHIF)) = 27,990 rubles (pay by December 25). With an income of 300,000 rubles (cumulative total for the year), you will need to pay additionally plus 1% (pay before July 1) of the difference (total income - 300,000 rubles), but no more than based on 8 minimum wages (for the Pension Fund of Russia ). Those. the maximum payment will be: 8 * minimum wage * 12 * 26% = 187,200 rubles (in 2017).

Those who are late with reporting (to the tax office) also had to pay contributions to the Pension Fund based on 8 minimum wages (until 2020). Since 2020, this norm has been abolished (letter of the Federal Tax Service of Russia dated September 13, 2017 No. BS-4-11 / [email protected] ). And in July 2020, they even announced an “amnesty” for those who were late with reporting for 2014-2016, the maximum fine will be removed (see statement) (PFR letter dated July 10, 2020 No. NP-30-26/9994).

For an additional 1% in the Pension Fund (it goes only to the insurance part, the FFOMS does not need it): there are 2 options under the simplified tax system “Income” 1) Transfer 1% before December 31, 2020 and reduce the simplified tax system tax for 2018 (See Letter Ministry of Finance dated February 21, 2014 N 03-11-11/7511) 2) Transfer 1% in the period from January 1 to July 1, 2020 and reduce the simplified tax system tax for 2020 (See Letter of the Ministry of Finance dated January 23, 2017 No. 03-11-11/3029)

You don’t have to read the dispute below, because... The Ministry of Finance issued Letter of the Ministry of Finance of Russia No. 03-11-09/71357 dated December 7, 2015, in which it recalled the letter of the Ministry of Finance of Russia dated October 6, 2015 No. 03-11-09/57011. And now at all levels they believe that it is POSSIBLE to reduce the simplified tax system by this 1%.

Shocking news: the letter of the Ministry of Finance of Russia dated October 6, 2015 No. 03-11-09/57011 states that this 1% is not a fixed contribution at all and the simplified tax system for individual entrepreneurs has no right to reduce the tax on it. Let me remind you that the position of the Ministry of Finance (especially such a windy one) is not a legislative act. Let's look at future judicial practices. There is also a letter from the Federal Tax Service of Russia dated January 16, 2020 No. GD-4-3/330, which expresses the position that it is possible to reduce this 1%.

In 212-FZ article 14 clause 1. It is directly stated that this 1% is a contribution in a fixed amount, the position of the Ministry of Finance, expressed in the letter of the Ministry of Finance of Russia dated October 6, 2015 No. 03-11-09/57011, contradicts this law:

1. Payers of insurance contributions specified in paragraph 2 of part 1 of article 5 of this Federal Law pay the corresponding insurance contributions to the Pension Fund of the Russian Federation and the Federal Compulsory Medical Insurance Fund in fixed amounts, determined in accordance with parts 1.1 and 1.2 of this article.

1.1. The amount of the insurance contribution for compulsory pension insurance is determined in the following order, unless otherwise provided by this article:

1) if the income of the payer of insurance premiums for the billing period does not exceed 300,000 rubles - in a fixed amount, defined as the product of the minimum wage established by federal law at the beginning of the financial year for which insurance premiums are paid, and the insurance tariff contributions to the Pension Fund of the Russian Federation established by clause 1 of part 2 of article 12 of this Federal Law, increased by 12 times;

2) if the income of the payer of insurance premiums for the billing period exceeds 300,000 rubles - in a fixed amount, defined as the product of the minimum wage established by federal law at the beginning of the financial year for which insurance premiums are paid, and the tariff of insurance premiums to the Pension Fund of the Russian Federation, established by paragraph 1 of part 2 of Article 12 of this Federal Law, increased by 12 times, plus 1.0 percent of the amount of income of the payer of insurance contributions exceeding 300,000 rubles for the billing period. In this case, the amount of insurance premiums cannot be more than the amount determined as the product of eight times the minimum wage established by federal law at the beginning of the financial year for which insurance premiums are paid, and the rate of insurance contributions to the Pension Fund of the Russian Federation established by paragraph 1 of part 2 of the article 12 of this Federal Law, increased by 12 times.

