The legal topic is very complex, but in this article we will try to answer the question “Is income tax deducted from the minimum wage in 2020?” Of course, if you still have questions, you can consult with lawyers online for free directly on the website.

Finally, there is an option to legally establish that the minimum wage in the region should be 15% higher than the subsistence level of an able-bodied citizen. In this case, no deduction will be needed - after withholding 13% income tax, you will get the required amount.

This risk looks rather dubious. For the employer, what is much more terrible is the social contributions for the employee, which he must make every month. Contributions to pensions, medicine and social insurance are a third of what is paid to the employee. The source of the problem of “gray” salaries lies precisely here.

What scheme for obtaining deductions may appear?

If we speak in all-Russian figures, then in 2020, everyone who receives a salary of up to 12,966 rubles per month should be exempt from personal income tax. By subtracting 13% of personal income tax from this amount, we get 11,280 rubles of the subsistence minimum - the required minimum wage.

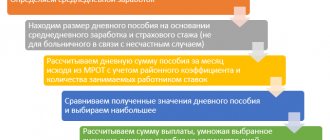

For each day of sick leave, the employee will receive 370 rubles 85 kopecks. If over the previous two years the employee took sick leave, then these days are subtracted from 730 days and, accordingly, the number of months is reduced.

- Combined work. According to para. 1 tbsp. 285 of the Labor Code of the Russian Federation, the employee receives funds for the time worked. The minimum wage is set based on 40 workers per week.

- Part time. The employee works less time and spends less effort. For example, the work of a pregnant woman, piecework, part-time work of students, etc.

Maternity

- work experience of more than six months with full-time work: the benefit is calculated from the average daily earnings and may exceed the minimum wage;

- less than six months of experience with full-time work: the monthly benefit calculation cannot exceed the monthly minimum wage.

it turns out if there are two or three of them - from 2800 and 4200. There are still some groups of people exempt from the 13% tax. The tax is taken from any official salary, there are simply tax deductions, for example, for minor children. You can apply for a deduction if you received paid treatment or paid for your child’s education. In order not to pay taxes, you need to receive a black salary. Income tax on wages is taken from any amount, but standard tax deductions are taken into account, for example, deductions for children (each child).

This is interesting: Debtors on microloans forum

The salary should be more than the minimum wage minus personal income tax or not

The minimum wage from November 1, 2015 is 17300 Moscow time. Tell me, should this amount be accrued as a minimum, or should this amount be paid in person, after withholding personal income tax?

In accordance with part three of Art.

133 of the Labor Code of the Russian Federation, the monthly salary of an employee who has fully worked the standard working hours during this period and fulfilled labor standards (labor duties) cannot be lower than the minimum wage.

What regulates the setting of the minimum wage of 12,500 in the Moscow region?

If there are instructions on the procedure for use?

(for example, who is entitled to an additional payment of up to 12,500? Does the effect apply to employees...

- Recalculation of maternity benefits 2020 from July 1, 2019 increase in the minimum wage, who needs to recalculate already paid maternity benefits (or in what cases?) How to reflect in the 6NDFL report payment for renting a car from an individual. a person who is not an employee of the organization. ✒ Calculation of 6-NDFL is presented for all individuals to whom your organization paid income....

- Paying a part-time job below the minimum wage What should be the minimum wage if a person gets a part-time job?

✒ The specifics of calculating wages for a part-time worker are regulated by Article 285 of the Labor Code of the Russian Federation. Salaries for part-time workers... - salary/tariff rate;

- compensation - various additional payments, including for difficult working conditions and climate, for night shifts and others;

- incentive payments - all kinds of bonuses, for example, at the end of the year, for length of service, and so on.

Can an employer pay an employee who has worked his full working hours a salary whose amount, after personal income tax withholding, is below the minimum wage?

Having considered the issue, we came to the following conclusion: Paying an employee a monthly salary, the amount of which after withholding personal income tax is less than the established minimum wage, does not contradict the law. In accordance with part three of Art.

133 of the Labor Code of the Russian Federation, the monthly salary of an employee who has fully worked the standard working hours during this period and fulfilled labor standards (labor duties) cannot be lower than the minimum wage.

The Tax Code of the Russian Federation considers wages to be one of the types of citizen’s income, subject to personal income tax (hereinafter also referred to as personal income tax).

The procedure for calculating and paying this tax is established by Chapter 23 of Part Two of the Tax Code of the Russian Federation.

Expert of the Legal Consulting Service GARANT Reviewer of the Legal Consulting Service GARANT The material was prepared on the basis of individual written consultation provided as part of the Legal Consulting service.

Can the salary be less than the minimum wage? When can you legally pay less than the minimum wage?

Now let's look at what a salary is - this is necessary to understand whether it is possible to set a salary less than the minimum wage.

The components of wages are:

In addition, there are certain types of payments that are not considered wages. For example, this is compensation for vacation, for a business trip, for forced cessation of work, and others.

