Unified form No. INV-11 - form and sample

INV-11 is a unified document used when inventorying deferred expenses.

We will tell you in our article what its specifics are and where you can download it. When is INV-11 used?

Features of filling out the document

Where to download form INV-11

Results

When is INV-11 used?

Using the INV-11 form, an act is drawn up in which the inventory commission records information about expenses of future periods - those that are actually incurred one-time, but are expensed over several periods (months, years).

The form of the document in question was approved by Decree of the State Statistics Committee of the Russian Federation dated August 18, 1998 No. 88. It is filled out in 2 copies. The first is sent to the accounting department, and the second remains at the disposal of the commission, which conducts the inventory. Representatives of the relevant commission, as well as the financially responsible person, sign both copies.

To fill out the INV-11 form, accounting records for account 97 and information obtained when checking this data during the inventory are used.

For information on the document establishing the subject, time frame for conducting the inventory and the composition of the commission carrying it out, read the article “Unified form No. INV-22 - and sample” .

Features of filling out the document

The act, which is drawn up in the INV-11 form, records:

- name of expenses of the future period;

- the total amount of relevant expenses;

- the date of occurrence of the relevant expenses and the period for their repayment;

- the amount of the estimated amount to be written off for each expense;

- the volume of write-offs already made and the balances of unwritten-off expenses as of the beginning of the inventory;

- the duration of the period between the inventory date and the moment expenses are incurred (in months);

- amounts to be written off as the cost of goods (per month or from the beginning of the year);

- the amount of the estimated balance of the relevant expenses, which is subject to repayment within the framework of a future period;

- amounts to be added or restored based on inventory results.

For information on the form used to reflect data on verification of settlements with counterparties, read the material “Unified Form No. INV-17 - Form and Sample” .

Where to download form INV-11

INV-11 act, corresponding to the format approved by Goskomstat, you can visit our website.

Download form INV-11

You also have access to a sample INV-11 form filled out by our experts.

INV-11

Results

Form INV-11 is an act reflecting the results of verification of amounts written off as expenses over several periods. The result of such a check may be an additional write-off for expenses or the restoration of amounts in expenses of future periods.

Source: https://nalog-nalog.ru/buhgalterskij_uchet/dokumenty_buhgalterskogo_ucheta/unificirovannaya_forma_inv11_blank_i_obrazec/

What is important to remember

- A financially responsible person cannot be a member of the commission.

- If accounting is carried out in a company using a special program, then the form can be printed immediately with the first nine columns filled out. Next, the commission members fill out the form themselves.

- The document is generated in two copies. The first is given to the accounting department, and the other remains with the members of the commission, and then it must be filed in a folder with all similar acts.

- The presence of spelling and other errors, as well as blots, in the act is not allowed.

- The document must be stored for at least 10 years.

https://youtu.be/62zb0J5vx94

Inventory report of future expenses (INV-11): sample filling, form, form

Standard forms of unified reporting help individual entrepreneurs and enterprises organize audit activities as part of a general inventory. Thus, form INV-11 is a table ready to be filled out with information obtained during the verification of the enterprise’s obligations to counterparties.

Carrying out an inventory in the direction consists of recalculating the data of future expenses, which are accumulated in account 97 in accounting.

The information obtained is compared with the data from the primary documentation.

Indicators in the relevant registers are used as documents confirming the actual existence of such costs or their consistent attribution to expenses in future periods.

What is an inventory act for deferred expenses (INV-11)

The functionality of the form consists of filling out the tabular part and subsequent registration to give the form legal significance. The register must be signed by the persons responsible for maintaining accounting records at the enterprise, staff inspectors and the manager.

The registration of receipt of expenses for future periods is shown in this video:

Concept and goals

The assets of an enterprise represent its main value. For this reason, the first persons to control such property are the responsible officials. The assets that are subject to monitoring during inventory activities include costs such as:

- Construction work expected in the future. Based on estimates and other documents, upcoming expenses for the purchase of materials and payment for the services of contractors are planned in monetary terms;

- Costs that cannot be classified as such based on the content of governing documents (classical PBU). In most cases, this category includes the costs of insuring employees, their property and cars. INV-11 will also include payment for licensing services and state fees;

- Software used by a company under a license agreement.