I also draw your attention to:

Article 75. Penalty

8. Penalties are not charged on the amount of arrears that a taxpayer (fee payer, tax agent) has incurred as a result of his compliance with written explanations on the procedure for calculating, paying a tax (fee) or on other issues of application of the legislation on taxes and fees given to him or an unspecified circle of persons by a financial, tax or other authorized government body (an authorized official of this body) within its competence (these circumstances are established in the presence of a corresponding document of this body, in the meaning and content related to the tax (reporting) periods for which the arrears arose, regardless of the date of publication of such a document), and (or) as a result of the taxpayer (payer of the fee, tax agent) fulfilling the motivated opinion of the tax authority sent to him during tax monitoring.

Article 111. Circumstances excluding a person’s guilt in committing a tax offense

3) execution by the taxpayer (fee payer, tax agent) of written explanations on the procedure for calculating, paying a tax (fee) or on other issues of applying the legislation on taxes and fees given to him or an indefinite number of persons by a financial, tax or other authorized government body (authorized an official of this body) within his competence (these circumstances are established in the presence of a corresponding document of this body, in the meaning and content related to the tax periods in which the tax offense was committed, regardless of the date of publication of such a document), and (or) the taxpayer’s fulfillment ( payer of the fee, tax agent) a reasoned opinion of the tax authority sent to him during tax monitoring.

You can refer to three such clarifications. They are taller.

With UTII, this 1% can be paid until the end of the quarter and then reduced UTII.

This 1% does not apply to the fixed part and the law does not say that it (or these 300,000) must be reduced proportionally (Article 430 clause 1 clause 1). Those. even if the individual entrepreneur did not register at the beginning of the year, the deduction is still 300,000 rubles.

Table by which the additional 1% is calculated (under different tax regimes)

| Tax regime | Income | Where is the income registered? |

| Reason: Part 8 of Article 14 of the Federal Law of July 24, 2009 No. 212-FZ as amended by the Federal Law of July 23, 2013 No. 237-FZ. If you use two or three systems (for example, simplified tax system + UTII), then the income from these systems must be taken in total for all systems. | ||

| BASIC (income from business activities) | Income subject to personal income tax. Calculated in accordance with Article 227 of the Tax Code of the Russian Federation However, costs can be taken into account on the basis of this Constitutional Court ruling. Also, when calculating income for calculating 1%, you can take into account professional tax deductions (Letter of the Ministry of Finance of Russia dated May 26, 2017 N 03-15-05/32399) | Declaration 3-NDFL; clause 3.1. Sheet B. In this case, expenses are not taken into account. See return application Line 060 of the 3-NDFL declaration |

| USNO | Income subject to the Single Tax. Calculated in accordance with Article 346.15 of the Tax Code of the Russian Federation For the simplified tax system, income is page 113 of the simplified tax system declaration. For the simplified tax system “income-expenses” - page 213. See return application The latest letters indicate that 1% of additional contributions should be calculated only from income (letter of the Ministry of Finance dated 02.12.2018 No. 03-15-07/8369) (letter of the Federal Tax Service dated 02.21.2018 No. GD-4-11/3541) (letter Federal Tax Service dated January 21, 2019 No. BS-4-11/799. | Result of column 4 of the Book of Income and Expenses. In this case, expenses are not taken into account. Many people find it difficult to calculate the simplified tax system along with the Pension Fund deduction. Use this automated simplification form in Excel. The form contains all years, taking into account additional individual entrepreneur contributions. For earlier years there is also - in the same place. |

| Patent system | Potential income. Calculated in accordance with Article 346.47 and 346.51 of the Tax Code of the Russian Federation | Income from which the cost of the patent is calculated. In this case, expenses are not taken into account. |

| UTII | Imputed income. Calculated in accordance with Article 346.29 of the Tax Code of the Russian Federation | Section 2 page 100 of the UTII Declaration (calculation here). If there are several Sections 2, all amounts on line 100 are added together. In this case, expenses are not taken into account. When calculating for the second quarter (and beyond), you need to take into account (plus) the profitability of previous quarters. |

| Unified agricultural tax | Income subject to Unified Agricultural Tax. Calculated in accordance with clause 1 of Article 346.5 of the Tax Code of the Russian Federation | Result of column 4 of the Book of Income and Expenses. In this case, expenses are not taken into account. |