But this is a general case, to which there are exceptions.

According to the law, an individual’s income tax is calculated on the amount of salary that the employer accrued to him.

And even if the “minimum wage” is charged, this does not exempt you from paying personal income tax.

Therefore, the employee will receive an amount reduced by the amount of tax.

If there are additional payments, it is necessary to calculate and take into account their amounts.

The salary can be reduced by the amounts of the mentioned additional payments - this will be the minimum salary of the employee.

Law office legal services

What does a salary consist of? Now let's look at what a salary is - this is necessary to understand whether it is possible to set a salary less than the minimum wage.

- incentive payments - all kinds of bonuses, for example, at the end of the year, for length of service, and so on.

- compensation - various additional payments, including for difficult working conditions and climate, for night shifts and others;

- salary/tariff rate;

In addition, there are certain types of payments that are not considered wages. For example, this is compensation for vacation, for a business trip, for forced cessation of work, and others.

However, for the first time, inspectors can get by with a warning.

Is it with or without personal income tax?

The minimum wage is the legally established minimum wage per month.

Application of the minimum wage The minimum wage is applied for:

- the insured person did not earn money for 2 calendar years before the date of the insured event;

- average earnings calculated for 2 calendar years are lower than calculated according to the minimum wage.

In some cases, temporary disability benefits and maternity benefits are paid in an amount not exceeding the minimum wage for a full calendar month. This limitation applies to insured persons:

- who have an insurance period of less than 6 months;

- violating the regime prescribed by the doctor.

Minimum wage applied for fines, taxes and penalties To calculate taxes, fees, fines and other payments that are calculated in accordance with the legislation of the Russian Federation, depending on the minimum wage, the basic amount of the minimum wage is applied.

Therefore, the salary itself may be lower than the minimum minimum wage; this is not punishable by law if the employee’s total salary per month, taking into account all additional payments, reaches up to the minimum wage.

Is it legal for an employee to be assigned a minimum wage, but after deducting tax, he receives significantly less?

Hello! Please tell me, is it legal for an employee to be assigned a minimum wage, but after deducting tax, he receives significantly less than the minimum wage?

Thanks for the free consultation. Wages are one of the types of income of a citizen, subject to personal income tax.

The procedure for calculating and paying this tax is established by Chapter 23, Part Two of the Tax Code of the Russian Federation.

Personal income tax and minimum wage

Moreover, these workers imagine that, firstly, everyone is deceiving them, and secondly, they know for sure.

that nothing is being held back, and are very impenetrable in their position.

It is very problematic to explain to them - the NK is not their order.

And the integrity of the guards, the bank’s care for clients, or whether it is necessary to accrue 5000.00, then the person receives 4350.00, which seems to be more than the minimum wage (I do not take into account the 400.00 benefit and the increase in the minimum wage in the regions), I just want to figure it out. The employee’s salary is set without taking into account it is included somewhere there is personal income tax or not. If our employee has 2 children under 18 years old, then I can do the following:

What to do if your salary is below the minimum wage

Current as of: March 7, 2020

It is important to note that if, after withholding personal income tax from the income due to the employee, he receives an amount less than the minimum wage, then this does not threaten the employer.

Keep in mind that from 05/01/2019 the minimum wage will increase to 11,163 rubles.

Source: https://credit-helper.ru/oklad-dolzhen-byt-bolshe-mrot-za-minusom-ndfl-ili-net-25741/

Is income tax deductible from the 2020 minimum wage?

Today, unfortunately, in terms of the minimum wage, Russia is in the bottom ranks of the countries of the world, below Latin America and even some African countries. At the same time, income tax is also deducted from the minimum wage, and indirectly, insurance premiums. Actually, these payments, as well as the economic recession, are the reason for such deplorable income guarantees for the population.

This is interesting: Alimony amount for a non-working father in 2020

Should minimum wage be taxed in 2020?

Violation of labor legislation requirements can be costly for the director of an enterprise. Its organization will become the object of close attention from fiscal authorities. Inspections of an enterprise's activities will inevitably lead to additional fines.

- Determination of the minimum amount of benefits for temporary disability, pregnancy and childbirth.

- Determination of the amount of taxes, fees, fines and other payments, which are calculated in accordance with the legislation of the Russian Federation depending on the minimum wage (a different amount is accepted, see below).

Minimum wage with or without personal income tax

1. Mandatory, which are carried out on the basis of the norms of the current legislation of the Russian Federation. 2. Deductions at the initiative of the employer (in accordance with labor legislation).