Standards in this area

The main governing document regulating the very form and procedure for its publication at the enterprise continues to be Resolution of the State Statistics Committee of the Russian Federation No. 88 of 1998. The set of unified reports provides recommendations for filling out and using the tabular part.

https://youtu.be/PQgdRFlMfSI

In their arguments when deviating from the form, accountants can refer to the specifics of the enterprise’s activities and the instructions of the Ministry of Finance of Russia PZ 10/2012. To prevent conflicts with regulatory agencies, it is recommended to secure the report used for inventorying expenses in future periods in the accounting policy album.

Filling out the act

A document ready for signature contains a sufficient number of fields in which the maximum amount of information can be reflected:

- Amounts that will be expensed in future periods, by item;

- Summary of relevant expenses;

- The date on which future expenses are expected to be incurred and the expected repayment period;

- Amounts planned for write-off of expenses that will be accrued;

- The period in months that will pass from the moment of approval of the inventory report to the date of occurrence of the corresponding expenses;

- Amounts to be written off to the cost of production for the month and from the beginning of the reporting year;

- Estimated indicators according to which adjustments will need to be made (additional write-off).

The completed act, in at least two copies, is submitted for approval to the members of the commission and then to the manager.

How to write off deferred expenses, see the video below:

Form

The standard act form is a two-page form consisting of a tabular and affirmative part. The number of sheets can be increased if it is necessary to reflect a large number of items in the enterprise nomenclature.

When drawn up, the affirmative part of the form gives the form legal significance. Based on such a document, it is possible to generate reporting information for requests, as well as hold responsible the relevant officials who are found guilty of negligence or theft of the organization’s property. All participants in the inventory bear joint responsibility for the quality of the internal audit.

Instructions

First of all, you must fill out the required details.

- The name of the organization, classifiers and other fields can be filled in automatically when the form is displayed from automated software systems.

- If the company does not have these, you can fill out the required fields once and save the form for later use.

- The composition of the commission is filled out on the basis of a target or installation order for the company.

- The composition of assets is taken from the indicators of account 97.

Forms and samples

Forms of audit documents are available for download here.

In order to apply the form for your enterprise, it is best to use a standard approved by the legislator. This will eliminate distortions and claims from inspectors. There may also be problems when downloading the act via electronic communication channels.

Sample of filling out INV-11

Who fills it out and signs it?

In practice, before conducting an inventory, an act is issued by the company’s accounting department. He returns there after serving the commission. The act is signed by all participants in the process, including the responsible designer and the head of the enterprise.

Future expenses using the example of OSAGO in 1C will be shown in the video below:

Source: https://uriston.com/kommercheskoe-pravo/buhgalteriya/vneooborotnye-aktivy/inventarizatsiya/inv-11.html

Inventory report of deferred expenses sample filling

Situations where a company's expenses constitute a balance sheet item; future expenses are clearly defined by legislative provisions on accounting.

But in some cases, the management and accounting department of the enterprise independently decides to include the costs incurred as deferred expenses (FPR).

Such a balance sheet item is also subject to an annual inventory; based on the results of this, the INV-11 form is filled out, which will be discussed in our editorial office.

The procedure for carrying out an inventory of BBP

Accounting for future expenses of the enterprise is carried out on synthetic account 97. Taking into account the characteristics of economic activity, this account amounts to the following expenses:

- payment for certificates and licenses;

- for the purchase of licensed software;

- contributions to construction;

- contributions for the activities of a self-regulatory company.

The purpose of the BPO inventory is to compare the amount in account 97 with the information reflected in the primary documentation. An inventory of deferred expenses is carried out mainly during the annual inspection of inventory balances. The procedure for conducting a BPR audit is regulated by Order of the Ministry of Finance of the Russian Federation No. 49.

During the audit, the commission checks the accuracy of the information reflected in the primary documentation, controls the write-off of expenses from account 97, and determines the need for additional write-off or return of excessively written off amounts of expenses.

For example, an enterprise made a payment for licensed software, the operation of which is planned for 1 year, and included the costs of its purchase against future costs; in this case, the costs are written off during this year, but not later. The BBP audit is aimed at determining the correctness of business transactions with account 97.

Based on its results, the commission generates the INV-11 statement; the sample form presented on our website will allow accountants to avoid mistakes when drawing up the document.