If the individual entrepreneur was closed and opened in the same year?

Then the periods are considered separately, as unrelated. Those. for one period a deduction of 300 thousand rubles is given. and for the second period of work, individual entrepreneurs are also given a deduction of 300 tr (Letter of the Ministry of Finance dated 02/06/2018 No. 03-15-07/6781). However, we do not specifically recommend using this loophole. The maximum you will receive is 3000 rubles and minus all duties and then 1500 rubles. You will spend ten times more time and nerves.

See the article: Return by an individual entrepreneur of personal contributions for previous years.

Example income is 1,000,000 rubles. 27,990 rubles: pay before December 25, 2020 (this is for any income). Plus 1% of the difference (1,000,000 - 300,000) = 7,000 rubles additionally paid before July 1, 2018 for the insurance part of the Pension Fund.

Constitutional Court ruling

On December 2, 2020, the Constitutional Court of the Russian Federation published Resolution No. 27-P

Its essence is that individual entrepreneurs on OSNO can take into account expenses when calculating an additional contribution (1% percentage of income) to the Pension Fund. Before this, individual entrepreneurs on any system calculated an additional contribution from their income. The decision applies only to individual entrepreneurs on OSNO, however, individual entrepreneurs in other systems can also refer to it to prove their case in court.

How to fill out receipts for mandatory insurance premiums for individual entrepreneurs in 2020?

Important. Please note that starting from February 4, 2020, the details for paying taxes and contributions in 26 regions of the Russian Federation will change. Please read here: I recommend checking your details with your tax office after this date, as well as updating your accounting programs.

Good afternoon, dear individual entrepreneurs!

Let’s assume that an individual entrepreneur without employees decides to pay mandatory contributions “for himself” for the full year 2020. Our individual entrepreneur wants to pay mandatory contributions quarterly, in cash, through a branch of SberBank of Russia. Also, our individual entrepreneur from the example wants to pay 1% of the amount exceeding 300,000 rubles per year at the end of 2020, but we will talk about this case at the very end of this article. (Of course, an individual entrepreneur on the simplified tax system has “income” with zero annual income, or less than 300,000 rubles per year should not pay this 1%.)

In this case, our individual entrepreneur must pay the state for 2018:

- Contributions to the Pension Fund “for yourself” (for pension insurance): 26,545 rubles

- Contributions to the FFOMS “for yourself” (for health insurance): 5,840 rubles

- Total for 2020 = 32,385 rubles

- Also, don’t forget about 1% of the amount exceeding 300,000 rubles of annual income (but more on that below)

A little hint. To understand where these amounts come from, I advise you to read the full article on individual entrepreneurs’ contributions “for themselves” for 2018:

https://youtu.be/HVSgbp_RLwc

But back to the article... Our individual entrepreneur wants to pay quarterly in order to evenly distribute the load throughout 2020.

This means that he pays the following amounts every quarter:

- Contributions to the Pension Fund: 26545: 4 = 6636.25 rubles

- Contributions to the FFOMS: 5840: 4 = 1460 rubles

That is, our individual entrepreneur prints two receipts for payment of insurance premiums every quarter and goes with them to Sberbank to pay in cash. Moreover, the deadlines for quarterly payments are as follows:

- For the first quarter of 2020: from January 1 to March 31

- For the second quarter of 2020: from April 1 to June 30

- For the third quarter of 2020: from July 1 to September 30

- For the fourth quarter of 2020: from October 1 to December 31

In our example, we will consider exactly the case when an individual entrepreneur pays quarterly. Almost all accounting programs and online services offer these terms for payment of contributions. Thus, the burden of mandatory insurance contributions for individual entrepreneurs is distributed more evenly.