3. Deductions at the initiative of the employee (based on a corresponding statement written by him).

Personal income tax withholding from wages in 2020 is carried out on the basis of the tax base, tax deductions and tax rates. It should be noted that they are used to calculate income tax only for residents of the Russian Federation. The tax rate, depending on individual income, can be:

Minimum wage 2020 - minimum wage from July 1, 2019

As we see, an employee’s salary can consist of several parts (salary, various additional payments, bonuses), so the employer can establish in a local regulatory act (staffing table) the minimum salary less than the minimum wage, but on the condition that taking into account compensation and incentive payments the employee's salary will not be lower than the established minimum wage. If an employee is only paid a salary, then its amount cannot be less than the minimum wage - federal or regional.

Subjects of the Russian Federation, Article 133.1 of the Labor Code, are given the right to establish on their territory a minimum wage that exceeds that indicated above (the so-called “minimum wage”).

In this case, the establishment of a higher minimum wage is permitted by the adoption by a constituent entity of the Russian Federation of a regional agreement on the minimum wage.

The meaning of such an agreement is that if such a normative act is adopted by a subject of the Russian Federation, employers operating on its territory must pay employees wages not lower than the minimum wage established by the law of the subject of the Russian Federation.

Minimum salary is subject to personal income tax

According to part one of Art.

129 of the Labor Code of the Russian Federation, wages are remuneration for work depending on the qualifications of the employee, the complexity, quantity, quality and conditions of the work performed, as well as compensation payments (additional payments and allowances of a compensatory nature, including for work in conditions deviating from normal, work in special climatic conditions and in areas exposed to radioactive contamination, and other compensation payments) and incentive payments (additional payments and incentive allowances, bonuses and other incentive payments).

From Art. 133 Labor Code of the Russian Federation and Art. 226 of the Tax Code of the Russian Federation it follows that the rule of part three of Art. 133 of the Labor Code of the Russian Federation on the relationship between wages and the minimum wage applies to the amount of wages calculated before the withholding of taxes and other payments (for example, according to writs of execution).

An employee who has been paid a monthly salary in the amount of the minimum wage is not exempt from paying personal income tax, and the tax is withheld by the tax agent from the accrued amount.

As a result, the amount given to the employee is guaranteed to be less than the minimum wage established by law, but there will be no violation of the law in this case.

Interesting: General procedure for conducting a special assessment of working conditions

Minimum salary with or without personal income tax

Do they take income tax now from the minimum wage? The minimum wage is the minimum wage, your salary is your income, on which personal income tax is subject to payment.

Perhaps this tax was not previously withheld from you due to the fact that you have the right to social and... from any amount of income from the minimum wage, as before, from income... All types of income are subject to taxation. From the minimum wage minus your 400 rubles. if there are children minus 600 rub.

for each and from the remaining amount 13% of income What taxes are charged on the minimum wage in Ukraine? to the pension fund to the social insurance and security authorities to the health insurance fund to the employment fund withholding income tax - minimum wage, mother is divorced, son in full-time education until the age of 18, income tax will be withheld at 13%.

January 2020 Typical VAT errors We continue to study the characteristic violations identified by the Federal Tax Service during on-site inspections. The Tax Service posted information about these violations on the website nalog.ru.

Let's look at current errors in calculating the VAT base and in applying deductions. Tax amnesty for individual entrepreneurs - 2020 Today, tax debts in Russia are registered for more than 40 million people, and the amount of debt exceeds 40 billion rubles.

, noted Russian President Vladimir Putin at a large press conference at the end of 2020.

- Article 136 of the Labor Code of the Russian Federation stipulates that the employer is obliged to pay cash to employees twice a month. One of these payments is called an advance.

- Article 226 of the Tax Code of the Russian Federation states that the employer is obliged to withhold personal income tax from the actual income of employees, and then transfer it to the budget.

- Article 223 of the Tax Code of the Russian Federation regulates the date of actual receipt of income - the last day of the month.

- Salaries are calculated for the period, taking into account various additional payments and coefficients;

- it becomes clear what types of income are subject to taxation;

- the taxpayer status is determined for the calculation and payment of income tax on wages;

- the taxpayer's rights to deductions are analyzed;

- the amount of income not subject to taxation, as well as deductions, is deducted from the salary amount;

- personal income tax is calculated at the appropriate rate.

Minimum wage 2020 minimum wage from May 1, 2019

The work of part-time workers is also paid in proportion to the time worked, depending on the terms of the employment contract (Article 285 of the Labor Code). The employer is not obliged to make additional payments up to the minimum wage to persons working part-time if the amount of their remuneration specified in the employment contract for part-time work does not exceed the minimum wage.

According to the rules of Part 3 of Article 133.1 of the Labor Code, the amount of the minimum wage for a specific subject is determined taking into account socio-economic conditions and the cost of living of the working population on its territory. Part 4 of Article 133.1. The Labor Code establishes that the minimum wage cannot be lower than the federal minimum wage.

Calculation of accruals and deductions from wages in 2019

Example 1. Kharchenko T.P. The official salary is set at 2300 UAH. and a 40 hour work week. In January 2020, the employee was on leave without pay for 2 days. According to the working time sheet, the employee worked 17 days, while the standard working time in January was 19 days.