Features of the statement design

Future expenses are considered to be one-time cash paid by a company for the acquisition of an asset, the operation and maintenance of which is planned for several months or years. To generate INV-11, an example of filling can be found on our website, you need account balances 97 and all the information obtained when checking the primary documentation for the acquired assets.

https://youtu.be/Yts-YBhEeRA

The statement must be drawn up in two copies, one of them is given to the responsible employee who keeps track of account 97, and the second remains with the accountant. When filling out this form, the following information is required:

- determination of the type of RBP;

- the amount of future costs;

- the date of occurrence of the RBP and the deadline for their repayment;

- the amount to be written off for each type of BPO;

- the amount of the write-off and the amount of the balance of unwritten-off costs as of the start date of the audit;

- the period from the occurrence of future costs to the date of the inspection (calculated in full months);

- the amount of costs subject to write-off or restoration (this amount is established based on the results of the audit and is written down in the INV-11 statement - an inventory report of future expenses).

The general requirements of the Methodological Instructions apply to the preparation of the document. Thus, the finished form of the act is endorsed by the signatures of all committee members, corrections and blots are not allowed, the totals for the amount and number of named RBPs are indicated on each page of the document, and must reflect clear and concise information.

Source: https://LawCount.ru/otchet/inv-11-akt-inventarizatsii-rashodov-budushhih-periodov/

Inventory of 97 accounts in 1s upp how to create

Attention

The start of the write-off is April, the end is May. I enter the document Write-off of deferred expenses for April. No movements are generated in the registers at all. SCP 1.2.14.1. What am I doing wrong, please tell me. Advertising space is empty BuyBed 1 - 05/05/08 - 18:53 Probably not all data is filled out in the reference book. Amount, division, accounts, cost item.

Also look at the SALT on your account, maybe you don’t have the amounts there (it was written off a long time ago or something) disk-2008 2 - 05/05/08 - 19:44 Yes, it seems like all this is there.

Form inv 11 – Lawyer

Where to download the INV-11 form of the INV-11 act, corresponding to the format approved by the State Statistics Committee, you can on our website. Download form INV-11 You also have access to a sample form INV-11 completed by our experts.

INV-11 Results Form INV-11 is an act reflecting the results of verification of amounts written off as expenses over several periods.

The result of such a check may be an additional write-off for expenses or the restoration of amounts in expenses of future periods.

- name of expenses of the future period;

- the total amount of relevant expenses;

- the date of occurrence of the relevant expenses and the period for their repayment;

- the amount of the estimated amount to be written off for each expense;

- the volume of write-offs already made and the balances of unwritten-off expenses as of the beginning of the inventory;

- the duration of the period between the inventory date and the moment expenses are incurred (in months);

- amounts to be written off as the cost of goods (per month or from the beginning of the year);

- the amount of the estimated balance of the relevant expenses, which is subject to repayment within the framework of a future period;

- amounts to be added or restored based on inventory results.

For information on the form used to reflect data on verification of settlements with counterparties, read the material “Unified Form No. INV-17 - Form and Sample”.

Inventory report of deferred expenses form n inv-11

It is not necessary to draw up an additional comparison statement if discrepancies are identified in the act, since it includes the functions of such a statement. The employee, who has checked the data given in the inventory act, indicates his position, writes his last name, and signs.

Attention

Such acts must be kept for at least 10 years. An example of filling out form INV-11 Inventory report of deferred expenses. First sheet (click to enlarge) Act of inventory of future expenses.

Second sheet (click to enlarge) Act of inventory of deferred expenses - filling out and form Evaluate the quality of the article.

Act of inventory of future expenses. form inv-11 (filling sample)

Inventory report for deferred expenses (sample)

Modern companies, as a rule, keep records using special programs; in this case, the inventory report is prepared with their help. The columns in which information is entered on the basis of accounting are filled in immediately, after which the prepared act is printed for the members of the commission.

Inventory act form of the unified form INV-11 To reflect the results of the reconciliation, the standard inventory act form INV-11, approved by the State Statistics Committee of Russia back in 1998 (Resolution No. 88), is usually used.

Inventory report of deferred expenses (inv-11 form)

OKPO, division, type of main activity according to OKVED;

- information about the document establishing the procedure for conducting the inspection - name (the desired option is selected from those proposed, the rest are crossed out), number and date (copied from the document);

- information about the inventory - the timing (dates of the first and last day of the procedure) is taken from the administrative document defining the procedure for the reconciliation ⊕ timing of the cash register inventory in 2018;

- details of the act - number and date (numbering is affixed in accordance with the rules established by the organization, may contain digital, alphabetic designations, as well as signs; the date corresponds to the actual day of registration).