And an individual entrepreneur using the simplified tax system of 6% can still make deductions from advances under the simplified tax system. Please note that if you have an individual entrepreneur account with a bank, it is strongly recommended that you pay contributions (and taxes) only from it. The fact is that banks, starting from July 2020, control this moment. And if you have a bank account for an individual entrepreneur, then be sure to pay all taxes and contributions only from the individual entrepreneur’s account, and not in cash

Follow the link:

https://service.nalog.ru/payment/payment.html?payer=ip#paymentEdit

We agree to the processing of personal data and click on the “Continue” button:

Select the payment method “Filling out all payment details of the document”

Since we pay as individual entrepreneurs, we check the boxes as follows:

Click the “Next” button

And we immediately indicate the required KBK

- If we pay a mandatory contribution to pension insurance “for ourselves,” then we enter the BCC for 2020: 18210202140061110160

- If we pay a mandatory contribution to health insurance “for ourselves,” then we enter another BCC for 2020: 18210202103081013160

Important: enter KBK WITHOUT SPACES!

That is, when you issue these two receipts for pension and health insurance, you will do this procedure twice, but at this step you will indicate different BCCs and different payment amounts, which are indicated above and highlighted in yellow.

Let me remind you once again about the payment amounts for the full year 2020:

- Contributions to the Pension Fund “for oneself” (for pension insurance): 26,545 rubles

- Contributions to the FFOMS “for yourself” (for health insurance): 5840 rubles

If you do it quarterly, the amounts will be as follows:

- Contributions to the Pension Fund: 26545: 4 = 6636.25 rubles

- Contributions to the FFOMS: 5840: 4 = 1460 rubles

It is clear that if the individual entrepreneur has worked for less than a full year, then you will have to recalculate the contributions yourself, taking into account the date of opening (or closure of the individual entrepreneur). Instead of paying fees for a full year.

And again click on the “Next” button. In the “IFTS Code” field, enter the tax office code. Let our individual entrepreneur live in the mountains. Ivanovo, and its tax office code is 3702 (see screenshot below).

Of course, you will enter your tax office code.

If you don’t know the code of your tax office, then pay attention to the hint on the right (see the picture above).

Click the “Next” button

We select the status of the person who issued the payment as “09” - taxpayer (payer of fees) - individual entrepreneur.

- TP – current year payments

- And indicate the tax period: GY-annual payments 2018

- Enter the payment amount (of course, you may have a different amount)

Next, enter your information. Namely:

- Surname

- Name

- Surname

- TIN

- Registration address

Please note that you need to pay fees on your own behalf. Click the “Next” button and check everything again...

After making sure that the data is entered correctly, click on the “Pay” button. If you want to pay in cash, using a receipt, then select “Cash payment” and click on the “Generate payment document” button

That's it, the receipt is ready

- Since we entered KBK 18210202140061110160, we received a receipt for payment of mandatory contributions to the pension insurance of individual entrepreneurs.

- In order to issue a receipt for payment of the mandatory contribution for health insurance, we repeat all the steps, but at the stage of entering the BCC, we indicate a different BCC: 18210202103081013160

Example of a receipt for a quarterly payment for compulsory pension insurance:

Example of a receipt for a quarterly payment for compulsory health insurance:

We print these receipts and go to pay at any Sberbank branch (or any other bank that accepts such payments). Payment receipts and receipts must be kept!

Important: It is better not to delay the deadline for paying mandatory contributions “for yourself” until December 31, as the money may simply “get stuck” in the depths of the bank. It happens. It is better to do this at least 10 days before the expiration date.

How to generate a receipt for payment of 1% of an amount exceeding 300,000 rubles per year?