Interesting: Heirs of the first and second stages

Over the past years, Ukrainians have been waiting for an increase in the size of the tax social benefit to 100% of the subsistence minimum for able-bodied persons, but changes were made to paragraphs of Law No. 909-VIII. 169.1.

1 NKU, which approves the size of the NSL at the level of 50% of the subsistence level established on January 1 of the current year. In 2020, the usual amount of tax social benefits will be 689 UAH, 150% of the NSL - 1033.50 UAH.

; 200% NSL - 1378.00 UAH.

How to calculate personal income tax from your salary

/ condition / Salary E.O. Ivanova is 36,000 rubles. per month. She has a daughter aged 12, due to which E.O. Ivanova is provided with a standard deduction for a child in the amount of 1,400 rubles. per month. In addition, in April she was paid an additional bonus of 12,000 rubles. Let's determine the amount of personal income tax withheld from the employee's income for the month of April.

Employers calculate the tax base for employee income, taxed at a rate of 13%, based on the results of each month on an accrual basis from the beginning of the year (clause 3 of Article 226 of the Tax Code of the Russian Federation). The amount of income the employee receives must be reduced by the personal income tax deductions provided to him (clause 3 of Article 210 of the Tax Code of the Russian Federation). That is, the tax base is calculated using the formula:

Minimum salary in 21018 minus personal income tax

Source: https://urist-yslugi.ru/test_category/minimalnaya-zarabotnaya-plata-s-ndfl-ili-bez

Tax deduction for single mothers

Single mother is a status that is assigned to a woman who gave birth without registering a marriage, and an application to establish paternity was not submitted to the registry office.

- If the child was born 300 days after the divorce from the previous spouse or there is a court decision that the husband is not the biological father of the child.

- Or the child was adopted by a woman out of wedlock . In all these cases, a dash is placed in the father column.

A certificate is issued in form No. 25 , where it is written that the father is registered according to the mother’s words. And it shouldn’t be considered as such. The child's surname comes from the mother.

Article No. 218 of the Russian Tax Code states that single mothers have the right to a double tax deduction for each child upon reaching 18 years of age.

- If, after reaching the age of 18, the child continues studying, then the period is extended by the end of studies, but no later than the age of 24.

- To receive a tax deduction , the employee must provide the necessary certificates to the personnel department or accounting department (a copy of the birth certificate and a copy of the certificate in form No. 25 issued to the registry office).

- The amount of tax deduction for a single mother is 2800 for two children , for all subsequent children 6000 rubles . For a student 6,000 and if a child of a single mother is disabled, then the same 6,000 rubles.

Russians with minimum wage may be exempt from income tax

The publication Izvestia reports today that some Russians may be exempt from personal income tax. If such a decision is made, there will be slightly fewer poor people in Russia. Let's figure out what we're talking about. What tax deduction may appear in our country for workers who receive wages at the minimum or slightly above the minimum wage.

What is it about

Almost exactly a year ago, the minimum wage in Russia reached the subsistence level for the first time. From May 1, 2020, the minimum wage in our country is equal to the subsistence level of an able-bodied citizen.

It would seem that this is quite obvious - the smallest salary should provide the worker so that he can at least satisfy the minimum needs for food and non-food goods and services.

Moreover, this obvious logic was enshrined in law. It has long been established that the minimum wage should not be lower than the subsistence level. But such a norm did not work; the state introduced a transition period for itself and took a long time to increase the minimum wage to its established lower limit.

Formally, at the moment the minimum wage and the subsistence minimum are equal. In 2019, the national average subsistence minimum for a working-age citizen is 11,280 rubles. The same minimum wage was established on January 1.

The problem is that the minimum wage today still does not reach the subsistence level.

It's all about taxes, which no one has canceled. It doesn’t matter what salary a Russian receives, in any case, 13% income tax is withheld from it. Accordingly, after deducting personal income tax, the minimum wage is “shrunk” to 9,814 rubles or 87% of the subsistence level.

The Russian tripartite commission for the regulation of social and labor relations (RTK), which includes the state, trade unions and employers' associations, has finally paid attention to this problem. Within the framework of the RTC, the possibility of exempting those who receive the minimum salary or a salary slightly above the minimum from income tax is being discussed.

A new tax deduction for minimum wage recipients may appear in Russia

In order to guarantee a real minimum wage at the subsistence level, it is necessary to exempt not only those who receive the minimum wage from tax. Those who earn a little more should be deducted.

If we speak in all-Russian figures, then in 2020, everyone who receives a salary of up to 12,966 rubles per month should be exempt from personal income tax. By subtracting 13% of personal income tax from this amount, we get 11,280 rubles of the subsistence minimum - the required minimum wage.

There is no exact data on how many employees could fall under such a deduction. Izvestia reports the closest statistics available - salaries below 13,800 rubles at the end of 2020. The year before, more than 15% of workers, or 11 million people, received such income.