To fill out the INV-11 act, the data from account 97 is used - its debit and credit turnover.

Unified form n inv-11

INV-11 “Act of inventory of future expenses” Resolution of the State Statistics Committee of the Russian Federation dated August 18, 1998 N 88 (as amended on March 27, May 3, 2000) Format: MS-Excel :: Size: 7 KB Used for inventory of future expenses periods.

It is drawn up in two copies by the responsible persons of the inventory commission based on the identification of balances of amounts listed in the corresponding account from the documents, signed and one copy is transferred to the accounting department, the second remains with the commission. Column 4 indicates “Total (initial) amount of expenses” - the total amount of costs (expenses) incurred in a given reporting period or not completely written off in previous periods, but relating to future reporting periods.

Blank form No. inv-11. act of inventory of deferred expenses

What needs to be done from March 19 to 23 The human brain is capable of remembering huge amounts of information. But even people with excellent memories sometimes forget important things.

Indeed, with today’s fast pace of life, there are often too many such things to do, especially for an accountant. Our weekly accounting reminders will help you not to forget anything and fulfill your obligations to regulatory authorities on time.

Individual entrepreneurs should not rush to pay 1% contributions for 2020. Firstly, because from this year the deadline for paying such contributions has been postponed from April 1 to July 1. Accordingly, 1% contributions for 2020 must be transferred to the budget no later than 07/02/2018 (July 1 – Sunday).

How to fill out form inv-11 (filling sample)?

After filling out the INV-11 act, one copy must be submitted to the accounting department, whose employee will check the correctness of the inventory form.

The INV-11 form includes indicators characteristic of inventory lists (acts) and matching statements, that is, if inconsistencies are identified, they do not need to be transferred to matching statements.

Discrepancies and conclusions from them are shown directly in the INV-11 form.

Form inv-11

As a rule, such reconciliation is carried out before the preparation of annual financial statements during the annual inventory. The rules for conducting inventory of BPO are regulated by orders of the Ministry of Finance.

To carry out the inventory, a commission is created, which cannot include persons financially responsible for the property being inspected. According to clause 3.35 of the order of the Ministry of Finance of the Russian Federation dated June 13.

95 No. 49, the inventory commission, based on a documentary check, determines the amount that should be reflected in the RBP account in accordance with the accounting policy adopted by the company.

The correctness of the write-off of costs in the reporting period is checked. Based on the results of the audit, the amounts to be written off or the amounts written off in excess are determined.

Blank form inv-11

The signatures of financially responsible persons are also affixed, who, by signing the act, confirm that the information contained in it corresponds to reality, these persons have no complaints or claims to the information presented. After completing all the necessary manipulations with the inventory report INV-11, it is transferred to the accounting department for verification.

INV-11 forms Below we have provided a sample of filling out INV-11, prepared according to this unified form. The RBP inventory report reflects:

- name of the company and the structural unit being inspected;

- details of the order on the basis of which the inventory is carried out;

- inventory timing;

- name, amount, date of occurrence of deferred expenses;

- information regarding the write-off of these expenses;

- inventory results, including identified amounts to be added or restored.

The BPO inventory report is drawn up in two copies.

One for storage by the inventory commission, and the second for transfer to the accounting service. This act is signed by all members of the inventory commission, as well as the financially responsible person.

Source: https://advokat-dtp.com/blank-inv-11/

Inventory of rbp in 1s 8 3

Depending on what receipt document is on hand (the price is “with VAT”, or “Without VAT, or “Including VAT”) the choice depends:

- If the price of the purchased GWS in the document is already indicated with VAT, then you must select VAT in the amount in the Document Prices parameters so that the 1C 8.3 program does not re-charge VAT on the cost of the GWS.

- If in the incoming document the prices are indicated without VAT, but the supplier and your organization are VAT payers, then you must select VAT on top so that the 1C 8.3 program automatically charges VAT on the cost of the goods and services.

- If we purchase goods without VAT, then there is no need to go to the Document Prices.

Write-off of deferred expenses is carried out in three ways:

- monthly, within a certain date range;

- daily (meaning calendar days), within a certain date range;

- in an arbitrary (special) way.