Indeed, those individual entrepreneurs whose annual income in 2020 will be MORE than 300,000 rubles are also required to pay 1% of the amount exceeding 300,000 rubles.

In order not to repeat myself, I am sending you to read a more detailed article about individual entrepreneur contributions “for yourself” in 2020:

We are now more interested in another question: where can I get a receipt for paying this 1%? Let me remind you once again that this payment must be made strictly before July 1, 2020. (based on the results of 2018, of course). So here it is. Unlike 2020, there is no separate BCC for paying 1%.

This means that when the time comes to pay this 1%, you will need to generate exactly the same receipt as for paying contributions to compulsory pension insurance.

That is, when issuing a receipt for payment of 1%, indicate BCC 18210202140061110160 (but it is possible that this BCC will change in 2020. Therefore, follow the news and update your accounting programs in a timely manner). There was already an attempt to introduce a separate BCC for 1% at the beginning of 2020, which was described here:

In fact, you have exactly the same receipt as when paying a mandatory contribution to pension insurance. Only there will be a different payment amount, of course.

https://youtu.be/MJaJZJpziek

That's all, actually.

But finally, I will repeat once again that such payments need to be processed in accounting programs and services. There is no need to do everything manually in the hope of saving several thousand rubles...

PS Let me remind you that the service can be found at this link: https://service.nalog.ru/

Best regards, Dmitry Robionek

Receive the most important news for individual entrepreneurs by email!

Stay up to date with changes!

By clicking on the “Subscribe!” button, you consent to the newsletter, the processing of your personal data and agree to the privacy policy.

I remind you that you can subscribe to my video channel on Youtube using this link:

https://www.youtube.com/c/DmitryRobionek

Reporting

The pension payment period is from January 1 to December 31 of the reporting year. The deadline for paying an additional 1% is from January 1 of the current year to April 1 (from 2020 (for 2020) - until July 1) of the next year. You can pay the fee in installments. For example, with UTII you need (with the simplified tax system it is advisable) to pay quarterly in order to deduct it from the tax. If an individual entrepreneur fails to pay a payment to the Pension Fund on time, a penalty

in the amount of 1/300 multiplied by the refinancing rate per day. Penalty calculator

Since 2012, individual entrepreneurs have not submitted reports to the Pension Fund (except for heads of peasant farms). For 2010 there was RSV-2, previously ADV-11.

Payment

KBK

Why is the BCC of a regular Pension Fund for exceeding 300 tr.

coincide with 2020? We have been paying for one BCC since 2020 - they are the same (letter of the Ministry of Finance dated 04/07/2017 No. 02-05-10/21007).

KBC are correct here.

On February 22, 2020, a new BCC was introduced for payments over 1% of insurance premiums - 182 1 0210 160 (order No. 255n dated December 27, 2017). However, then it was canceled (order dated February 28, 2018 No. 35n). For the additional percentage, the BCC does not change.

| Payment type | Until 2020 (for any year - 2020, 2020, etc.) | After 2020 (for any year - 2020, 2020, 2020, etc.) |

| Insurance contributions for pension insurance of individual entrepreneurs for themselves in the Pension Fund of the Russian Federation in a fixed amount (based on the minimum wage) | 182 1 0200 160 | 182 1 0210 160 |

| Insurance contributions for pension insurance of individual entrepreneurs for themselves in the Pension Fund of the Russian Federation with income exceeding 300,000 rubles. | 182 1 0200 160 | 182 1 0210 160 |

| Insurance premiums for medical insurance for individual entrepreneurs for themselves in the Federal Compulsory Compulsory Medical Insurance Fund in a fixed amount (based on the minimum wage) | 182 1 0211 160 | 182 1 0213 160 |

How long should payments be kept?