We gave an average example for the country. The RTK proposes a fairer solution - to tie the actual minimum wage not to the all-Russian subsistence minimum, but to the regional value.

In each individual region of Russia, wages should not be lower than the cost of the minimum set of goods and services specifically in that region. It is impossible to live on the national average of 11,280 rubles, for example, in the north or the Far East, where the cost of living can be twice the national average.

What scheme for obtaining deductions may appear?

If such a law comes into force at all, there are several possible mechanisms for providing such a deduction for personal income tax.

The first is at the request of the employee himself to the tax authorities. The employer will withhold income tax from the salary, and the employee can apply for an income tax refund once a year. This is how deductions for treatment, education, and home purchases work today.

This option is bad for many reasons. The employee will receive a salary below the minimum throughout the year. Then he will have to collect certificates and submit them to the tax authorities. For tax officials, the additional flow of people is also an extra headache.

The second option is to receive a deduction through your employer. The accounting department itself will fill out all the paperwork and justify to the tax authorities why salary taxes are not withheld from the employee. This option is more convenient and obvious.

Finally, there is an option to legally establish that the minimum wage in the region should be 15% higher than the subsistence level of an able-bodied citizen. In this case, no deduction will be needed - after withholding 13% income tax, you will get the required amount.

Risks for the state

Experts interviewed by Izvestia say that the emergence of such a deduction means some risks for the state. They say that it will be beneficial for employers to set a minimum wage for employees so as not to pay taxes. The rest will be issued in an envelope.

This risk looks rather dubious. For the employer, what is much more terrible is the social contributions for the employee, which he must make every month. Contributions to pensions, medicine and social insurance are a third of what is paid to the employee. The source of the problem of “gray” salaries lies precisely here.

It is unlikely that the emergence of a personal income tax deduction for minimum wage recipients will seriously affect the growth of the share of “gray” income in Russia. But for those who actually earn the minimum, a tax exemption could be good news.

, please select a piece of text and press Ctrl+Enter.

| You can share this material with your friends: |

Source: https://newsment.ru/context/rossiyan-s-minimalnoj-zarplatoj-mogut-osvobodit-ot-podohodnogo-naloga/

How is the amount of income tax taken into account when using a deduction?

It is necessary to understand that a tax deduction of any type - for example, social or, as an option, property - is provided to the payer solely at the expense of those amounts of income tax that he himself transferred to the budget. We are talking about actually repaid obligations to collect personal income tax, the rate of which is, as is known, 13 (thirteen) percent. Thus, if a citizen did not have taxable income and, accordingly, did not pay the corresponding amounts of personal income tax to the budget, he does not have the right to claim such a deduction.

It turns out that the real amount of tax compensation (deduction) directly depends on the amount of personal income tax actually paid by the entity to the budget.

The conditional deduction is paid to the citizen in full only when the amount of such compensation either corresponds to the total amount of tax transferred by the payer at the time of registration of the deduction, or is less than this amount.

What to do if the amount of the claimed compensation for income tax paid exceeds the personal income tax amount? It should be noted that the taxpayer in such a situation does not particularly risk anything. Experts say that such a phenomenon is considered quite common in Russian taxation practice. It is more than possible to receive a full tax refund under such circumstances. A taxpayer claiming a deduction in an amount exceeding the amount of tax actually paid should thoroughly understand the available methods for solving this problem.

Minimum salary before or after deduction

If an employee has deductions made from his wages - according to a writ of execution, due to financial liability to the employer, for the payment of alimony, then the final amount he receives may be much lower than the minimum wage. However, this situation is also not a violation of the law if the total amount of wages accrued to the employee was initially at the stipulated level.

The employer's refusal to join regional agreements.

If the salary is not lower than the minimum wage at the federal level, but lower than the minimum wage provided for by regional legislation, this situation may be acceptable if the employer has properly refused to comply with regional agreements and justified his refusal. However, this requires quite a lot of procedural costs on the part of the employer itself and can ultimately lead to conflicts with local authorities and trade union organizations.

New minimum wage

So, his salary for July 2020 will be 3,928.56 rubles. (5,000 rubles / 21 working days x 11 working days)

days + 2,500 rub. / 21 workers days

x 11 work. days). At the same time, the employee’s salary for days worked in July cannot be lower than RUB 4,085.71.

(RUB 7,800 / 21 working days x 11 working days)

days). Therefore, the employee must pay an additional 157.15 rubles.

(4 085,71 — 3 928,56).

Article 93 of the Labor Code of the Russian Federation provides that, by agreement between the employee and the employer, a part-time working day (shift) or a part-time working week can be established both upon hiring and subsequently. When working part-time, the employee is paid in proportion to the time he worked or depending on the amount of work he performed.

Consequently, his salary must be compared with the minimum wage, calculated in proportion to the established working time.

Minimum wage with or without personal income tax

d. The total amount of these charges must be no less than the minimum wage.