With ERP. By the way, in older versions of 1C 8.2, inventory takes place according to the same principles, only the appearance of the interface differs.

The general inventory scheme in the 1C program is as follows:

- Creating and filling out an inventory document. It is used to fill in actual data on the presence or absence of items in the warehouse. The document does not make any entries.

- If a shortage of goods is detected, it must be written off using the document “Write-off of goods” (less often, “Retail sales report”).

- If there is an excess, it is accounted for using “Goods Receipt“.

Let's look at these documents in detail.

INV-11

Form INV-11 was approved by Decree of the State Statistics Committee of August 18, 1998 No. 88, and is a unified form used in cases where an organization carries out an inventory of FPR (deferred expenses).

Inventory of deferred expenses is an internal audit carried out on the basis of an order or instruction issued by the enterprise.

Based on the results of its implementation, the head of the organization must make a decision to write off additional funds for BP expenses, or, if a violation is detected, to restore them, if during the inventory the commission reveals accounting violations.

The requirements for filling out an act according to this form is a mandatory norm when the inventory commission records documented verified information on BP expenses - already incurred virtually at a time, but related to expenses that will follow during one or more upcoming periods.

The act is filled out by members of the commission created for the inspection.

One copy of the completed act must be transferred to the accounting department for subsequent processing, and the second copy must be registered in the accounting documents of the commission that conducted the inventory and filed in the Inventory Check Reports folder.

In order to avoid mistakes, the members of the commission, who upon inspection will draw up INV-11, must be provided with a sample of completion and explanations on the BPR in advance.

The certificate's witnesses are the members of the commission who filled out the INV-11, as well as the person bearing financial responsibility.

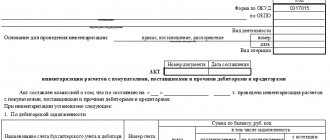

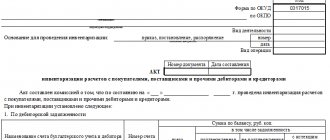

The unified form INV-11 has four informative elements:

- title, containing information: about the installation data of the enterprise,

- about the order on the basis of which this inventory is carried out;

- containing information about the date and conduct of the inventory;

- reflects factual information about the types and amounts of expenses;

- containing the conclusions and signatures of the commission members, as well as responsible and officials.

It should be remembered that the Inventory Report can be drawn up in any form, but with the mandatory details of the approved document. Therefore, it is easier to use the approved form of the INV-11 form, which you can download below, so that the compiled document serves as the basis for entering information into the General Ledger.

When members of the commission fill out an act, only factual information obtained during the inspection, as well as accounting data according to Article 97, can be used.

The inspection report drawn up in the INV-11 form must include the following information:

- name or type of expenses, indicating the code;

- total amount - indicated for each (or specific) type of expense as of the starting date;

- indicator for the amount intended to be written off separately for each type of expense;

- the amount to be written off to the RBP at the time the inventory begins;

- the amount of amounts that are subject to write-off to the cost of products or goods (for the reporting period or the previous period from the beginning of the financial year);

- the actual volume of funds already written off, as well as the balances subject to write-off, at the time of the inventory check;

- date of occurrence and repayment terms of expenses;

- the duration of the period (in months) during which it is planned to repay the balance of the debt;

- the balance of the amount that, according to the inventory check, is subject to addition in subsequent periods (or restoration).

In order to avoid mistakes, before drawing up and signing an inventory report for deferred expenses, you can see a sample of filling out the document below.

Source: https://mari-a.ru/v-pomoshh-predprinimatelyu/inv-11

Menu

How to take inventory of 97 accounts in 1 from 8

Each type of expense can be separated into a group of elements of the “RBP” directory, and each expense is its final element.

The RBP element card in 1C Accounting 8.3 contains the necessary details that allow you to display assets in the balance sheet and write them off as expenses for the current period.

After excluding a separate line for BPR from the balance sheet, this type of asset can be reflected in different lines, therefore, for the correct classification of BPR in the balance sheet lines, the attribute “Type of asset in the balance sheet” is used. Its values are fixed in the configuration; the user can select one of the predefined types:

https://youtu.be/TipRxgQY95A

Depending on the rule for recognizing expenses in accounting, one or another recognition method is selected:

The method affects the calculation of the amount of write-off of the RBP for the current expenses of the reporting month.