Within 6 years after the end of the year in which the document was last used for calculating contributions and reporting (Clause 6 of Part 2 of Article 28 of the Federal Law dated July 24, 2009 No. 212-FZ) or 5 years (clause 459 Order of the Ministry of Culture of Russia dated August 25 .2010 N 558)

Methods

Attention! Starting from 2020, the new KBK and the new recipient of contributions are not the Pension Fund of Russia, but the Federal Tax Service. Even contributions for December must be transferred according to the new BCC to the Federal Tax Service (except for contributions to the Social Insurance Fund for injuries). Here you can find out the details of your Federal Tax Service.

There are four ways:

- Through Sberbank in cash. Completed three Sberbank pension receipts (xls). PF data must be taken from their payment slips. Then you need to provide copies of receipts to the pension fund.

- If you have a bank account, then you can use it for Samples of payment orders for 2016-2017 and the Free Business Pack program to generate them for instructing the bank to make transfers through a bank account.

- Via Internet banking. For example, Tinkoff is one of the most convenient.

- You can combine these methods or use any of them in any order.

Article 113 of the Tax Code of the Russian Federation on the three-year limitation period does not apply to the Pension Fund of the Russian Federation! For such contributions, the requirement for payment is made “no later than three months from the date of discovery of the arrears” (Article 70 of the Tax Code of the Russian Federation). Arrears can be identified for any period. Therefore, keep your bills for the rest of your life.

If I am an individual entrepreneur and at the same time an employee in another organization, can I not pay Pension Fund contributions as an individual entrepreneur?

Contributions will need to be paid both here and there. Taxes and contributions of individual entrepreneurs and employees are in no way connected and there are no benefits.

What kind of income must be on the simplified tax system for 6% income in order to deduct the entire amount of the Pension Fund and the Compulsory Medical Insurance Fund from the simplified tax system?

Individual entrepreneurs (not employers) can reduce the simplified tax system (if income is simplified tax system) to 100% (employers reduce it to 50%) In 2020, we will divide 23,153.33 rubles. rubles by 0.06 and we get 385,888.83 rubles. income for the year, or 32,157.40 rubles. per month (if it is less, the simplified tax system is not paid). In 2020 we will divide 27,990 rubles. rubles by 0.06 and we get 466,500 rubles. income for the year, or 38,875 rubles. per month (if it is less, the simplified tax system is not paid). In 2020 we will divide 32,385 rubles. rubles by 0.06 and we get 539,750 rubles. income for the year, or 44,979.17 rubles. per month (if it is less, the simplified tax system is not paid).

With such income or less, an individual entrepreneur without employees is always more profitable than the simplified tax system, because then the tax is simply not paid. Unlike OSNO, UTII, PSN.

Return

You can return the funds if:

- Paid more by mistake

- If you were given the maximum for a failed return

- If you did not take into account expenses under OSNO and simplified tax system, income and expenses

See return application

How to fill out a payment order for payment of contributions

- Payer status - 09

- Gearbox - 0

- Your data: Full name (IP) //Residence address//

- Tax details

- KBK code

- OKTMO code

- Basis of payment - TP

- Tax period - GD.00.2018

- Payment order: 5

- Code - 0

- Fields 108, 109 - 0, field 110 - not filled in

- Purpose of payment

- In the Payer status field, enter 09 - individual entrepreneur.

- Enter 0 in the checkpoint field.

- In the Payer field, indicate your full name (IP) //Residence address//.

- In the Recipient field, enter the details of the tax office.

- In field 104, enter the KBK code.

- In field 105, enter the OKTMO code (municipality code) for your address.

- In the Basis of payment field, indicate TP - payments for the current year.

- In the Tax period field, enter GD.00.2019.

- In the Payment sequence field, enter 5.

- In the Code field, enter 0.

- In fields 108–109, enter 0. Field 110 is blank.

- Specify the purpose of payment:

- Insurance contributions for compulsory pension insurance on income not exceeding 300 thousand rubles. (for a fixed amount of contributions),

- Insurance contributions for compulsory pension insurance on incomes over 300 thousand rubles. (for additional 1%),

- Insurance premiums for compulsory health insurance.