The employer, as a tax agent, withholds personal income tax from the accrued salary amount.

Therefore, the amount actually paid to the employee may be less than the minimum wage. If an employee works part-time or part-time, then he can receive less than the minimum wage per month: there are no legal obstacles here.

Minimum wage in calculating benefits In accordance with Federal Law dated December 29, 2006 No. 255-FZ (clause 1.1 of Art.

Can an employer pay an employee who has worked his full working hours a salary whose amount, after personal income tax withholding, is below the minimum wage?

Personal income tax from income less than minimum wage

Now the minimum wage is 85% of the subsistence level.

The amount of payments is influenced by several indicators:

- First of all, experts estimate the rate of inflation.

- The amount of the minimum wage depends on the number of unemployed.

- Economists take into account production growth indicators that affect the financial situation of regions.

Since January of this year, employers cannot pay their employees less than 9,489 rubles. The minimum wage performs several functions:

- The amount paid to the employee during illness depends on the size of this indicator.

- Without the minimum wage, it is impossible to calculate payments due to expectant mothers.

In the accounting department of any enterprise, specialists take into account the requirements prescribed in Art.

Is income tax deductible from the 2020 minimum wage?

In cash, the employee will receive 17,800 - (17,800 x 13%) = 17,800 - 2,314 = 15,486 rubles.

Therefore, personal income tax in general is 13%. Even on a salary equal to the minimum wage, you must pay 13% personal income tax. In this case, there will be no tax exemption, despite the fact that you will receive an amount below the minimum wage.

It's easier to ask a lawyer! to our lawyers - it’s much faster than looking for a solution. Minimum wage (minimum wage) An employee's salary must be no less than the minimum wage.

Receiving a deduction that exceeds the amount of income tax: options

The various ways to obtain compensation deductions are worth considering in detail, with examples characterizing typical situations.

First opportunity

First, submit through the tax service the part of the claimed deduction corresponding in amount to the income tax transferred to the budget at the time of application, and next year – the rest of the compensation, processed through new personal income tax transfers. If necessary, the unused balance of personal income tax compensation can be distributed into several parts and processed gradually in subsequent periods.

Example. In January 2020, a citizen purchased an apartment, paying 2 (two) million rubles for it. The costs incurred allow him to claim compensation in the amount of 260,000 rubles, which is 13% of 2 (two) million rubles. The monthly salary of this subject is 50,000 rubles. A tax of 6,500 rubles is stably withheld and transferred from this income, which is 13% of 50,000 rubles. In 2020, a citizen issues a deduction through the tax service in the amount of income tax paid for the year, which is 78,000 rubles (6,500 rubles multiplied by 12 months). The subject will be able to receive a similar amount of compensation with the same earnings in 2020. The balance of the due compensation is gradually processed in subsequent periods according to the described scheme.

Second possibility

The first part of the compensation payment is processed through the fiscal authority, and the rest of the deduction is processed through the employer (income payer), if there is a legal opportunity to implement such a scheme. Providing compensation to a citizen with this approach will be carried out simultaneously with the monthly withholding of personal income tax on paid income. Further receipt of compensation is also made through the employer - until the available balance of the claimed deduction is completely exhausted.

Example. Considering the conditional example outlined above, we can assume that a citizen who, in January 2020, formalizes the due compensation in the amount of 78,000 rubles through the tax authority, decides to request the required deduction through his employer and provides him with the necessary papers. The compensation is issued to the employee in February, which allows him to receive 71,500 rubles by the end of 2020 (6,500 rubles multiplied by 11 months).

Thus, the citizen’s total deduction for 2020 will be 149,500 rubles, which is the sum of the two requested compensations (78,000 and 71,500). This was made possible by using two available schemes simultaneously. In 2020, however, this entity will no longer be able to apply to the fiscal authority for a personal income tax refund, since the employer has already provided the required deduction. Meanwhile, the employee will have the right to again apply to his employer for compensation, practicing this scheme until the claimed compensation is fully paid.

Third possibility

You can initially issue a deduction through the employing organization, and then continue to receive the declared compensation according to this algorithm, taking into account the amount of the requested compensation. If an employee receives additional income subject to personal income tax, he will be able to request the balance of the due deduction through the fiscal authority.

Example. Appealing to the conditional example discussed above, we can assume that a taxpayer who purchased his own home in 2020 decided to immediately request compensation for it from his employer: Having issued such a deduction only from February 2020, the citizen for the remaining 11 (eleven) months receives compensation totaling 71,500 rubles. Continuing to regularly pay personal income tax in 2017 and receive the required compensation through his employer, the subject receives an annual deduction in the amount of 78,000 rubles. In January 2020, the employee is given a bonus in the amount of 1,000,000 rubles. The income tax withheld from this amount (130,000) allows the citizen to receive the balance of compensation in the amount of 110,500 rubles (the previously compensated 71,500 and 78,000 are deducted from 260,000). The amount of personal income tax unused by the taxpayer (19,500 rubles), defined as the difference between 130,000 and 110,500, will be sent to the budget.

Mort on hand or until personal income tax is withheld

Minimum income is a personal income tax or in your hands

- Is minimum income subject to personal income tax?

- Is it with or without personal income tax?

- Minimum wage (minimum wage)

- Minimum wage with or without personal income tax

- Minimum wage with or without personal income tax

Is minimum income subject to personal income tax? Minimum wage if:

- the insured person did not earn money for 2 calendar years before the date of the insured event;

- average earnings calculated for 2 calendar years are lower than calculated according to the minimum wage.

In some cases, temporary disability benefits and maternity benefits are paid in an amount not exceeding the minimum wage for a full calendar month. An employee who is accrued a monthly salary in the amount of the minimum wage is not exempt from paying personal income tax, and the tax is withheld by the tax agent from the accrued salary. amounts.

Minimum income is a personal income tax or in your hands

Minimum wage. The employer, as a tax agent, withholds personal income tax from the accrued salary amount. Therefore, the amount actually paid to the employee may be less than the minimum wage.

If an employee works part-time or part-time, then he can receive less than the minimum wage per month: there are no legal obstacles here.

Minimum wage in calculating benefits In accordance with Federal Law dated December 29, 2006 No. 255-FZ (clause 1.1 of Art.

Minimum wage with or without personal income tax Can an employer pay an employee who has worked the full standard working time a salary the amount of which, after withholding personal income tax, is below the minimum wage? Having considered the issue, we came to the following conclusion: Paying an employee a monthly salary, the amount of which after withholding personal income tax is less than the established minimum wage, does not contradict the law.

What salary should be at least minimum wage?

The procedure for calculating and paying this tax is established by Chapter 23 of Part Two of the Tax Code of the Russian Federation.

The employer is not obliged to make additional payments up to the minimum wage to persons working part-time if the amount of their remuneration specified in the employment contract for part-time work does not exceed the minimum wage.

Subjects of the Russian Federation, Article 133.1 of the Labor Code, are given the right to establish on their territory a minimum wage that exceeds the federal one established by Law No. 82-FZ (Article 133.1 of the Labor Code of the Russian Federation).

Will it be taken?

The employer is obliged to calculate personal income tax on all employee income, with the exception of those listed in Article 217 of the Tax Code of the Russian Federation.

How to legally avoid paying income tax?

Salary is taxable income, from which income tax (NDFL) is withheld - the calculation mechanism.

It doesn’t matter how much wages are paid, personal income tax must be deducted in any case.

Therefore, from a salary equal to the minimum, the employer also needs to calculate personal income tax (13%).

The question of the need to withhold income tax from the minimum wage arises due to the fact that after deducting the tax amount in hand, a person receives a salary less than the established minimum.

The employee, knowing that his work should not be paid below the established minimum wage, begins to be indignant, asking why he received so little, whether the employer violated his rights under Article 133 of the Labor Code of the Russian Federation.

In fact, the employer is not violating anything here.

Comparison of the assigned wage with the minimum wage limit must be carried out in relation to the amount accrued to the employee before tax.

Salary before income tax is the amount of money that is assigned to an employee for the work duties he performed during the pay period.

This salary is called accrued; it should not be less than the minimum wage.

Further, tax deduction obligations apply to the accrued amount:

- Income tax (personal income tax) – 13% of the accrued amount is withheld (subtracted), the employee will receive the difference in accrual and tax;

- Insurance contributions are calculated in excess of salary at a total rate of 30% and are paid to ensure compulsory insurance; contributions are not deducted from the accrued amount and are paid at the expense of the employer.

If for a month an employee receives a salary equal to the minimum wage, then 13% of income tax must also be deducted from it and contributions must be calculated.

The employee will receive less than the minimum amount due to the withholding of personal income tax from it. This is normal, it is permitted by law.

It is important to consider one point. An employee’s salary should not be less than the minimum, provided that he has worked a full month and performed the necessary duties.

If an employee worked for less than a full month, for example, was on sick leave for some time, or on vacation at his own expense, then his salary may be less than the minimum wage.

What tax is calculated according to the law in Russia?

Only income tax is calculated from the minimum wage; its rate for residents of the Russian Federation is 13%, for non-residents – 35%.

There are no more tax deductions from your salary.

Insurance premiums are not deducted from the accrual, as they are an expense of the employer, not the employee.

Example

Initial data:

Salary of Petukhov A.A. is 11,280 rubles. for a full month worked with a five-day working week.

June 2020 Petukhov worked out completely.

What salary will he receive in June?

Calculation:

The accrued wages should not be less than the minimum; Petukhov was accrued 11,280 rubles for the full month of June, which does not violate the established requirement.

Personal income tax = 11,280 * 13% = 1466.40.