Right not to pay

This right only exists if you have zero income for the year, so there is almost no point in it.

From 2020, the right not to pay contributions remains. However, it is regulated by other laws.

The payers specified in subparagraph 2 of paragraph 1 of Article 419 of this Code do not calculate and pay insurance contributions for compulsory pension insurance and compulsory medical insurance for the periods specified in paragraphs 1 (in terms of conscription military service), 3, 6 - 8 parts 1 of Article 12 of the Federal Law of December 28, 2013 N 400-FZ “On Insurance Pensions”, as well as for periods during which the status of a lawyer was suspended and during which they did not carry out relevant activities. (Clause 7 of Article 430 of the Tax Code Chapter 34 Insurance premiums)

Now look at 400-FZ, Article 12 of the Law on Insurance Pensions:

1) the period of military service, as well as other service equivalent to it

3) the period of care of one of the parents for each child until he reaches the age of one and a half years, but not more than six years in total;

6) the period of care provided by an able-bodied person for a group I disabled person, a disabled child or a person who has reached the age of 80 years;

7) the period of residence of spouses of military personnel performing military service under a contract, together with their spouses, in areas where they could not work due to lack of employment opportunities, but not more than five years in total;

the period of residence abroad of spouses of employees sent to diplomatic missions and consular offices of the Russian Federation, permanent missions of the Russian Federation to international organizations, trade missions of the Russian Federation in foreign countries, representative offices of federal executive authorities, state bodies under federal executive authorities or as representatives these bodies abroad, as well as to representative offices of state institutions of the Russian Federation (state bodies and state institutions of the USSR) abroad and international organizations, the list of which is approved by the Government of the Russian Federation, but not more than five years in total;

the period of residence abroad of spouses of employees sent to diplomatic missions and consular offices of the Russian Federation, permanent missions of the Russian Federation to international organizations, trade missions of the Russian Federation in foreign countries, representative offices of federal executive authorities, state bodies under federal executive authorities or as representatives these bodies abroad, as well as to representative offices of state institutions of the Russian Federation (state bodies and state institutions of the USSR) abroad and international organizations, the list of which is approved by the Government of the Russian Federation, but not more than five years in total;

However, you can not pay only if during the above periods no business activity was carried out (income 0 rubles) (Article 430, paragraph 8 of the Tax Code of the Russian Federation). It is necessary to submit documents confirming the absence of activity during the specified periods. As you understand, it’s easier to just close the IP.

For such an exemption, it is necessary to provide an Application for exemption from payment of insurance premiums (pdf, 615 kb.) (Letter of the Federal Tax Service of Russia dated 06/07/2018 N BS-4-11 / [email protected] “On the recommended form of the Application”).

Show/hide Right not to pay from 2013 to 2020:

Since 2013, you can avoid paying fixed contributions for the following periods:

- conscription service in the army;

- the period of care of one of the parents for each child until he reaches the age of one and a half years, but not more than three years in total;

- the period of care provided by an able-bodied person for a group I disabled person, a disabled child or a person who has reached the age of 80 years;

- the period of residence of spouses of military personnel serving under contract with their spouses in areas where they could not work due to lack of employment opportunities, but not more than five years in total;

- the period of residence abroad of spouses of employees sent to diplomatic missions and consular offices of the Russian Federation, permanent missions of the Russian Federation to international organizations, trade missions of the Russian Federation in foreign countries, representative offices of federal executive authorities, state bodies under federal executive authorities, or as representatives of these bodies abroad, as well as to representative offices of state institutions of the Russian Federation (state bodies and state institutions of the USSR) abroad and international organizations, the list of which is approved by the Government of the Russian Federation, but not more than five years in total.

However, if no business activity was carried out during the above periods (Parts 6-7, Article 14 of Law 212-FZ), it is necessary to submit documents confirming the absence of activity during the specified periods. Those. all the conditions above must be present, and the income must also be zero. In this case, it is easier to close the individual entrepreneur.