Insurance premiums = 11,280 * 30% = 3384.

Salary in hand = 11,280 – 1466.40 = 9813.60.

That is, in fact, the employee will receive the amount of 9813.60 rubles, which is below the minimum wage, but this is not a violation, since the employee receives his salary after tax.

The procedure for obtaining a tax deduction if it is greater than personal income tax

If the tax deduction is greater than personal income tax, then in this case a citizen can:

- a citizen has the right to apply for half the tax deduction after 1 year (in this case it is possible to receive the remaining part). At the same time, it will include new calculations made in the tax period for the next year;

- the second method involves registering an IC by submitting an application to the tax office for the first part of the deduction. The second part can be completed through the employer. Thus, in the future you can receive compensation through your employer;

- the third method involves receiving a deduction exclusively through the employer. If a citizen has additional income that is subject to taxation, it will be processed through the Federal Tax Service.

Example:

The employee's salary for May amounted to 20 thousand 475 rubles. In turn, withholding in favor of personal income tax amounts to 2 thousand 662 rubles.

In June, the employee went on vacation, and the salary in this regard amounted to 2 thousand 300 rubles. Thus, the income turned out to be less than the deduction amount, and at the same time excessive deduction occurs. The employer may ask the employee to do the following. You can credit personal income tax in the next tax period or return it with prior notice.

Example of calculating deduction for children

Let's consider the first example, when the deduction amount exceeds the employee's income.

In January, employee Sidorov received a salary of 30,000 rubles. He has three minor children, so he is not subject to personal income tax:

(400 + 1400 + 3000 = 5800 rub.

For the first month the tax amount was:

(30000 – 5800) × 0.13 = 3146 rub.

The following month, employee Sidorov took leave without pay and did not work for almost the entire month. His salary was 3500 rubles. This income is less than its deductions, so the employee does not pay personal income tax for February. But it is worth remembering the cumulative total. Let's calculate the amount of deductions for these two months.

(30000 + 3500 – 5800 × 2) × 0.13 = 2847 rub.

The tax amount for January-February is 2847 rubles. Thus, there is an extra amount of personal income tax paid since 3,146 rubles were withheld from Sidorov during this period (January-February). The surplus is 299 rubles (3146 – 2847 = 299). The employer can carry this excess forward to the next tax period, and the employee will pay less tax. If for some reason the employee has not received back the overpaid personal income tax, then at the end of the year he can independently contact the local Federal Tax Service to receive the overpaid personal income tax.

legal information

First, you need to understand what a personal income tax deduction is and how it is calculated.

A tax deduction implies a payment to the municipal budget from the income (wages) of the taxpayer. The employer, according to the legislation of the Russian Federation, withholds no more than 13%, since this requirement is prescribed by Law 23 of the Tax Code of the Russian Federation.

The total withholding amount is divided into several categories:

- social insurance fund;

- pension fund;

- medical insurance in the Russian Federation.

IMPORTANT !!! In turn, a tax deduction (TD) allows an employee to return part of the taxes paid. It is worth noting that tax deduction payments are made exclusively to that category of citizens who are officially employed, i.e. their income is subject to taxation.

Thus, the following persons are recognized as taxpayers:

- citizens of the Russian Federation who are officially employed;

- citizens who are not residents, but receive income in the Russian Federation.

Now it’s worth figuring out which category of citizens has the right to apply for a tax deduction from their own income.

Citizens who have the right to a tax deduction for personal income tax:

- who spent their income on education for themselves and their children;

- who received an apartment or house at their own expense;

- who spent their money on expensive treatment;

- combat veterans;

- simple category of citizens.

It is also necessary to briefly consider each tax deduction category:

- The first category is general tax deductions. A general tax deduction is provided for children (1 thousand 500 rubles for the first child and 3 thousand rubles for subsequent children). It is provided to parents (mother and father), parents of spouses (grandparents), adoptive parents who are guardians. Disabled children, in turn, will receive at least 12 thousand rubles per month.

Example of calculating property deduction

The maximum amount of tax benefits of a property nature is 2 million rubles. According to the law, a citizen can return 13%, that is, 260 thousand. Every year, an officially employed citizen will receive a return of 13% of their income for the year. Those. At first, tax deductions will be deducted from your salary, but at the end of the year, when you contact the Federal Tax Service, the benefit will be returned. Let's look at an example.

In 2020, taxpayer Petrov purchased real estate - an apartment worth 3 million rubles. His monthly salary in 2020 was 45,000 rubles. For the year, Petrov paid income tax in the amount of:

45000 × 12 × 0.13 = 70200 rub.

Accordingly, Petrov will be able to return only 70,200 rubles for 2020. Petrov will have an unpaid benefit in the amount of 189,800 rubles, which will be returned over the next years. If Petrov’s annual income does not change, the benefit will be fully returned in 4 years. For three years he will receive 70,200 rubles, for the fourth year 49,400 rubles.